![]()

![]()

![]()

![]()

- Interim Update 21st October 2015

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The SEC drives

Money-Market Funds (MMFs) into Treasury debt and other investors into gold

As

explained by giant US fund manager Fidelity last week, in July-2014 the U.S.

Securities and Exchange Commission (SEC) issued new rules for the further

regulation of MMFs that are to be implemented by October-2016. Under the new SEC

rules, non-government MMFs may impose a redemption fee or temporarily halt

redemptions if fund liquidity falls below certain limits. However, MMFs that

hold only government and agency (Fannie and Freddie) debt securities will not be

affected by the new rules. Therefore, some Fidelity MMFs that previously

invested in senior corporate loans and secured debt securities are transitioning

to government funds. The transition is expected to be complete by December of

this year.

Fidelity is not the only fund manager that is responding to the coming new rules

by changing the holdings of some MMFs from non-government to government

securities. It is currently expected that around $1T of assets will be affected.

In other words, the new rules are expected to boost the demand for short-dated

US Treasury/Agency securities to the tune of about 1 trillion dollars and reduce

the demand for short-dated corporate debt by the same amount.

We doubt that this was a deliberate ploy to underpin the Treasury market,

because the demand for Treasury securities was/is already abundant. It's more

likely that a shift of this magnitude from corporate to government debt is an

unintended consequence of the new rules.

Intentional or not, a likely effect will be a steeper US yield curve over the

coming 12 months. The reason is that the rule changes will put additional

downward pressure on interest rates at the short end but probably won't affect

interest rates at the long end, causing long-term interest rates to rise

relative to short-term interest rates. This means that the rule changes are

likely to make the interest-rate backdrop more bullish for gold.

The Stock Market

The US

The SKEW Index gets 15 minutes of fame

The SKEW Index, which is calculated from out-of-the-money S&P500 put options,

rises to higher levels as investors become more fearful that there will be a

"black swan" event such as a stock market crash in the near future (a rising

SKEW reflects an increasing desire to hedge against extreme downside over the

coming 30 days). It has been published by the CBOE for more than 4 years, but

until the past month we had never seen it mentioned anywhere. Over the past

month, however, we've seen it mentioned in articles from several different

sources. SKEW is suddenly popular! But is it useful?

The answer is no. SKEW values have been all over the place and have not

consistently predicted anything in the past. For example, in August of this year

the SKEW rose as the stock market fell sharply, but there was no anticipation of

the market decline in the performance of SKEW (the rise in the SKEW was a

reaction to the price decline). Furthermore, there have been many times when

SKEW rose sharply and the market subsequently did very little.

SKEW is also not useful as a contrary indicator, because sometimes it does rise

just prior to significant declines.

As far as we can tell, its values are almost random.

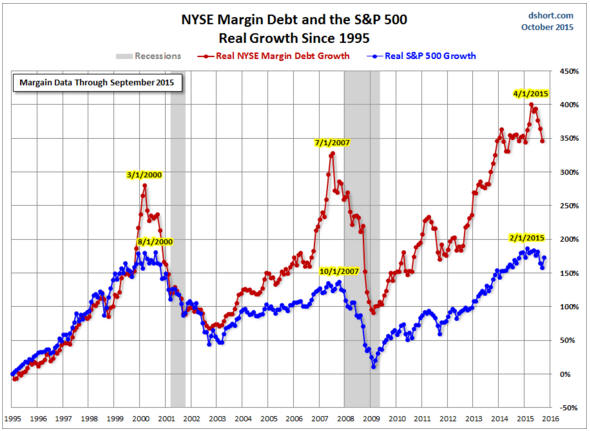

NYSE Margin Debt points to a bear market

Regardless of how far into 'nosebleed territory' it moves, leverage in general

and margin debt in particular is bullish for asset prices as long as it

continues to increase. It's only after market participants begin to scale-back

their collective leverage that asset prices come under pressure. That's why the

pronounced downturn in NYSE Margin Debt from its April-2015 all-time high should

be taken as a warning that a US equity bear market got underway in July.

The reversal in NYSE Margin Debt from its April-2015 high is illustrated by the

following chart from Doug

Short. Notice the similarity of this year's Margin-Debt reversal to the

reversals that occurred in early-2000 and mid-2007.

Due to the stock-market rebound, Margin Debt will probably increase in October.

If so, a subsequent decline to below the September low would be the final nail

in the bull market's coffin.

As things currently stand, a resumption of the trend towards greater leverage

cannot be ruled out. It just appears to be very unlikely.

Current Market Situation

We doubt that the S&P500 Index (SPX) will breach or seriously challenge its 24th

August low over the remainder of this year, but a tradable decline will probably

soon begin. It could therefore soon be appropriate for short-term traders to

establish bearish positions.

A rise by the SPX to the 2050s would make the short-term risk/reward

sufficiently bearish to warrant a bearish speculation. However, in the latest

Weekly Update we noted that a better -- because it would allow for tighter risk

management -- entry point would be provided by a multi-day pullback followed by

a rise to a slightly lower high. A third approach would simply be to start

averaging into a bearish speculation immediately with the initial

risk-management plan of exiting if the SPX makes a new multi-month high after

early-November.

To give you a rough idea of what we are expecting to happen over the weeks

ahead, we'll return to the 2011 Model. We've been using the H2-2011 price action

as a guideline for what to expect this year, and although we do not think that

2016 will be similar to 2012 we will continue to use 2011 as a model as long as

it continues to work.

The first of the following charts shows the SPX during 2011 and the second of

the following charts shows the SPX since the beginning of this year. The

similarities are obvious. If the SPX now does exactly what it did at the same

stage in 2011 it will rise sharply to the vicinity of its 200-day MA over the

coming few days before embarking on a decline that quickly retraces at least

half of the preceding multi-week rebound. However, it isn't reasonable to rely

on the SPX tracking the 2011 path so precisely, which is why we have outlined

three different ways of entering a short-term bearish speculation.

Argentina

There will be a presidential election in Argentina on 25th October, with a

second round to be held on 22nd November if the first round is not sufficiently

decisive. As a result of this election Argentina will end up with a new

president, but the victor will almost certainly be from the same party as the

current president. This probably means that Argentina is not going to get a

respite from economically-destructive policy-making over the years immediately

ahead.

One of Argentina's biggest economic problems is inflation of both the monetary

kind and the price kind, with the latter being a consequence of the former.

Argentina's government admits to "price inflation" of around 14%, but

non-government sources indicate that the actual pace of purchasing-power loss is

close to double the official number. The dramatically faster rate of "price

inflation" quoted by non-government sources is probably in the right ballpark

since it is consistent with the country's rapid pace of money-supply growth.

The stock market can benefit from rapid monetary inflation, even when the

monetary inflation is causing a blatant "price inflation" problem. The reason is

that stocks are claims on real assets. In a high-inflation environment it is

therefore usually much better to bet against bonds than against stocks.

Prior to the past few months Argentina's stock market was holding up quite well,

even when its performance was measured in US$ terms. In fact, although the top

half of the following chart shows that the Global X Argentina ETF (ARGT) made

new 2-year lows during September-October, the bottom half of the same chart

shows that ARGT has essentially gone nowhere (in an interesting way) over the

past two years relative to emerging-market equities in general. In other words,

relatively bad policy-making hasn't yet led to relatively bad performance by

Argentina's stock market.

This is more evidence that stock-market performance is often a poor indicator of

economic performance.

Gold and the Dollar

Gold

The US$ gold price has pulled back from last week's high. In the process it has

dropped below its 200-day MA and important lateral support/resistance at $1170,

thus negating the recent upside breakout. What does this tell us about the

future?

It tells us very little. Although last week's upside breakout has been negated,

the price action over the past 5 trading days currently has the look of a

routine consolidation. There is not yet any evidence of a short-term trend

reversal from up to down.

Gold has short-term lateral support in the mid-$1150s defined by the

late-September high and short-term support in the low-$1150s defined by the

20-day MA. Once the 20-day MA rises to meet lateral support in the mid-$1150s,

which is something that will happen in the next two days, the mid-$1150s will

become trend-defining support. In other words, a daily close below this support

would then signal a short-term trend reversal from up to down.

As an aside, confirmation of a trend change often doesn't happen until after the

price has moved a significant distance in the direction of the new trend. This

is why it can often make sense to do some selling after the market in question

has become short-term 'overbought' but before there is any evidence that the

rally has ended.

At this stage the odds favour the 'routine short-term consolidation' view, in

which case the gold price won't close below the mid-$1150s before resuming its

rally and rising to a new multi-month high. That being said, we do not expect

that gold will do any better over the next couple of months than rise to the

$1220s. That is, we think that the maximum realistic short-term target for the

US$ gold price is only about 3% above last week's high.

Gold Stocks

Like gold, the HUI has pulled back over the past 5 trading days. Also like gold,

there has been nothing in the HUI's price action to suggest that the pullback is

anything more serious than a routine consolidation within a short-term upward

trend. Note that in the gold-mining sector, short-term consolidations within

upward trends often last 5-8 trading days.

A minor positive divergence between gold and the HUI over the past three trading

days adds some weight to the 'routine consolidation' view. We are referring to

the fact that on Wednesday 21st October, the US$ gold price closed below

Monday's low while the HUI closed above Monday's low.

At this stage a rise by the HUI to the low-150s remains a realistic short-term

possibility. However, the following comment from the email sent to subscribers

early this week is worth repeating:

"Bear in mind...that although last week's high for the HUI was 10% below the

level that we considered both a likely and a maximum short-term upside target,

the two most important gold-stock ETFs reached the lower ends of the upside

target ranges mentioned in recent TSI commentaries. Specifically, GDX reached

the lower end of the $17-$18 range and GDXJ reached the lower end of the

$23.50-$24.00 range. Also, GDXJ touched its 200-day MA before pulling back

sharply over the past two trading days."

The chart displayed below shows that GDXJ not only touched its 200-day MA last

week, but also touched its channel top. In effect, GDXJ has already reached the

HUI equivalent of the low-150s.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

![]()