![]()

![]()

![]()

![]()

- Interim Update 24th February 2016

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

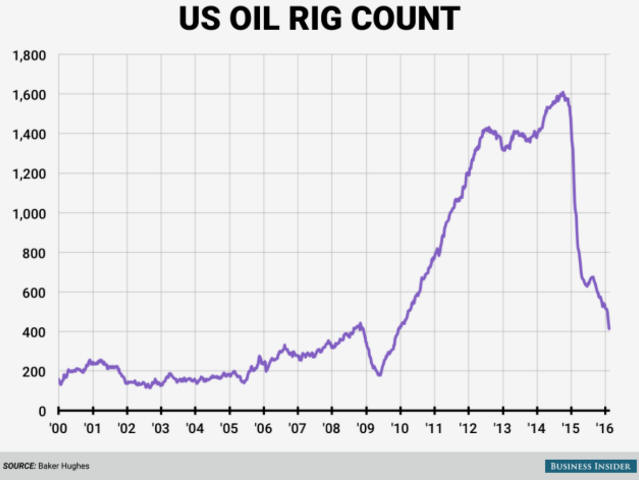

Oil Update

The life and death of an

investment bubble

The following chart shows the life and death of an investment bubble.

The inflation of the bubble during 2009-2014 was due to money-pumping and other

central-bank policies. More specifically, it was caused by the combination of

rapid monetary inflation in many countries, most notably China, leading to

unsustainably-high demand for oil and a very high price for oil, and by Federal

Reserve policies that led to artificially-low interest rates and a frantic

search for yield in the US. Since the price of oil did not accurately reflect

sustainable demand, when demand began to fall the massive investment in new

supply was revealed to be what "Austrian" economists call mal-investment. The

bubble deflated.

As is always the case, the gains achieved during the bubble period proved to be

ephemeral and resources were wasted on a grand scale. Furthermore, the full cost

of the wastage will never be known, because it is only possible to 'see' the

losses in the shale-oil and related businesses. It will never be possible to see

what would have been if the price system had been allowed to work, that is,

there will never be any way of knowing the productive investments that would

have been made if the intervention-crazy Fed had not unwittingly implemented

policies that channeled far too many resources into the development of shale-oil

fields.

Most disturbingly, there is no recognition within the halls of central banking

and very little recognition within the ranks of mainstream economists and

financial journalists that the problems now being encountered by the oil

industry are primarily due to the falsification of prices by central banks.

Janet Yellen seems to believe that all problems facing the US economy stem from

outside the US and that the Fed has done almost everything right. The Fed has

certainly done everything by the book. The problem is that the book is

completely wrong.

A consequence of there being almost no understanding in the central-banking

world of the economic damage wrought by the falsification of prices is that the

deliberate policy of price falsification is bound to continue unabated. This is

as close to a certainty as you will get in the financial world. The difficulty

is in figuring out the short- and intermediate-term effects of the policy.

Current Market Situation

The collapse in the quantity of drilling rigs operating in the US oil industry

hasn't yet had a big effect on production, but it eventually will. If it doesn't

happen this year it will happen next year. Moreover, the market price will begin

to discount a more bullish supply-demand situation well before it becomes

apparent in the production data.

US oil production is going to decline, but this is not the only reason we expect

a significantly higher oil price within the coming 12 months. In addition there

is the on-going central-bank policy that entails fomenting a new bubble in an

effort to mitigate the short-term pain stemming from the bursting of an earlier

bubble, and the likelihood that before this year is over the market will be

prompted to factor a higher risk of a Middle-East oil-supply disruption into

current prices.

One of the first signs that the oil price has bottomed on an intermediate-term

basis will be a weekly close above the 10-week MA (the blue line on the

following chart). A more conclusive, although less timely, sign of a sustainable

bottom will be a weekly close above the 40-week MA (the black line on the

following chart). Notice that both of last year's rallies ended exactly at the

40-week MA.

The Stock Market

The US

Revisiting the relevant comparison

As explained a few times last year and most recently in the 13th January Interim

Update, we think it makes more sense to compare 2015-2016 with 2000-2001 than

with 2007-2008. This is because the present-day fundamental, monetary, sentiment

and technical backdrops all have more in common with 2000-2001 than with

2007-2008. In particular, both 2000 and 2015 had a strong dollar, very weak

markets for gold and gold-mining stocks, widespread belief that the US economy

was by far the world's strongest, a Federal Reserve making small steps towards

tighter monetary conditions, and an investment boom in large-cap tech stocks. It

is also because a new bear market is unlikely to evolve along the lines of the

most recent preceding example (the one that is freshest in everyone's mind).

Here is an updated version of a chart-based comparison we showed multiple times

over the past 12 months. We initially showed this comparison during the first

half of last year to make the point that there was an upside breakout in the

NYSE Composite Index (NYA) shortly before a major top in 2000 and that the same

thing could be in store this time around.

As it turned out, the NYA broke out to the upside last May-June and has since

performed similarly to how it performed during the months following 2000's false

upside breakout.

We stated in our 13th January commentary that if the similarity persisted then

there would be a short-term bottom during the first quarter of this year. The

similarity has persisted, so that's still the case. Moreover, the 11th February

price action (the SPX's quick spike below its January low) and the

sentiment-related evidence outlined in the latest Weekly Update suggest that the

short-term bottom expected for Q1 is already in place.

Comparisons such as the one shown above can be visually appealing, but they

should never be relied on. Every cycle has significant differences and we can be

confident that even though the current market is presently following roughly the

same path as 2000-2001, at some point it will deviate.

Such comparisons can, however, provide legitimate clues as to what's possible in

the future. Taking the 2000-2001 analogy along with the sentiment backdrop and

the extent to which the stock market was 'oversold' during the week before last,

we should be open to the possibility that there will be a rebound to the 200-day

MA or perhaps even a little higher within the coming three months.

Current Market Situation

In the latest Weekly Update we said that S&P500 (SPX) resistance at 1950 would

probably soon be tested. It was tested the next day, after which there was a

routine 1-2 day pullback.

It is reasonable to expect that the 1950 resistance level will be breached

within the next couple of weeks. Assuming it is breached, the next upside target

will be the more important lateral resistance that lies at 1990-2000. Getting

through this resistance would likely result in an extension of the rebound to

near the 200-day MA (currently at 2028, but slowly declining).

Our guess is that the overall rebound from the January-February double bottom

will continue in fits and starts until the SPX reaches the vicinity of its

200-day MA. However, we are certainly open to other possibilities and will take

the evidence as it comes.

Gold and the Dollar

Gold

Here's how we concluded the gold discussion in the latest Weekly Update:

"Although it is not something we would bet on, with support at $1190 having

passed its first test and with the COT situation not yet bearish a quick move to

a new high for the year is a realistic possibility. Round-number resistance at

$1300 and the January-2015 peak at $1308 will be obvious near-term targets if

the February high of $1264 is breached."

There was considerable volatility in the gold market over the first three days

of this week and a potentially significant downward reversal on Wednesday 24th

February, but the situation is not materially different now than it was at the

end of last week. The gold market remains 'overbought' and it is possible that a

short-term top was put in place on 11th February when the price spiked up to

$1264, but a short-term top hasn't yet been clearly signaled.

As previously advised, a daily close below $1190 would be a clear signal that a

short-term top was in place. Also, the 20-day MA has moved up to the $1180s and

will be above $1190 by the end of this week. Once it moves above $1190 a daily

close below the 20-day MA could reasonably be interpreted as confirmation of a

short-term top.

Until a short-term top is signaled via a daily close below $1190 and/or the

20-day MA there will be a realistic chance of a rise to the resistance that lies

at $1300-$1308. This resistance, in our opinion, defines the maximum

daily-closing upside potential with regard to the coming two months, although it

is likely to be breached within the coming 6 months.

Whether or not the gold price makes a new high for the year in the near future

will be strongly influenced by the relative strength of the banking sector. The

reason is that the relative strength of the banking sector, as indicated by the

SPX/BKX ratio (the S&P500 Index divided by the Bank Index), has been the gold

market's dominant fundamental price driver over the past 12 months.

The chart displayed below shows that the recent sharp rise in the US$ gold price

followed closely behind a sharp rise in the SPX/BKX ratio, which was the result

of a mini panic out of bank stocks. The chart's message is that for gold to

extend its rally the banking sector will have to continue weakening.

Additional relative weakness in bank stocks is a good bet with regard to the

coming 12-24 months, but it won't surprise us if bank stocks rebound in absolute

and relative terms over the coming 1-2 months.

Gold Stocks

Current Market Situation

Although the US$ gold price peaked two weeks ago and is now more than $30 below

its 11th February intra-day high, the HUI has continued to push upward and made

a new high for the year on Wednesday 24th February. On a short-term basis it

remains as 'overbought' as it ever gets, but it hasn't yet signaled that a

short-term top is in place. To put it another way, the warning bells of a

correction are ringing loudly, but there is no evidence yet that the correction

has begun.

We can be sure that there will be a correction that causes the HUI to trade at

or below its 50-day MA within the coming three months. The unknown is where the

50-day MA will be when it hits the current price. The longer it takes for the

50-day MA to intersect the current price, the higher the level at which the

intersection will occur.

For example, the 50-day MA is now at 125, but at the rate it is rising it will

be around 140 by the end of next month. It is possible, therefore, that a

multi-week correction could hold at or above lateral support at 140 and also

touch the 50-day MA.

The evidence continues to build that a short-term top is close at hand AND that

a bull market has begun. In addition to the evidence cited in recent

commentaries, this includes the performance of the HUI/gold ratio.

Due to the dramatic strength in gold-mining stocks relative to gold bullion over

the past six weeks, the HUI/gold ratio is now about 20% above its 40-day MA.

This is illustrated below. At the same time as it points to gold-mining stocks

being stretched to the upside on a short-term basis relative to gold bullion,

this situation has longer-term bullish implications. The reason is that the only

other occasions over the past 16 years when the HUI/gold ratio was 20% or more

above its 40-day MA happened during 2001-2002 (the first two years of a bull

market) and late-2008 (the first two months of a multi-year rally).

The historical record suggests that the HUI/gold ratio will drop to its 40-day

MA or lower within the coming three months, before resuming its advance.

What are we doing with our gold-stock portfolio?

We did a minor amount of selling on Wednesday 24th February and still have three

small-scale above-the-market sell orders in place, but we have essentially

retreated to our 'core' gold-mining exposure and will not do much more selling

of gold stocks unless things get crazy on the upside.

We are now 40%-45% in cash, which is as high as we want to go. Some of this cash

will be put to work by scaling into non-gold (oil, gas and industrial-metal)

commodity stocks, a process that has already begun and that has been reflected

in TSI commentaries over the past couple of weeks.

Also, we have begun to scale into GDX put options to partially hedge our core

exposure to the gold-mining sector. We will be happy to write-off these

insurance puts if it turns out that they aren't needed.

The Currency Market

The Dollar Index tested resistance at 97.5 on each of the first three trading

days of this week. If it ends the week above this resistance it will greatly

reduce the probability of a decline to the low-90s prior to the start of a rally

to new highs.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

![]()