![]()

![]()

![]()

![]()

- Interim Update 28th October 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

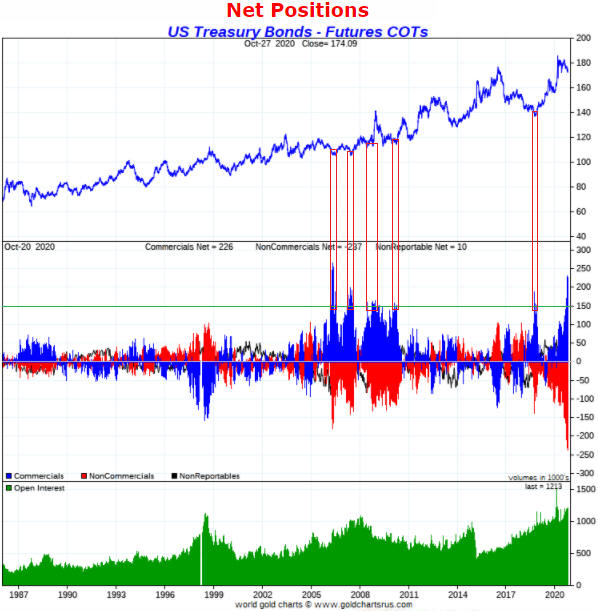

Too much bond

bearishness

It's likely that central banks

will keep their collective boot on rates at the short end of the curve for

at least another year, but due to increasing fear of inflation we expect

that there will be irresistible upward pressure on yields at the long end

of the curve in 2021. Right here and now, however, this line of thinking

appears to be too popular. We say that because the total speculative

net-short position in T-Bond futures is at a 13-year high and close to an

all-time high.

The middle section of the following weekly chart

illustrates the current lopsided sentiment in the T-Bond futures market.

The blue bars indicate the commercial position, which is the inverse of

the total speculator position. The near record-high commercial net-long

position equates to a near record-high speculator net-short position.

By drawing lines on the chart we have attempted to make the point that

there has never been significant weakness in the T-Bond price during the

months immediately after the commercial net-long position in T-Bond

futures has risen above 150K contracts (it was 226K contracts last week).

The historical sample size is small and it certainly could be different

this time, but clearly the current sentiment situation is far from ideal

for a bearish T-Bond speculation.

The upshot is that one of the

best trades over the next few years could be a bet on higher yields (lower

prices) for long-dated government bonds, but that is not a trade that

appeals to us right now.

Additional

thoughts on Bitcoin

In the latest Weekly Update we

wrote that due to the integration of bitcoin into the payment systems

operated by major on-line financial services companies and the evidence

that "forking" (replicating the bitcoin network) does not significantly

affect bitcoin's market value, bitcoin has a real shot at becoming a

popular medium of exchange. We also wrote that the more popular bitcoin

became as a medium of exchange, the greater would be the risk of a

government ban. Here are three other aspects of the bitcoin story that we

think are worth knowing.

First, most of our readers would be aware

that a record of all bitcoin transactions is maintained on a distributed

digital ledger called a "blockchain". The blockchain was the first

successful attempt to create a distributed, permissionless, de-centralised

ledger/database, but it probably won't be the last. This is a long-term

threat to any blockchain-based currency.

Second, the bitcoin

network consumes a lot of electricity. This is by design, since the

intention was to make the creation of a new bitcoin more like the

production of a gold ounce and less like the creation of a modern national

currency unit. Due to the resources (power) consumed in creating new

bitcoins and maintaining the integrity of the network, it could be argued

that using bitcoin is less 'green' than using the digital currency of a

central bank. In other words, helping the environment could be added to

fighting crime and terrorism to 'justify' a government decision to ban

bitcoin.

Third, it's almost certain that governments, via their

central banks, will issue their own digital currencies (cryptocurrencies)

within the next few years. For example, the US Federal Reserve possibly

will issue something along the lines of "Fedcoin".

We addressed this topic three years ago in a

post at the TSI Blog.

As mentioned in the above-linked blog

post, the driving force behind a state-sponsored cryptocurrency would be

the maximisation of tax revenue, in that the replacement of physical cash

with a digital system that enabled every transaction to be

monitored/recorded would eliminate a popular means of doing business below

the government radar. Fighting crime/terrorism, helping the environment,

promoting economic growth and reducing the health risk posed by the

person-to-person exchange of physical money (an obvious new justification

stemming from this year's events) would be nothing more than pretexts.

The introduction of state-sponsored cryptocurrencies such as "Fedcoin"

probably would increase the public's demand for decentralised

cryptocurrencies such as bitcoin, but governments and central banks don't

want competition for the money they issue/control. From their perspective,

there would be no point creating "Fedcoin" or something similar only to

have many economic transactions go unmonitored due to the use of bitcoin.

Therefore, the risk of the government banning bitcoin will ramp up after

the central bank issues its own digital currency.

The Stock Market

A week ago, we wrote: "We

suspect that it [the SPX] will maintain a downward bias between now and

the early-November US election unless there is good news on the 'stimulus'

and/or vaccine fronts."

There was no good news on the stimulus

or vaccine fronts. In fact, the COVID-related news has been all bad over

the past several days, with the number of daily new cases hitting new

highs in the US and skyrocketing in many European countries. Therefore,

the downward bias has been maintained.

The SPX has broken below its

50-day MA and probably is setting its sights on the 200-day MA near 3100.

We expect that any attempt to rebound from significantly north of that

level within the next couple of days will fail, because the market is not

'oversold' and because right now there are too many "known unknowns" for

buyers to have much conviction.

The new/larger waves of COVID cases have caused governments in Europe

to panic and impose lockdowns, which is a much bigger problem than the

virus itself. The lockdown strategy was ill-conceived to begin with and

failed the first time around, but political leaders often feel the need to

do something even if that something is counterproductive.

Over the

past few days the governments of France and Germany announced new national

lockdowns. This will have very negative economic consequences in the

short-term and the long-term.

In response to the lockdowns that

have been announced and in fear of what's to come, the SPDR EURO STOXX 50

ETF (FEZ) plunged over the first three days of this week and is now well

below its 200-day MA. This is illustrated by the top section of the

following chart, while the bottom section of the chart shows that the

FEZ/SPY ratio has dropped to near its low for the year. The decline in the

FEZ/SPY ratio is bearish for the euro.

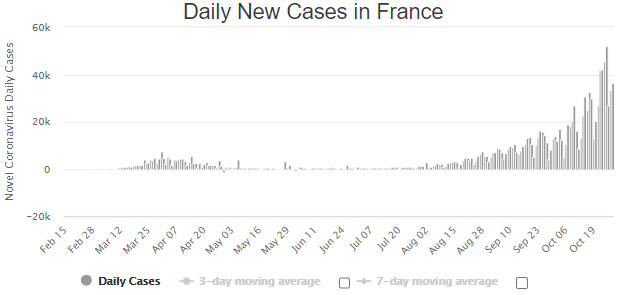

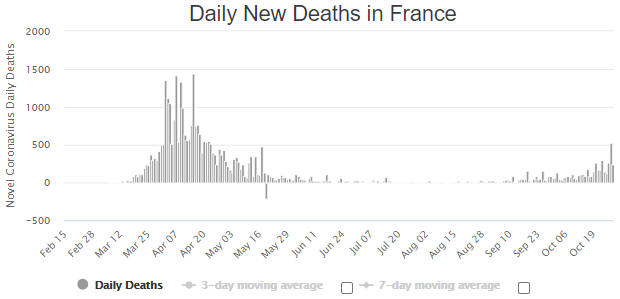

Getting less attention than it deserves is the plunge in the COVID

mortality rate. We are referring to the fact that the much larger wave of

daily new cases has been accompanied, to date, by a much smaller wave of

daily new deaths. France is a good example.

As mentioned above, the SPX probably is on its way to around 3100.

That's about 5% below the 28th October close. Be aware, though, that it

could fall further depending on next week's election outcome and the

extent to which governments panic regarding the increase in COVID cases.

Our plan is to wait for either an 'oversold' extreme or evidence of a

turnaround before doing any significant new buying.

Gold and the Dollar

Gold and Silver

In the latest Weekly Update, we wrote:

"The market looks

poised for a correction-ending plunge to $1800 or lower. This is the most

likely near-term scenario and if it happens it should create a good

opportunity to buy in preparation for the rally to new highs that we

expect to begin before year-end."

The price action over the

first three days of this week was consistent with the market

interpretation outlined above. The gold price appears to be rolling over

into what could be the correction-ending decline.

We continue to

think that the low-$1800s is the most likely place for a correction low,

but there is a risk that a general financial-market liquidation and

concomitant surge in the US$ could push the gold price down as far as

$1700.

Silver's short-term position is similar to gold's. Silver could trade

as low as US$19.00, although there is support near $21.00 and $20.00 that

could act as a floor.

Gold Stocks

The HUI plunged 7% on Wednesday

28th October to a new multi-month low.

Since the beginning of the gold mining correction in early-August our

view has been that a) the 200-day MA (for the HUI and GDX) was the most

likely place for a correction low, and b) October was the most likely

month for a correction low. The HUI's 200-day MA has risen to the 280s and

is now within reach. If it is tested within the final two days of this

week (the final two trading days of October) then we still could get an

October low, but if a rebound begins from near the current level (that is,

without a preceding downward spike to the 280s) then the odds will favour

an extension of the correction into November.

Note that the 280s

(for the HUI) is the most likely place for a correction low, because this

price area contains the 200-day MA and an important lateral support level

defined by the 2016 high. However, there is downside risk to lateral

support near 260.

The relative strength that was being exhibited by

the gold mining sector a couple of weeks ago has disappeared. This is

evidenced by the following daily chart, which shows that the HUI/gold

ratio plunged to a 4-month low on Wednesday 28th October. The chart also

shows that the HUI/gold ratio has closed below its 150-day MA for the

first time since early-April.

As mentioned in the latest Weekly

Update, the HUI/gold ratio climbing back above its 40-day MA (the blue

line on the chart) would be evidence that the correction is over.

The Currency Market

The Dollar Index (DX) has

done very little over the past three months. It stopped trending downward

in late-July, but it has spent almost the entire time since then within a

2-point horizontal range. It broke upward from this range during the third

week of September only to reverse course within a few days.

Over the past three months we've had 96-98 in mind as a target for

what we think is a countertrend rally within a cyclical decline. This

target remains plausible and could be reached in quick time if there is

some panic in the financial markets.

Note that during a panic

investors and speculators sell whatever they can, not necessarily what

they would prefer to sell. This can result in relatively high-quality

assets being dumped in a scramble for cash (usually US dollars). The

relatively high-quality assets then recover quickly after the panic

subsides.

Updates on Stock Selections

Notes: To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question.

![]() Energy

Transfer LP (NYSE: ET) slashes its distribution

Energy

Transfer LP (NYSE: ET) slashes its distribution

Energy

Transfer (ET) is a Master Limited Partnership (MLP) that builds and

operates O&G pipelines and storage facilities in the US. In the 15th

October Weekly Update we compared it to TSI stock Enable Midstream (ENBL),

and wrote:

"As is the case with ENBL, the current

attractiveness of ET has a lot to do with its distribution yield. A week

ago we mentioned that ENBL's distribution yield was almost 17%. After a

subsequent 10% rebound in ENBL's unit price, the yield is now about 15%.

ET's current yield (US$0.305/quarter, or US$1.22 annualised) is almost

23%, which is extraordinary.

The main reason that ET yields a lot

more than ENBL is that ENBL has already 'bitten the bullet' and slashed

its distribution amount for risk management purposes, whereas ET's

quarterly distribution amount is the same now as it was a year ago.

Clearly, the stock market is anticipating a reduction in ET's quarterly

distribution.

If ET manages to get through the current period of

economic weakness without cutting its distribution then the unit price

should return to its early-2020 level of US$11-$12 before the middle of

next year, but in the more likely event that the distribution amount is

reduced by about 30% then the unit price still could make it back to the

June-2020 high near US$9.00 within the next 9 months."

As

expected, ET has cut its quarterly distribution, but by 50% rather than

the 30% mentioned above. This has dropped its yield to below that of ENBL

(at Wednesday's closing prices ENBL was yielding 14.5% and ET was yielding

11.6%). We suspect that the distribution was cut by more than necessary

for risk management purposes.

Our views are unchanged. We still

think that ET stands a good chance of returning to the June-2020 high near

US$9.00 within the next 9 months and we still prefer the gas-focussed ENBL

to the larger and more diversified ET, although both have attractive

intermediate-term risk/reward ratios near current prices.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

http://www.goldchartsrus.com/

![]()