![]()

![]()

![]()

![]()

- Interim Update 23rd January 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Euro-Zone Issues

Who will buy euro-zone

government bonds?

Euro-zone (EZ) government bond yields

are massively distorted. For example, despite last year's political scare

and a government-debt/GDP ratio of more than 130%, the yield on a 10-year

Italian government bond is about the same as the yield on a 10-year US

Treasury Note. For another example, the governments of France, Spain and

Portugal currently are able to borrow money for 10 years at much lower

interest rates than the US government. This situation is absurd given

relative default and "inflation" risks, but it exists due to the ECB's

manipulation. The manipulation was ratcheted down at the start of this

month when the ECB ended its bond-buying program, leading to the question:

Now that the ECB has stepped aside, who will buy EZ government debt at

anywhere near current yields?

The reality is that there will be

substantial on-going demand from pension funds, commercial banks,

insurance companies, mutual funds, hedge funds and other bond speculators,

at least while the "inflation" risk is perceived to be low. One of the two

main reasons is that the structure of the current monetary system

effectively forces the large holders of cash to buy government debt.

To see what we mean by the above statement, assume you want to

maintain $100,000 of cash-like liquidity. In this case you can deposit the

money in a bank, knowing that you will be covered by government insurance

if the bank goes bust. Now assume that you want to maintain $10 billion of

cash-like liquidity. In this case you can't deposit the money in a bank

without risking a near-total loss, because if the bank goes bust only a

trivial portion of your deposit will be covered by insurance. You are, in

effect, forced to buy the most liquid debt securities.

The other

main reason that there won't, anytime soon, be a substantial net decline

in the desire to hold EZ government debt is the belief that at some point

the ECB will return to the market as a large, price-insensitive buyer.

On the surface the belief cited in the above sentence seems

reasonable, because there is no evidence that central bankers have learned

anything from their past mistakes. There is no doubt that the leaders of

the major central banks will be inclined to react to the next bout of

economic weakness the same way they reacted to previous bouts -- by

creating new money as part of an effort to manipulate interest rates

downward. However, outside the world of central banking there are now many

people who understand that "QE" achieved nothing positive -- that it

helped some governments cope with their excessive debt burdens, but only

at the expense of savers and long-term economic progress. Consequently,

the pushback against downward manipulation of interest rates will be

greater in the future than it was in the past.

This won't stop the

ECB from attempting to falsify the price of credit in the future. In fact,

there is already talk of a new

TLTRO (Targeted Longer-Term Refinancing Operation) being introduced

before the middle of this year and we expect that the ECB will be

monetising bonds again well before year-end. However, we also expect that

political pressure, mostly but not solely from Germany, will cause the

next bond-buying program to be smaller-scale.

Anyway, our point is

that despite the ridiculously-low current levels of government bond yields

in the EZ and the ECB's removal, at the start of this month, of the most

important downward-acting force on these yields, the demand for EZ

government debt isn't about to collapse. Instead, what we should see from

here is a steady rise in EZ government bond yields as governments and

existing holders of bonds are forced to offer better deals (higher yields)

to attract new buyers. Eventually the upward trend will accelerate in dramatic fashion

due to plunging confidence (rapidly-rising fear of default), but that

isn't likely to happen this year.

The absurdity known as

"TARGET2"

TARGET2 is the system set up in the euro-zone to

clear inter-bank payments. The Bundesbank (Germany's central bank)

describes it as a payment system that enables the speedy and final

settlement of national and cross-border payments. The problem is that

often there is no "final settlement" under TARGET2. Instead, credits and

debits can build up indefinitely.

To understand the issue it first

must be understood that although the 19 countries that comprise the

euro-zone use a common currency, the euro-zone isn't really a unified

monetary system. It is more like 19 separate monetary systems, each of

which is overseen by a National Central Bank (NCB). These NCBs are, in

turn, overseen and coordinated by the ECB. TARGET2 is the means by which

money is transferred quickly and efficiently between these 19 separate

monetary systems. The transfer may well be quick and efficient, but, as

noted above, it often doesn't result in final settlement.

Further

explanation is

provided by the Bundesbank, as follows:

"...both the

Bundesbank and the Banque de France will be involved in a cross-border

payment transaction made in settlement of a German export to France, for

instance. That transaction begins when the French importer's commercial

bank in France debits the purchase amount from the importer's account and

submits a credit transfer in TARGET2 to the German exporter's commercial

bank in Germany. The Banque de France then debits the amount from the

TARGET2 account it operates for the French commercial bank and posts a

liability owed to the Bundesbank. For its part, the Bundesbank posts a

claim on the Banque de France and credits the amount to the German

commercial bank's TARGET2 account. The transaction is concluded when the

commercial bank credits the amount in question to the account it operates

for the German exporter.

At the end of the business day, all the

intraday bilateral liabilities and claims are automatically cleared as

part of a multilateral netting procedure and transferred to the ECB via

novation, leaving a single NCB liability to, or claim on, the ECB.

Viewed in isolation, the transaction used as an example above leaves the

Banque de France with a liability to the ECB and the Bundesbank with a

claim on the ECB at the end of the business day. These claims on, or

liabilities to, the ECB are generally referred to as TARGET2 balances."

The example given above by the Bundesbank refers to a German export to

France, but the same process would apply when someone transfers money from

a bank deposit in one EZ country to a bank deposit in another EZ country.

For example, the electronic wiring of funds from a commercial bank account

in Italy to a commercial bank account in Luxembourg would leave the Banca

d'Italia with a liability to the ECB and the Banque Centrale du Luxembourg

with a claim on the ECB.

The process described above means that

there is never any net clearing of cross border payments at the NCB level.

Unless the money flowing in one direction (into Country X) equals the

money flowing in the opposite direction (out of Country X), credit/debit

balances will build up and there is no limit to how large these balances

can become.

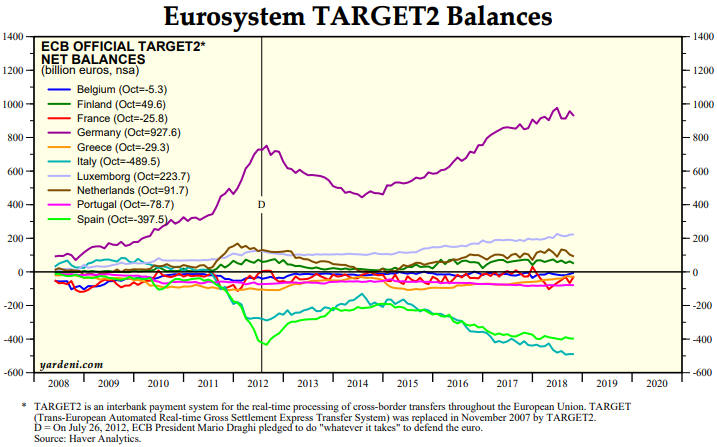

As illustrated by the following

chart from Yardeni.com,

this is not just a hypothetical issue. The NCBs of some EZ countries, most

notably Germany and Luxembourg, now have huge positive TARGET2 balances,

and the NCBs of some other EZ countries, most notably Italy and Spain, now

have huge negative TARGET2 balances.

As at October-2018, the central bank of Germany was owed 928 billion

euros by the TARGET2 system, while together the central banks of Italy and

Spain owed 887 billion euros to the TARGET2 system. Is this a problem?

The system is so strange that there doesn't appear to be a clear-cut

answer to the above question, at least not one that we can fathom. It

could be a huge problem or it could be no problem at all.

The

Bundesbank is sitting there with an asset valued at almost 1 trillion

euros that will never pay any interest and cannot be collected. At first

blush this appears to be a huge problem. It implies that at some point the

asset will have to be written off, perhaps leading to a very expensive

bailout funded by German taxpayers. But then again, due to the way the

current monetary system works it may well be possible for TARGET2 balances

to grow indefinitely with no adverse consequences. That's why we haven't

devoted any commentary space to this issue in the past.

If we were

forced to give an answer to the above question it would be that rising

interest rates, burgeoning government debt levels and private bank

failures will become system-threatening issues in the EZ long before the

TARGET2 balances pose a major threat.

The Stock Market

The senior US stock indices

pulled back to start the week. This could mean that multi-week tops were

set last Friday, but there will have to be additional weakness over the

next few days to confirm this possibility. As illustrated by the following

daily charts of the SPX and NDX, so far all that's happened is pullbacks

to 50-day MAs. These pullbacks could be routine tests of last week's

upside breakouts.

To put it another way, it's possible that the US

stock market's initial rebound from the December low ended last Friday,

but the decline from Friday's high has not been of sufficient magnitude,

yet, to signal a reversal of the multi-week trend. Until the SPX and the

NDX close below their respective 50-day MAs there will be a decent chance

that the 18th January highs will be exceeded prior to such a reversal.

The coming multi-week decline could fully retrace the rebound from the

December low, but a partial (say, 50%) retracement is now more likely.

With regard to timing, if a reversal is signaled within the coming week or

so then a significant low could occur on or near 15th February, the Fed's

next big "QT" day.

It's worth mentioning that our put/call indicator, which is shown in

the bottom section of the following chart, remains very close to its sell

zone. All the signals generated by this indicator over the past two years

have been timely.

Gold and the Dollar

Gold

There was a minor downside breakout in the US$ gold price last Friday.

Over the first two trading days of this week the gold market traded

quietly, with the US$ gold price remaining slightly below its 20-day MA.

Consequently, for all intents and purposes nothing has changed since we

posted the latest Weekly Update.

As noted in the latest Weekly Update, "...the US$ gold price could

drop as far as the low-1240s without confirming a reversal of its

short-term trend. However, if the market is still in a short-term upward

trend then the additional downside from here should be limited by the

50-day and 200-day MAs in the low-$1250s."

We view the

low-$1250s as a reasonable 2-4 week target, but there is a risk of a

larger decline.

Gold Stocks

For the

gold-mining indices and ETFs, nothing changed over the first two trading

days of this holiday-shortened (in the US) week. As illustrated by the

first of the following daily charts, the HUI traded in a narrow range

slightly below its 50-day MA and lateral resistance at 152.5. As

illustrated by the second chart, GDX chopped around in the narrow gap

between its declining 200-day MA and its rising 50-day MA.

A

counter-trend bounce could take the HUI to resistance at 157, while an

immediate extension of the decline probably would lead to tests of support

at 142.5 for the HUI and $19.30-$19.50 for GDX.

Right now we like the idea of having our long exposure to the

gold-mining sector hedged via GDX March (or later) put options and would

view a near-term bounce in the HUI to around 157 as an opportunity to buy

some additional put-option insurance. This implies that while the

above-mentioned support levels (142.5 for the HUI, $19.30-$19.50 for GDX)

are realistic downside targets, we view the short-term downside RISK as

being significantly greater.

Keep in mind that a gold bull market

has NOT been signaled. Until it is or until the gold-mining indices/ETFs

again look 'washed out', it will make sense for long-focused traders and

investors to be cautious.

Just to be clear, we are anticipating an

upward bias for the gold-mining sector during the first 3-6 months of this

year, but we don't expect a powerful rally or even a consistent upward

trend. We are anticipating a choppy advance involving multi-week rallies

followed by substantial retracements. Of course, we aim to adjust our

expectations if/when the facts change.

The Currency Market

Last week the Dollar Index (DX) negated a bearish chart pattern by

closing above 95.75. Over the first two trading days of this week it

consolidated last week's up-move.

Prior to last week we were

expecting a decline to support at 93.5, but we are now devoid of opinion.

The fundamental backdrop is neutral, the price action is non-committal,

and without the COT data we can't properly assess the sentiment situation.

In effect, we are on the sidelines waiting for either the price action or

the fundamental currency-market drivers to signal the most likely

direction of the next tradable move.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

![]()