![]()

![]()

![]()

![]()

- Interim Update 25th October 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Investing in bubbles

Many assets show signs of being

immersed in bubbles right now. The most obvious example is the

cryptocurrency speculation, which includes Bitcoin, the numerous and

rapidly-multiplying Bitcoin alternatives and, more recently, the stocks

that are involved in cryptocurrency 'mining'. Other examples are the broad

US stock market, the stocks of companies involved in social media and/or

e-commerce, the market for junk bonds, and a group of junior mining stocks

where just the hint of a possible discovery has led to spectacular price

gains and market capitalisations that bear no resemblance to current

reality.

The most enthusiastic participants in each bubble believe

that although bubbles exist elsewhere, there is a special set of

circumstances that justifies the seemingly high valuations in the asset

that they happen to like. For example, many of the cryptocurrency

enthusiasts believe that the US stock market's valuation doesn't make

sense but that Bitcoin's valuation does, and many stock-market bulls

believe that the S&P500's current level is justified whereas Bitcoin's

valuation is ridiculous. However, the bubbles are all related in that they

all stem from the returns on traditional investments having been driven to

near zero by the actions of central banks.

Now, just because an

asset is immersed in an investment bubble doesn't mean that it should be

avoided. Buying something after it enters bubble territory can be very

profitable, because huge gains will often occur AFTER valuation reaches a

point where it no longer makes sense to a level-headed investor. The

problem is, if you 'know' that a particular asset is immersed in a bubble

then you will be constantly on the lookout for evidence that the bubble

has ended and that the inevitable implosion has begun. In effect, you will

constantly have one foot out the door and will be acutely vulnerable to

being shaken out of your position in response to a normal correction.

A related problem is that once something has entered bubble territory

the normal corrections tend to be vicious. Each correction will look like

the start of the ultimate collapse, so unless you are a true believer

(someone who believes so strongly in the story that they are oblivious to

the absurdity of the valuation) you will be unable to hold through. For

example, during the first half of September the Bitcoin price had a

peak-to-trough decline of about 40%. This looked at the time as if it

could be the first leg of a total collapse, but it turned out to be just a

short-term correction. Only a true believer in the cryptocurrency story

could have held through this correction.

Eventually, of course, a

vicious price decline turns out to be the start of a bubble implosion. The

true believers will naturally hold, thinking that it's just another bump

on the road to a much higher price. They will continue holding while all

the gains made during the bubble are given back.

An implication is

that you need to be a true believer to do phenomenally well from an

investment bubble, but if you are a true believer then you will be wiped

out after the bubble collapses.

Alternatively, you may decide to

participate in an investment bubble while knowing it's a bubble. In doing

so you may be able to generate some good profits, but in general you will

be too quick to sell. Therefore, while the bubble is in progress your

profits will pale in comparison to those achieved by the true believers,

although you will stand a better chance of retaining your profits over the

long haul.

The worst-case scenario is to be a non-believer and

non-participant in a bubble, but to eventually get persuaded by the

relentless rise in price that special circumstances/fundamentals justify

the valuation and that a large commitment is warranted. That is, to become

a true believer late in the game. This worst-case scenario is what happens

to most members of the general public.

What will the Fed

do in 2018?

Donald Trump will soon nominate

the next Fed chairman. The nominated person will be Powell, Taylor,

Yellen, Warsh or Cohn, each of whom is a Keynesian and a card-carrying

member of the political-economic-financial establishment. As a

consequence, regardless of who 'gets the nod' we can be sure that it will

be business as usual at the Fed. In other words, we can be sure that the

monetary policy-making course of the recent past will continue for at

least the next couple of years. We therefore don't have to wait for the

name of the next Fed chairman to be revealed to hazard guesses at what the

Fed will do in the future. So, what do we expect from the Fed?

Before getting to what we expect let's take a look at what the 'market'

expects. What the market expects the Fed to do on the interest-rate front

next year is encompassed in the price of the January-2019 Fed Funds

Futures (FFF) contract, since the price of this contract will be almost

100% determined by the expected level of the Fed Funds Rate (FFR) at the

end of 2018.

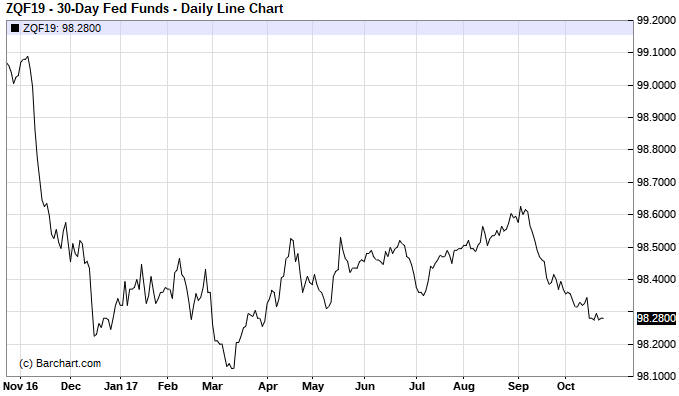

The following daily chart shows that the January-2019

FFF contract was recently priced at 98.28. Since the interest rate implied

by a FFF contract is 100 minus the price of the contract, this means that

the market expects the FFR to be about 1.75% at the end of next year.

The current level of the FFR is 1.00-1.25%, and unless something

dramatic happens between now and mid-December the FFR will end the year at

1.25-1.50% (a 0.25% Fed rate hike in December-2017 is a near certainty).

This means that the mid-point of the Fed's target range should be 1.375%

at the end of this year.

The implication is that currently the

market is expecting either one or two 0.25% rate hikes from the Fed in

2018. Is this reasonable?

We don't know, because what the Fed does

in the future will be determined to a great extent by what the stock and

bond markets do in the future. To put it another way, unless you know what

the stock and bond markets are going to do next year then you cannot

possibly know what the Fed will do next year. All you can do is guess.

Based on what we currently expect from the stock and bond markets, our

guess is that the Fed will make at least two rate hikes during the first

half of 2018 in response to rising inflation fear and then take at least

one of the hikes back during the second half in response to stock market

weakness.

The Stock Market

An 'overbought' extreme can

sometimes be more of a sign of strength than a sign of impending danger.

An example was discussed in the latest Weekly Update in relation to

the fact that on Friday 20th October the daily RSI of the Dow Industrials

Index hit its highest level since 1980. We noted that previous extreme

daily RSI readings for the Dow, where "extreme" is defined as above 80,

had in all but two (out of about fifteen) cases since 1980 been followed

by a routine short-term correction. The two exceptions occurred in

August-October of 1987 and January-March of 1994, when the Dow traced out

a crash pattern following the 'overbought' extreme.

Consequently,

if we don't see a crash pattern start to form over the next few weeks then

we should expect a surge to well above the current level within the coming

few months. The start of a crash pattern would involve a decline of 5%-8%

within the next 2-4 weeks followed by a rebound that retraced about half

of the decline from the peak.

Another topical example is Japan's Nikkei225 Index. When the Nikkei

dropped a little on Wednesday 25th October it ended an extraordinary

16-day winning sequence that took the daily RSI(14) to its highest level

since 1986.

It's likely that the 'overbought' extreme will usher in

some corrective activity, but the performance reflects strong and growing

demand for Japanese equities relative to what is, in effect, a shrinking

supply. Also worth mentioning is that the demand was strong enough

relative to supply to push the Nikkei through major resistance defined by

the 2015 peak as if this resistance didn't exist.

The supply of

Japanese equities is effectively shrinking due to the actions of Japan's

central bank. As part of its asset monetisation program the Bank of Japan

has been buying ETFs and now owns about 75% (by market value) of all ETFs

traded on the Tokyo stock exchange. This 'only' amounts to about 5% of the

total stock market, but a market-wide supply reduction of 5% is definitely

significant.

Gold and the Dollar

Gold

The

fundamental backdrop was gold-bearish at the end of last week and became a

little more so over the first three days of this week. The price action

has been uneventful, though, with a loss of only $1.50 from last week's

close to the close of trading on Wednesday 25th October.

There

continues to be important nearby support at $1260. This support has not

been seriously tested yet, but equivalent support in the gold-mining

sector has been decisively breached.

The recent performances of the

gold-mining indices suggest that bullion support near $1260 will not hold

for much longer. As noted in the latest Weekly Update, if this short-term

support gives way then a quick decline to intermediate-term support at

$1200-$1220 may follow.

There could be sizable reactions in the bond and currency markets to

the outcome of the ECB meeting later today. This implies that there could

also be a sizable reaction in the gold market to the same news.

As

far as we can tell, the most popular guess within the trading community is

that the ECB will announce that its bond-buying program will continue

through the first half of next year at half the current 60B euro/month

pace. However, there appears to be enough disagreement over what will be

announced and what it will mean that there could be significant reactions

in currencies and bonds -- and therefore in gold -- even if this is what

the ECB ends up doing.

Gold Stocks

In the

latest Weekly Update we wrote:

"The one thing that all the

gold-mining indices and ETFs have in common is that the decline from the

early-September high to the early-October low was much stronger than the

rebound from the early-October low. This suggests that in each case the

October rebound was a consolidation within a continuing downward trend and

that a drop to a new 2-month low will happen soon.

A drop to a new

2-month low wouldn't require significant additional weakness from here,

but there is the risk that a sizable 1-2 week decline will begin before

the end of this week. By "sizable" we mean a decline that takes the HUI

down to near support at 180 and GDX down to near support at $21, that is,

a decline of about 10%."

We now know for sure that the October

rebound was a consolidation within a continuing downward trend because all

the gold-mining indices and ETFs made new 2-month lows over the first

three days of this week. Perhaps more significantly, the HUI/gold ratio

also made a new 2-month low. In fact, the following chart shows that the

HUI/gold ratio is close to making a new low for the year.

The good news is that the weakness over the past three days caused the

gold-mining indices to become short-term 'oversold' for the first time

since early-July. The drop in the HUI's daily RSI to the low-30s (see

chart below) is evidence. This could be setting the scene for a tradable

rally to begin soon, but only if there is significant additional weakness

over the next several days.

To be clearer, we would not be keen on

trading a rebound that began from near the current level, at least not

with the fundamental- and sentiment-related information we have today.

However, a HUI decline of another 5%-10% within the coming week or so

could create an attractive risk/reward for a long-side trade in the

gold-mining ETFs even if the fundamental backdrop remains gold-bearish.

The Currency Market

Over the past two months

we've written often about the Canadian dollar (C$) and our expectation

that it would decline to the mid-70s before a sustainable low became a

realistic possibility. We haven't said anything about the Australian

dollar (A$) except that it was in a similar position to the C$ -- likely

to drop at least as far as the mid-70s before bottoming.

The A$ has

now retraced more than half the rally from its May low and is almost

'oversold' on a short-term basis. It has also reached the top of a price

range (76-77) where there is significant support. We should therefore be

alert for signs of a correction low.

Note that there probably won't

be a correction low until the total speculative net-long position in A$

futures has been reduced to almost nothing, but the COT information is

reported only once per week and with a 3-day lag. Evidence in the COT data

that the A$ is close to a bottom could therefore come after the price

action has signaled a bottom.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.barchart.com/

![]()