![]()

![]()

![]()

![]()

- Interim Update 22nd April 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Relax, the Fed is going

to make everyone "whole"

Last week, a highly paid (we

assume) JP Morgan analyst opined:

"When it comes to market

developments, we believe that the Fed's action last Thursday represents a

pivotal moment in this crisis. Powell's statement included that "we will

continue to use these powers forcefully, proactively, and aggressively

until we are confident that we are solidly on the road to recovery" and

probably the most important, historic statement, "We should make them

whole. They did not cause this." This crisis is different from any other

in recent history in that it was not caused in any way by businesses or

investors. Unhindered by moral hazard, the response of fiscal and monetary

authorities is and will continue to be unprecedented, with the goal of

essentially making everyone 'whole.' We believe the significance of this

development is underestimated by markets, and this reinforces our view of

a full asset price recovery, and equity markets reaching all-time highs

next year, likely by H1. Investors with focus on negative upcoming

earnings and economic developments are effectively 'fighting the Fed,'

which was historically a losing proposition."

Well, if moral

hazard was the only thing that prevented the Fed from acting in the past

to eliminate everyone's losses, then why has the Fed never bothered to

eliminate poverty? After all, not every poor person is in that situation

due to having done something wrong. In particular, none of the children

living in poverty are to blame for their predicament.

Taking a

broader view, if it is possible for the central bank to make everyone

"whole", then why are some countries poor? These countries have central

banks that are capable of doing what the Fed is now promising to do.

The problem, of course, is that the central bank cannot add real

wealth to the economy. It cannot produce anything of real value. All it

can do is conjure money and credit out of nothing, thus setting in motion

countless exchanges of nothing for something and distorting the price

signals upon which markets rely. This is a recipe for more poverty and

generally lower living standards in the long term.

At some point

during the second half of this year, the release of pent-up demand as

restrictions are removed and people go back to work, combined with the

flood of new money generated by the Fed, could make it seem as if there

has been a 'V' bottom in the economy and that the entire recession lasted

only about four months. This could enable the SPX to return to within 10%

of its February-2020 all-time high before year-end. However, the price

distortions that have been and will be caused by the effort to make

everyone "whole" will prevent a sustainable recovery.

The deluge of

new money will boost asset prices and the prices of life's necessities,

but many businesses that closed their doors during March of 2020 will

never re-open and many people who lost their jobs will remain unemployed

(and thus dependent upon government handouts). Also, many of the people

who do end up with jobs will find that their real incomes have fallen,

because there will be an excess supply of labour and the currency's loss

of purchasing power will be reflected to the greatest extent in the prices

of things that are in relatively short supply. For the majority of people,

therefore, the post-shutdown economy will never be as good as the

pre-shutdown economy, not despite the Fed's efforts but largely because of

them.

The Oil Glut

The greatest 'long

squeeze' ever?

Normally it is only the shorts that can be

squeezed, but early this week there was a dramatic 'long squeeze' in the

oil market.

When you take a non-leveraged long position, your

maximum loss is usually 100%. The reason is that most prices can't go

below zero. On Monday of this week, however, the price of oil for May-2020

delivery in the US futures market closed at NEGATIVE $38/barrel. It had

ended the preceding trading day at around $18/barrel, so in the space of a

single trading day the loss on a non-leveraged long position in May-2020

oil futures was more than 300%.

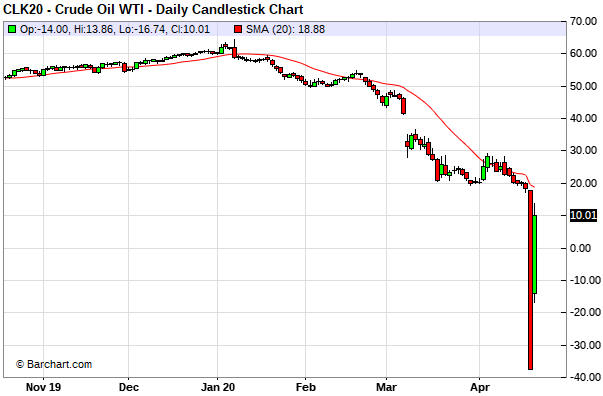

Here's the daily chart showing

Monday's extraordinary price collapse and Tuesday's partial recovery in

the May-2020 oil contract. Note that the contract expired on Tuesday 21st

April.

With the benefit of hindsight it isn't hard to understand how the oil

price could drop well below zero for a short period. The situation arose

because anyone still long the May contract at that time could have been

forced to take delivery, but for all intents and purposes there was no

storage space. If you have entered a contract that would require taking

immediate delivery of oil but you have nowhere to put the oil, then to

avoid being in breach you would have to pay whatever it took to get out of

the contract. On Monday 20th April, that effectively involved paying

someone as much as $38/barrel to take oil off your hands.

At this

stage only the May-2020 contract in the US oil futures market has traded

below zero. However, Monday's dramatic performance by the May contract

obviously scared speculators in later contracts, because on Tuesday the

June-2020 contract collapsed from above $20 to as low as $6.50 before

recouping part of its loss.

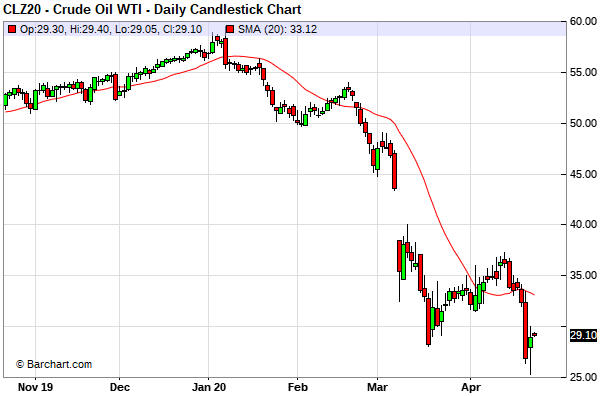

The following daily chart shows that

even the December-2020 contract, which is 6-7 months from its delivery

period, took a tumble. At the end of last week it was in the mid-$30s, but

over the first three days of this week it plunged to the mid-$20s before

rebounding to $29.

Companies that profit from the glut

Increasing

oil demand after the virus-related restrictions are removed and decreasing

oil supply in response to the low price eventually will eliminate the oil

glut. However, that likely will take at least 6 months and could take more

than a year. In the meantime, the companies that sell oil storage will

have unusually high profit margins. This includes tanker companies such as

Euronav (EURN), Frontline (FRO) and Teekay (TNK).

Rather than

transporting oil from one part of the world to another, the owners of

VLCCs (Very Large Crude Carriers -- ships that can store about 2 million

barrels of oil) can now get paid for storing oil at daily rates that are

multiples of what they were getting paid a year ago. For example, the

average daily rate for a VLCC over the past 10 years was

US$30,000-$40,000, but, thanks to the oil glut, deals are now being done

at around US$200,000/day. US$200K/day is not a sustainable rate, because

it amounts to about $3 per month ($36 per year) per barrel. However,

US$70K-$100K/day could be achievable over at least the remainder of this

year.

The upshot is that the demand for tankers is going through

the roof due to the desperate need to find somewhere to put the excess

oil, and, as a result, the companies that own tankers should generate

substantially higher earnings over the quarters ahead.

The stocks

of the large tanker companies have done relatively well this year. For

example, the following chart shows that EURN is almost flat year-to-date,

which is good compared to most stocks. However, the stock market appears

to be underestimating the earnings that these companies will deliver over

the next 12 months.

Buying tanker stocks to profit from the oil glut was described by

Harris Kupperman

as one of the best trades in decades. Kupperman discusses the trade in

some detail in the podcast at

https://www.curzioresearch.com/this-will-be-the-greatest-trade-in-decades/,

beginning at around the 22-minute mark.

It would be reasonable to

start averaging into a position in tanker stocks with the aim of holding

for 6-12 months. The upside potential over this period is at least 100%,

versus downside risk that could be limited to 20%-30% using a trailing

stop. Be aware, though, that these stocks are 'overbought' on a short-term

basis and could 'correct' with the broad market over the weeks ahead.

We are going to participate in this trade in our own account and may

add a tanker stock (probably EURN, the largest independent tanker company)

to the TSI List within the next two months.

The natural gas

cycle low, revisited

In January we wrote about the

potential for the US natural gas (NG) market to make a cycle low during

the first quarter of the year. We updated our view a week ago when we

wrote:

"The NG price didn't bottom during the first quarter,

but it's possible that a bottoming process got underway in March and that

the cycle low occurred on 2nd April. A daily close above US$2.00 would be

preliminary evidence that at least a short-term bottom is in place."

The spot NG price currently is in the $1.80s, but the following daily

chart shows that the June-2020 futures contract has edged above $2.00.

It's possible that the current up-move will be limited by the 200-day

MA in the $2.10-$2.20 range. If so, a subsequent pullback to near the

50-day MA followed by a rally that took out the April high would confirm

an upward trend reversal.

Peyto Exploration and Development

(PEY.TO), our favourite NG producer, has gained more than 150% since its

March low and has fully retraced its February-March crash. It is still a

long way below its 12-month high, but buyers near the recent low should

consider taking some money off the table. This is partly due to the risk

of a sizable short-term decline in the broad stock market.

With the

stocks of well-managed companies such as PEY, it often makes sense to

trade around a core position. This involves doing some buying during the

periodic purges and some selling during the ensuing surges, all the while

maintaining significant ('core') exposure.

The Stock Market

The S&P500 Index (SPX) reached

its 50-day MA late last week and pulled back over the first three days of

this week.

The pullback from last week's high has been too shallow to date to

confirm that a short-term top is in place and that a significant

correction is underway. Therefore, as things stand right now there is a

decent chance that the SPX will move a little higher before commencing a

meaningful decline.

We view the short-term risk/reward as decidedly

bearish, though, mainly because we perceive short-term upside potential of

no more than a few percent. Perhaps the SPX will gain enough additional

ground to achieve a solid break above its 50-day MA -- and thus get

'everyone' convinced that the old bull market has resumed -- before

beginning its next tradable move to the downside.

There is no

guarantee that it will, but if the SPX breaks above last week's high

within the next several days it will create another good opportunity to

establish bearish speculations or hedges via the vehicles mentioned in the

latest Weekly Update. Furthermore, if the SPX is able to achieve a more

solid break above its 50-day MA than it managed last Friday then it would

be reasonable to view a subsequent daily close below the 50-day MA as

evidence of a downward trend reversal.

Before leaving the US stock

market it is worth mentioning that the Dow Transportation Average (TRAN)

may again be leading to the downside. The upper section of the following

daily chart shows that TRAN's post-crash rebound peaked (to date) nine

trading days ago, and the lower section of the chart shows that the

TRAN/SPX ratio just made a new low for the year. This is evidence that an

intermediate-term trend reversal from down to up has not occurred.

Gold and the Dollar

Gold and Silver

At the end of last week, the US$ gold price (basis the June-2020

futures) was testing lateral support at $1690-$1700. The test continued

during the first two days of this week and included a spike below the

20-day MA, after which there was a sharp rise.

The fact that

support held means that nothing has changed. There is short-term downside

risk stemming from speculator positioning in the futures market, but the

fundamentals are bullish and the price action has not yet signalled a

short-term reversal from up to down.

Like the US$ gold price, the US$ silver price tested its 20-day MA on

Tuesday. However, silver's overall performance since the March low

continues to have the look of a countertrend rebound. As previously

advised, we think that silver will avoid a test of its March low, but a

decline within the next couple of months to the $13.50-$14.00 area would

not be a surprise.

Gold Stocks

The HUI closed at a new multi-year

high on Wednesday 22nd April and in doing so created the first positive

divergence between the gold sector and the bullion market -- in this case,

a higher high for the HUI in parallel with a lower high for gold -- since

last November. It was an upside breakout, but upside breakouts are not

reliable signals when they occur in markets that were stretched to the

upside prior to the breakout.

A daily close below 240 by the HUI

would signal a downward trend reversal. Until/unless that happens, trend

followers could assume that the trend is up.

20 points (about 8%)

above Wednesday's close is long-term resistance defined by the 2016 top,

which originally was our target for the intermediate-term rally that got

underway last June. Perhaps this old target will be reached within the

next few days. If so, the market will have taken a very circuitous route

to its destination.

As previously advised, we are viewing short-term strength in the gold

sector as an opportunity to do some selling/hedging. At the same time, we

recognise the sector's extraordinarily bullish fundamentals and therefore

intend to maintain substantial 'core' exposure.

Hopefully there

will be a good opportunity to remove hedges and do some new buying within

the next several weeks.

The Currency Market

There isn't much happening in the currency market, although the

short-term daily chart of the Australia dollar (A$) is comment worthy.

The following chart shows that the A$ poked its head above its 50-day

MA early last week before pulling back. This means that the A$ is in a

similar position to silver and the SPX. Each of these different markets

experienced a strong A-B-C rebound from a crash low during the third week

of March to some sort of high near the 50-day MA last week.

It isn't surprising that the A$'s performance over the past several

weeks has been similar to the SPX's performance, given that the A$ tends

to be positively correlated with global growth expectations. That silver

would be trading in synch with the A$ and the SPX is more difficult to

understand. Over the long-term silver tends to trade in synch with gold,

which is the ultimate counter-cyclical asset, but silver has an industrial

(pro-cyclical) demand component that appears to be holding sway at the

moment.

Anyway, it's a good bet that the A$ will continue to trend

up and down with the SPX over the coming month or two. This probably means

that its next significant move will be to the downside, although like the

SPX it could make a new multi-week high before reversing course.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.barchart.com/

![]()