![]()

![]()

![]()

![]()

- Interim Update 28th June 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Long-term wealth

destruction machines

The stocks of gold and

silver-mining companies can be good investments for periods of up to a few

years, but investors should understand that under the current monetary

system these companies are almost guaranteed to destroy wealth over the

long term. The main reason is that gold and silver mining companies are

affected in a similar-but-magnified way by the boom-bust swings that

adversely affect the entire economy. We've covered this issue in the past,

but it's important enough to revisit from time to time.

In the same

way that the mal-investment fostered by the Fed's monetary inflation has

caused the US economy to effectively stagnate over the past 17 years, the

bad investment decisions fostered by the periodic floods of money towards

gold mining have made the industry inefficient. That is, just as the

economic busts that follow the central-bank-promoted economic booms tend

to wipe out all the gains made during the booms, the gold-mining industry

experiences a boom-bust cycle of its own with even worse results. The

difference is that the booms in gold mining roughly coincide with the

busts in the broad economy.

The crux of the matter is that when the

financial/banking system appears to be in trouble or it is widely feared

that central banks are playing fast and loose with the official money, the

stock and bond markets are perceived to be less attractive and

gold-related investments are perceived to be more attractive. However, the

gold sector to the stock and bond markets is like an ant to an elephant,

so the aforementioned shift in investment demand results in far more money

making its way towards the gold-mining industry than can be used

efficiently. Geology exacerbates the difficulty of putting the money to

work efficiently, in that gold mines typically aren't as scalable as, for

example, base-metal mines or oil-sands operations.

First Majestic

Silver (FR.TO) and Yamana Gold (AUY) are two of the countless examples of

long-term wealth destruction within the gold/silver sector. These

companies have experienced strong growth and have been enormously

profitable at times over the past 12 years, but over the entire period

they have both generated large cumulative losses despite the metals they

produce having roughly tripled in price.

FR managed to generate a

cumulative loss over this 12-year period of about US$53M, which is

obviously not good. However, FR's lousy overall performance pales in

comparison to the wealth destruction accomplished by AUY.

AUY has

achieved a cumulative loss of more than US$3B since 2004. To put this in

perspective, the market cap of the company is currently about US$2.5B,

meaning that over the course of a period in which the gold price gained

more than 200% this gold producer accumulated losses that are more than

the current market value of the entire company. That's part of why AUY

shares do not offer good value right now despite being priced no higher

than they were in 2004.

Gold itself is not made less valuable by the monetary-inflation-caused

inefficiencies and widespread wastage that periodically beset the

gold-mining industry, which explains why gold bullion has been making

higher highs and higher lows relative to the average gold-mining stock

since the late-1960s. The following weekly chart shows the gory details.

In particular, the chart shows that gold-mining stocks, as represented by

the Barrons Gold Mining Index (BGMI) up to 1996 and the HUI thereafter,

have been in a downward trend relative to gold bullion for almost 50

years. There's no good reason to expect this downward trend to end while

the current monetary system remains in place.

There is a lot of money to be made from investing in gold stocks --

even the spectacular wealth destroyers such as AUY -- at the appropriate

times. However, it's important for investors to understand that regardless

of how cheap the stocks are relative to gold bullion at the time of

purchase, eventually they are going to be even cheaper. Opportunities to

realise large profits should therefore always be taken and gold-mining

stocks should never be thought of as heirlooms to be passed on to the next

generation.

The Stock Market

The US

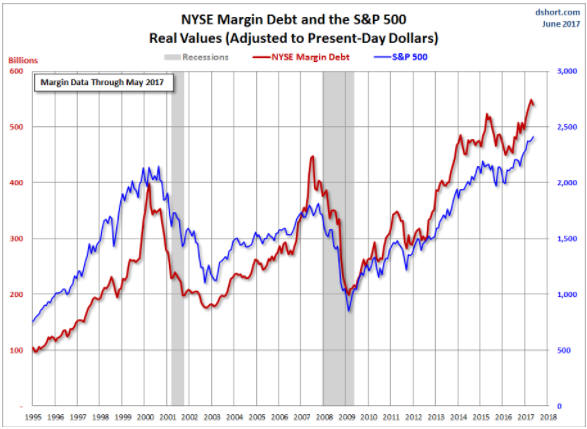

A downtick in NYSE Margin Debt

It's way too soon to know if this is significant, but it's worth

mentioning that NYSE Margin Debt dropped a little in May (the figure for

May was published this week).

Chart source:

Advisor Perspectives

The monthly margin-debt figure is of

interest to us because it is the most direct indication of stock-market

leverage and because regardless of how expensive the market is there will

not be a major top as long as leverage is increasing.

Current Market Situation

The price

action during the first two days of this week looked bearish for the

NASDAQ100 Index (NDX), with the index initially rising and then abruptly

reversing course. However, short-term support at 5650 held and there was

an upward reversal on Wednesday.

With this Friday being the end of

the month and the quarter, short-term bearish traders should allow for

some additional strength in the NDX over the final two days of the week in

response to 'window dressing' by funds that have big positions in the

handful of stocks that have dominated the NDX and the entire market since

the beginning of the year. However, the potential for a quick and sizable

decline will remain as long as the end-of-quarter window-dressing doesn't

enable the NDX to close above its early-June peak.

The ProShares UltraShort QQQ (QID) is still a reasonable short-term

speculation provided that a) it is bought when the NDX is below, but

within a few percent of, its early-June peak, and b) a daily-closing

loss-limiting stop is placed slightly above the early-June peak.

Interestingly, the recent signs of weakness in the NDX have been

accompanied by signs of strength in the steel sector of the US stock

market. Refer to the following daily chart of SLX (the VanEck Steel ETF)

for details.

The recent strength in the steel sector appears to be at least partly

caused by non-subtle hints from the Trump Administration that it will soon

implement further measures to protect this industry from international

competition. The measures would probably include new tariffs and/or import

quotas, resulting in higher prices for steel in the US and greater profits

for US steel producers.

All measures undertaken by governments to

limit trade or to make trade more costly are counter-productive and

therefore stupid (assuming that a stronger economy is the goal), but

additional measures to protect US steel producers would be stupid almost

beyond belief. This is because the steel-producing sector of the US

economy is tiny relative to the steel-using sector of the US economy. For

example, steel-using businesses (autos, construction, etc.) employ

10-times more people than steel-producing businesses. For another example,

the value added by the US steel industry is about 0.2% of GDP whereas the

value added by companies that use steel in manufacturing processes is 5.8%

of GDP.

Anyhow, regardless of the fundamental reasons (if any)

behind it, SLX's recent reversal of fortune could be part of a 'changing

of the guard' that will result in commodity-related equities generally

performing much better than the likes of the "TFAANGs" during the second

half of this year.

Europe

The EURO STOXX 50

Index (STOX5E) has spiked down to and rebounded from the 3500 level twice

over the past 10 trading days. This support level (3500) must be breached

to signal that something more than a routine short-term correction is

occurring.

Gold and the Dollar

Gold

The

200-day MA (near $1240) was reaffirmed as short-term support for the US$

gold price on Monday 26th June when the price spiked below this MA

intraday and then rebounded to end the day above it. Therefore, it would

continue to make sense for bullish traders to use a daily close below the

200-day MA as a stop. Short-term resistance begins with the 50-day MA in

the high-$1250s, so oscillations between $1240 and the high-$1250s can be

viewed as irrelevant 'noise'.

While an important June-July low for the US$-denominated gold price is

no longer likely, there is a good chance of an important June-July low for

the euro-denominated gold price (gold/euro).

As illustrated by the

following daily chart, gold/euro broke below lateral support during the

first half of this week and ended the 28th June session at a new low for

the year. Moreover, the 28th June close was only 18 euros above the

December-2016 bottom, meaning that gold/euro is currently within 18 euros

of a 12-month low.

The weakness in gold/euro is mainly due to what

we perceive to be unsustainable strength in the euro. A July reversal is

likely.

Gold Stocks

Current

Market Situation

The gold-mining indices and ETFs

consolidated over the first three days of this week. The consolidation was

minor and didn't affect the short-term bullish potential suggested by last

week's price action.

As mentioned in the latest Weekly Update,

nimble traders could buy GDX or GOEX for multi-week trades and set initial

daily-closing stops slightly below last week's lows ($21.59 for GDX and

$21.75 for GOEX). The stops are very important because if these ETFs close

below last week's lows then they could go a lot lower before making

short-term bottoms.

The Currency Market

The euro broke out to a

new high for the year on Tuesday and followed through to the upside on

Wednesday. The catalyst was a hint from ECB chief Draghi that the ECB's

"inflation"-promoting actions had been sufficiently successful to enable

the tapering of its bond-buying within the next few months. However, the

preceding inability of the Dollar Index (DX) to break above resistance at

97.5 (the DX is effectively the reciprocal of the euro) warned that an

upside breakout in the euro and a corresponding downside breakout in the

DX was possibly in store.

There are four reasons to suspect that

this week's breakouts in the euro and the DX will turn out to be

trend-ending moves. They are:

1) As illustrated by the following

chart, the euro is now close to a range of intermediate-term resistance.

2) The DX's weakness has not yet been confirmed by the gold market.

Specifically, with other gold-price drivers evenly balanced we would

expect the bullion market and the gold-mining sector of the stock market

to be much stronger IF the DX had commenced a major downward trend.

3) The DX has just fallen to its 150-week MA, which is similar to what

it did in 1999 prior to the start of a substantial rally. Refer to the

following weekly chart for details.

4) The euro's Commitments of Traders (COT) situation is bearish.

That being said, from a risk/reward perspective this is not a good

time to make a sizable bet on the DX and against the euro. There are two

reasons: First, although it is not the most likely scenario there is a

realistic chance that the DX has made a major top and will accelerate to

the downside over the next few months. Second, until there is a short-term

reversal it will not be clear where a risk-limiting stop should be placed.

If there is a reversal over the days ahead then we will consider

adding a DX-bullish/euro-bearish trading position via the ProShares

UltraShort Euro ETF (EUO).

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() US

Gold Corp. officially changes its name to US Gold Corp.

US

Gold Corp. officially changes its name to US Gold Corp.

We

recently added US Gold Corp. to the TSI Small Stocks Watch List. At the

time it was called Dataram and was trading on the NASDAQ under the symbol

DRAM, but it is now officially called US Gold Corp. and trades on the

NASDAQ under the symbol USAU. There are only 12.7M shares outstanding.

The symbol change became effective on 26th June and on that day there

was a high-volume decline in the stock from around US$3.00 to the

US$2.30s. We don't know why. The stock then quickly returned to around

US$3.00, which could mean that the spike down to the $2.30s established a

sustainable low.

USAU's current value is underpinned by the Copper

King gold-copper project in Wyoming. This project has a roughly 1M-oz gold

resource and a PEA that suggests economic viability at the current gold

price. However, a large (multi-hundred-percent) rise in the stock price

probably depends on exploration success at the Keystone gold project in

Nevada. To get this type of rise in the stock price the exploration team

won't have to generate results confirming that Keystone hosts an

economically-viable deposit, but it will have to generate results that

suggest the potential for such a deposit.

Drill targets are in the

process of being defined and exploration drilling is expected to begin

during the final quarter of this year.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

![]()