![]()

![]()

![]()

![]()

- Interim Update 26th July 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Commodities

The copper market

catches fire

The copper price surged to a 2-year high on

Tuesday 25th July and is now testing long-term resistance at $2.90-$3.00.

There were many guesses in the press about the reason for this week's

sharp price rise, including optimism about China's economic growth and

concerns about production at some of the world's largest copper mines.

What's our guess?

Our guess is that it was partly driven by

speculation regarding the increasing copper demand for use in electric

vehicles*. This is a long-term positive that shouldn't have a big effect

on the supply-demand balance anytime soon, but speculative enthusiasm

doesn't have to be firmly grounded in reality.

Whatever the reason,

it is clear that speculators have played the biggest role in this week's

rapid rise in the copper price. We say this because of the behaviour of

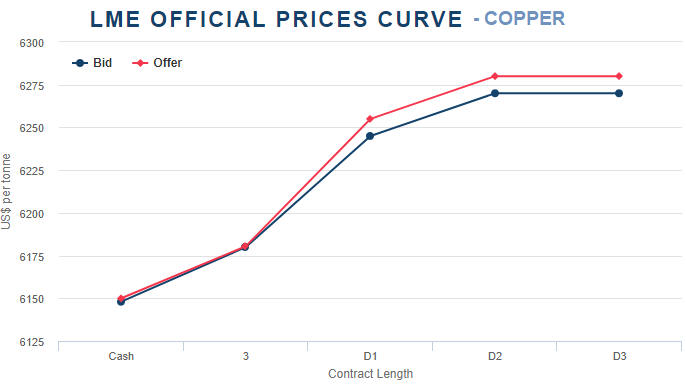

the "term structure" in the copper futures market. As illustrated by the

first of the following charts from the London Metal Exchange (LME) web

site, there continues to be a 'normal' upward slope over time in the

prices of copper futures, meaning that later-dated contracts are priced

higher than earlier-dated contracts. To put it another way, the copper

market is in a normal state of "contango". This means that there is no

current tightness of supply nor any expectation among commercial traders

that supply will tighten in the foreseeable future.

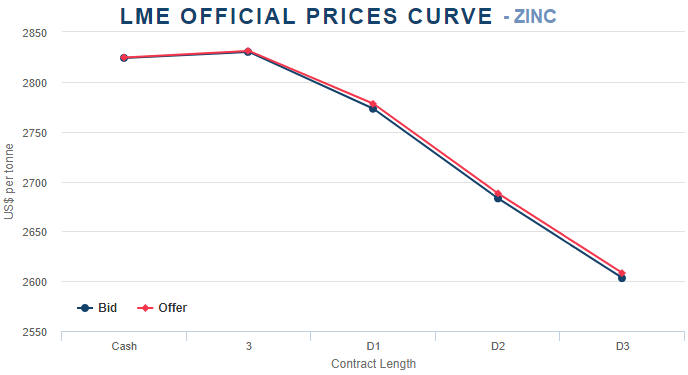

The second of

the following charts from the LME site shows the "term structure" of a

base-metal market with bullish fundamentals. This chart shows a downward

slope in the zinc futures curve, meaning that the zinc market is in

"backwardation". The implication is that in the zinc market there is

current tightness of supply and an expectation that the tightness will

persist.

The fact that the copper price is being driven upward by speculators

rather than commercial users doesn't mean that the price is close to an

important top (although it is probably nearing a multi-week top). First,

the speculators could be correctly anticipating a bullish change in the

fundamentals. Second, the latest COT data suggests that there is plenty of

additional scope for the build-up of speculative 'longs'.

We

highlighted the opportunity to bet on a short-term rise in the copper

price two weeks ago, with a particular focus on FCX (the world's largest

publicly-traded copper producer). FCX was trading at US$12.27 at the time.

We reiterated the opportunity a week ago, when FCX was trading at $13.11.

As illustrated below, in response to this week's gain in the copper price

the stock has rallied to $15.06.

For exposure to copper, Nevsun Resources (NSU) is another stock that

is worth mentioning at this time. Unlike the junior and mid-tier

copper-mining stocks that have already rocketed upward, NSU is still in

basing mode.

NSU offers exposure to two of the best -- based on our

expectation of what will happen to prices over the coming 6-12 months --

commodities, namely copper and zinc. Specifically, NSU is a current

producer of copper and zinc (mainly zinc) at its Bisha project in Eritrea

and owns one of the best exploration-stage copper projects in the world in

the form of the Timok Upper Zone (TUZ) in Serbia.

Due to the

country risk associated with Eritrea we have not considered owning NSU

shares over the past several years, but we estimate that well over half of

NSU's value is now linked to the newly-acquired (as of mid-2016) TUZ

project.

*We discussed this potential price driver in

the 19th June Weekly Update under the heading "Oil's loss will be copper's

gain".

More interested in buying weakness than selling

strength in oil

Our most recent comment on the oil market

was in the 10th July Weekly Update. At that time we wrote:

"If

the oil price bottoms near last week's [the 7th July] low and subsequently

moves up to around $50 then we will consider taking a new position in USO

(oil ETF) put options, but we have recently become more interested in

buying into oil-price weakness than selling or speculating bearishly into

oil-price strength. There are two reasons, the first of which is the

emerging evidence of a general financial-market shift in favour of

"inflation" plays such as industrial commodities. The second and more

important reason is that the rally in the Canadian dollar (C$) has

eliminated the main factor underpinning our bearish oil view."

The oil price did bottom near the 7th July low and has since moved up

to around $50, but for the reasons mentioned in the above excerpt from our

10th July report we have not taken a new position in USO put options.

There's still a realistic chance that the oil price will drop into the

$30s before reaching a sustainable price low, but the risk of this

happening is now smaller and the overall financial-market backdrop

indicates that our primary focus should be on building up long-side

exposure to industrial commodities. This includes oil, although we prefer

the industrial metals.

The Stock Market

Time for a VIX

speculation?

In the 10th May Interim Update we wrote:

"With the VIX at such a low level it is tempting to buy VIX call

options. At least, it would be if the options weren't so expensive.

VIX call options with a few months to expiry often seem expensive

because they are based on VIX futures prices rather than on the index

itself. For example, even though the VIX ended the 10th May session at

only 10.2, the October-2017 VIX futures contract ended the same session at

15.6. Consequently, if you were to buy October-2017 VIX calls right now

you would be buying calls that are priced on the basis of an underlying

index value of 15.6.

The large premium to the spot index at which

VIX futures contracts usually trade is the reason you will lose money

buying a volatility ETF/ETN such as VXX unless you get the timing exactly

right. These ETFs/ETNs are regularly rolling from relatively low-priced

nearer-dated contracts into relatively high-priced later-dated contracts,

leaking value as they go."

The VIX has since fallen from 10.2

to 9.6 (see chart below), but, more significantly for anyone interested in

trading the October-2017 call options, the price of the VIX October-2017

futures contract has since fallen from 15.6 to 13.4. This means that the

October call options are now a lot cheaper. For example, since 10th May

the price of the VIX October-2017 $15 call option has dropped from around

$3.00 to around $1.30.

At Wednesday's closing price of US$1.33 the VIX October-2017 $15.00

call options offer a good risk/reward, especially given that we are

entering the 3-month period of the year when the largest volatility spikes

have occurred in the past. If the stock market gets through the next three

months without a significant volatility spike then these options will lose

all of their remaining value and expire worthless, but we suspect that all

it would take to generate a 300%+ profit opportunity in the options would

be for the SPX to experience a 5%-10% decline prior to the 18th October

option expiry date.

Due to the attractive risk/reward, we have

added the VIX October-2017 $15.00 call option to the TSI List at US$1.33.

Keep in mind that in the absence of a significant volatility spike within

the next three months, the likely loss on this trade will be 100%.

Note that we do not suggest buying a VIX ETF or ETN. In our opinion, this

should be an option trade or no trade.

Gold and the Dollar

Gold

On

Wednesday the Fed did what we and most observers were expecting, which is

leave its targeted interest rates unchanged and continue to pave the way

for the start of a gradual balance-sheet reduction process. As we

mentioned in a

blog post

early this week: "Unless the stock market tanks in the meantime,

this balance-sheet reduction will probably be announced on 20th September

(following the FOMC Meeting) and kick off in October."

The

Fed's words prompted a minor positive reaction in the gold market. For

example, the following daily chart shows that the SPDR Gold Shares ETF

(GLD) ended the day with a gain of 0.8%. This small gain didn't alter the

chart pattern, though.

For the reasons mentioned in the latest Weekly Update (sentiment, the

gold-bullish shift in the fundamental backdrop and silver's positive

price-momentum divergence) we are open to the possibility that what was

originally expected to be a counter-trend rebound from the early-July low

will evolve into something more substantial. An upside breakout by the

gold-mining sector (see below) would indicate that we are dealing with

something more than a counter-trend rebound in the bullion market.

Gold Stocks

The gold-mining sector is now in a

very interesting position, in that over the coming few days it must either

break out to the upside or reverse downward. The reason is that GDX

reached the top of its contracting range on Wednesday 26th July.

As

illustrated by the following daily chart, GDX is essentially in the same

position now as it was when it reversed downward from multi-week highs in

April and June. Will it be different this time?

All it will take to generate evidence that it is different this time

is a daily close above Wednesday's intra-day high, meaning a daily close

above $23.06 for GDX and a daily close above 197.5 for the HUI. If upside

breakouts occur then the initial targets for the indices/ETFs will be the

February highs (220 for the HUI, $25.50 for GDX).

The

Currency Market

Different currencies have different types

of short- and intermediate-term drivers. For example, the A$ and C$ tend

to be so strongly influenced by commodity prices that almost nothing

matters except the commodity-price trend. For another example, over the

past two years the euro's performance against the US$ has been dominated

by the Germany-US 10-year interest-rate differential, although prior to

that it was most strongly influenced by the strength of European equities

relative to US equities. For a third example, refer to the following chart

showing the Yen and the US$ gold price.

Due to the performance of

the Yen having been so similar to the performance of the US$ gold price it

is reasonable to conclude that either the Yen is being driven by the gold

price or that the Yen and gold have some fundamental drivers in common.

The latter possibility is the more plausible, although we confess to being

puzzled by how tight the Yen-gold relationship has been over the past two

years.

Due to the strength of the positive correlation between the Yen and

gold, if you are bullish on the Yen you should probably buy gold. This is

because in all likelihood they will keep moving in the same direction, but

if the relationship breaks down it probably will be because the BOJ or the

Japanese government does something so stupid that the gold price shoots

upward while the Yen drops.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Removing

Cordoba Resources (CDB.V), adding Nevsun Resources (NSU)

Removing

Cordoba Resources (CDB.V), adding Nevsun Resources (NSU)

A

few weeks ago CDB.V announced a deal that worsened the risk/reward by

enough to make us want to remove the stock from the TSI List. We wrote

that we would remove the stock when it next traded above C$0.80, but we

have run out of patience and have decided to remove it at Wednesday's

closing price of C$0.77. At this price the trade ends with a break-even

result.

To maintain the same level of exposure to copper in the TSI

List we have added NSU as a trading position with an expected duration of

3-9 months. NSU was briefly discussed earlier in today's report, but here

are a few more details:

1) Based on a total current share count of

302M, NSU has a market cap of US$785M at the 26th July closing price of

US$2.60.

2) The company has a strong balance sheet, with no

long-term debt and US$196M of working capital at 31st March.

3) In

the June quarter the company's Bisha project produced 43M pounds of zinc

and 5.7M pounds of copper.

4) Based on a PEA completed in

March-2016, at a copper price of US$3.00/pound the TUZ project has an

after-tax NPV(8%) of US$1.55B and an IRR of 106%. At a more conservative

copper price of $2.40/pound the after-tax NPV(8%) is still a substantial

US$1.1B.

5) A PFS for the TUZ is scheduled for completion in

Q4-2017.

6) Our back-of-the-envelope valuation for NSU is

US$3.40/share at $2.40/pound for copper and US$4.10/share at $3.00/pound

for copper.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.lme.com/

![]()