![]()

![]()

![]()

![]()

- Interim Update 23rd August 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Industrial metals

short-term overshoot

In the past we've explained that

the prices of industrial metals, as a group, tend to rise relative to gold

when long-term interest rates are rising and fall relative to gold when

long-term interest rates are falling. This relationship is evident on the

following chart comparison of the 10-year T-Note yield (TNX) and the

GYX/gold ratio (the Industrial Metals Index divided by the US$ gold

price). Also evident on the following chart is a divergence since the end

of last month.

The recent divergence involves an extension to

GYX/gold's rally in the face of a declining 10-year bond yield. The gold

price has gained about $20 during this period, which means that the

divergence is due to strength in the industrial metals rather than

weakness in gold.

It's possible that the divergence will be closed

within the next few weeks via a rise in the 10-year bond yield, but we

think that it is due to an overshoot by the industrial metals group and

will be closed by relative weakness in this group.

We expect the short-term overshoot in the industrial metals to be

corrected via relative strength in gold in the near future. However, due

to our view that long-term interest rates will trend upward over the

coming 12 months we expect additional strength in the industrial metals

relative to gold beyond the short-term.

The Stock Market

The Dow Transportation Average

(TRAN) broke below its 200-day MA last week. During the first three days

of this week it rebounded to its 200-day MA and then dropped back to the

vicinity of last week's low. In fact, on Wednesday 23rd August it traded

at its lowest price since late-May.

It's therefore fair to say that the TRAN is behaving the way it should

if our short-term bearish outlook is correct. At the same time, the senior

US stock indices are yet to do anything particularly bearish.

By

reversing course shortly after making a new high in July the NASDAQ100

Index (NDX) opened up the possibility that it had completed a

reliably-bearish false upside breakout, but at this stage the ensuing

choppy decline looks more like a bullish consolidation than the start of a

downward trend.

We've reached the point where the senior US stock indices (the SPX,

the NDX and the Dow Industrials Index) will soon have to accelerate

downward to keep our short-term bearish view alive. Alternatively, an

extension of the downward drift of the past four weeks would indicate that

we are dealing with something more benign than the anticipated 10%-20%

correction, as would a daily close above the high of the past fortnight.

Gold and the Dollar

Gold

More misinformation about gold demand

The article "You

Are Being Lied To About "Low" Gold Demand" purports to show that

reports of low gold demand are fictitious and that, far from being low,

gold demand has been unusually high over this year to date. Unfortunately,

this article adds to the massive pile of misinformation about gold demand.

The article linked above can be put into the "not even wrong"

category. To explain, when something is wrong it can be shown to be wrong

using logic or empirical evidence, but when something is "not even wrong"

it is so jumbled and/or based on such absurd premises that it defies

dispute via reasoned counter-argument.

As an example of what we

mean, not long ago a Keynesian central banker (is there any other kind?)

used a car metaphor to describe the economy. Within the context of this

metaphor, the central bank's job is to operate the gas pedal and the brake

to move the economy forward at the optimum speed*. This metaphor paints

such a fantastical picture of the world it is difficult to argue against

it.

In more general terms, it is somewhere been very difficult and

impossible to logically argue against a proposition or piece of analysis

that is based on a ridiculous premise. With Keynesian economics, for

instance, the problem isn't so much that the logic is wrong; the problem

is that the premises upon which the logic is based are completely out of

touch with reality. In fact, if you accept the absurd premises underlying

the theory then the logically-deduced policy recommendations make sense.

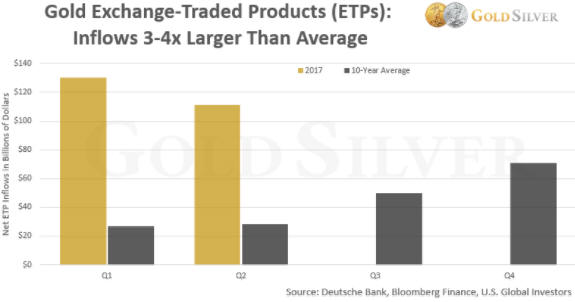

Returning to the above-linked article, the author attempts to

prove that gold demand has been very strong over the course of this year

by citing Exchange-Traded Product (ETP) in-flows. Specifically, he shows

that "net in-flows" into gold ETPs such as the SPDR Gold Shares ETF (GLD),

measured in dollars, were much higher than average during the first 6

months of this year.

For ease of reference, here is the relevant

chart from the article:

But what does "net in-flow" even mean? Every transaction involves a

purchase and a sale, with money being transferred from the buyer to the

seller. There is never any net flow of investment into an ETP.

The

only way that "net in-flow" makes any sense in this context is if it is

alluding to an increase in the amount of physical gold held by ETPs. The

fact is that when traders bid up the price of an ETF such as GLD beyond

its net asset value the ETF's Authorised Participants scalp an arbitrage

profit via a process that involves the creation of new ETF shares and the

addition of gold bullion to the ETF's assets. However, the quantity of

gold that moves into and out of ETF inventories is tiny compared to the

"net in-flow" figures indicated on the above chart.

As evidence we

point out that the "net in-flow" figures for the first half of this year

indicated on the above chart equate to about 6,500 tonnes of gold, but the

following chart shows that a) the TOTAL amount of gold held by GLD, by far

the largest of the gold ETFs, is only about 800 tonnes, and b) the amount

of gold held by GLD is roughly the same now as it was at the end of last

year. Actually, it's about 20 tonnes less.

We therefore can't fathom the "net in-flow" figures cited in the

article, but that's not why we say that the article is "not even wrong".

The main problem with articles such as this and pretty much all of the

gold demand analysis spewed out by the World Gold Council is that the

underlying premise is nonsensical. The underlying premise is that shifts

in gold demand can be determined independently of price -- by taking into

account the quantities of gold flowing from one part of the market to

another or one geographical region to another. However, none of these

flows results in any change whatsoever in the total demand for gold

because every so-called 'flow' involves an increase in demand on the part

of the buyer and an exactly offsetting decrease in demand on the part of

the seller.

In any market that clears, including the gold market,

the total demand is always equal to the total supply. Furthermore, for all

intents and purposes in gold's case the total supply is constant (the

total aboveground supply of gold increases by about 1.5% every year),

which means that the total demand for gold is effectively constant. What

changes is the relative intensity of buying and selling. When buyers

become more motivated than sellers at a particular price then the price

will rise to maintain the supply-demand equilibrium. When sellers become

more motivated than buyers at a particular price then the price will fall

to maintain the supply-demand equilibrium. The price can therefore be

defined as the thing that changes in order to maintain the supply-demand

balance.

Consequently, price is the ONLY reliable indicator that

the demand for gold has risen or fallen, or, to put it more accurately,

the change in price during a period is the ONLY reliable indicator of

whether the buyers or the sellers were more motivated during the period.

At the end of last year the gold price was US$1152 and at the time of

writing it is in the US$1290s. We therefore know that gold demand amongst

traders/investors who price their gold in US dollars has attempted to

increase since the end of last year, with the price having risen by about

US$140 to maintain the supply-demand balance. Unfortunately, this fact

tells us nothing about what will happen to the gold price in the future.

What happens to the gold price in the future will be determined by

the relative motivations of buyers and sellers in the future, which will

be influenced by central-bank actions, government actions, economic

expectations and what's happening in other markets.

*In April-2017, Janet Yellen said: "Before, we had to press down on

the gas pedal trying to give the economy all of the oomph that we possibly

could," and [the Fed is now trying to] "give it some gas, but not so much

that we're pushing down hard on the accelerator."

Current Market Situation

There was

a potentially-significant downward reversal in the US$ gold price last

Friday, but at this stage there has been no follow-through to the

downside. Instead, over the first three days of this week the price

essentially traded sideways in the $1290s.

Sentiment is neither a

headwind nor a tailwind for the gold price at the moment, while the

fundamental backdrop is bullish. As long as the fundamental backdrop

remains supportive and sentiment is no worse than neutral it will be

reasonable to expect that near-term pullbacks will be minor and that a

solid break above $1300 is coming.

With reference to the following

daily chart, there is technical support at the 20-day MA (the rising black

line, currently at $1281) and then in the low-$1260s. For a pullback to be

defined as "minor" it would have to avoid a daily close below $1260.

Gold Stocks

The HUI traded sideways in a

narrow range over the first three days of this week. As illustrated below,

it remains near the top of a wide, downward-sloping wedge that began to

form about 6.5 months ago.

There is still a chance that the pattern drawn on the above chart will

end via a downside breakout, but the longer it continues the more likely

it will end via an upside breakout. At this time an upside breakout

followed by a rise to a new 12-month high is the most likely outcome,

although, as mentioned in recent commentaries, the gold-mining sector is

due for a short-term cycle low in early-September. Ideally, then, there

will be a pullback over the next couple of weeks followed by a tradable

rally.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Revisiting

Nevsun Resources (NSU). Recent price: US$2.12

Revisiting

Nevsun Resources (NSU). Recent price: US$2.12

It is never

a good idea to let a failed short-term trade become a long-term

investment. In NSU's case, however, the same news that caused the failure

of our short-to-medium-term trade has increased the long-term

attractiveness of the stock.

To explain, poorer-than-expected

performance at the Bisha zinc-copper mine in Eritrea prompted NSU's new

CEO to come up with a revised strategy that involves a smaller open pit

with a 4-year life (previously the Bisha mine was expected to have a

remaining life of 8 years). Cutting Bisha's remaining life in half was a

shock to the market and was responsible for the bulk of the recent

stock-price plunge (see chart below), but the positive aspect of this

change of plan is that it results in a further shift in the company's

focus/emphasis to the Timok copper-gold project in Serbia. In effect, the

new plan involves milking Bisha for all it's worth in the next 4 years and

investing the proceeds in the development of Timok. We view this as a

prudent move because capital should be directed, to the greatest extent

possible, towards the lower-risk/higher-quality project.

If the

strength in the zinc market proves to be sustainable (we think it will)

then Bisha, with its 200M+ pounds of annual zinc production, could throw

off a lot of cash over the next four years. So much so that between now

and mid-2021 NSU may be able to build the Timok mine (current capex

estimate: US$213M), fund an aggressive exploration program at Timok and

pay a dividend without raising any additional money.

At today's

metal prices we estimate that fair value for NSU is around US$4.00/share,

or almost double the current price. Furthermore, if copper and zinc prices

perform in line with our expectations then a year from now the 'fair

value' could be much higher.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

![]()