![]()

![]()

![]()

![]()

- Interim Update 22nd November 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Another Uranium Update

There's a lot happening in the

uranium sector and therefore another brief update is warranted, although

the main purpose of today's uranium commentary is to address an error in

the latest Weekly Update.

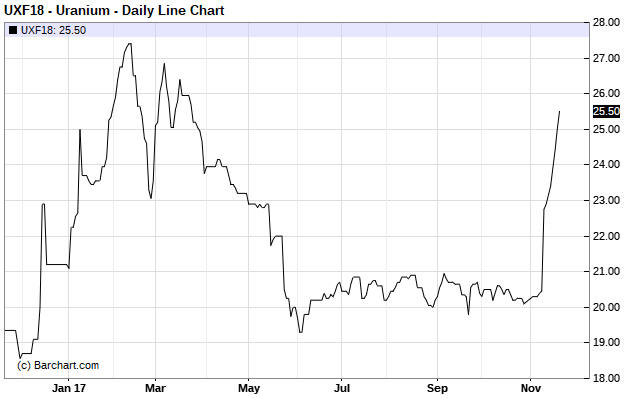

In the Weekly Update, we wrote: "Despite

the market for physical uranium remaining moribund and the uranium price

remaining near $20/pound, uranium mining equities continue to catch a bid.

In doing so they are continuing to follow a path that is very similar to

the one taken at around this time last year." The data source we were

using hadn't updated the uranium price for more than a week and so we

missed the fact that there had been a significant bounce. Based on the

January-2018 uranium futures contract, a daily chart of which is presented

below, the uranium price ended last week at $25.00 following a quick-fire

rally of more than 20% over the preceding days. As a consequence, the

premium to net asset value at which the Uranium Participation Fund (U.TO)

was trading was nowhere near as large as we thought*.

The recent

sharp rise in the uranium price actually increases the similarity between

this year and last year, although this year's surge started about a month

earlier than last year's.

In the Weekly Update we revisited the similarity between the

performance of Energy Fuels (UUUU) during the final two months of last

year and its performance since this year's late-October bottom. We wrote:

"If UUUU continues to follow a similar path to last year then it will

soon peak near US$1.90, after which it will pull back to the vicinity of

its 50-day MA in the low-$1.50s before surging anew."

Despite

the price of the January-2018 uranium futures contract pulling back from

$26 on Tuesday to $24.50 at the close of trading on Wednesday 22nd

November, UUUU broke through resistance at US$1.90 on Wednesday in

sympathy with another sharp sector-wide rise in uranium-mining share

prices. As a consequence, the initial rebound from the low is now even

stronger this year than it was last year. However, a correction to the

50-day MA could still happen.

We don't know that a decline to the 50-day MA will occur over the

weeks ahead. What we do know is that a decline to the vicinity of the

50-day MA for UUUU and most other uranium stocks will be required to

create the second good set-up for new buying, the first having been

created by the late-October plunge to support defined by last year's low.

*We wrote that the premium was about 28%, but

it was probably 8%-10% then and is probably about 13% now. 13% is too

high, but it isn't ridiculous.

Collapsing

Stories

A few weeks ago we discussed the

extraordinary enthusiasm for story stocks. These are stocks that have

attracted massive demand based on an interesting story and have been bid

up to the point where the stock price bears no resemblance to what the

underlying business is currently worth. In some cases the underlying

business will develop in a way that justifies the stock price, but in the

vast majority of cases the stock price will eventually collapse.

The prices of two of the story stocks given as examples in our earlier

discussion have recently collapsed, although their stock-market valuations

are still absurdly high relative to the companies' assets. We are

referring to Garibaldi Resources (GGI.V) and HIVE Blockchain Technologies

(HIVE.V). As illustrated by the following daily charts, GGI's stock price

has dropped by more than 50% over the past 3 trading days and HIVE is down

by more than 50% from the high that was reached 14 trading days ago.

Of these two stocks, HIVE has less remaining downside risk. As long as

the 'crypto mania' continues, HIVE's cryptocurrency-mining datacentres

will have significant value. GGI's exploration-stage base-metal assets,

however, are possibly worthless under any conditions.

The Stock Market

The bull market is

valuation driven

Recently there has been a lot of talk in

the financial press about the equity bull market being earnings-driven,

but this is only true if you don't look back further than the past 9

months. In reality, the bullish trend has been primarily driven by

valuation, meaning that the main driver of higher prices has been a rising

market-wide price/earnings (P/E) ratio.

As evidence we present the

following chart of the S&P500's P/E ratio. This chart shows that the P/E

ratio has risen from a low of 13 in October-2011 to a current level of

24.7. This is a 90% increase. Over the same period the S&P500 Index (SPX)

rose from 1100 to 2600, or by 136%. The implication is that two-thirds of

the gain in the SPX from its October-2011 bottom has been due to investors

being prepared to pay a higher earnings multiple for stocks. To put it

another way, in terms of effect on share prices the willingness of

investors to pay a higher multiple of earnings for the same shares has

been twice as important as earnings growth.

Like almost everything else in the financial markets, the P/E ratio

doesn't go up or down in a straight line. It therefore isn't surprising

that the major upward trend in the P/E ratio that began back in October of

2011 contains numerous pullbacks, including a pullback over the past two

quarters. The pullbacks can be caused by a falling SPX or rising earnings.

The most recent pullback was caused by rising earnings, with the most

significant earnings improvement happening in the energy sector.

That the current bull market has been valuation-driven is not in any way

abnormal. The fact is that all long-term equity bull markets are

valuation-driven. In other words, for the most part equity bull markets

are NOT about earnings growth; they are about people being prepared to pay

more for a dollar of earnings.

The most unusual aspect of the

current long-term equity bull is that it began at a medium valuation

rather than a low valuation. It therefore reached 'over-valuation

territory' quite early in its life, but this didn't stop it or even slow

it down.

Current Market Situation

The

dip-buyers remain in control in the US stock market and last week's

tentative bearish signal was quickly negated. There is a litany of reasons

to be concerned that a 10%-20% down-move will soon begin, but the price

action has not yet signaled a reversal.

Turning to Europe, a week

ago we wrote:

"The EURO STOXX 50 Index (STOX5E), the European

equivalent of the Dow Industrials Index, has just dropped for 8 days in a

row and suffered a quick peak-to-trough decline of about 5%. There's a

good chance of a rebound over the next few days, but it's likely that the

2017 peak is in place and that a 1-3 month (or longer) correction is

underway."

The expected rebound began immediately and may have

already run its course.

Gold and the Dollar

Gold

The

gold market has experienced strange price action over the past several

days. There has been the greatest intra-day volatility in months and minor

breakouts in both directions with no follow-through in either direction.

In particular:

1) There were intra-day reversals in opposite

directions on Tuesday and Wednesday of last week.

2) After an

uneventful Thursday there was a solid break above the recent trading range

last Friday.

3) Friday's price action looked bullish, but on Monday

of this week the gold price more than fully retraced Friday's gain and

closed below its 20-day MA.

4) Monday's price action looked

bearish, but the bulk of Monday's loss was recouped over the course of

Tuesday and Wednesday.

The indecisive price action could be due to

the opposing forces of a fundamental tailwind and a sentiment headwind.

The gold price should be rallying in response to a fundamental backdrop

that is unequivocally bullish at this time, but rallies can't get any

traction because the speculating community is already net long in a big

way.

Our expectation is the same now as it was when we wrote the latest

Weekly Update. We think that a multi-week rally to the mid-$1300s (at

most) is underway.

Gold Stocks

The

gold-mining sector, as represented on the following chart by GDX, held up

well in the face of Monday's sharp decline in the gold price and then

moved up to resistance at $23.00 over the ensuing two days. A daily close

above $23.00 would break GDX above its 200-day MA and confirm that a

short-term rally was underway.

As noted in the latest Weekly Update, if a short-term rally is

underway in the gold-mining sector and this year's cyclical pattern

continues then the next 1-2 month top could occur as soon as

early-December or as late as early-January. More specifically, a

continuation of the cyclical pattern would result in an early-December top

followed by a sharp decline to an early-January bottom OR a rally to an

early-January top.

The Currency Market

The

Dollar Index (DX) has now retraced about half of its September-October

rally, which means that the decline from the early-November peak is still

within the bounds of a normal correction. At the same time, it has closed

below its 50-day MA and unless it rebounds on Friday -- the US financial

markets being closed on Thursday for Thanksgiving -- it will end the week

below its 20-week and 200-week MAs. Ending the week below these weekly MAs

would have bearish implications.

The main reason to believe that the DX's early-November peak will not

turn out to be the ultimate peak for the rally that began in September is

related to sentiment. The sentiment situation recently became very

supportive for both the Yen and the Swiss Franc, but for all intents and

purposes the DX is the reciprocal of the euro and the speculating

community remains lopsidedly bullish about the euro's prospects. This

limits the euro's short-term upside potential and the DX's short-term

downside potential.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() In

an email sent to subscribers on Monday (20th November) we added Resolute

Mining (RSG.AX) to the TSI Stocks List as a short-to-intermediate-term

trade.

In

an email sent to subscribers on Monday (20th November) we added Resolute

Mining (RSG.AX) to the TSI Stocks List as a short-to-intermediate-term

trade.

It's possible that RSG will become available at a

significantly lower level early next year in sympathy with a final

sector-wide decline (the price chart would point to a target of around

A$0.75 if support near A$1.00 were to give way), but there's no guarantee

that a final sector-wide decline lies in store and RSG offers very good

value near its current price in the low-A$1.00 area. That's why we

suggested buying half a position near the current price with the aim of

buying the other half IF there's a sector-wide sell-off into an early-2018

low.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.barchart.com/

http://bigcharts.marketwatch.com/

![]()