![]()

![]()

![]()

![]()

- Interim Update 20th May 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

There will be a 'V'

recovery...sort of

The rebound from the H1-2020

plunge into recession probably will look like a 'V', at least initially.

This is not because conditions will become positive as quickly as they

became negative, but because conditions got so bad so quickly that charts

of economic statistics such as industrial production and retail sales will

appear to make a 'V' bottom in Q2-Q3 of this year. However, the 'V' won't

mark the start of a genuine recovery.

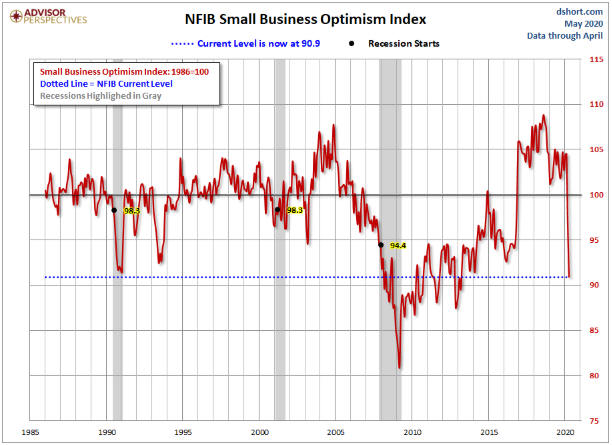

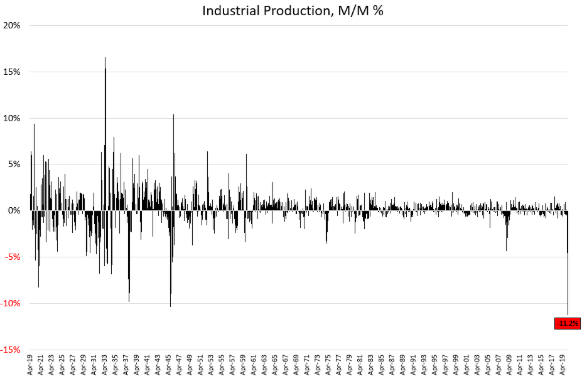

The following charts show

what we mean by "got so bad so quickly".

The first chart shows that

within the space of three months the Small Business Optimism Index

collapsed from a level that indicated a high level of optimism to one of

the lowest levels in the 34-year history of the index. The only other

decline of this magnitude occurred during the 2005-2008 period and took

more than two years.

The second chart shows that Industrial

Production has just registered its largest month-over-month decline in at

least 101 years. By this measure, even the worst months of the Great

Depression were not as bad as April-2020.

Source:

dshort

Source:

Hedgeye

There are thousands of people who have lost their

businesses -- in some cases, businesses that they spent the bulk of their

adult lives building -- over the past two months as a result of the

lockdowns. These people probably are feeling angry and/or devastated.

However, we get the impression that the vast majority of people have

accepted the lockdowns with equanimity. They haven't taken to the streets

to protest the economic destruction that has been wrought by their

political overlords. Instead, they have shrugged off the most rapid

decline in industrial production in history and a sudden rise in the

unemployment rate from below 4% to above 20%. How is this possible?

It's possible only because the government and the Fed have showered

the people with money. The money that has been created out of nothing is

acting like pain-suppressing medication. In effect, the government and the

Fed have administered anaesthetic so that the patient felt no pain as

vital organs were removed. Without this anaesthetic, the populace would

not have remained docile as its basic rights were cancelled and its

economic prospects were greatly diminished.

Money, however, is

just the medium of exchange. It facilitates the division of labour*, but

it does not constitute real wealth. For example, if every current dollar

were instantly replaced by ten dollars, there wouldn't be any additional

wealth. The point is that the government and the Fed cannot make up for

the decline in real wealth caused by the lockdowns by providing more

money. All they can do is change the prices of the wealth that remains.

There will be a 'V' shaped recovery, but due to the destruction of

real wealth stemming from the lockdowns the rising part of the V is bound

to be much shorter than the declining part of the V. This will lead to a

general realisation that life for the majority of people will be far more

difficult in the future than it was over the preceding few years.

Returning to our medical analogy, eventually the anaesthetic will wear off

and the patient will have to start dealing with the consequences of having

lost a kidney, a spleen, a lung and half a liver.

*In the absence of money, a tomato farmer who needed some dental work

would have to locate a dentist who needed a few crates of tomatoes.

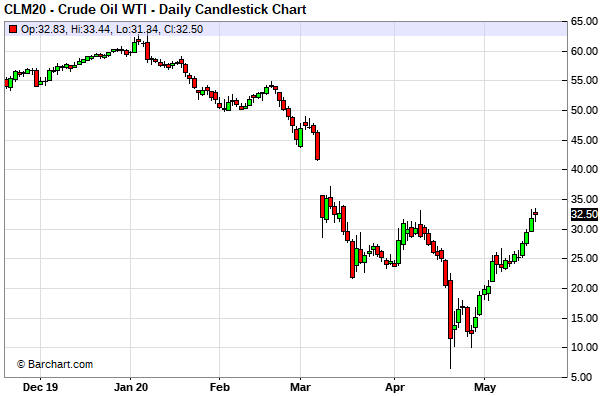

The June oil

contract expires without incident

At around this time last month

the May-2020 oil futures contract expired with a bang. On expiry day the

price plunged by an incredible 350% to NEGATIVE $38/barrel. It was

probably the most dramatic day in the history of oil trading. It was

caused by some traders getting themselves into the position where they

could be forced to take delivery of physical oil at a time when oil

storage space was in such short supply that its price had gone through the

roof.

It was feared that something similar would happen leading up

to the expiry of the June-2020 oil futures contract, but the following

daily chart shows that this fear proved to be unfounded. The June-2020 oil

futures contract expired with a whimper on Tuesday of this week.

There is no doubt that it is much easier and less costly to store oil now

than it was a month ago. Also, it is clear that anyone trading June-2020

oil from the long side and who didn't have ready access to oil storage

learned from what happened in April and exited before the delivery period.

Due to the tightening supply situation the December-2020 oil futures

contract could trade as high as $40 prior to the start of the next

meaningful decline, but the short-term risk/reward is neutral due to the

risk that demand will not rebound as quickly over the next few months as

many speculators seem to be expecting. Adding to the risk side of the

equation is that there has been another regional virus-related lockdown in

China.

*This is the top of the short-term

target range we mentioned in earlier commentaries. At the moment this

contract is trading near $35, which is the bottom of our short-term target

range.

Platinum blasts through

resistance

The platinum price crashed in

March and briefly traded below $600/oz. We wrote at the time that this

constituted a big over-reaction, because the price was more than fully

discounting a large decline in demand for the metal but failing to account

for a large decline in the supply of the metal.

Fast forwarding to

the current situation, in the latest Weekly Update we noted that the

platinum price remained within the trading pattern of the preceding month,

but that Friday's price action suggested that an upside breakout followed

by a quick move to resistance in the high-$800s was coming. As it turned

out, the market performed even better than anticipated and the price broke

through resistance like a sharp knife through warm butter.

The

platinum market is now almost 180 degrees from where it was in mid-March

and is in a similar short-term position to the stock market, in that it

appears to be reflecting too much economic-recovery optimism.

The Stock Market

Soon after the stock market

bottomed in March we mentioned that 2800-2900 was a reasonable target for

the rebound that was just getting underway. The top of this target range

was reached in mid-April.

We subsequently mentioned that the SPX's

rebound could extend as far as the 200-day MA near 3000, which it almost

has done. However, our opinion over the past few weeks has been that while

some additional upward progress was possible, the short-term risk/reward

had become decidedly skewed towards risk.

One plausible scenario

involved the SPX trading sideways within a roughly 10% range over the

ensuing few months as short-term economic/medical pluses (optimism

associated with the return to work and COVID-19 medication progress) were

counteracted by the realisation that long-term economic damage has been

done, but at the same time there was a realistic chance that the SPX would

drop back to test its March low. In other words, a small amount of

additional reward potential versus substantial risk.

A portion of

the small additional reward potential was used up during the first three

trading days of this week, while the warnings about short-term downside

risk became louder.

The most important new signs of increasing risk

are:

1) The new multi-month high achieved by the SPX on Wednesday

20th May was accompanied by a lower high in the NYSE Advance-Decline Line

(ADL). Refer to the following daily chart for the details. This is a

bearish divergence/non-confirmation.

The 3-day MA of the equity put/call ratio (the blue line on the

following chart) has dropped to only 0.47, which reflects considerable

bullishness on the part of the 'dumb money'. This sentiment indicator has

almost returned to its January-February extreme, despite the intervening

economic disaster.

The above bearish signs don't predict an immediate top, they just

suggest that technical- and sentiment-related negatives have been added to

the fundamental negatives. Therefore, don't be lulled by this week's new

rebound high for the SPX into thinking that the market is now less risky.

It is more risky.

This is a time to be looking for selling

opportunities and/or tightening stops and/or hedging in some way. Unlike

the senior US stock indices, some commodity-related stocks and ETFs still

have significant short-term upside potential. For example, the Oil

Services ETF (OIH) could be about to complete a basing pattern (see chart

below). However, the entire market looks vulnerable.

We think the

best-case scenario involves a multi-month period of range trading by the

SPX. This scenario is plausible and potentially would allow the relatively

cheap commodity-related stocks/ETFs to make catch-up moves, but, as

mentioned earlier, a return to the March low is also plausible.

Gold and the Dollar

Gold

The

US$ gold price tested its April high on Monday of this week and then

reversed. Monday was an outside down day, but it didn't negate last week's

upside breakout. It would take a daily close below $1716 to do that and a

daily close below $1680, or a weekly close below $1690, to signal a

short-term trend change from up to down.

The surge in the gold/SPX ratio from below to well above its 200-week

MA (the blue line on the following chart) in March of this year confirmed

that a gold bull market began in Q3 of 2018. However, until gold/SPX

exceeds its March high there will be a risk that the March-2020 stock

market crash caused the gold/SPX ratio to generate a false signal. Our

concern is that the only other false signal by the gold/SPX ratio over the

past four decades resulted from the October-1987 stock market crash.

Gold Stocks

The HUI broke above long-term

resistance at 286 last Friday and consolidated above resistance during the

first three days of this week.

A daily close below 280 would warn

that last week's breakout was a false signal. Putting it another way, at

this stage it would be reasonable for traders to assume that last week's

breakout was the genuine article as long as the HUI holds above 280 on a

daily closing basis.

Despite last Friday's upside breakout by the HUI, with regard to our

gold stock portfolio we are looking for opportunities to take some money

off the table. Our preference is to scale out of positions into strength

rather than attempt to catch the top or sell after the price has confirmed

a downward trend reversal, especially when dealing with the junior gold

stocks. The scaling process obviates the need to get the timing exactly

right and leaves us with 'core' exposure in case the market runs away to

the upside.

We probably won't buy new insurance in the form of GDX

put options until there is preliminary evidence of a top. At the moment, a

daily HUI close below 280 would be the preliminary evidence.

The Currency Market

Over the first three days of

this week the Dollar Index (DX) moved from the top to the bottom of its

short-term contracting range. It will have to close below 98.7 or above

100.6 to break out of this pattern.

The pattern suggests that

there will be at least a 2-point move in the direction of the breakout,

which is not something that we will be interested in trading.

We

continue to expect that the next tradable (substantial, multi-month) move

in the DX will be to the downside.

Over the past three months the Australian dollar (A$) traded in synch

with the SPX. Like the SPX it crashed during the final week of February

and the first half of March, rebounded to the 50-day MA by mid-April,

consolidated for a while and then extended its rebound to slightly below

the 200-day MA this week. The correlation suggests that the A$ is

vulnerable to stock market weakness.

We remain bullish with regard

to the A$'s intermediate-term prospects. This is mainly because the

currency should benefit from the higher commodity prices that will

materialise over the coming 2 years thanks to the combination of

profligate money creation and reduced commodity supply outside Australia.

In the short-term we are concerned about the potential effects on

A$ demand of a sizable stock market decline.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() The

Tanker Trade

The

Tanker Trade

On 8th May Euronav (EURN), the owner of a

fleet of oil tankers that had just reported a huge increase in quarterly

earnings and dividend, was added to the TSI List as a trade with an

expected duration of 3-9 months. Our aim at that time was to add a second

tanker stock (probably Frontline (NYSE: FRO)) to the TSI List within the

ensuing few weeks.

Frontline (FRO)

reported its Q1 results on Wednesday

20th May. As was the case with EURN, FRO announced a huge increase in

earnings and dividend.

FRO reported quarterly earnings of

US$0.84/share and declared a quarterly cash dividend of US$0.70/share.

This means that FRO shares are being priced at less than 10-times a single

quarter's earnings and that the stock is yielding almost 10% based on a

single quarter's dividend.

As was also the case with EURN, the

stock market's reaction to FRO's spectacular earnings was minimal.

The stock market clearly expects that day rates for tankers will

plunge during the second half of this year, which is certainly possible

due to the intersection of supply cuts and a modest increase in demand. In

fact, there are signs that tanker rates have peaked. For example, FRO's

20th May press release contained this quote from its CEO: "The tanker

market has corrected downwards in recent weeks and faces pressure in the

short term, both from production cuts and inventory draws...".

However, we continue to like the tanker trade because a pessimistic

forecast for tanker day rates appears to be fully discounted by current

share prices. This suggests that the risk is low and that future surprises

are more likely to be positive than negative.

We may add FRO to

the TSI List in the future as part of our tanker trade, but at this stage

we will stick with EURN. If we do add FRO it probably will be prior to 3rd

June, which is when the stock goes ex-dividend.

Battening down the hatches

Battening down the hatches

In the 23rd March

Weekly Update we explained why we would start applying trailing stop

losses (TSLs) to the stocks and ETFs that go into the "Trading Positions &

ETFs" section of the TSI Stocks List. Here's part of what we wrote at that

time:

"We generally don't use protective stops in our own

trading/investing (we use other methods to manage risk, including the ones

mentioned above as well as buying insurance in the form of put options

from time to time). Also, we generally don't apply any risk management

techniques to the TSI Stocks List, primarily because it's a list of

speculating/investing ideas and not a recommended portfolio. We have

decided that from now on, however, unless stated otherwise we will apply a

20% trailing stop (based on daily closing prices) to stocks and ETFs that

go into the "Trading Positions & ETFs" section of the Stocks List. This

will force us to focus on securities that offer reasonable liquidity and

to be more disciplined.

The 20% trailing stop will be applied to

all future inclusions in the "Trading Positions & ETFs" section of the

Stocks List, but at the moment it only applies to the PPLT (Physical

Platinum ETF) position added last week and the U.TO (Physical Uranium

Fund) position added via today's report."

Due to the

increasing short-term risk for the overall market as well as the potential

for additional short-term gains in some commodity-related stocks/ETFs, we

now will apply TSLs to other TSI trading positions. In each case, the

initial stop will be based on the highest closing price of the past two

months. The stop subsequently will be adjusted upward if this price is

exceeded.

The details are shown in the following table.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.barchart.com/

![]()