![]()

![]()

![]()

![]()

- Interim Update 27th September 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Commodities

Bearish copper

fundamentals, bullish zinc fundamentals

In the 26th July

Interim Update we wrote that speculators had played the biggest role in

copper's recent price rise. This was apparent due to the behaviour of the

"term structure" in the copper futures market. Specifically, there was a

'normal' upward slope over time in the prices of copper futures

(later-dated contracts were priced higher than earlier-dated contracts),

indicating that there was no current tightness of supply nor any

expectation among commercial traders that supply would tighten in the

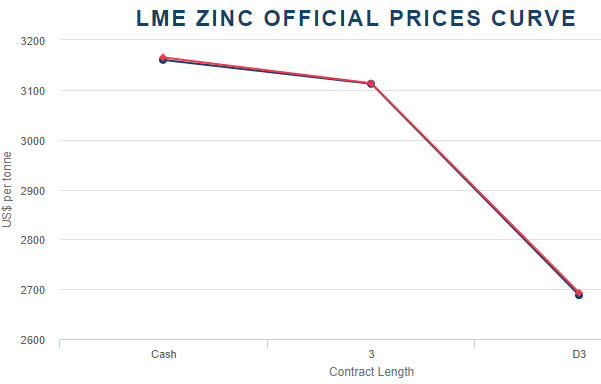

foreseeable future. In the same commentary we wrote that the zinc market's

"term structure" was bullish, because a downward slope in the zinc futures

curve implied that there was current tightness of supply and an

expectation that the tightness would persist.

The prices of both

metals subsequently made additional gains and peaked in early-September,

but whereas the copper price has given back these gains the zinc price

remains near its early-September peak. Here are the relevant charts.

The physical supply-demand situation has since become less supportive

for the copper price and even more supportive for the zinc price. This is

evidenced by the charts displayed below. The first chart shows that the

copper futures curve now has a moderately steep upward slope, meaning that

the copper market is very well supplied at this time. The second chart

shows that the zinc futures curve still has a downward slope. Furthermore,

the downward slope of the zinc futures curve has steepened over the past 2

months, meaning that the price gains have not yet started to alleviate the

'tightness' in the physical market.

A good argument can be made (and we have made it) that the increasing

popularity of electric vehicles and the related increase in the demand for

copper will put irresistible upward pressure on the copper price over the

next few years. However, the fundamental driver that matters the most in

the base-metals markets currently points to additional weakness in the

copper price, at least relative to the zinc price, in the short term.

The oil market confirms an upward trend reversal

When the oil price closed above $51 on Monday 25th September it

confirmed the upward reversal of its intermediate-term trend.

Even if the signal is valid, it is common for an obvious confirmation

of strength to be followed by a pullback. That's especially so when the

obvious confirmation occurs after the market has rallied for a few weeks

and is 'overbought', which is the current situation in the oil market.

Also, it's likely that the oil price will be pressured lower over the

coming few weeks by US$ strength and a broad-based commodity correction.

We noted a couple of months ago that it was time to stop selling

strength and to start buying weakness in the oil market. A pullback over

the coming few weeks could create the next short-term buying opportunity

in anticipation of the oil price moving up to the $60s during the first

half of next year.

The Stock Market

Team Trump has again

announced broad-brushed information about its proposed revamping of the US

tax code. And again, much was said about the large cuts to various

taxes and little was said about how the cuts would be funded.

If

sweeping tax cuts eventually get implemented it's likely that they won't

be funded. In other words, the reduction in tax payments will lead to

larger federal deficits and a faster pace of federal debt accumulation.

This means that the tax cuts will be yet another Keynesian stimulus

program.

The stock market currently likes Keynesian stimulus and in

all likelihood will continue to do so until government bond yields begin

to accelerate upward, at which point an increase in government

deficit-spending will be viewed by equity traders as a reason to sell

rather than a reason to buy.

Despite the boost provided by the new

round of tax-cut jawboning, the SPX remains inside the very narrow range

in which it has moved since breaking to a new high 13 trading days ago. A

daily close below 2480 would be preliminary evidence of an upside breakout

failure while a daily close below 2450 (the short-term channel bottom)

would seal the deal.

Price-action-wise, the most important development during the first

three days of this week was the additional strength in the Bank Index

(BKX) and the BKX/SPX ratio. As illustrated below, the strength was

sufficient to break the BKX out of its 9-month channel.

Also, there were upside breakouts on Wednesday in two stock indices

that were laggards until about 5 weeks ago. We are referring to the

Russell2000 SmallCap Index (RUT) and the Dow Transportation Average

(TRAN).

Gold and the Dollar

Gold

It

doesn't help that the Dollar Index is rebounding, but the T-Bond market is

by far the most important source of the recent downward pressure on the

US$ gold price. The recent decline in the T-Bond price (rise in the T-Bond

yield) is both related to and leading to increasing confidence in the

banking sector, narrowing credit spreads, a higher real interest rate and

a falling bond/dollar ratio, all of which are bearish for gold. The

overall effect is that the GTFM, which appeared to be firmly entrenched in

bullish territory as recently as two weeks ago, is now perilously close to

turning bearish.

The most likely way for the short-term downward

pressure to be removed from the gold price would be for the stock market

to decline by enough to prompt a meaningful shift towards the perceived

safety of the T-Bond.

Turning to the following daily chart, we note

that the US$ gold price closed below its 50-day MA on Wednesday 27th

September. The 50-day MA needed to hold to avoid invalidating the

short-term bullish case, but given the non-supportive sentiment backdrop

and the deterioration (from gold's perspective) in the fundamental

backdrop it is not surprising that it has been breached.

The breach of the 50-day MA does not imply that there will be a lot

more downside in the gold price. What it implies is that the

early-September gold-price peak will hold for a few months.

With

regard to the most likely price for a short-term bottom, the 200-day MA

near $1250 is a realistic target. However, rather than targeting a

specific price it makes more sense to target a 'technical' condition

and/or sentiment situation.

Based on what happened in May and July

there's a decent chance that the next short-term bottom in the gold price

will coincide with gold's daily RSI(14) touching 30. This could occur as

soon as next week.

Gold Stocks

The HUI had

'last ditch' short-term support at 197.5. This support was breached on a

daily closing basis on Wednesday 27th September.

As is the case

with gold, the HUI's breach of support does not imply that there is a lot

more downside in store. Instead, it implies that the early-September top

was more important than we initially thought and that the next multi-week

rally will end at a lower high (that is, below 220).

The HUI has strong support at 180-185. This support range is a

potential target for a short-term bottom now that 197.5 has given way.

Regardless of whether the aforementioned support range is reached, we

expect that the gold-mining indices will make short-term bottoms within

the next two weeks in parallel with interim extremes in the gold price (a

low), the T-Bond price (a low) and the Dollar Index (a high).

The Currency Market

A

monetary-policy divergence for the ages

The policies of the

Fed and the ECB have been diverging since March-2015, when the ECB

introduced quantitative easing (QE) five months after the Fed ended a

similar course of action. The divergence became more pronounced when the

Fed kicked-off its rate-hiking program in December-2015 and next month

(October-2017) it will become as extreme as it can get.

It's likely

that in October-2017 the ECB will announce the 'tapering' of its 60B

euro/month QE program. However, this won't be a signal that the ECB's

monetary policy is about to become less 'accommodative', because a

reduction in the quantity of bonds that are monetised each month will go

hand-in-hand with a substantial extension of the program.

Specifically, the ECB has committed to monetise 60B euros of bonds per

month until December-2017, but has said nothing about what will happen

thereafter. In other words, the program currently runs until the end of

this year. The most reasonable expectation is that the program will be

extended well into 2018 at a reduced monthly rate.

In our opinion,

there is no chance that the ECB's QE program will end before mid-2018 and

a realistic chance that it will continue until 2019.

Also, there is

almost no chance of the ECB hiking its targeted interest rates within the

coming three months. Furthermore, while the ECB may remove its negative

interest-rate policy (NIRP) during the first half of next year, there's a

high probability that its deposit rate, which currently sits at negative

0.40%, will be no greater than zero in mid-2018.

At the same time,

the Fed has already hiked the equivalent of its deposit rate on four

occasions and probably will have implemented at least two more hikes by

the middle of next year. Also, the Fed is about to kick off a quantitative

tightening (QT) program beginning at $10B/month and ramping-up over the

ensuing 12 months to $50B/month.

It therefore seems that for at

least the next 9 months we will have the ramping-up of a Fed

money-supply-contraction program and the Fed moving its targeted interest

rates further into positive territory alongside a continuing ECB

money-supply-expansion program and the ECB maintaining either NIRP or

ZIRP. This means that the monetary-policy divergence that began in

March-2015 is about to become extreme, with the Fed ramping up its

tightening at the same time as the ECB extends its aggressive loosening.

Now, this doesn't imply that there will be something more than a 1-3

month rebound in the Dollar Index (DX) from its recent low and an

associated 1-3 month pullback in the euro from its recent high. The

monetary-policy divergence is clearly bullish for the US$ relative to the

euro, but the US$/euro exchange rate is driven by differences in market

interest rates that don't always follow monetary policy shifts in an

obvious way. For example, despite the Fed being 'tighter' than the ECB

throughout this year to date, the difference between the yields on 10-year

US and German government bonds (the interest-rate differential the matters

the most in this case) moved in the euro's favour until mid-July. Refer to

the following chart comparison of the euro (the blue line) and the

Germany-US 10-year bond-yield differential (the green line) for details.

Note: From mid-July until early-September the euro overshot to the upside

due to speculative buying that was not supported by the dominant

fundamental driver.

The bottom line is that monetary policy is becoming increasingly

supportive for the US$ relative to the euro, but the bond yields set by

the market will determine whether or not this translates into US$ relative

strength.

Current Market Situation

Although a reversal was yet to be confirmed by the price action, we

have been assuming that the Dollar Index made a short-term bottom in

early-September. This assumption was confirmed by the price action over

the past three trading days when the DX broke above lateral support at

92.5, lateral support at 93.0 and the 50-day MA.

Resistance at 94

is a likely 2-week target.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.lme.com/

http://www.kitco.com/

![]()