![]()

![]()

![]()

![]()

- Interim Update 24th June 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The Stock Market

In the latest Weekly Update we

concluded the US stock market discussion as follows:

"Due to

the bearish fundamentals, the news-related risks and the extent to which

prices became stretched to the upside a couple of weeks ago, this is a

time to be very cautious. However, due to the on-going deluge of money and

the mixed sentiment situation, it is not a time to be aggressively

bearish.

We continue to anticipate a short-term correction that

(for the SPX) probably will be limited to a 50% retracement of the rally

from the March low."

Although there was a significant price

decline on Wednesday 24th June, the overall picture is unchanged. We are

anticipating a short-term decline in the SPX to 2700-2800, but to signal

that something more than a minor multi-week consolidation is underway the

SPX will have to break below 3000. It ended Wednesday's session at 3050,

which happens to be slightly above the psychologically-important 200-day

MA.

The Russell2000 ETF (IWM), which is the focus of our current bearish

speculations (the TSI Stocks List contains an IWM October-2020 put option

and our own account contains IWM put options with August-2020 and

October-2020 expiry dates), is in a weaker position than the SPX. It broke

below its 200-day MA and important lateral support during the week before

last, tested its downside breakout last week and resumed its short-term

downward trend on Wednesday 24th June. We are anticipating a decline to

$125 or lower.

Gold and the Dollar

Gold

During the first half of this week the US$ gold price briefly traded at a

new multi-year high and then pulled back. This has created the appearance

of a successful test of the April-2020 high.

In euro terms the gold price is yet to test its April-2020 high, but

on Tuesday of this week it broke above its 50-day MA. This is a positive

development.

According to the mainstream press, strength in the US$ was to blame

for gold's price reversal on Wednesday. The problem with that reasoning is

that over the past year the US$ gold price has been positively correlated

with the Dollar Index more than half the time. This is illustrated by the

following chart.

The US dollar's exchange rate is just one of

several drivers of the gold price. Weakness in the DX generally will be

associated with strength in the US$ gold price if all things remain equal,

but all things rarely remain equal.

Rather than being due to any particular fundamental development,

inter-market relationship or news, it's most likely that Wednesday's

reversal in the US$ gold price was driven by technically-oriented selling

by speculators after important resistance (the April high) was reached.

We think that gold will break above its April-2020 high within the

next few weeks, perhaps following some consolidation in the $1750-$1780

range. However, at this time we aren't anticipating a major rally to

all-time highs (the all-time high was around US$1925 in 2011). Our guess

is that gold's next short-term peak will be in the $1815-$1850 range,

although much will depend on the progress (or lack thereof) with regard to

reopening economies and developing effective COVID-19 treatments. The

slower the progress, the greater the demand for the safety offered by

gold.

Silver

At this stage, silver's

correction from its early-June peak looks similar to the correction that

unfolded during April-May. To maintain the similarity, the silver price

(basis the July-2020 futures contract) will have to hold above $17.00

during additional corrective activity over the days ahead.

We think

that silver has short-term upside potential of $2-$3 and short-term

downside risk of $2-$3, resulting in a neutral risk/reward. However, on an

intermediate-term basis the potential reward is much greater than the

risk.

Gold Stocks

Over the first three days of this

week the HUI broke above its 50-day MA, tested long-term resistance at 286

(the 2016 high) and then pulled back to its 50-day MA. This price action

is constructive and is more evidence that the gold sector's correction is

complete.

That being said, there is significant short-term risk in

the gold mining sector due to the mounting evidence that the broad stock

market is in the early part of a correction that could take the SPX down

by as much as 10%. It's hard to imagine that the HUI and the gold mining

ETFs would remain above their recent lows if the SPX were to suffer a

quick decline to 2700-2800.

Ideally (from a short-term bullish perspective) the HUI will remain

above its 50-day MA on a daily closing basis during pullbacks over the

days ahead, but last Thursday's low (256) should be viewed as critical

support. Breaching this support probably would be followed by a quick

decline to the vicinity of its 200-day MA (around 230), which, assuming no

major change in the fundamentals, would offer both short-term and

long-term traders an excellent opportunity for new buying.

The Currency Market

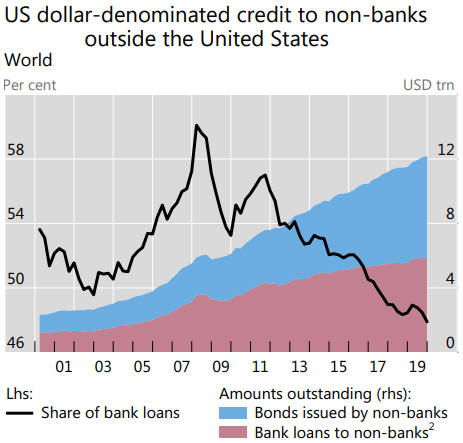

Revisiting the global US$ short position

Financial market

discussions and analyses often focus on fundamental issues that don't

matter, or at least don't provide useful clues regarding the likely future

performance of the market in question. A good example is the so-called

"global US$ short position", which is regularly cited in support of a

bullish outlook for the US$.

The argument is that the roughly $12

trillion of US$-denominated debt outside the US constitutes a short

position that will create massive demand for dollars and thus put

irresistible upward pressure on the Dollar Index (DX). There is an element

of truth to the argument, but the "global US$ short position" always

exists. It exists during US$ bull markets and it exists during US$ bear

markets. Furthermore, the shaded area on the following chart shows that it

steadily increases over time and that even the 2008-2009 Global Financial

Crisis resulted in only a minor interruption to the long-term trend.

Consequently, it isn't a major intermediate-term or long-term driver of

the US dollar's exchange rate.

Source:

https://www.bis.org/statistics/gli2004.pdf

The element of truth

to the "global US$ short position" argument is that a significant

strengthening of the US currency relative to the currencies of other

countries will increase the cost of servicing dollar-denominated debt in

those countries. This lessens the ability to borrow additional US dollars

and puts pressure on existing borrowers to reduce their US$ obligations.

In effect, it leads to some short covering that magnifies the upward trend

in the US dollar's exchange rate. This means that while the "global US$

short position" won't cause the US$ to start strengthening, it can

exacerbate a strengthening trend.

We mentioned above that there is

no empirical evidence that the "global US$ short position" drives major

trends in the US dollar's exchange rate, but that doesn't guarantee that

the pile of US$-denominated debt outside the US won't become an important

exchange-rate driver in the future. The reason that it won't become

important in the future is that prices are driven by CHANGES in supply and

demand. The US$12T+ of foreign dollar-denominated debt represents part of

the existing demand for dollars, meaning that the demand-related effects

of this debt on the dollar's exchange rate are 'in' the market already. At

the same time, the total supply of dollars is growing rapidly.

At

this point it's worth addressing the idea that the Fed would be powerless

to stop the US$ from appreciating if a major 'debt deflation' got

underway. This is nonsense. Until the law of supply and demand is

repealed, someone with the unlimited ability to increase the supply of

something WILL have the power to reduce the price of that thing.

The Fed's power to reduce the relative value of the US dollar was

demonstrated in spades over the past few months. The major

financial-market panic and economic collapse of March-2020 predictably

resulted in a desperate scramble for US dollars, leading to a fast rise in

the DX. However, it took the Fed only two weeks to overwhelm the surging

demand for dollars with a deluge of new dollar supply.

The upshot

is that the so-called global US$ short position is not a valid reason to

be a US$ bull.

The fundamentals that

matter

The "global US$ short position" always exists and

inevitably increases over time, so its existence doesn't determine the US

dollar's performance relative to other currencies. What, then, does

influence the performance of the Dollar Index (DX) over intermediate-term

timeframes?

As discussed in many previous TSI commentaries, it

seems that the most important fundamental drivers of the US$/euro exchange

rate, and therefore the most important fundamental drivers of the DX

(since US$/euro is about 60% of the DX), are US equities relative to

European equities and the US-Europe interest rate differential. We use the

SPY/EZU ratio to measure the former and the 10yr T-Note yield minus the

10yr Bund yield (UST10Y-DET10Y) to measure the latter.

The

following chart compares the DX with the above-mentioned drivers over the

past eight years.

We consider the fundamental backdrop to be

bullish for the DX when both fundamental influences (the SPY/EZU ratio and

the US-Germany yield differential) are in upward trends, neutral when the

fundamental influences are trending in opposite directions and bearish for

the DX when both fundamental influences are in downward trends. On the

following chart, the US dollar's fundamentals are deemed to be neutral

during Periods A and E, bullish during Periods B and D, and bearish during

Period C.

Note that even though the fundamental backdrop has been neutral for

the DX since late-2018, the DX has had an upward bias during this period.

This suggests that relative equity strength is more important than the

interest rate differential. That being said, the DX is less than one point

higher today than it was in late-2018, so the upward bias did not lead to

a meaningful net gain.

Also note the pronounced downward reversal

in the relative equity strength indicator over the past three months. This

is part of why we think that the DX made a multi-year top in March-2020.

Current Market Situation

The DX made a multi-week bottom about two weeks ago and has since been in

correction (countertrend rebound) mode. We are intermediate-term bearish

on the DX, but we expected this rebound.

The DX's short-term

risk/reward is neutral, with upside potential to around 98.5 and downside

potential to around 94.5 (the March-2020 low). It's likely that the

March-2020 low will be breached before year-end, but not until the final

quarter. In the meantime we are looking for a choppy market, with

multi-week periods dominated by risk-off sentiment giving the DX a boost

and multi-week periods dominated by risk-on sentiment pushing the DX

downward.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Mosaic

(MOS) stopped out

Mosaic

(MOS) stopped out

MOS closed below its trailing stop loss

on Wednesday 24th June and has been removed from the Stocks List. The

result was a loss of 37%.

This is another stock that we expect to

return to the List in the future. It could return as a long-term position,

because it's a good fit with one of our long-term investing themes (owning

fertiliser stocks as a way of profiting from rising prices for

agricultural commodities during 2020-2022).

Changes to the

TSI Small Stocks Watch List (SSWL)

Changes to the

TSI Small Stocks Watch List (SSWL)

The SSWL is a list of stocks that are too risky and/or illiquid to be

considered for the TSI Stocks List. We don't track these stocks closely in

the TSI commentaries, but they have favourable risk/reward ratios (in

general: high risk versus much higher potential reward) and could be of

interest to speculators who are able to do their own due diligence. Today

we are deleting two stocks from the SSWL.

The first deletion is

Artemis Resources (ARV.AX), an exploration-stage gold, copper and cobalt

miner. This company has several "irons in the fire", but the only one of

real interest to us was its 50/50 JV with Novo Resources (NVO.V) at the

Purdy's Reward conglomerate gold prospect near Karratha in the northern

part of Western Australia.

ARV's stock price has 'perked up'

recently, but the company has exited its JV with NVO so the main reason

for our interest in the stock no longer exists. Therefore, it has been

removed from the SSWL.

The second deletion is Cassini Resources

(CZI.AX). CZI owns 30% of the West Musgrave Project (WMP), a large,

low-grade base metals (nickel and copper) project in Western Australia, as

well as some much smaller and earlier-stage exploration projects. Oz

Minerals (OZL.AX) owns the other 70% of the WMP.

We originally

brought CZI to the attention of our readers in October-2016, when it was

trading at A$0.05. We thought that the stock market was substantially

under-valuing CZI's 30% stake in the WMP and that OZL eventually would

make a takeover bid in order to consolidate its ownership of the project.

It was a long time in coming, but a deal has been done for OZL to purchase

CZI.

Under the deal, each CZI share will be exchanged for OZL

shares with a current market value of about A$0.15, A$0.01 of cash and a

share of a new company called Caspin Resources. Caspin will own CZI's

non-WMP exploration-stage assets -- 80% of the Yarawindah Brook Ni-Cu-PGE

project and 100% of the Mt Squires Au-Ni-Cu project.

We estimate

the value of OZL's bid to be A$0.18-A$0.19. The stock is currently trading

at A$0.16.

From our perspective, the CZI story has ended as

originally expected. Therefore, the stock has been removed from the SSWL.

It would be reasonable for CZI shareholders to sell their shares on

the market or hold for the takeover consideration. Selling now could make

sense for risk management purposes, but holding for completion of the

takeover would provide ownership of a nearly-free lottery ticket in the

form of Caspin shares.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

![]()