![]()

![]()

![]()

![]()

- Interim Update 22nd July 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Commodities

The Emerging Copper

Shortage

There has been a spectacular rise in the copper

price from its March-2020 low. In fact, after trading at a 4-year low and

coming close to trading at a 10-year low in March, the copper price is now

close to a 2-year high and is comfortably above the level at which it

ended last year. It's just as well that central banks aren't able to

counteract the powerful deflationary forces in the world. Imagine how fast

the copper price would have risen if they could*.

Speculation has played a role in the copper rally of the past four

months. This is evidenced by speculators in Comex copper futures having

gone from being net-short by about 40K contracts near the March-2020 price

low to being net-long by about 40K contracts today. However, speculator

buying is being driven by the legitimate concern that the supply situation

in the copper market is tightening.

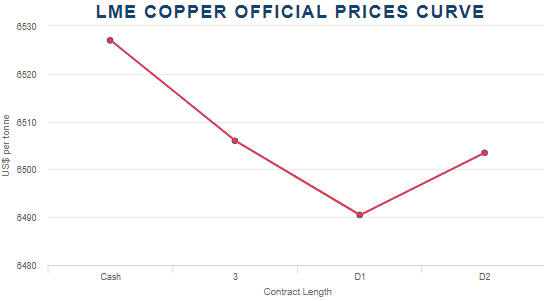

The evidence that supply is

tightening in the copper market includes the following chart from the

London Metal Exchange (LME) web site. This chart shows that the spot

copper price is above the 3-month price and that the 3-month price is

above the December-2021 price, that is, it shows that the copper market is

in backwardation. This is an unusual circumstance that points to the

current supply of the physical commodity being low relative to the current

demand.

The evidence also includes the social distancing measures that have

been implemented at copper mines throughout Chile, where about 30% of the

world's copper is produced. Over the past few months the large Chilean

copper mines have managed to sustain production at their pre-COVID levels

and in some cases have even increased production by a small amount,

despite having smaller workforces due to the need for social distancing.

This was made possible by NOT doing routine maintenance. The general

failure to do maintenance work during Q2-Q3 of this year should result in

lower production at the world's largest copper mines late this year and

during the first half of next year.

We remain intermediate-term

bullish on copper, but we expect a sizable pre-election correction.

*Hopefully the sarcasm is obvious.

The Platinum Breakout

In the 1st July Interim

Update we reiterated our view that the platinum price was in the early

stages of a cyclical advance driven by reduced mine supply, massive

monetary inflation and the metal's low relative valuation. We also

mentioned that it might have just completed a short-term correction.

The platinum price has since risen from the US$830s to the US$950s and

in doing so has broken above an obvious lateral resistance level.

Breaks above obvious resistance levels aren't reliable indicators of

future performance. Consequently, we almost never buy immediately after an

upside breakout. Instead, we prefer to buy pullbacks to support and view

upside breakouts as the reward for having had the good sense and fortitude

to buy the preceding weakness.

The Stock Market

Unprecedented

We've had to use the word "unprecedented" an unprecedented number of

times over the past five months.

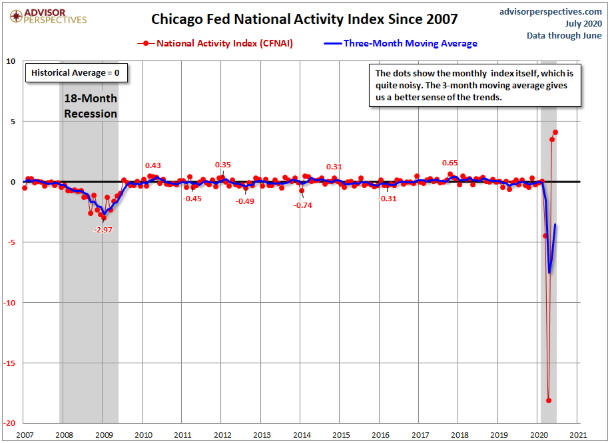

The following chart of the

Chicago Fed's National Activity Index (CFNAI) illustrates the extent to

which the recent past deviates from the norm. The CFNAI is a composite of

85 monthly indicators and is constructed so a zero value equates to the US

economy growing at its historical trend rate. Negative values indicate

below-average growth and positive values indicate above-average growth.

When the government locks-down the bulk of the economy, naturally

there's a collapse in economic activity. When the government then showers

the populace with money, naturally the initial result is a dramatic

increase in economic activity (since the negative effects of rampant money

creation and deficit spending come much later). These actions have pushed

many economic indicators into uncharted territory.

Source:

dshort

Strange bedfellows: The mega-cap tech stocks and

the gold miners

The following chart shows that since the

beginning of the 'coronacrisis' there has been a strong positive

correlation between the NASDAQ100 Index (NDX) and the gold mining sector

(represented on the chart by the HUI). At first glance this seems

downright weird, but there is a reasonable explanation for the

correlation.

The explanation is that the lockdowns didn't hurt, and in some cases

even boosted, the prospects of the mega-cap tech stocks (e.g., Amazon,

Microsoft, Alphabet (Google), Facebook, Apple, Netflix) that dominate the

NDX. The economic disarray caused by the lockdowns and the ensuing efforts

to mitigate the short-term economic pain also boosted the prospects and

therefore the investment appeal of companies that mine gold.

We

suspect that the positive correlation between the NDX and the HUI will be

maintained for at least three more months, with both reaching important

tops within the next several weeks and then 'correcting' together.

Current Market Situation

The S&P500 Index (SPX)

has edged above its early-June high to a new 5-month high. It is up on the

year and less than 4% below its all-time high, so everything must be fine.

Obviously everything is not fine, but money supply matters.

It's

interesting that the NYSE Advance-Decline Line (ADL), which is shown in

the lower section of the following chart, didn't confirm this week's new

multi-month SPX high. The non-confirmation will be significant (bearish)

if it persists.

In essence, what the US stock market is showing is the effect of

currency depreciation. This time around the effect won't be limited to the

financial markets, however, because although the Fed is busily monetising

bonds, the government is busily ensuring that a lot of money goes to the

general public. As a result, over the next 12 months the effects of the

monetary inflation should be most obvious in the prices of commodities,

goods and services. If so, there will be downward pressure on

price/earnings (P/E) ratios in the stock market, leading to relatively

poor performance by the 'growth' stocks that are dominating at the moment.

In a nutshell, "stagflation", which is coming soon if it isn't here

already, leads to lower growth premiums and generally lower valuations in

the stock market. The stocks of commodity producers and other companies

that profit from the "inflation" should do well, but that's because of a

rising 'E' not a rising 'P/E'.

An implication is that the Fed's

ability to boost the stock market's valuation may have run its course.

That could be why the SPX's performance has been laboured since

early-June. It isn't going down, but it is struggling to make additional

headway.

We continue to think that the short-term risk/reward is

bearish for the senior US stock indices, but with sentiment remaining

mixed it's possible that the market will hold up for a few more weeks.

Gold and the Dollar

Gold

In

the latest Weekly Update we wrote that gold's recent price action had the

look of a consolidation within a short-term upward trend, the implication

being that an extension of the short-term upward trend was likely. Over

the past two days the US$ gold price broke above its early-July high to

new multi-year highs, so we are getting the expected extension.

Unlike the silver market (discussed below), the gold market isn't immersed

in an upside blow-off. At least, it isn't yet. Therefore, at this stage

there isn't a reason to expect anything more bearish than a routine

short-term correction in the gold market.

Silver

Silver took off like a scalded cat over

the past few days. We mentioned in the latest Weekly Update that a test of

long-term resistance in the $21-$22 area, or about $2 above last week's

close, was possible prior to the next substantial correction. The price

surged to this resistance area on Tuesday and blew past it on Wednesday.

With resistance in the low-$20s having been overcome, how high can the

price go before it reaches a multi-month top?

In situations such as

this, the 'when' question (what is the likely time of the top?) is a lot

easier to answer than the 'where' question (what is the likely price level

of the top?). The answer to the 'when' question is: Soon. Due to the

silver market having entered upside blow-off mode, the next multi-month

top could occur as early as this week and should occur before the end of

next week.

When silver tops it usually doesn't leave us guessing

for long. The tops that follow rapid rises usually are signalled by either

a large single-day price decline or a dramatic intra-day price reversal.

Gold Stocks

The gold mining sector

(represented on the following daily chart by the HUI) has extended its

upward trend and is now slightly 'overbought'. Like gold and unlike

silver, it isn't immersed in an upside blow-off, so at this stage there

isn't a reason to expect anything more bearish than a routine short-term

correction.

Further to the discussion in last week's Interim Update, it continues

to look like the gold sector is headed for a multi-month top between

early-August and early-September. If a 2-3 week correction begins within

the next few days then the scales will tip in favour of an early-September

peak, but if the market presses higher with only 1-2 day interruptions to

the advance then an earlier peak will be likely.

The

Currency Market

The Dollar Index

(DX) tests critical support

The DX extended its decline over

the first three days of this week and is now testing support defined by

its March-2020 low. This support is critical, because a monthly close

below it would remove almost all remaining doubt that the US$ has

commenced a cyclical bear market.

We expect that the DX will

rebound soon and therefore avoid a solid break below its March-2020 low

for now. However, a downside breakout is likely within the next few

months.

The euro has taken out its March-2020 extreme already, but, as is the

case with the DX, confirmation requires a monthly close beyond the March

extreme and that might have to wait until later this year.

The Canadian dollar (C$) versus the

Australian dollar (A$)

Over the past few months we have

devoted a fair amount of commentary space to explaining and reiterating

our 1-2 year bullish outlook for the A$, but we have said very little

about the other senior commodity currency (the C$). Our most recent

comment about the C$ was in the 1st July Interim Update, when we repeated

our view that the A$ would have an upward bias over the coming 1-2 years

and mentioned that the C$ also should do well, albeit not as well as the

A$.

In the 13th July Weekly Update we listed five reasons to expect

a major rally in the A$ over the coming 1-2 years, the most important of

which was/is the coming rise in commodity prices. This is bullish for the

A$ due to the strong positive correlation between this currency and the

general commodity-price level. It is bullish for the C$ for the same

reason.

The positive correlation between the C$ and the S&P Spot

Commodity Index (GNX) is clearly evident on the following chart.

We expect that both the A$ and the C$ will be elevated by a cyclical

bull market in commodities, but why is it likely that the A$ will

outperform the C$?

The main reason is that the C$ tends to be weak

relative to the A$ during multi-year periods when the Dollar Index is

weak. This is probably because of the closeness of the Canadian and US

economies.

The following chart compares the C$/A$ exchange rate

with the Dollar Index (DX) and illustrates the point we are trying to

make. The chart shows that there isn't a reliable relationship in the

short-term, but the big trends in the C$/A$ rate tend to be the same as

the big trends in the DX. If the DX has commenced a big trend to the

downside, then so, in all likelihood, has the C$ relative to the A$.

Trends in the exchange rates of the major currencies are

self-limiting. This is because both extreme currency strength and extreme

currency weakness prompt central bank and government intervention designed

to stop the trend. Consequently, even if our analysis is totally correct

there are limits to how strong we should expect the A$ to become.

Based on what happened over the past two decades, the downside limit for

C$/A$ appears to be in the low-to-mid 0.90s. In other words, the A$ could

trade 5%-8% above the C$ before the current cycle is over, but it isn't

reasonable to expect much more than that.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Alkane

Resources (ALK.AX) began trading 'ex' the Australian Strategic

Materials (ASM) spinout on 21st July. The stock opened A$0.06 lower and

then recovered to end the day unchanged, which could mean that the market

is valuing ASM at A$0.30/share (5 times 0.06, since initially there will

be one ASM share for every five ALK shares) and that subsequently there

was sufficient strength in the gold mining sector to offset the effect of

the ASM distribution.

Alkane

Resources (ALK.AX) began trading 'ex' the Australian Strategic

Materials (ASM) spinout on 21st July. The stock opened A$0.06 lower and

then recovered to end the day unchanged, which could mean that the market

is valuing ASM at A$0.30/share (5 times 0.06, since initially there will

be one ASM share for every five ALK shares) and that subsequently there

was sufficient strength in the gold mining sector to offset the effect of

the ASM distribution.

We won't know until after ASM shares begin

trading on 30th July. What we do know is that A$0.30/share would equate to

a market cap of about A$36M for ASM, which would be very low given the

potential value of ASM's Dubbo Specialty Metals project. We almost

certainly will be buyers of ASM shares on the market if they are available

near A$0.30 when listed on 30th July.

We have added ASM to the

"Trading Positions" section of the TSI List assuming an initial price of

A$0.30 and an effective dividend to ALK shareholders of A$0.06/share.

However, we'll adjust the initial ASM price (and the associated ALK

dividend amount) if ASM doesn't trade close to this level at some point

during its first few days as a listed company.

Also, we have

removed ALK from the TSI List. The reason is that the stock is now trading

well above our estimate of fair value. The company potentially will grow

into its current valuation due to drilling success at the Boda target and

expansion of the Tomingley Gold Operation, but at this time the

intermediate-term risk/reward is not sufficiently attractive.

The

stock is up by about 120% since the beginning of this year and more than

500% since its inclusion in the TSI List back in 2016. Along the way there

have been many buying and selling opportunities. ALK served us well.

We had planned to add Resolute Mining (RSG.AX), a

mid-tier gold producer with mines in West Africa, to the TSI List as a

trading position in today's report, but on Wednesday 22nd July the stock

price broke upward from a basing pattern and gained 13%. This has worsened

the short-term risk/reward by enough to prevent us from 'pulling the

trigger'. However, we will add RSG to the TSI List if it trades at A$1.26

within the next two weeks.

We had planned to add Resolute Mining (RSG.AX), a

mid-tier gold producer with mines in West Africa, to the TSI List as a

trading position in today's report, but on Wednesday 22nd July the stock

price broke upward from a basing pattern and gained 13%. This has worsened

the short-term risk/reward by enough to prevent us from 'pulling the

trigger'. However, we will add RSG to the TSI List if it trades at A$1.26

within the next two weeks.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.lme.com/

http://bigcharts.marketwatch.com/

![]()