![]()

![]()

![]()

![]()

- Interim Update 23rd November 2016

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The long-term bottom

for interest rates

The yields on long-dated US

Treasury debt have made significant gains since bottoming 4-5 months ago.

Due to emerging evidence of "price inflation" and the expectation of more

"price inflation" to come, they are likely to comfortably exceed this

year's highs during 2017. However, for the three reasons outlined below a

major rise in interest rates is more likely to be next decade's story than

a story for the next 1-2 years.

The first reason is that the US

stock market's valuation can only be justified if the assumption is made

that US government bond yields will remain at 2% or lower forever. If the

10-year yield moves up to 3% then this assumption will be exposed for the

silliness it is, prompting a substantial downward re-rating of the stock

market. A large stock-market decline would, in turn, drive the 10-year

interest rate back down as part of a flight to safety. In other words,

interest rates will probably be capped over the next couple of years by

the effects that higher interest rates would have on equity valuations.

Another reason is that the US economy is likely to enter its next

recession in 2017. While it wouldn't be unprecedented for interest rates

to rise during a recession (they rose during the 1973-1974 recession, for

example), with debt levels at or near historic highs it's far more likely

that a 2017-2018 recession would be accompanied by falling inflation

expectations, increasing demand for money and a shift towards the

perceived safety offered by US Treasury debt.

A third reason to

expect the US 10-year yield to be capped at around 3% for at least the

next couple of years is the tendency for long-term rising trends in

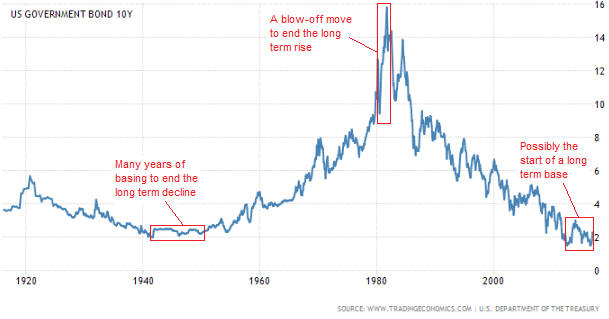

interest rates to end via blow-off moves (as per the early-1920s and the

early-1980s) and for long-term falling trends in interest rates to end via

many years of basing. To show what we mean, here's a very long-term chart

of the US 10-year yield.

The historical sample size is admittedly very small, but if the

current long-term declining trend ends in a similar way to the previous

long-term declining trend then the US 10-year T-Note yield will spend a

few more years in a range bounded by the 2012 low at around 1.4% and the

2013 high at around 3.0%.

Here's a short-term chart showing the

potential trading range assuming that the secular interest-rate trend is

in the process of shifting from down to up.

If we are right, then interest-rate moves will be difficult to trade

over the next couple of years. Profiting from the swings will require very

good timing.

Oil Update

As discussed in a

post at the TSI Blog earlier this week, a sizable gap between the oil

price and the Canadian Dollar (C$) has again opened up. There is no

guarantee that this gap will be closed via a decline in the oil price, as

it could also be closed via a rally in the C$. There's also no guarantee

that it will be closed at all. However, the historical record suggests

that the gap will be closed and that it will happen via weakness in the

oil price.

The upshot is that we are being presented with a new

opportunity to speculate on a lower oil price or to hedge

commodity-related long positions via oil (USO) put options.

Primarily for hedging purposes, we have begun to average into a position

in USO February-2017 $10 put options and expect to have a full (albeit

small) position within two weeks. We chose February options because

cyclical/seasonal factors suggest that January-February is the most likely

time for the next multi-month bottom in the oil price.

The Stock Market

The US

The S&P500 Index (SPX) has followed the Dow Industrials Index into new

high territory. It must end the week above the August high of 2194 to

confirm the breakout, but with only half a day of US trading left in this

week (due to Thanksgiving, the US market is closed on Thursday and open

for only half a day on Friday) it is likely to do so.

The NASDAQ100

Index (NDX), however, is still trading below its September and October

highs.

A significant pullback over the next few weeks is certainly possible,

but every technical indicator we track now points to a 6-12 month

extension to the US equity bull market. This doesn't mesh with what's

happening on the earnings front or with most economic indicators, although

it is consistent with the acceleration in the pace of money-supply growth

over the past two months.

Greece

Despite

the fact that Greece is widely perceived to be an economic basket-case,

it's now worth considering an intermediate-term bullish speculation on

Greece's stock market via the Global X MSCI Greece ETF (GREK). Even though

this ETF is US$-denominated and has therefore been pressured downward over

the past few months by weakness in the euro, it has broken above a

downward-sloping trend-line that originates way back in early-2015 and

appears to be in the process of tracing out an intermediate-term basing

pattern. The top of the base is near $9.00.

The economic problems facing Greece are substantial. They are also

very well known, which is why Greek equities have very low valuations on

average. For example, the

ETF Research Centre indicates that GREK is trading at only 0.3-times

book value. By way of comparison, the S&P500 trades at 2.7-times book

value and the euro-zone average is about 1.4-times book value.

Almost any asset can be a good investment or a bad investment. It all

depends on the price.

We have begun to average into GREK in our own

account and will probably add it to the TSI List if it pulls back to

around $7.50.

Gold and the Dollar

Gold

The

US$ gold price has broken below trend-defining support in the low-$1200s.

If the break below $1200 is confirmed by the weekly close it will be

another nail in the coffin of the bull-market scenario.

Gold's main problem is bearish fundamentals. At no time during the

rally from the December-2015 low were the fundamentals definitively

bullish, and right now they are more bearish than they have been in years.

Very few long-term gold bulls understand this. They look at what

central banks are doing and automatically assume that the fundamental

backdrop is gold-bullish, but gold's fundamentals are determined by the

expected effects of monetary policies rather than the actual efficacy of

the policies. To put it another way, gold's fundamentals are determined by

monetary and economic confidence rather than the actual ability of a

policy course-of-action to have a positive effect. This may seem vague,

but monetary/economic confidence and expectations can be measured by

quantities such as credit spreads, the TIPS yield, the yield curve, and

the bond/dollar ratio.

As mentioned in the latest Weekly Update,

the good news for gold 'longs' is that some of gold's most influential

fundamental price drivers are stretched beyond normal bounds in a

gold-bearish direction. This makes it likely that the downward pressure

will soon dissipate, potentially enabling a significant rebound. We

mentioned, for example, that both the T-Bond and the Dollar Index were

very extended -- to the downside for the T-Bond and to the upside for the

Dollar Index -- on a short-term basis, making it likely that the

bond/dollar ratio will soon begin to rebound.

The bond/dollar ratio

became even more stretched in a gold-bearish direction during the first

half of this week, but the same analysis applies.

Also stretched

beyond normal bounds on a short-term basis is the Yen, a fact that we are

mentioning in the "Gold" section of today's report because the Yen is the

currency that over the past several years has had the strongest

correlation with gold. Just as the low-$1200 area was a likely target for

a bottom in the gold price and just as gold is spiking below this

important support range, the 89-90 area was a likely target for a bottom

in the Yen and the Yen has just spiked below this support range.

The extent to which the Yen is stretched to the downside on a short-term

basis is evidenced by the RSI(14) displayed at the bottom of the following

daily chart. A daily RSI(14) as low as 17 is rare.

Silver

We just wanted to point out that the

silver price is now very close to important lateral support at $16.00,

which for the past few months has been considered the most likely level

for a correction low.

There is no longer a good chance of $16.00

being the final bottom for the correction/downturn that began in July, but

this is a price area from which a multi-week rebound will potentially

begin.

Gold Stocks

In reaction to gold's break below

$1200, the HUI traded at its lowest level in more than 7 months and

dropped back to the bottom of its well-defined price channel on Wednesday.

Interestingly, however, it didn't close below its 14th November intra-day

low. There is therefore still a hint of a bullish non-confirmation between

gold bullion and the associated mining stocks.

It's worth repeating the following two paragraphs from the latest

Weekly Update, because although the gold price has broken below support at

$1200 the overall situation is not materially different:

"If a

turn to the upside doesn't happen immediately it will probably do so

before the end of November. This is not only because the gold-mining

indices are 'oversold', but also because the short-term blow-off moves in

T-Bonds and the US$ (the source of the current downward pressure on

gold-related investments) will soon exhaust themselves.

The rebound

that follows the coming short-term reversal could last a few weeks and

could be strong enough to create the impression that a new

intermediate-term upward trend has begun, but the price action of the past

two weeks has increased our conviction that the overall correction/decline

won't end before the first quarter of next year."

The

Currency Market

After a small pullback on Monday, the

Dollar Index continued its relentless up-move on Tuesday and Wednesday. It

has now risen on 12 of the past 13 trading days.

Despite the Dollar

Index's clear-cut break to new multi-year highs, none of the Dollar

Index's component currencies has made a new multi-year low. Of particular

relevance given that it is almost 60% of the Dollar Index, the euro hasn't

yet traded below its March-2015 bottom.

There's a good chance that the euro will not only trade below its

March-2015 bottom but also drop below parity with the US$ during the first

few months of next year. However, it is probably close to its low for this

year.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.tradingeconomics.com/

![]()