![]()

![]()

![]()

![]()

- Interim Update 23rd September 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The Stock Market

In theory, a US Supreme Court

Justice is an impartial judge of the legality and constitutionality of court

decisions, government statutes and presidential directives. In practice,

however, each Supreme Court Justice is influenced by his/her political

leaning. As a result, a vacancy on the Supreme Court of the United States

is viewed as an opportunity for the party with the power to nominate the

replacement (in the current case, the Republican Party) and a threat to

the other major party. Consequently, the process of nominating and

confirming a new Supreme Court Justice can be acrimonious and get in the

way of agreements on other issues.

That's why the death last Friday

of Supreme Court Justice Ginsburg has reduced the probability of the

Republican and Democratic parties striking a pre-election stimulus deal.

The nomination/selection of a new Supreme Court Justice would be

contentious at the best of times, but at the moment it is even more so

because it is happening shortly before an election that will itself be

contentious.

The reduced probability of a pre-election stimulus

deal increases the US stock market's short-term downside risk, but we

continue to think that the most likely outcome is a normal correction. For

the SPX, a normal correction would encompass a test of the 200-day MA. The

following chart shows that the 200-day MA is about 130 points (4%) below

Wednesday's closing price.

A normal correction is being signalled by the Volatility Index (VIX).

As illustrated by the following chart, the VIX's performance over the past

month looks similar to its performance during the June correction. That's

despite the current correction being larger than the June correction in

terms of the SPX's peak-to-trough decline.

Note that if the VIX

were to return to near its early-September high within the next two weeks

then the similarity with the June-July period would disappear. This would

warn that something more bearish than a normal correction was in progress.

Apart from the reduced probability of a pre-election stimulus deal,

there are two reasons to be concerned that the decline from the

early-September peak could develop into something more bearish than a

normal correction.

The first reason is the performance of the NYSE

Advance-Decline Line (ADL), which is shown in the lower section of the SPX

chart presented above. Unlike the June correction, the September

correction was preceded by a bearish divergence between the SPX and the

ADL. Also, the ADL has been weaker during the current corrective period

than it was in June.

The second reason is that there has been far

more weakness in the mega-cap tech stocks since the early-September peak

than there was during the weeks following the early-June peak. The

difference is obvious on the following daily chart of the NASDAQ100 Index

(NDX). The chart shows that the NDX's upward trend hardly even paused for

breath during June, whereas the decline from the September peak looks like

trend reversal. At best, this is signalling an intra-market leadership

change.

We reiterate that a normal correction (maximum 4% additional downside

for the SPX) is considered the most likely outcome, but at the same time

we acknowledge the risk that something more bearish will happen. Something

more bearish for the stock market probably would go hand-in-hand with the

Dollar Index reaching the top of our upside target range (98).

Gold and the Dollar

Gold

Gold has broken decisively below support at US$1920. This suggests that

the price could fall as far as lateral support in the low-$1700s before a

correction low is in place, although there is lateral support near $1800

that could act as a floor. Gold also has broken out to the downside in

euro terms.

If there is a rebound attempt over the final two days

of this week it probably will be limited by the $1920 level that was

tested numerous times before being breached on Monday of this week. In

other words, former support is now resistance.

The fundamental backdrop remains bullish for gold. This indicates that

we are dealing with a correction within the context of a multi-year

advance and not the start of major downward trend.

This week's

breakdown suggests that a correction low will be set within the coming

month and could be set as soon as next week. If so, the US$ gold price

probably will be making new highs by early next year.

Silver

In the latest Weekly Update we noted that the US$

silver price had barely moved during Tuesday-Friday of last week, but that

it appeared to be slowly forming a short-term top. The topping

interpretation was confirmed in no uncertain terms on Monday of this week.

Monday's 10% plunge in the silver price left the $26.00 demarcation

level in the dust. Wednesday's 6% plunge then added to the damage by

taking out the early-August low.

The bad news is that significant short-term downside risk remains. The

good news is that this week's dramatic increase in volatility could result

in the silver market reaching a correction low as soon as next week.

As mentioned in previous TSI commentaries over the past two months,

silver has short-term downside risk to the vicinity of the 200-day MA

(around US$19.00). Despite that still being the case, we took profits on

half of our SLV put options on Wednesday 23rd September. This was done to

ensure that whatever happens from here, we end up with a sizable profit on

the position. Also, we plan to take profits on the balance of our SLV puts

if lateral support at around $21.00 for silver futures is reached within

the next several days. The reason is that even though the decline could

extend to $19, at $21 or lower silver's short-term risk/reward would be

bullish.

Gold Stocks

In the email sent to

subscribers in response to Monday's market action, we wrote:

"The

HUI must close below 320 to confirm that the August-September cycle worked

this year (for the sixth year in a row). It didn't do that on Monday 21st

September, but there's a risk that it is tracing out a crash pattern and

will plunge within the next two weeks."

A crash pattern

involves an initial decline from an intermediate-term high, followed by a

rebound or consolidation that can retrace up to 100% of the initial

decline and then a second decline that transforms into a crash after the

low of the initial decline is breached. Most crash patterns don't end in

actual crashes, but to get a crash a market usually has to go through the

sequence outlined above.

In the current case of the HUI, a sharp

initial decline from the early-August high of 374 to a low of 320 was

followed by several weeks of consolidation that retraced about 75% of the

initial decline. In the email sent earlier this week we were referring to

the risk that taking out 320 would set off a crash.

Support at 320

was taken out on Wednesday 23rd September.

We aren't expecting a

bona fide crash, but, as mentioned numerous times over the past several

weeks, we do think there is a realistic chance of the HUI trading as low

as the 260s before its correction ends.

We generally advocate scaling in on weakness, but not randomly. The

current situation is that the gold mining indices/ETFs a) have just broken

below important support levels, b) are well above the next important

support levels, and c) are not yet oversold. Therefore, right here and now

there is no good reason to buy for a short-term trade. If you buy for a

short-term trade at this time you may get lucky, but relying on luck is

not a good strategy.

We would be sceptical regarding the

sustainability of any rebound that started from near the current level. If

an attempt to rebound is made over the coming 1-2 days then former support

for the HUI in the 320s probably would act as resistance.

Our guess

at this time is that a correction low for the gold mining sector will be

in place by the end of next week, but we'll take the evidence as it comes.

The Currency Market

The Dollar Index (DX) and the euro

Much of what will happen

in the financial world over the coming 1-2 months hinges on the US$. The

world seems very different when the DX is trending upward than it does

when the DX is trending downward.

In the latest Weekly Update, we

wrote:

"While there is a risk that the currency-market action

of the past seven weeks will prove to be nothing more than a pause to the

short-term trend that got underway in May, we think that the DX's

performance since late-July looks like a basing pattern and that the

euro's performance over the same period looks like a topping pattern."

Due to what happened over the first three trading days of this week we

can now be certain that the price action of the past two months involved

basing for the DX and topping for the euro. As previously advised and with

reference to the daily charts displayed below, the DX should rise to 95-96

and could rise to 97-98 before resuming its longer-term decline, while the

euro should drop to around 115 and could trade as low as 112 before

resuming its longer-term advance.

We plan to exit at least half of

our euro (FXE) put options if the euro reaches 115 within the next two

weeks.

The Commodity Currencies

We

have focussed on the Australian dollar (A$) over the past six months

because it was considered to be the major currency that would benefit the

most from a cyclical rise in commodity prices. We also have noted that the

Canadian dollar (C$) should benefit from the rise in commodity prices,

albeit to a lesser extent due to the tendency for the C$ to be weak

relative to the A$ during multi-year periods when the Dollar Index is

weak.

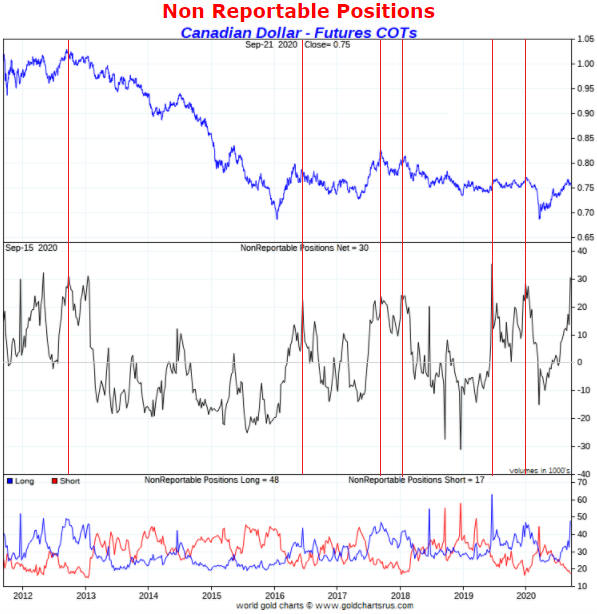

The C$ is being singled out for discussion today because the

latest Commitments of Traders (COT) report revealed a sentiment extreme

associated with the positioning of NonReportable (a.k.a. small) traders in

C$ futures. We are referring to the fact that the net-long position of the

NonReportable traders recently rose to near its highs of the past 9 years,

implying that the 'dumb money' recently became as bullish about the C$ as

it usually gets.

The following weekly chart shows that every other

time over the past eight years that the NonReportable traders in C$

futures were as 'long' as they were last week, the C$ was close to a peak

of at least short-term significance.

We think that the C$ and the A$ have commenced 1-3 month corrections

within 1-2 year upward trends. For the C$, a normal correction would

result in a decline to around 73.

For the A$, a normal correction would result in a decline to around

68.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Introducing

Aeris Resources (ASX: AIS). Shares: 1873M issued, 1967M fully diluted.

Recent price: A$0.052.

Introducing

Aeris Resources (ASX: AIS). Shares: 1873M issued, 1967M fully diluted.

Recent price: A$0.052.

AIS is an Australia-based

copper-gold producer with a current market cap of about A$95M. The company

has working capital of A$37M and long-term debt of A$68M, meaning that its

net debt is A$31M and its EV (market cap plus net debt) is A$126M. The

debt figure includes a payment of A$15M due to Evolution Mining on 30th

June 2022, but we haven't included contingent payments of up to A$50M due

to Evolution Mining during the period from 1st July 2022 to 30th June

2027. The payments to Evolution are linked to AIS's purchase of

Evolution's Cracow gold mine three months ago.

During the financial

year ending 30th June 2021, AIS expects to produce about 70K ounces of

gold at its Cracow mine in Queensland and 53M pounds of copper at its

Tritton mine in NSW. At US$1900/oz for gold and US$3.00/pound for copper,

the FY2021 production guidance results in revenue of around US$292M

(A$390M), 54% of which is copper-related and 46% of which is gold-related.

We are interested in AIS mainly for its copper production, but the gold

production reduces risk.

The projected FY2021 cash costs are

US$735/oz for gold and US$2.17/pound for copper, assuming an average

A$/US$ exchange rate of 0.75. This means that the production should be

very profitable.

With A$390M of profitable annual revenue AIS would

be worth A$0.19/share even if it were only valued at 1-times revenue. Why,

then, is the market currently valuing the stock at A$0.052?

The

reason is that the company's two operating mines have short reserve lives.

Specifically, at 31st December Cracow had only 114K ounces of gold

reserves and Tritton had only 220M pounds of copper reserves, meaning that

Cracow currently has only 1-2 years of remaining life and Tritton has only

4 years of remaining life. However, AIS's management expects that

sufficient additional reserves will be proved-up to enable the lives of

both mines to be extended by several years. Given the historical

performance, this appears to be a reasonable expectation. For example,

Cracow has produced 80K-100K ounces of gold per year for a great many

years without ever having more than 273K ounces of P&P gold reserves.

From an investing/speculating perspective, the opportunity is that the

company will do enough to convince the market that substantial mine-life

extensions are likely. This could result in a 200%+ increase in the AIS

stock price with no change in metal prices. At the same time, the low

current valuation mitigates the downside risk.

There are three

other parts of the AIS story worth highlighting at this time.

The

first is that the company has hedged, via forward sales, about half of its

production between now and July-2021. The hedging was done at slightly

above current metal prices and should ensure that cash flow is strongly

positive over the next three quarters, but we would view it as a negative

if the company were to engage in additional hedging. Most people buy the

stocks of copper and gold miners for leverage to copper and gold prices,

not for steady cash flow.

The second is that AIS has a $256M

carried-forward tax loss on its balance sheet that could be used to offset

future taxes. This will be a valuable asset if the company becomes very

profitable.

The third is that the AIS share structure and share

price are not appropriate for a company with AIS's assets. This issue

could be resolved via a 1-for-10 or 1-for-20 share consolidation.

The AIS stock price has fallen by more than 20% over the past two weeks

and has returned to intermediate-term lateral support. Despite the overall

market risk, this is a reasonable price level to start scaling into the

stock.

We have added AIS to the TSI List as an intermediate-term

trading position, but depending on what happens over the next few months

we may end up making it a long-term position.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

http://www.goldchartsrus.com/

http://bigcharts.marketwatch.com/

![]()