![]()

![]()

![]()

![]()

- Interim Update 25th March 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Potential platinum

supply shock

Commodity supply disruptions

resulting from measures implemented to prevent the spread of the

coronavirus could lead to huge price rises in some commodities, especially

since supply disruptions will collide with government efforts to stimulate

demand. The platinum market could be affected more than most, for two

reasons.

The first reason is that earlier this week the

South African government announced a 21-day lock-down commencing at

midnight on 26th March. This means that for the next three weeks all of

the country's mines will be closed. Since South Africa (SA) produces about

75% of the world's platinum, this will be a significant supply disruption

for the platinum market (unlike the gold market, current mine supply is

critical to total supply in the platinum market). Furthermore, a

significant supply disruption could turn into a major supply shock if the

lock-down is extended.

As an aside, something similar could happen

in the copper market due to the temporary closure of mines in Chile and

Peru. About 30% of the world's copper production comes from Chile and

another 10% comes from Peru.

The second reason is the extent to

which the platinum price was beaten down over the past month. In addition

to hitting a 17-year low in dollar terms and an all-time low in gold

terms, platinum traded at its lowest price in more than 20 years relative

to the Industrial Metals Index (GYX).

We suspect that platinum's

relative cheapness combined with its supply vulnerability will result in

the metal trading at a MUCH higher price within the coming 12 months. In

the short-term, the sort of price crash experienced by platinum over the

past several weeks typically would be followed by a strong rebound and

then a pullback to test the crash low.

The TSI List has exposure to

platinum via PPLT (the Physical Platinum ETF), which was added early last

week.

The Stock Market

The following daily chart shows

that the number of individual NYSE-traded common stocks making new

12-month lows has collapsed from more than 1200 on 12th March to only 34

on 25th March. This means that the majority of stocks bottomed about two

weeks ago, even though the NYSE Composite Index and most other US stock

indices made new multi-year lows on Monday of this week. The positive

divergence between the market internals and the indices that developed

during 12th-23rd March set the stage for a strong rebound.

We wrote in the latest Weekly Update and in last week's Interim Update

that it was reasonable to expect a rebound that retraced about half the

decline from the February peak after a short-term bottom was in place.

This would be regardless of the market's long-term prospects. For example,

if last week's S&P500 (SPX) low of around 2300 had been the crash low then

the retracement target would be around 2850.

Due to this Monday's

new low near 2200, the most plausible target for a rebound is 2800. As

illustrated by the following daily chart, 2800 is slightly below lateral

resistance.

Depending on the news backdrop, the expected rise to around 2800 could

happen within two weeks or it could be a drawn-out affair involving an

early-April test of this week's low. The huge amount of money being

created out of nothing by the Fed and the $2T stimulus package being

rushed through the US parliament put the odds in favour of the former

(quick rise) scenario, but more bad news on the coronavirus front could

result in the latter scenario.

Gold and the Dollar

Gold

Claims of a gold shortage are not only wrong,

but also dangerous

As always happens when there is a sharp

decline in the gold price, there recently was chatter on the internet

about the price action not being consistent with 'evidence' of a shortage

of physical gold. These periodic claims about a shortage of physical gold

are always wrong. Also, in one important respect they are dangerous.

There can never be a shortage of physical gold because almost all of

the gold that has been mined throughout history is still around in

saleable form today. Every year the gold mining industry makes a small

addition to the existing aboveground stockpile (the stockpile grows by

about 1.5% per year thanks to mining), but the aboveground stock is so

large relative to the amount of annual production that even if the entire

gold mining industry were to shut down there would not be a shortage of

physical gold.

Of course, there can be a temporary shortage in

parts of the world of some items that are made from gold. For example,

coin dealers can't afford to maintain in their stores a large volume of

every different type of gold coin, so they predict what they will sell

within the ensuing few months and stock up accordingly. Sometimes they run

out of stock due to an unexpected increase in demand for certain coins,

which leads to new orders being placed at the local mint. It takes time

for the mint to fill these orders and during this period it will not be

possible for some prospective buyers to obtain the coins they desire, at

least not at reasonable prices. There also will be times when the coin

dealers stock up on particular items in anticipation of demand that

doesn't materialise.

Neither the situation where coin dealers are

temporarily out of stock nor the situation where coin dealers have an

unusually large amount of unsold inventory indicates anything about the

overall supply of and demand for physical gold.

As mentioned above,

it simply isn't possible for there to be a genuine shortage of physical

gold. However, it is possible that at some point the vast majority of gold

owners will refuse to exchange their gold for dollars. Although this could

create the impression that there is a major shortage of gold, this

impression would be false. Rather than indicating a lack of physical gold

supply, it would indicate a lack of demand for dollars. To explain using

an absurd example, a man who wants to buy physical gold using Monopoly

money will find no takers, not because there isn't plenty of gold

available for sale but because nobody wants to exchange their gold for

Monopoly money.

The situation described in the above paragraph

would be foreshadowed by persistent and large backwardation in the gold

futures market. That is, for an extended period of time the spot price of

gold would be well above the price of the nearest futures contract and the

nearest futures contract would be priced well above the distant contracts.

That is not the current situation. Currently, the gold futures curve is

almost flat, but with a slight upward slope. Given that short-term US

interest rates are near zero, this is not in any way strange or indicative

of a lack of demand for US dollars. On the contrary, it indicates that on

a global market-wide basis there is ample physical gold supply to meet the

demand being expressed by the holders of dollars. That being said, the

gold futures curve has flattened over the past few days, which indicates

that the recent surge in the gold price had more to do with the buying of

physical gold (400oz and 1kg bars, not coins*) than the speculative buying

of gold futures. It's a similar story in the silver market.

We

mentioned near the start of this discussion that claims of a shortage of

physical gold are dangerous as well as wrong. Such claims are dangerous

because the most popular argument against returning to gold as money (the

general medium of exchange) is that there is insufficient gold in the

world. According to apologists for the current monetary system and

denigrators of earlier systems that were based on gold, the money supply

should be very flexible so that it can be rapidly expanded in times of

stress or simply to meet the needs of a growing economy. In effect, the

"goldbugs" who periodically assert that there is a shortage of physical

gold are saying to the gold haters: "You are right! We should never go

back to having gold as money because if we did we eventually would end up

with a severe shortage of money."

In summary, there will never be a

shortage of physical gold. There could, however, be a shortage of gold

available to be exchanged for fiat currency, but that's not the situation

today.

*The public's demand for gold coins

is such a small part of the overall market for physical gold that it

generally won't affect the spot price of gold.

Current Market Situation

In the

email sent to subscribers after this Monday's US trading session, we wrote

that the Fed had ramped up its efforts by committing to buy almost

anything (using money created out of nothing, of course) and that it was

getting involved in direct lending to businesses of all sizes. Also, we

pointed out that this new cunning plan had boosted inflation expectations

and in doing so reduced the real US interest rate (the real interest rate

is the nominal interest rate minus the EXPECTED rate of currency

depreciation), causing the fundamental backdrop to shift in gold's favour.

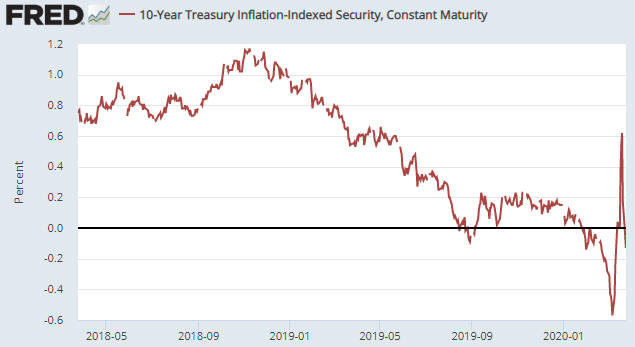

The following chart of the 10-year TIPS yield, a proxy for the US real

interest rate, illustrates what we were talking about. Notice that the

TIPS yield was around negative 0.60% in early-March but then rocketed

upward. This was in response to the collapse in inflation expectations.

Last Thursday (19th March) it was around positive 0.60%, which was close

to a 12-month high, but then inflation expectations began to rise and the

TIPS yield was pushed back into negative territory.

In the same email we wrote that the actions being taken by the Fed

could put a higher floor under the gold price and enable gold to test its

Q1-2020 peak by May-2020. However, things are happening much faster than

expected. As it turned out, the plunge in the real interest rate was the

catalyst for the biggest 2-day rise in the gold price (in dollar terms) in

history, enabling a test of the Q1-2020 peak near $1700 during Tuesday's

frenetic trading session. Across the financial world, price moves that

normally take months are happening in days and price moves that normally

take weeks are happening in hours.

We doubt that gold will embark on a new intermediate-term advance

until there has been a more substantial reduction in speculator long

interest than has occurred to date. However, the on-going craziness of the

financial-market environment and the actions being taken by central banks

and governments make short-term forecasting more futile than usual.

Gold Stocks

We have written that the most

likely place for a countertrend rebound in the HUI to end is the area

between lateral resistance at 200 and the 200-day MA. The 200-day MA

currently is at 214-215. As illustrated below, the HUI reached the top of

the rebound's target range on Wednesday 25th March.

We can't be certain that the rapid rebound from the 16th March low is

a countertrend move, but that's the most prudent assumption until/unless

proved otherwise. Importantly, at this stage there is nothing in the price

action to suggest that we are dealing with something more bullish than a

reaction that will be followed by a decline to test the crash low. For

example, in 1987 the initial rebound in the XAU (the HUI didn't exist back

then) also involved a rapid rise to the vicinity of the 200-day MA.

In general, a crash is followed by a strong 1-2 week rebound and then

a multi-week decline that tests the crash low. A larger/longer upward move

then becomes a good bet, assuming that the test of the crash low is

successful. To indicate that this pattern is NOT being followed the HUI

will have to achieve consecutive daily closes above its 200-day MA.

The Currency Market

Volatility is still the

order of the day in the currency market.

During the two weeks prior

to this week the Dollar Index (DX) rocketed upward. In reaction to being

stretched to the upside late last week, we now have the inevitable

pullback.

A routine pullback would end at or above 100, while a

weekly close below 99 would suggest that last week's upside breakout was

yet another fakeout.

We still think that the next intermediate-term trend in the DX will be

to the downside, and in this regard we have the Fed on our side. The Fed

has gone completely bonkers (a technical term) and entered full-on dollar

destruction mode. The ECB is also completely bonkers, but that happened

several years ago. The big change is with the Fed.

The Fed is being

egged on in its mindboggling pursuit of "inflation" by many people who

should know better and undoubtedly will, at some point in the future,

complain about the long-term damage caused by the Fed in its efforts to

"support the economy" during the coronavirus panic of 2020. It is only

during times of crisis that you discover who are the genuine supporters of

free markets.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Short-term

trade suggestions

Short-term

trade suggestions

1) GDXJ

The idea

was to buy GDXJ at US$22.50 or lower this week, preferably near the open

on Monday. However, the Fed's announcement prior to the start of trading

on Monday lit a fire under the gold sector and prevented GDXJ from trading

near our targeted buy price. Consequently, this trade suggestion is

cancelled.

2) SLV May-2020 $14.00 call option

This call option was added to the TSI List last week and will be

exited if it trades at US$1.40. For the option to trade at $1.40 within

the next week the silver price probably will have to make an additional

gain of about $1.

3) GDX June-2020 $20.00 put option

The gold mining indices/ETFs have risen almost as far as they should

IF we are dealing with a typical post-crash rebound. Also, if we are

dealing with a typical post-crash rebound then the next significant move

should be a decline that tests the crash low. Due to the potential for

such a decline, the above-mentioned GDX put option will be added to the

TSI List.

The option last traded at US$0.79 and ended with a

bid-ask spread of US$0.53-US$0.90. We will use the mid-point of this

spread (US$0.72) as our entry price.

Note that this trade idea is

most appropriate for those who have substantial exposure to gold mining

stocks, that is, for those who are well and truly covered in case the gold

mining rally continues.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://research.stlouisfed.org/

![]()