![]()

![]()

![]()

![]()

- Interim Update 27th December 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Cryptomania Update

From the 18th December Weekly

Update:

"We are now two weeks away from the start of a 2-week

window in which previous speculative manias have 'blown out'. Also, there

are precedents for blow-off tops in asset prices shortly after the start

of futures trading. Therefore, 'cryptomania' could be close to its zenith.

Be aware, though, that at this point a 30%-40% price crash could turn

out to be nothing more than a bull market correction. It will only be

known -- to the extent that such things can ever be known -- that a major

top is in place if there is a price crash, a rebound to a lower high and

then a decline to below the crash low."

On an intra-day basis,

a 45% price crash happened during Monday-Thursday of last week. This means

that the intra-day high of around $20,500 (basis the nearest futures

contract) on Monday 18th December could turn out to be the all-time high,

in which case last week's crash was the first part of a total, or

near-total, collapse. If so, the bitcoin bubble popped one week after the

commencement of futures trading on the CBOE and on the same day as the

commencement of futures trading on the CME.

Despite the ample

evidence that the enthusiasm for bitcoin and the associated "alt-coins"

was an extraordinary popular delusion and that the past few weeks was a

major speculative finale, there is still a realistic chance that last

week's price crash was a bull market correction. As mentioned above,

confirmation of a major top requires a price crash (done), a rebound to a

lower high (possibly in progress) and then a decline to below the crash

low.

The crash low in the cash market was $10,000, but for the

nearest futures contract it was $11,300.

Interesting COTs

Our most recent market update

was an

abbreviated Christmas edition sent by email last Friday. It was sent

before the latest Commitments of Traders (COT) report was published, so

this is our first chance to discuss the report's contents. We just want to

mention two significant developments.

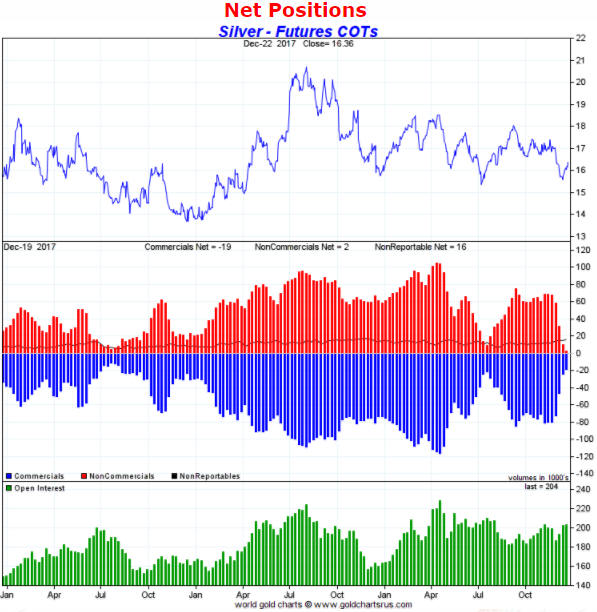

First, the following chart

shows that at the date of the most recent COT data (19th December) the

total speculative net-long position in silver futures (the inverse of the

blue bars in the middle section of the chart) was at its lowest level

since Q3-2015. This probably means that the current rally in the silver

price will extend to $17.50-$18.50 regardless of whether we are dealing

with a new intermediate-term upward trend or a counter-trend rebound.

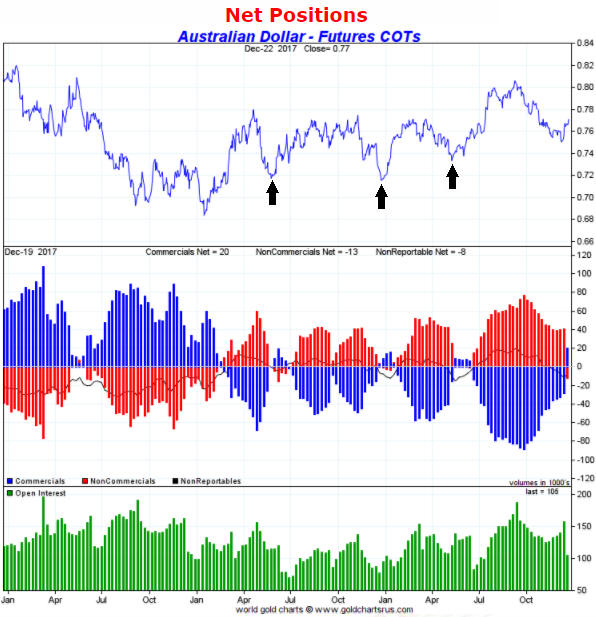

The second development worth mentioning is the change in the

Australian dollar's COT situation.

Three months ago the A$'s COT

situation was extremely bearish. Prior to last week it had been getting

less bearish (more bullish) at a steady pace in parallel with a downward

correction in the A$/US$ rate, but the latest COT numbers reflect a

dramatic improvement.

The latest COT numbers indicate that

speculators, as a group, were net-short the A$ by 20K contracts after

having been net-long by about 30K contracts a week earlier. This turn of

events means that the A$'s COT situation at 19th December was similar to

what it was at the last three multi-month price bottoms (marked by the

arrows on the following chart).

We have been expecting the A$ to

make a correction low in January or February. It still might, but the COT

data suggest that the low is already in place and that the A$ will do no

worse than test its December low within the coming two months.

Can monetary

deflation offset monetary inflation?

The answer to the above question is no; once there has been sufficient

monetary inflation to cause major economic problems the situation cannot

be put right by deflating the money supply. In fact, deflating the money

supply would magnify the pain. Understanding why this is the case requires

a brief explanation of why monetary inflation is so dangerous.

The

large-scale creation of money out of nothing doesn't cause a uniform rise

in prices. It causes some prices to rise faster than others and in doing

so leads to business owners, entrepreneurs and investors having false

impressions about the amount of future demand. It also causes a false

impression about the amount of real savings in the economy. These false

impressions, in turn, lead to many investing and business decisions that

will eventually prove to be ill-conceived.

Once the mistakes caused

by the falsification of price signals start being realised, a corrective

process -- usually called a recession -- gets underway. This entails a

widespread reduction in new investment, the liquidation of inventories,

the shelving of expansion plans and the reallocation of resources.

Naturally, the corrective process will result in temporary unemployment,

excess capacity and the general under-utilisation of resources.

Unfortunately, in today's world it will also result in central banks

creating a lot more money out of nothing in an effort to prompt a new

round of spending errors that will, according to Keynesian theory,

counteract the consequences of earlier spending errors.

In summary,

monetary inflation is a problem primarily because it falsifies the price

signals upon which business decisions are made, not because it leads to a

rise in the so-called "general price level".

Obviously, shrinking

the money supply can't mitigate the consequences of the bad decisions that

were prompted by the earlier expansion of the money supply. To explain by

way of a hypothetical example, assume that monetary inflation causes the

price of commercial real estate to sky-rocket and in response a real

estate developer begins to construct a large office building. Also assume

that two-thirds of the way through the construction it becomes apparent

that the future demand for office space will be much lower than originally

forecast, meaning that the building will not be needed. At this point, a

large quantity of resources has been consumed by a project that will not

be economically viable and may not even be completed.

Just as the

creation of money out of thin air causes price distortions, so does the

vanishing of money into thin air. When money is destroyed on a large scale

there isn't a uniform reduction in prices throughout the economy; instead,

some prices collapse while others fall by a small amount or not at all.

Deliberately deflating the money supply will therefore never make sense,

although under the current monetary system it is inevitable that some of

the money that gets loaned into existence during a boom will be destroyed

during the ensuing bust.

The Keynesian economists who guide the Fed

are blissfully unaware of how monetary inflation and deflation affect the

economy. As far as they are concerned, the economy is like a bathtub

containing an amorphous fluid called "aggregate demand". In this

unrealistic view of the world, the job of the central bank is to pump-in

or pump-out demand with the aim of keeping the bathtub filled to a

desirable level.

After a great many years of pumping into the

imaginary bathtub, in October of this year the Fed finally decided that

the level was a little high and began pumping out (it has begun to destroy

money, albeit at a very slow pace). As discussed above, this can only

hurt. However, the way the current system works the Fed has no choice.

Even if its new leadership understood that the damage has been done and

that reducing the money supply could only magnify the inevitable negative

consequences, for the Fed to retain credibility a deliberated monetary

contraction is almost mandatory.

This is because a Fed decision to

maintain its balance sheet at today's bloated level would be a tacit

admission that QE results in a permanent addition to the money supply as

opposed to a temporary exchange of money for assets. This would not be an

issue in the present, but it would become an issue the next time the Fed

decided that QE was appropriate. Furthermore, since the Fed monetises

assets that eventually mature, holding its balance sheet at today's

bloated level forever would necessitate the endless monetisation of new

assets to replace the maturing old assets.

Therefore, we can be

confident that the Fed will persist with its deflationary 'pumping-out'

operation until asset prices plunge. After prices plunge, the pumps will

be reversed in an effort to prompt a new round of spending errors.

The Stock Market

Tesla (TSLA) is one of the

poster children for the bull market in technology-related stocks. In the

18th December Weekly Update we wrote that:

1) TSLA was possibly the

most over-priced large-cap stock in the US market.

2) There were

signs in TSLA's chart that it may be close to completing a top of at least

intermediate-term significance.

3) A weekly close below $300 would

complete TSLA's topping pattern and project a decline to around $200,

where the stock would still have a very high valuation (renowned

short-seller Jim Chanos believes that Tesla's equity would be

appropriately valued at zero).

4) TSLA was a reasonable candidate

for a bearish speculation in the $340-$360 range, with an initial

protective stop placed slightly above the September high.

The stock

price has since dropped from the mid-$340s to $311, or about 10%, but it

is still within the confines of its 6-month trading range. Only a break

below $300 followed by downward acceleration would confirm that the price

action of the past 6 months constituted a major top as opposed to a

bull-market consolidation.

Of the senior US stock indices, the NASDAQ100 Index (NDX) is the best

proxy for the bullish trend. This is because the NDX is the senior index

that is most strongly influenced by the large-cap stocks that have been

the focal points of speculation over recent years.

The NDX has

consolidated over the past few days and looks set to make at least one

more new high. This next high could turn out to be very important.

In the market update sent by email last Friday, we wrote:

"Based

on current chart patterns, it's likely that the first sign of serious

weakness will occur in Europe, not in the US.

The EURO STOXX 50

Index (STOX5E) has now spent 26 trading days oscillating within a

horizontal range, the bottom of which lies at 3525. It closed at 3571 on

Thursday 21st December.

A daily STOX5E close below 3525 would be a

sign of serious weakness and could be a timely prompt to establish a new

bearish speculation focused on the more highly-priced US market, while a

daily STOX5E close above 3620 (the top of the range) would suggest that

the market was temporarily out of danger."

The STOX5E has now

spent 28 days within the above-mentioned range.

We expect a

downside breakout by the STOX5E in early-January.

With regard to bearish speculations, our own account contains a

position in TSLA put options expiring in April-2018 and we are looking for

an opportunity to add some April-2018 QQQ put options. For those who

prefer to avoid options trading it could make sense to average into QID

(ProShares UltraShort QQQ) over the next few trading days.

Gold and the Dollar

Gold

The

rebound in the gold price from its mid-December-2017 low has been purely

sentiment-driven, in that the price has moved upward in response to

speculators becoming increasingly bullish -- and becoming net buyers of

gold futures -- even though the fundamental backdrop has not been

supportive. In this respect it is similar to the initial decline from the

September-2017 peak, in that during the three-week period immediately

following the early-September peak the price was pushed downward by the

scaling back of an extremely aggressive speculative net-long position

despite the fundamental backdrop being gold-bullish.

Almost

regardless of what happens to gold's true fundamentals, we expect that the

shift in speculative sentiment will result in the gold price making some

additional headway over the coming few weeks. However, an

intermediate-term (6-12 month) upward trend would require a substantial

fundamental shift in gold's favour. This could happen in response to an

intermediate-term decline in the broad stock market, but it hasn't begun

yet.

With regard to the short-term price action, gold is nearing

important lateral resistance at $1300. We suspect that this resistance

will hold if tested within the next few days and that there will be some

corrective activity over the coming 1-2 weeks. The rally should then

resume.

Taking into account the COT situation, gold's price action and the

recent performance of the HUI/gold ratio, at this time the rally from the

mid-December low looks similar to the rally from the early-July low.

Gold Stocks

The rally from the December low

has not yet moved the HUI above its 200-day MA. However, GDX, GDXJ and the

XAU have broken solidly above their respective 200-day MAs. GDX's breakout

is illustrated by the daily chart displayed below.

The gold-mining indices and ETFs are probably close to highs that will

hold for at least two weeks, but even if we are dealing with nothing more

than a counter-trend rebound there is likely to be additional upside

before the overall rebound is complete. What we expect from here is an

interim high within the coming three trading days followed by a pullback

to the vicinity of the 50-day MA and then a move to above the

aforementioned interim high.

The Currency Market

92.5 has consistently acted as support and resistance for the Dollar

Index (DX) over the past 5 months. Right now it is an important support

level. If the DX breaks through this support and doesn't reverse course

soon after, then a decline to a new 12-month low will be on the cards.

We suspect that the 92.5 level will hold for now or that a downside

breakout within the next few days will prove to be short-lived. This is

because the DX presently has both sentiment and fundamentals on its side.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Potential

addition to the TSI Stocks List: Aura Minerals (TSX: ORA). Shares: 34M

issued, 35M fully diluted. Recent price: C$2.61

Potential

addition to the TSI Stocks List: Aura Minerals (TSX: ORA). Shares: 34M

issued, 35M fully diluted. Recent price: C$2.61

In 2016 we

wrote of our interest in Rio Novo Gold (RN.TO). We thought that the stock

offered very good value below C$0.20 considering the economics and

construction-ready status of the company's Almas gold project in Brazil,

but were put off by the weak balance sheet. Our tentative plan at the time

was to add RN to the TSI Stocks List if, and only if, it raised enough

money at a low-enough cost to solidify its financial position while

remaining an excellent value proposition. That never happened.

Here

we are more than a year later with RN still offering excellent value and

still having a very weak balance sheet (at 30th September it had a working

capital deficit of US$5M), meaning that it is in no condition to move the

Almas project forward. The difference, now, is that RN has agreed to be

taken over by Aura Minerals (ORA.TO), a gold-mining company with the same

controlling shareholder (Northwestern Enterprises), in an all stock deal*.

The merging of these two companies was announced last week and makes

so much sense that we wonder why it didn't happen sooner. This is a case

of one plus one being a lot greater than two, because the combination

removes the individual weaknesses.

ORA is profitable, has a healthy

balance sheet and is currently producing gold at the rate of around 120K

ounces/year from a mine in Honduras and two mines in Brazil. With its

existing assets it may be able to increase its production rate, but not by

much. In other words, it lacks organic growth potential. RN, on the other

hand, has huge growth potential but no way of financing the growth. When

RN becomes part of ORA there will be a clear and fairly short path to a

40% increase in the latter's annual production, given that the Almas

project is expected to have average annual production of 52K ounces.

If the merger is completed as planned then the combined company will

have 43M shares, 55% of which will be held by Northwestern.

We

roughly estimate the post-merger value of an ORA share to be C$6.70, which

is about 160% above the current share price. This assumes that a) the 120K

ounces/year of current production is worth US$1000/oz (much lower than

average), b) the Almas project is worth 50% of the NPV estimated in the

Feasibility Study** completed last year, c) the combined company initially

will have net working capital of US$30M, and d) ORA's other assets are

worthless.

The most important short-term company-specific risks

are:

1) The merger doesn't get approved by minority shareholders.

2) An asset sale that was arranged by ORA a few weeks ago and that

should add US$40M to its balance sheet in February falls through.

Both of the above events have low probabilities, but if either happens it

will be a deal-breaker for us.

Despite the apparent value at the

current price (C$2.61), we aren't going to add ORA to the TSI List at this

time. Instead, we'll wait for a better opportunity. The main reason is

that the stock price has risen sharply on low volume over the past two

weeks and is close to resistance defined by its 2016 high (see chart

below). The other reason is that with gold and the gold-mining indices

having not yet signaled the start of an intermediate-term rally, there

should be no hurry to buy any gold-mining stock.

Hopefully there

will be a significant pullback in the stock price within the next few

weeks. If there is then we will add an ORA position to the TSI List,

either directly or indirectly (via RN). Specifically, ORA will be added to

the List if it trades at C$2.05 or RN will be added to the List if it

trades at C$0.10. Note that paying C$0.10 for RN would be equivalent to

paying about C$1.90 for ORA.

*0.053 of an ORA share for each RN share.

**At a gold price of $1250/oz the Almas project was

estimated to have an after-tax NPV(5%) of US$147M and an IRR of 34%.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.goldchartsrus.com/

![]()