![]()

![]()

![]()

![]()

- Interim Update 26th December 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

TSI Holiday Season

Schedule Reminder

- The Weekly Update that

would have been posted on Sunday 30th December (as per the normal

publishing schedule) will instead be posted on Tuesday 1st January. This

will allow us to incorporate the yearly closing prices into our

discussion/analysis.

- There will be no Interim Update on Thursday

3rd January.

- The normal TSI publishing schedule will resume with

the Weekly Update on Sunday 6th January.

The Lithium

Market

Monitoring the price of lithium

is not easy, because there is no lithium contract on the LME or any major

futures market. In other words, there is no benchmark. Instead, prices are

negotiated between producers and consumers on a case by case basis.

Further complicating matters is that the commonly-traded lithium comes in

two forms with different prices. There is Lithium Carbonate and Lithium

Hydroxide. A consequence is that information on lithium pricing often must

be obtained from the large producers or users of the commodity*.

Most lithium carbonate comes from lithium-containing brines, known as

salars, in Argentina and Chile. Salar brines are underground reservoirs

that contain high concentrations of dissolved salts (including lithium)

and generally are found below the surfaces of dried lakebeds. As explained

HERE,

to extract lithium from brines the salt-rich waters must first be pumped

to the surface into a series of evaporation ponds where solar evaporation

occurs over a number of months. When the lithium chloride in the

evaporation ponds reaches an optimum concentration, the solution is pumped

to a recovery plant where extraction and filtering remove any unwanted

boron or magnesium. It is then treated with sodium carbonate (soda ash),

thereby precipitating lithium carbonate. The lithium carbonate is

filtered, dried, and ready for delivery.

Lithium hydroxide, on the

other hand, is mostly extracted from spodumene and other minerals via

hard-rock mining processes.

The cost of producing lithium carbonate

from salars is generally much lower than the cost of producing lithium

hydroxide from hard-rock mines. However, the carbonate usually requires

further processing to make it suitable for batteries, whereas the

hydroxide can be directly used in batteries. Considering that batteries

for electric vehicles (EVs) should be the most important source of future

demand growth, this potentially gives the producers of the hydroxide a big

advantage.

Putting some numbers to the aforementioned advantage, a

30th November

article at mining.com notes:

"UK-based consultants Roskill

predicts annual growth of nearly 39% through 2031 for hydroxide compared

to 13% CAGR for lithium carbonate.

Total consumption of hydroxide

is expected to rise four-fold versus carbonate, with demand climbing to

1,605,500 tonnes and 460,100 tonnes respectively by 2031."

We

suspect that most consultants are greatly underestimating the rate at

which the production of EVs, and therefore the demand for lithium, will

grow over the next 7 years. As a consequence, the demand-growth advantage

of hydroxide is probably even greater than suggested by Roskill.

Even with much faster EV adoption than currently envisaged by most

analysts there shouldn't be a sustained shortage of lithium at any time.

The reason is that the lithium-mining industry is capable of ramping-up

supply in response to a rising price. For example, the steep upward trend

in the lithium price from Q1-2016 to Q1-2018 prompted a supply response

that led to a substantial price correction over the past three quarters.

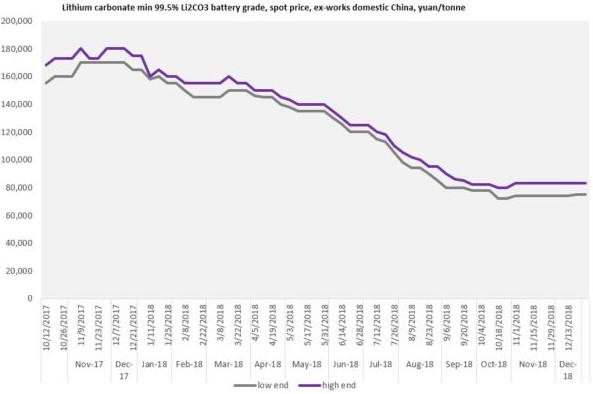

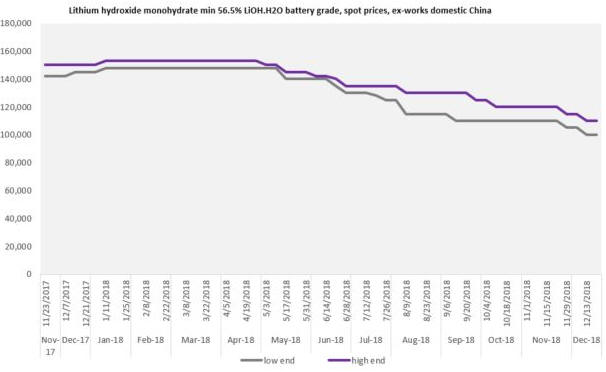

The price correction is illustrated by the following charts from

https://www.metalbulletin.com/lithium-prices-update, the first of

which shows the price of lithium carbonate (ex-works China) in yuan/tonne

and the second of which shows the price of lithium hydroxide (ex-works

China) in yuan/tonne.

Notice that the hydroxide price has held up

much better than the carbonate price. Specifically, notice that the low

end of the carbonate price range has moved from a 2018 peak of about

180,000 yuan/tonne (US$25,700/tonne) to 75,000 yuan/tonne

(US$10,700/tonne), while the low end of the hydroxide range has moved from

a 2018 peak of 155,000 yuan/tonne (US$22,100/tonne) to 100,000 yuan/tonne

(US$14,300/tonne). That is, hydroxide has gone from a 14% discount to a

33% premium.

Due to the demand-growth advantage of hydroxide over

carbonate it's a good bet that the hydroxide premium will continue to

increase, although the premium is limited by the fact that at some point

it would become more economical to convert lithium carbonate into a form

suitable for use in EV batteries than to purchase the battery-ready

lithium hydroxide.

Nothing is guaranteed and there is a risk that all the new investment

in lithium hydroxide production now happening in Australia will be more

than sufficient to cater for the coming increase in demand, but, as

mentioned above, we suspect that most forecasters are greatly

under-estimating the future EV-related demand for battery metals such as

lithium. We therefore like the idea of maintaining long-term exposure to

well-financed lithium hydroxide producers/developers such as Mineral

Resources (MIN.AX) and Kidman Resources (KDR.AX).

*For example, when Orocobre (ASX: ORE,TSX: ORL)

recently advised that its average selling price for lithium carbonate

was expected to be only US$10,800/tonne in Q4-2018, it was surprising new

information that caused a broad sell-off in lithium mining stocks.

The Stock Market

In the latest Weekly Update we

marveled at the extent to which the NASDAQ had become stretched to the

downside as measured by the number of individual NASDAQ stocks making new

12-month lows. We wrote:

"...on Thursday of last week...the

number of individual-stock new lows on the NASDAQ was a lot greater than

on any other day since the beginning of 1998 with the exception of during

the crescendo of the 2008 crisis and near the conclusion of the 1998

crisis."

Well, the situation became even more extreme on

Monday 24th December. As indicated by the thick blue line on the following

chart, at the close of trading on 24th December the 5-week MA of NASDAQ

New Highs minus NASDAQ New Lows dropped slightly below the lowest level

reached during the 2008 panic. In other words, by this measure the NASDAQ

was more stretched to the downside early this week than it was at the

crescendo of the Global Financial Crisis.

Other indicators currently aren't as extreme as the one displayed on

the above chart. For example, although the VIX got as high as 36 on Monday

of this week (see chart below) we are yet to get the sort of VIX spike

that usually marks the conclusion of a steep 10%-20% drop in the SPX.

Putting the VIX aside, it's extraordinary that the market has become

so 'oversold' only three months from a major peak. Either we are into a

bear market that will turn out to be the worst since the 1930s or the

entire decline is going to be over much sooner than expected. Both

possibilities are realistic, but it would be prudent to assume the former

and act accordingly until proven otherwise.

Turning to the price

action, volatility was extreme during the first two trading days of this

holiday-shortened week. The SPX plunged 2.7% to a new 12-month low on

Monday and then accomplished a spectacular 5% up-move on Wednesday.

Former intermediate-term support at 2500-2550 is now resistance and

probably will hold if tested over the next couple of weeks. This implies

that a lot of the near-term upside potential may have been exhausted on

Wednesday.

Thanks to a 6.2% surge on Wednesday, the NDX is already testing the

intermediate-term support (now resistance) that was breached last week.

In the discussion of the Oil Services ETF (OIH) in the latest Weekly

Update we wrote that the downward momentum extreme pointed to a 'W' bottom

rather than a 'V' bottom. A 'W' bottom would involve a low now/soon

followed by a rebound and then a test of the low during January or

February.

It's a similar story for the senior US stock indices.

Considering the extent to which these indices became 'oversold', 'V'

bottoms are less likely than 'W' bottoms. That is, assuming that at least

a 1-2 week bottom is now in place there should be a test of this week's

low prior to the start of a multi-month rally. That's regardless of

whether we are dealing with a new bear market or a substantial bull-market

correction.

Gold and the Dollar

Gold

Gold and the S&P500 (SPX) are at opposite ends of an investment seesaw.

They sometimes trend upward together or downward together due to changes

in the primary measuring stick (the US$), but when one is in a long-term

bull market the other will be in a long-term bear market. Which is in a

bull market and which is in a bear market can be established by charting

one relative to the other.

Here is a weekly chart of the gold/SPX

ratio going back to 1980. Crosses above and below the blue line on this

chart (the 200-week MA) have a near perfect record of indicating, in a

timely manner (for investors, not short-term traders), transitions between

gold bull and gold bear, with just one false signal caused by the 1987

stock market crash.

The gold/SPX ratio is now very close to

generating a bear-to-bull signal for gold and, by extension, a

bull-to-bear signal for the US stock market.

On Wednesday 26th December the US$ gold price rose to the $1280s in

response to fear of further weakness in the stock market. It then gave up

its gains as the stock market began to strengthen.

Although the

gold market is not 'overbought' and remains supported by constructive

sentiment and slightly-bullish fundamentals, Wednesday's market action

indicates that a 1-2 week top may be in place. However, the short-term

upward trend will be intact as long as the price doesn't close below

US$1240.

Taking into account sentiment, fundamentals, price action and the

expected performances of related markets (stocks, bonds and the US$), we

expect to see gold trading well into the $1300s during the first quarter

of 2019. However, as noted above we won't be surprised if there is a

multi-week correction/consolidation before significant additional gains

are made.

Silver

For the first time in many

months, silver's short-term chart pattern looks more bullish than gold's.

Of particular significance, on Wednesday 26th December the silver price

finally broke above resistance at $14.90 and sustained its breakout to

day's end. In doing so it appears to have completed a base.

Wednesday's breakout suggests that silver will trade up to at least the

$15.60s and possibly to $16.00 within the next few weeks.

We recently added the SLV $14.00 call option with an 18th January 2019

expiry date to the TSI List. SLV is priced about $1 below silver bullion,

meaning that a quick move by the silver price to $15.60-$16.00 should

result in the SLV price rising to $14.60-$15.00. If this were to happen

prior to 18th January then our options would trade at $0.60-$1.00. As

previously advised, for TSI record purposes the option will be exited if

it trades at $0.60.

Gold Stocks

The Gold

Miners ETF (GDX) has lateral resistance at $21.00 and resistance at the

top of its short-term channel (currently near $21.40). The most important

nearby support is at $19.80.

On Wednesday of this week GDX did

something similar to what it did a week earlier, which is rise to its

channel top and then reverse course. The 26th December downward reversal

was not as pronounced as the 19th December downward reversal, though, and

GDX ended the day exactly at its 200-day MA.

GDX's poor performance

relative to gold bullion on Wednesday suggests that the downward reversal

from the channel top marked at least a 1-2 week high. However, the

gold-mining ETFs and indices stand a good chance of making significant

additional headway during the first quarter of next year.

Ideally,

GDX will hold above $19.80 during any near-term corrective activity.

The Currency Market

The Dollar Index (DX)

still has to close below 95.75 to confirm a short-term top. If/when that

happens, the initial target will be 93.5.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

![]()