![]()

![]()

![]()

![]()

- Interim Update 24th May 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Just how weak is the US

economic expansion?

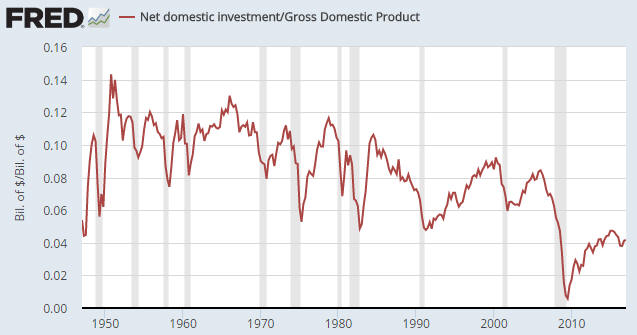

TThe following chart

encapsulates what's wrong with the US economy and why it will continue to

deteriorate on a long-term basis unless Keynesian monetary and fiscal

policies are abandoned.

The chart shows that US Net Domestic

Investment* oscillated between 6% and 12% of nominal GDP until the

late-1970s, with moves outside this range being short-lived. From the

late-1970s to the present, however, it has been in a downward trend and at

no time since the final quarter of 2007 has it been above 6%. Furthermore,

from the early-1950s through to 2007 it never fell below 4.8%, even at the

depths of the worst recessions. And yet eight years into the current

economic expansion the level is only 4.2%.

According to the "Austrian" school of economics, the downward trend in

Net Domestic Investment relative to GDP can be explained by the

combination of a) Federal Reserve manipulation of interest rates and money

supply that caused the economy to careen from boom to bust and caused vast

amounts of capital to be consumed via the countless ill-conceived

investments that were incentivised by the manipulation, b) increased

government spending (the more the government diverts resources to its own

uses, the less opportunities there will be for the private sector to

invest in new business ventures and technologies), and c) regime

uncertainty (the more unpredictable the actions of an interventionist

government the more reticent the private sector will be about making

long-term investments).

The "Austrians" are right.

Of the

aforementioned contributors to the decline in the amount of investment in

future growth, the first (the machinations of the Fed) has been by the far

the most important until now. That's why the downward trend accelerated in

2007. It was in 2007 that the real-estate-related investment boom fueled

by the Fed began to unravel in earnest, leading to a financial crisis and

recession that prompted a new round of monetary manipulation that was

unprecedented in its aggression and relentlessness. In effect, the doctor

prevented a proper recovery by numbing the patient with a large and

never-ending flow of morphine.

Unfortunately, with a central bank

chief who believes that monetary stimulus has helped support the economy

and a

president who believes that the government should "prime the pump",

there is no chance of the policies that brought about the economic decline

being abandoned anytime soon.

*Net Domestic

Investment is total investment minus the investment needed to maintain the

existing capital stock. It is the investment that leads to growth in

productivity and, therefore, to real economic progress.

The Stock Market

The US

Although the S&P500 Index (SPX) ended the 24th May session at an all-time

closing high, it hasn't yet decisively broken above its 1st March high.

For all intents and purposes it has now spent almost three months trading

sideways.

With the benefit of hindsight we know that the 17th May plunge was not

the warning shot it initially appeared to be. It didn't change or signal

anything of significance. The market (the SPX) now has an opportunity to

effect an upside breakout, but note that it has just risen for five days

in a row and is acutely vulnerable to a negative catalyst.

The

steel sector of the US stock market is worth featuring today because it is

in a position where a modicum of additional strength would signal the end

of a multi-month decline. We are referring to the fact that the VanEck

Vectors Steel ETF (SLX) ended Wednesday's session at the top of a

well-defined downward-sloping channel that began to form three months ago.

A daily close above $38.60 would break SLX above its channel top and

its 50-day MA. This would be more of a problem for our bearish outlook

than a new high in the SPX, because SLX is economically-sensitive and is

not being supported by the handful of large-cap market darlings

("TFAANNG": Tesla, Facebook, Amazon, Apple, Netflix, Nvidia and Google)

that has kept the SPX near its all-time high.

Gold and the Dollar

Gold

Over the past 5 days the US$ gold price has moved in a narrow range

slightly below lateral resistance in the low-$1260s and slightly above its

50-day and 200-day MAs. This price action leaves the door open to a

near-term test of the April high.

In euro terms, however, the gold price is well below its 50-day and

200-day MAs and is desperately trying to hold lateral support defined by

its March low (the equivalent of US$1195).

The difference between gold's recent performance US$ terms and gold's

recent performance in euro terms is bearish. It doesn't preclude a rise in

the US$ gold price to the vicinity of its April high within the coming

week or so, but it is consistent with the view that near-term strength

would prove to be fleeting and would be followed by a decline to new

multi-month lows.

Gold Stocks

Current Market Situation

The HUI

may have made a rebound peak last week, but with gold retaining the

potential to test its April high there is still a realistic chance of the

HUI moving up to 205-210 before commencing a decline that should take it

to a new low for the year and will possibly take it to a new 12-month low.

One of the main reasons to expect the HUI to make a new low for the

year within the coming two months is the performance of the HUI/gold

ratio. As illustrated below, this ratio has been making lower highs and

lower lows since February. This sort of performance by the HUI/gold ratio

is usually followed by significant short-term weakness in both gold and

the HUI.

Gold stocks for a multi-month trade

The stage is being set for an important low (probably the low for the

year) and an excellent buying opportunity in the gold-mining sector during

June-July. Our guess at this time is that the low for the gold-stock

indices will occur in July, but it's reasonable to expect that individual

gold-mining stocks will bottom at different times and that some will

bottom by mid-June. In particular, some of the junior gold-mining stocks

that are adversely affected by the next quarterly rebalancing of GDXJ will

probably bottom by/on 16th June.

We intend to add two or more

gold-stock trading positions to the TSI list within the next two months in

anticipation of a rally lasting at least three months. The stocks we add

will ideally have all of the following attributes:

1) 'Oversold' on

a short-term basis

2) Under-valued in both absolute and relative

terms

3) Solid balance sheet

4) Low risk of a dilutive

equity financing

5) Likely to significantly outperform the

gold-mining ETFs during the next sector-wide rally

6) Likely to be

adversely affected by the mid-June GDXJ rebalance

To date we have

short-listed five gold-mining stocks for potential trades, two of which

are current members of the TSI List. In alphabetical order, here they are:

1) Asanko Gold (AKG)

AKG is producing gold at

the rate of about 235K-oz/year at Stage 1 of the Asanko Gold Mine (AGM) in

Ghana and has a plan to increase its production to about 450K-oz/year by

2020 (the Stage 2 Expansion).

There is a potential issue with the

resource estimate for Stage 1 of the AGM (the Nkran deposit), in that the

deposit possibly contains a lot less recoverable gold than assumed in the

mine plan. This risk is now widely known, which is why AKG has been much

weaker than GDXJ over the past six months.

The risk has been

mitigated by the stock's relative weakness and the fact that the mining

emphasis will shift over the next few years due to the Stage 2 Expansion.

Furthermore, it shouldn't prevent the stock from rebounding strongly from

whatever low is made over the next several weeks.

Our tentative

plan is to add a trading position in AKG in anticipation of a rebound to

at least US$3.00, although we haven't yet decided on a buy level. We would

probably be interested at US$1.75, but a lot will depend on the

Feasibility Study (FS) for Stage 2. The FS results are due on 5th June.

2) Continental Gold (CNL.TO)

CNL is developing

the high-grade Buritica gold project in Colombia. The project is just

entering the construction phase, with the company having received all

necessary permits and arranged all necessary financing.

We perceive

an uncomfortably-high risk that the Buritica project's resource model is

not accurate and therefore that the economics will not be anywhere near as

good as those estimated in the Feasibility Study (FS), but if that risk is

going to materialise it won't be until the project goes into production in

2020. It shouldn't be an issue over the next 6 months.

Assuming

that the FS economics are roughly correct, CNL offers good value near its

current price of C$3.44. However, to improve our risk/reward we are hoping

for the opportunity to take a position near where the stock was trading in

early-May -- just before it cleared the final financing hurdle. Such a

buying opportunity could arise due to the combination of sector-wide

weakness and the reduction in CNL's weighting within GDXJ.

Our plan

is to add a CNL.TO trading position to the TSI List at C$2.85 in

anticipation of a rebound to C$4.50-C$5.00.

3) Premier Gold (PG.TO)

PG is an existing TSI

stock and therefore needs no introduction. It has a strong balance sheet,

about 130K-oz/year of current production, ample leverage and an attractive

valuation. It will also be vulnerable to the effects of GDXJ selling prior

to mid-June.

Our plan is to add a PG.TO trading position to the TSI

List at C$2.30 in anticipation of a rally to around C$4.00.

4) Ramelius Resources (RMS.AX)

Like PG, RMS is

an existing TSI stock and therefore needs no introduction. Also like PG,

it has a strong balance sheet, about 130K-oz/year of current production,

ample leverage, an attractive valuation and a vulnerability to the effects

of GDXJ selling prior to mid-June.

Our plan is to add an RMS.AX

trading position to the TSI List at A$0.33 in anticipation of a rebound to

the A$0.50s.

5) Sandstorm Gold (SAND)

SAND is a mid-tier

royalty/streaming company. Unlike the stocks of the large

royalty/streaming companies (Franco Nevada and Royal Gold), SAND shares

offer good value. However, to get the sort of leverage to a general

gold-sector rebound that we are looking for our purchase price will have

to be significantly below the current level. Anything in the US$2.50-$2.75

range would probably work well.

At this stage our plan is to add a

SAND trading position to the TSI List at US$2.60 in anticipation of a

rebound to US$4.00-$4.50, but it might turn out that we are being too

stingy and will have to raise our buy price. We will see how it goes, but

anything under US$3 would be reasonable.

The Currency Market

A routine counter-trend

rebound in the Canadian dollar (C$) would have stopped at around 74, but

with Wednesday's strength the C$ has moved a little beyond this target.

This could be nothing more than an extension to the pattern of the past 12

months -- a pattern that involves breaks to new lows being quickly

followed by upward reversals and recoveries to either the 200-day MA or

the top quartile of the channel drawn on the daily chart displayed below.

If so, the C$ has no more than 1 point of additional short-term upside

potential.

Our guess is that the C$'s intermediate-term downward trend will

resume within the next several days and won't end until July-August.

However and as mentioned in the latest Weekly Update, the C$'s

extraordinarily bullish COT situation opens up the possibility that the

early-May low will turn out to be the low for the year.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() New

TSI Stock Selection: Cordoba Minerals (TSXV: CDB). Shares: 89M issued, 96M

fully diluted. Recent price: C$0.77

New

TSI Stock Selection: Cordoba Minerals (TSXV: CDB). Shares: 89M issued, 96M

fully diluted. Recent price: C$0.77

We hadn't planned to

add more exposure to copper to the TSI List until the third quarter of

this year, because there's a good chance of further weakness in the price

of copper and the prices of copper-mining equities over the coming three

months. However, the recent sharp decline in CDB's stock price has

established the sort of intermediate-term risk/reward that shouldn't be

ignored. We perceive additional downside risk of around 20% versus upside

potential of at least 100%.

CDB is effectively Robert Friedland's publicly-traded vehicle for

minerals exploration/development in Latin America. Friedland's private

company High Power Exploration (HPX) is earning 65% of CDB's

district-scale San Matias copper-gold project in Colombia by paying all

costs to advance the project to the point where it has a completed

Feasibility Study (FS). Also, HPX owns about 37% of CDB.

The FS

that HPX is currently funding will focus on the Alacran copper-gold

deposit, a medium-grade copper-gold porphyry. According to the initial

Inferred resource reported in early-January, the deposit contains 827M

pounds of copper at an average grade of 0.70% and 644K ounces of gold at

an average grade of 0.37-g/t.

Based on the above-mentioned resource

and the fact that it will end up with only a 35% stake, CDB is far from

cheap at its current market cap of C$68M. The reasonable expectation,

however, is that the resource will get much bigger with additional

exploration. Friedland certainly wouldn't be interested unless there was

multi-billion-pound potential.

As well as the strong potential to

host a large, economically-viable medium-grade copper deposit, there are

signs that the project hosts a significant quantity of high-grade gold. In

fact, the stock's extreme volatility over the past 5 months was mostly

about this high-grade gold opportunity, with a single spectacular gold

intercept of 0.9m averaging 4,440-g/t in January propelling the stock from

the C$0.90s to the C$1.50s and subsequent drilling results that failed to

duplicate the success leading to the recent collapse.

We like the

chances of additional spectacular gold intercepts being reported, but our

CDB speculation doesn't depend on them. It depends on the ability of the

CDB-HPX joint venture to define a large, medium-grade copper-gold porphyry

with good economics.

In addition to recent drilling results that

didn't meet the high expectations of some shareholders, the stock has

probably been under pressure due to the likelihood of an equity financing

in the near future. The company only has about C$1M of working capital and

will therefore need to raise more money soon, but it won't need to raise a

lot of money because HPX will be paying all project exploration and

engineering expenses for the foreseeable future.

Our suggestion is

to take an initial position in CDB near its current price of C$0.77 and be

prepared to average-in over the next few months.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://bigcharts.marketwatch.com/

http://research.stlouisfed.org/

![]()