![]()

![]()

![]()

![]()

- Interim Update 27th May 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The coming plunge in US

oil production

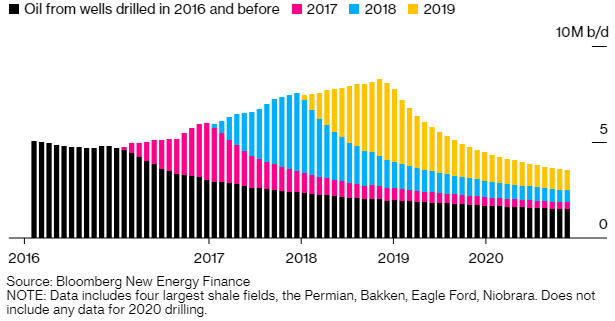

A characteristic of oil

production from shale is a fast production decline (there is an initial

surge and then a rapid tapering of production from a typical well drilled

into a shale oil field). The producers of shale oil overcome this

challenge by constantly drilling new wells.

The point is

illustrated by the following two charts, both of which come from the

Bloomberg article posted

HERE. The first chart highlights the production declines from wells

drilled prior to 2020. The second chart shows what would happen to US

shale oil production if no new wells were drilled after May-2020 (in

effect, it shows the expected production decline from all existing wells).

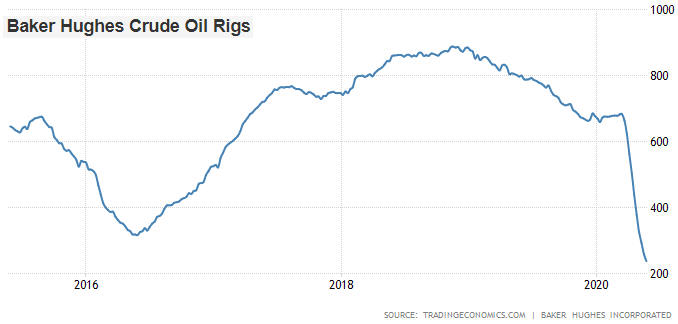

The drilling of new wells will continue. However, the next chart shows

that there already has been a precipitous decline in the number of

operating drill rigs -- from around 700 at the start of this year to

around 230 today. Furthermore, for most US companies focused on shale oil

production an oil price in the $30s will not provide sufficient incentive

to increase drilling activity. As a result, US oil production should trend

downward over the next several months.

The huge reduction in US drilling activity combined with the OPEC+

production cuts and a rebound in demand due to the easing of virus-related

restrictions has brought the oil market back into balance. The market

remains well supplied, but there is no longer a glut and a further

tightening of supply is likely over the months ahead due to the decline in

the US rig count.

It probably will take a sustained rise in the oil

price to well above $40/barrel to create a sufficient economic incentive

to ramp up drilling activity in the US. We expect this to happen within

the next 12 months, but not within the next 4 months. Therefore, we don't

expect to see oil below $20 again, although a downward correction in the

oil price probably will coincide with the next meaningful decline in the

stock market.

Trading around a

core position

One of our favourite money

management techniques is trading around a core position, where a core

position is the amount of exposure we want to maintain to a stock that we

think has a very bullish intermediate-term risk/reward. This tactic takes

advantage of volatility while minimising both risk and opportunity cost.

Trading around a core position works best with volatile stocks, such

as the stocks of junior mining companies, that are in long-term upward

trends or trading within long-term horizontal ranges, although it also can

be applied to stocks that are in declining trends. It's a way of

generating income from stocks that don't pay dividends or increasing the

income from stocks that do pay dividends. In effect, it amalgamates

long-term trading (a.k.a. investing) and short-term trading.

The

idea is that you add to your core position in a stock following a pullback

to a support area or after the stock price becomes stretched to the

downside ('oversold'), and then take profits on the additional shares

after the stock price rebounds to a resistance area or becomes stretched

to the upside ('overbought'). The decision to exit the add-on shares in

such a situation should be straightforward given that your core position

will cover you should the stock price continue to rise. There is, of

course, a risk that the stock price will continue to fall after the add-on

shares are purchased. This risk can be managed by a) applying the tactic

only to the stocks of companies with healthy balance sheets and b) not

buying more than you would be comfortable being stuck with if a rebound

doesn't materialise in the short-term.

Here are two recent examples

from our own account involving stocks that we follow at TSI.

The

first example is Alkane Resources (ALK.AX), a junior gold miner. As

indicated on the following daily chart, twice over the past six months we

bought ALK shares in the low-to-mid-$0.50s and then sold in the $0.90s. We

did this while holding a medium-large core position in the stock that we

plan to keep at least until the spin-out of its specialty metals project

in Q3-2020 and potentially for much longer. Note that the stock traded in

the A$0.90s again during the first two days of this week, but the

preceding pullback wasn't deep enough to prompt the initiation of a new

short-term trade and the $0.90s isn't high enough to prompt a reduction in

our core position.

The second example is Peyto (PEY.TO), a mid-tier natural gas producer.

As indicated on the following daily chart, we were buyers of PEY shares in

the C$1.40s during the March crash (we mentioned this purchase at the

time). These shares were added to a medium-large core position. The stock

subsequently traded as low as C$0.90 before rocketing up to around C$3.00.

We sold the add-on shares near the 200-day MA in the C$2.80s (we

mentioned at the time that a short-term profit-taking opportunity had

arrived in this stock) and continued to maintain a core position.

Trading around a core position is part of the scaling approach to

buying and selling that we advocate. Scaling involves building a position

over time (ideally during weakness) and then exiting over time (ideally

during strength). For a stock that meets the relevant criteria, a core

position should be established by scaling in over time.

Scaling

in/out of positions and trading around core positions eliminates the need

for accurate timing of buy/sell decisions. The alternative is to try to

figure out the right times to go 100% in and 100% out. If you think that

you can consistently get the timing exactly right, you are kidding

yourself and are a financial accident waiting to happen.

Summing

up, with the stocks of well-managed and financially-solid companies it

often makes sense to trade around a core position. This involves doing

some buying during the periodic purges and some selling during the ensuing

surges, all the while maintaining significant ('core') exposure.

The Stock Market

The rally in the US stock market

continued this week, enabling the SPX to move slightly above its 200-day

MA. We addressed this possibility in the latest Weekly Update, when we

wrote:

"A sustained break above the 200-day MA at this time

would be a big surprise, but perhaps there will have to be at least a 1-3

day move above this widely watched MA to convince the majority that the

bull market has resumed and establish a sentiment backdrop that would be

consistent with an important top."

Of greater significance is

that the rally broadened out over the past two days. This is evidenced by

the following daily chart, which shows that the recent bearish divergence

between the SPX and the NYSE Advance-Decline Line (ADL) is now very close

to being eliminated.

The broadening-out of the rally is also evidenced by the charts of the

Dow Transportation Average (TRAN) and Russell2000 SmallCap ETF (IWM) shown

below. TRAN and IWM not only surged to new multi-month highs in nominal

dollar terms over the past two trading days, they also were strong

relative to the SPX.

The fundamentals (as indicated by our Equity True Fundamentals Model -

ETFM) remain decidedly bearish, so the risk of another substantial decline

is high. However, the fundamentals don't tell us anything about timing.

The concluding two paragraphs from last week's Interim Update still

apply. Here they are again:

"This is a time to be looking for

selling opportunities and/or tightening stops and/or hedging in some way.

Unlike the senior US stock indices, some commodity-related stocks and ETFs

still have significant short-term upside potential. For example, the Oil

Services ETF (OIH) could be about to complete a basing pattern (see chart

below). However, the entire market looks vulnerable.

We think the

best-case scenario involves a multi-month period of range trading by the

SPX. This scenario is plausible and potentially would allow the relatively

cheap commodity-related stocks/ETFs to make catch-up moves, but, as

mentioned earlier, a return to the March low is also plausible."

Here is an update of the OIH chart referred to in the above excerpt

from last week's Interim Update. There was an upside breakout (to complete

the basing pattern) on Wednesday 27th May that suggests the potential for

a quick rise to the $140s.

With regard to our own money management, advantage was taken of

Wednesday's strength to exit the OIH shares purchased during the March

crash (we mentioned the purchases in a TSI email alert at the time), but

we are maintaining exposure to OIH via January-2021 call options purchased

during and before the crash. Our current plan is to exit these calls if

there is significant additional strength within the next few weeks.

Gold and the Dollar

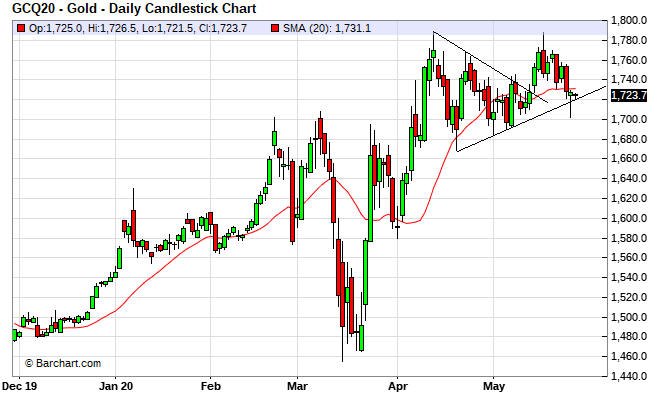

Gold

Below is a daily chart of the August-2020 gold futures contract.

Since testing its April-2020 high at the start of last week, the gold

price has pulled back. It's possible that gold has 'double topped'

slightly below $1800, but a daily close below $1680 or a weekly close

below $1690 is still needed to signal a short-term trend reversal.

Gold Stocks

On Tuesday of this week the HUI

broke below lateral support in the 280s and its 20-day MA. This is

preliminary evidence that a multi-month top is in place. A daily close

below support at 260 would be more conclusive evidence of a top. This

support survived a test on Wednesday.

The historical record tells us that May tops in the gold mining sector

can lead to correction lows anywhere from June to November. This

time-window is too wide to be useful, and in any case we can't find any

historical analogues of the gold mining sector's recent price performance

and current situation. As far as we know, never before has there been a

bona fide crash and full recovery within such a short period.

In

looking for relevant historical comparisons, the best we have been able to

come up with is that February-May of this year was an ultra-compressed

version of what took place between March-2008 and December-2009. It's

certainly the case that from a fundamental perspective the current

situation in the gold mining sector is similar to the situation during

2009.

As mentioned in earlier commentaries, after crashing in 2008

and fully recouping its losses by late-2009, the HUI commenced a

correction that took it back to the vicinity of its 50-week MA. If a

short-term top is in place then a similar outcome this time around would

result in the HUI bottoming in the 220s within the next couple of months.

If the HUI closes below 260 then 220 will become our target for a

correction low and the next sector-wide buying opportunity.

The Currency Market

The way we have drawn the

angled lines on the following daily chart makes it look like the Dollar

Index (DX) has just broken out to the downside, but the purpose of these

lines is simply to illustrate that the DX has been oscillating within a

narrowing range. To decisively break out of this range the DX will have to

either close below its early-May low (98.7) or close above its mid-May

high (100.6).

We suspect that there will be at least two points of

additional movement in the direction of the breakout.

Regardless of which way the DX breaks out of its current short-term

range, we expect that fundamental shifts over the months ahead will create

irresistible downward pressure on the US$. These fundamental shifts are

associated with relative stock market performance, interest rate

differentials and the Fed's plan that any increase in the demand for

dollars will be met with a counteracting increase in the supply of

dollars.

With regard to the coming 1-2 years we continue to be

bullish on the Australian dollar (A$), but our short-term concern is that

this currency will retrace at least half of its March-May rally after the

US stock market completes its post-crash rebound. The reason for our

concern is illustrated by the following chart, which shows the strong

positive correlation between the A$ and the SPX over the past four months.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://tradingeconomics.com/

https://www.barchart.com/

http://bigcharts.marketwatch.com/

![]()