![]()

![]()

![]()

![]()

- Interim Update 23rd September 2015

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Unintended Consequences

Whenever the government

intervenes in the economy in order to bring about what it deems to be a more

beneficial outcome than would have occurred in the absence of intervention,

there will be winners and losers but the overall economy will invariably end up

being worse off. Moreover, it is not uncommon for one of the long-term results

of the intervention to be the diametric opposite of the intended result.

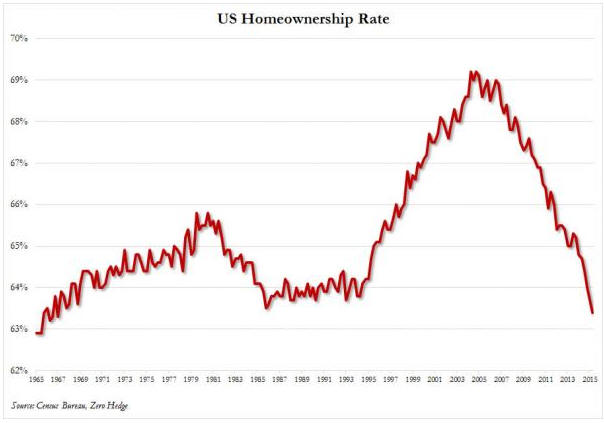

A great example of the actual result of government intervention being the

opposite of the intended result is contained in a chart that formed part of a

recent article at ZeroHedge.com. The chart, which is displayed below, shows

the home ownership rate in the US.

Here, in brief, is the story behind the above chart.

During the Clinton (1993-2000) and Bush (2001-2008) administrations the US

Federal Government decided that it would be beneficial if a larger number and a

broader range of people were home-owners. The government therefore began making

a concerted effort to not only increase the US home-ownership rate, but also to

make home loans easier to obtain for less-qualified buyers.

This was achieved in part by the more aggressive implementation, beginning in

1993, of the Community Reinvestment Act (CRA) of 1977. Under the cover of the

CRA, banks were forced to reduce their lending standards for lower-income groups

in general and 'minorities' in particular. For example, government regulations

created during the 1990s set bank loan-approval criteria and quotas with the aim

of increasing loan quantities, and even went so far as to require the use of

"innovative or flexible" lending practices to address the credit needs of

low-and-moderate-income (LMI) borrowers. Of course, banks that are forced by the

government to lower their standards when assessing the loan applications of

less-qualified borrowers must also lower their standards for other borrowers,

because they can't reasonably approve an application from one customer and then

reject an application from a better-qualified customer.

An increase in the home-ownership rate was also achieved by assigning an

"affordable housing mission" to the government-sponsored enterprises (Fannie Mae

and Freddie Mac). To make it possible for Fannie and Freddie to achieve this

mission their automated underwriting systems were modified to accept loans with

characteristics that would previously have been rejected. In addition, Fannie

and Freddie cited the new "mission" as a reason that their mortgage portfolios

should not be constrained.

At this point we would be remiss not to mention the helping hand provided by the

Fed. Without the Fed's aggressive money-pumping and lowering of interest rates

during 2001-2003 there would have been less credit and less money available to

the buyers of homes. The Fed's actions ensured that there would be a credit

bubble, while the government's actions ensured that the residential housing

market would be the focal point of the bubble.

The above chart shows that the government was initially -- and predictably --

successful in its endeavours. The home-ownership rate sky-rocketed as it became

possible for almost anyone to borrow money to buy a house. The chart also shows

that the home-ownership rate has since collapsed to its lowest level since the

1960s. This collapse was a natural consequence of the credit bubble, in that

household balance-sheets were drastically weakened by the taking-on of

debt-based leverage during the bubble and the post-bubble plunge in asset

prices.

The bottom line is that the interventions designed to increase home ownership

ultimately contributed to the home-ownership rate falling to the point where it

is now at a multi-generational low. Not just an unintended consequence, but the

opposite of the intended consequence.

The Stock Market

The US

Overview

In terms of price, a significant extension of the decline in the US stock market

is likely prior to a short-term bottom. It is especially worth noting that, as

was the case in August, there is the potential for a sudden and rapid downward

acceleration prior to a meaningful low. In terms of time, however, a short-term

bottom is probably not far away.

As we've consistently maintained over the past couple of months, the first half

of October is the most likely time for a short-term bottom regardless of whether

the decline from the mid-July peak is a bull-market correction or the first leg

of a new cyclical bear market. October gets underway during the second half of

next week, so we are only one week away from entering the most likely 2-week

time-window for a short-term bottom.

For short-term traders (not long-term investors), it will be worth participating

in the rally that follows the coming short-term bottom. Therefore, while it

makes sense right now to continue leaning towards the bearish side, traders

should be ready to shift the other way in the near future.

The Price Action

The following chart of the Bank Index (BKX) is one of several reasons to suspect

that while a multi-month bottom is likely within the coming three weeks, the

decline from the May-July peak in the US stock market was just the first leg of

a 1-2 year cyclical bearish trend. The chart shows that the BKX had been working

its way upward within a channel since late-2011 and broke decisively below the

bottom of this channel last month.

It looks like the BKX has been tracing out a long-term topping pattern since

early last year. Completion of the major top would be signaled by a weekly close

below lateral support at 65-66. We doubt that this will happen within the next

couple of months, but a test of this support is likely prior to a short-term

bottom.

Over the past two weeks the Dow Transportation Average broke above its 50-day

MA, gained some additional ground and then reversed downward. This is similar to

the way an interim peak was put in place in early-August -- just prior to the

start of a steep 3-week decline.

The World

The following chart shows that the Dow Jones World Index (DJW) is close to a

2-year low. Like the S&P500 Index, it broke out to the upside last week and then

almost immediately reversed downward.

A breach of the August low is likely prior to a short-term bottom.

Gold and the Dollar

Gold

In the email alert sent to subscribers in response to Tuesday's market action we

wrote that, as expected, the 20-day MA was acting as near-term support for the

US$ gold price. With the support having been successfully tested on Tuesday, we

concluded: "What gold has done over the first two days of this week currently

looks like a 'pause for breath' within a short-term upward trend. If so, the

rally should resume in the next day or so."

The rally resumed on Wednesday, but to maintain its short-term upward bias gold

must continue to hold above the 20-day MA on a daily closing basis.

As illustrated by the following daily chart, the US$ gold price has minor

lateral resistance at $1140 and more important lateral resistance at $1170. The

200-day MA, which is presently near $1180, could also prove to be an obstacle.

In other words, there is strong resistance at $1170-$1180. In the absence of a

dramatic news-related catalyst, this resistance range probably defines gold's

maximum upside potential over the weeks immediately ahead.

Gold Stocks

The HUI's rebound from its early-August low immediately ended after reaching the

50-day MA. Last week's rally did exactly the same. A shallow pullback during the

first half of this week would have been neither surprising nor bearish, but the

quick return to the lows of the past 2 months suggests that there will be a new

low prior to the start of a multi-month rally.

Rather than showing a chart of the HUI, today we are showing a chart of the XAU.

The reason is that the XAU's chart pattern is clearer.

The top half of the following chart shows that the XAU has been tracing out a

declining wedge pattern since early-August, with sequences of declining tops and

marginal new lows. The bottom half of the chart shows that there is presently no

sign of strength in the XAU relative to gold, which is to be expected given that

the XAU is close to its bear-market low. As previously explained, there is

generally no bullish divergence between the gold-mining indices and gold bullion

at a major bottom. Instead, the gold-mining indices lose value relative to gold

until the day of the major price bottom, at which point they suddenly become

relatively strong.

We interpret the declining wedge as a bottoming pattern. As a consequence, we

expect that any new low in the near future will be marginal. That's an opinion

that could obviously be wrong, but it's the most realistic view given the extent

of the price decline to date and the almost-palpable bearishness about the

prospects for gold-mining stocks.

That being said, if you are a short-term trader you don't need to have an

opinion about the XAU's (and the HUI's) additional downside potential,

especially if you are anticipating a rally and looking for an opportunity to

speculate on the long side. The reason is that after the gold-mining indices

commence an intermediate-term rally or a new bull market, the initial rise from

the bottom invariably breaks above the 50-day MA in quick time and then moves

far enough above this MA so that it can act as support during the first

significant correction. Furthermore, the initial 4-8 week advance in a new

intermediate-term upward trend or bull market invariably takes the price at

least 40% above its low. With the 50-day MA for both the XAU and the HUI only

about 8% above the current price, a reasonable plan could involve 'going long'

as soon as these indices closed above their respective 50-day MAs.

Here are two XAU and XAU/gold charts showing examples of intermediate-term

bottoms in the gold-mining sector. The first chart covers the intermediate-term

(and major) bottom of November-2000. The second chart covers the

intermediate-term bottom of August-1986, which currently looks more similar to

the recent price action. Notice the speed of the initial rally in both cases.

Sentiment is the main reason that the gold-mining indices and ETFs haven't yet

been able to sustain an advance. The US$ gold price has shown some modest signs

of strength, but the popular view is that the gold price will eventually drop to

new lows. Furthermore, gold-mining stocks are being affected by the on-going

weakness in other mining stocks. For example, the HUI's flat performance since

early-August is disappointing, but it is much better than the performance of

SPTMN (the Diversified Metals and Mining Index). SPTMN has lost 25% of its value

over the same period.

The Currency Market

The lines we've drawn on the following daily chart show that the Dollar Index's

performance since its March peak has taken the form of a contracting range.

Although the US$ was sufficiently stretched to the upside to set in place a

major peak in March-2015, the price action since the top looks more like an

intermediate-term consolidation than the start of a long-term decline.

The positions of the lines are somewhat arbitrary, but if the contracting-range

interpretation is correct then there is important resistance at around 97.5 and

important support at 93.5-94.0.

We had thought that the Dollar Index would drop to its 24th August spike low

(92.5) or a little lower if the SPX did the same, but we now suspect that the

dollar's near-term downside will be limited by support at 93.5-94.0. This is not

only because of the trend-line drawn on the above chart but also because there

has been evidence in the recent price action that the euro is no longer

benefiting from stock-market weakness. This could mean that the 'hot money' that

used borrowed euros to fund equity speculations has exited the bulk of its

positions.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

![]()