![]()

![]()

![]()

![]()

- Interim Update 29th July 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

12-Month Forecast,

updated 29th July 2020

We published a 12-month forecast

on 20th January, 2020. Due to government decisions to lock down large

parts of many economies in response to a flu virus, this forecast was

overwhelmed by events over the ensuing two months. We therefore did a

forecast update on 15th April, but at that time there were too many

unknowns to be specific.

Probably the most important part of our

January-2020 forecast was our outlook for "inflation", the reason being

that most of our market views hinged off our "inflation" view. In January

we wrote that the next 12 months would involve a substantial (by the

standards of the past 10 years) increase in what most people think of as

"inflation". In April we didn't change our "inflation" forecast, but an

adjustment was appropriate.

We explained the adjustment using a

metaphor. We wrote: "Originally, we were going to take a flight from

Singapore to northern California. Now, we will be flying from Singapore to

Alaska, but we will be getting there via New Zealand." In other

words, there was going to be even more "inflation" than originally

envisaged -- after a big move in the opposite direction.

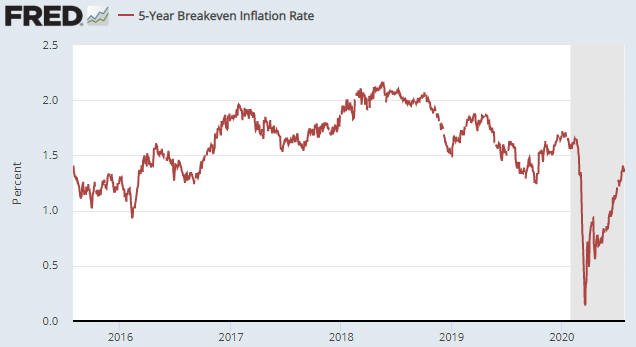

By way of

additional explanation, here is a chart that shows the "5 year breakeven

inflation rate". In effect, this chart shows the expected (by the market)

yearly rate of CPI growth over the next few years. This year started at

around 1.7%, after which there was a plunge to around 0.2% and then an

upward move to around 1.4%. We think that the post-March-2020 upward trend

is destined to continue over at least the next 12 months.

Our reason for expecting much higher "price inflation" was/is not only

the tremendous size of the monetary response to the economic damage caused

by the lockdowns, but also the way the new money was/is being distributed.

Of particular relevance, unlike the previous bouts of Quantitative Easing

that were totally focused on pumping money into the financial markets,

this time around a lot of new money has been and will continue to be

provided directly to businesses and individuals. This should ensure that

the 'problematic' inflationary effects (the effects on the prices of

everyday goods and services, as opposed to the prices of assets) of the

2020 money pumping will be much greater.

In the April update we

summed up our adjusted "inflation" outlook by writing: "...the stage

is being set for a veritable tidal wave of new money to meet a reduced

supply of goods and services. This WON'T result in hyperinflation in the

US or other developed economies in the foreseeable future (say, the next

two years), but it very likely will result in much higher levels of "price

inflation" within 12 months of the passing of the immediate COVID-19

crisis."

We don't have to make another adjustment, but it is

now possible to be more specific. The immediate COVID-19 crisis ended in

May-June, so our expectation is that the US (many other countries too, but

the problem will be bigger in the US due to that country's

disproportionately-large increase in government spending) will be

experiencing the highest rate of "price inflation" in more than 10 years

by Q2-2021.

The idea of a Q1-2020 detour followed by a steeper move

in the direction originally envisaged applies almost across the board to

the markets we track. For example, in January we forecast that the Dollar

Index (DX) would trend downward over the ensuing 12 months as the US stock

market became a relative laggard and as 'capital' shifted towards the

economies that provided the most leverage to commodity production, and

that the Australian dollar (A$) would be the strongest of the major

currencies. The "coronacrisis" prompted a scramble for US dollars during

the first half of March that led to a rapid rise in the DX and a crash in

the A$, but since the third week of March the DX has trended downward and

the A$ has been the world's strongest major currency by a wide margin.

For another example, in January we wrote that the monetary inflation

rebound promoted by central banks would boost the prices of industrial

commodities such as oil and copper to a far greater extent than it boosted

economic growth and overall corporate profitability. This is starting to

become evident. It's likely that oil and the stocks of oil producers will

perform worse over the course of 2020 than we expected in January, but

industrial metals and the associated equities look set to do as well as

originally expected. Furthermore, oil should return to its January-2020

high (near $60) or higher by the second quarter of next year.

Regarding the US stock market, in January we wrote:

"The

long-term US equity bull market won't end in 2020, but the January-2020

high for the S&P500 Index (SPX) will be close to its high for the year.

More specifically, we expect a sizable correction from a January high

followed by a rally that makes only a marginal new high (at best) before

the next sizable correction gets underway. In this regard, 2020 will have

a lot more in common with 2018 than with 2017 or 2019."

We

ended up getting a crash rather than just a "sizable correction", but the

SPX actually has followed the expected pattern and probably will continue

to do so. However, it's certainly possible that for all intents and

purposes the long-term equity bull market ended in the first quarter of

this year.

We say "for all intents and purposes" because we think

that the SPX will exceed its early-2020 all-time high during the first

half of next year if not sooner, but that the new high will be solely the

result of US$ depreciation. In other words, it looks like the US stock

market's 'real' bull market top is behind us.

Regarding the US

economy, although coming into this year the message from our favourite

leading indicators was that a recession would begin during the first half

of 2020, we guessed in January that there would be sufficient monetary

inflation to postpone the start of a recession until 2021. The lockdowns

invalidated this guess.

Both the monetary and fiscal responses to

the lockdown-related economic collapse should ensure that there won't be

anything like a complete recovery from the H1-2020 recession for many

years. As explained over the past couple of months, we are expecting the

economic rebound that got underway during May-June of this year to peak

during the first half of next year at well below the January-2020 level

and for the US economy to be back in official recession territory by the

first half of 2022.

Regarding the bond market, in January of this

year we thought that yields would move higher during 2020, but not

substantially so, and that the US yield curve would steepen. The US yield

curve has steepened significantly since early this year, but thanks to the

economic lockdowns the US T-Bond yield made a new all-time low in

March-2020 and has since chopped around near its low. We expect that bond

yields will rise over the coming 12 months and that the yield curve will

continue its steepening trend, but that the magnitudes of both moves will

be less than they 'should' be due the actions of the Fed.

In

general, we expect the price trends that were set in motion between

mid-March and mid-April of this year to continue until at least the second

quarter of next year. This means that with regard to the next 9-12 months

we are looking for continued weakness in the US$ and strength in the

commodity currencies, across-the-board strength in commodity prices,

strength in gold in US$ terms but not in terms of industrial metals or the

S&P Spot Commodity Index (GNX), strength in non-US equities relative to US

equities, and strength in the gold mining sector of the stock market.

As always there will be corrections along the way, with the period

between now and the early-November US election being a likely time-window

for significant countertrend moves.

Commodities

Oil is about to break

out

For the past 1.5 months the oil price has oscillated

between its 20-day MA and long-term lateral resistance at $42. In mid-June

the gap between these support/resistance levels was about $7, but because

the 20-day MA is rising the gap is now only $1.15. This almost guarantees

that there will be a breakout in one direction or the other within the

next week or so.

Due to the low volatility and the fundamental

backdrop, the more likely direction of the breakout is to the upside.

Uranium takes a hit

There were sizable

declines in most uranium-related stocks on Wednesday 29th July, led by a

12% plunge in the stock price of Cameco (CCJ). As evidenced by the

following daily chart, CCJ fell far enough to negate its recent break

above resistance at US$11.00.

The main reason for the weakness was the decision of Cameco management

to put the Cigar Lake mine (the world's highest-grade uranium mine) back

into production in September-2020. Cigar Lake produced 18M pounds of U3O8

in 2019 and was placed on "care and maintenance" in March-2020 in response

to the low uranium price and the 'coronacrisis' lockdowns.

The

decision to restart the Cigar Lake operation is significant because the

potential for a cyclical bull market in uranium is based on the

combination of reduced supply and stable demand. Our view, and likely the

view of many other speculators/investors, was that Cigar Lake would remain

off-line until after the per-pound uranium price made a sustained move

into the US$40s. The fact that it is being restarted with the per-pound

uranium price in the low-$30s is therefore a surprise.

CCJ's

management knows the supply-demand situation in the uranium market better

than anyone, so it is possible that global supply has tightened to the

point where Cigar Lake can be put back into production without derailing

the upward trend in the uranium price. Also, it is not 100% certain that

Cigar Lake will reopen in September as currently planned, because

virus-related restrictions or a drop in the uranium price to below $30

could prompt another re-think. However, we have decided to retreat to the

sidelines while waiting to see whether the Cigar Lake restart proceeds

and, if so, what effect it has on the market.

Further to the

above, we are going to remove from the TSI List the Uranium Participation

Fund (U.TO) trading position that was added in March and the Energy Fuels

(UUUU) trading position that was added only three weeks ago. The result of

the first trade is a profit of about 50% and the result of the second

trade is a profit of about 7%. This means that the sole remaining uranium

speculation in the TSI List is a CCJ call option expiring in January-2021.

The Stock Market

Over the past couple of weeks we

have discussed the huge disparities between the performances of different

US stock indices. In particular, we have pointed out that at the same time

as the NDX was showing signs of entering correction mode, other indices

were showing signs of exiting correction mode.

Nothing changed over

the first three days of this week. The NDX is still showing signs of

having entered correction mode more than two weeks ago, while the Dow

Transportation Average (TRAN), one of this year's biggest laggards,

appears to be on its way to a 5-month high. Here are the relevant daily

charts.

The performance disparities between different parts of the market

suggested that there was a plausible bullish alternative to a sizable,

market-wide short-term correction. This bullish alternative would involve

a rotation from the stocks/sectors that have been relatively strong to

those that have been relatively weak, leaving the SPX in the 3100-3300

range.

Given that the bullish alternative to a sizable market-wide

correction is not particularly bullish for the SPX, we have stated that

the SPX's short-term risk/reward is bearish. As mentioned above, nothing

changed over the first three days of this week.

Gold and the Dollar

Gold

The

US$ gold price has moved above its 2011 high into new all-time high

territory. Unlike the silver market the gold market has not experienced a

major upside blow-off, but the gold price has risen for 9 days in a row

and is working on its 8th consecutive weekly rise. This implies that on a

short-term basis it is stretched to the upside and probably about to

commence at least a 1-2 week correction.

Silver

In the latest Weekly Update, we wrote:

"We expect that silver's next multi-month top will be in place

before the end of this week."

And:

"...the tops

that follow rapid rises in the silver price usually are signalled by

either a large single-day price decline or a dramatic intra-day price

reversal. We didn't get either of these signals late last week, so the

blow-off to the upside could continue this week."

The blow-off

to the upside did continue this week, with the price rocketing up from

last week's close of $22.85 to an intra-day high of $26.27 on Tuesday 28th

July.

We suspect that Tuesday's spectacular price action marked a

multi-month top for silver. The reversal from Tuesday's intra-day high

wasn't quite as definitive as we'd like, but the extraordinary volatility

indicated by the almost-20% daily price range suggests that a mini mania

ended on that day.

Even if the 28th July intra-day high ($26.27)

turns out to be important, we won't be surprised if the high is tested

within the next month or so. For example, due to silver's tendency to lag

gold at important price bottoms and lead gold at important price tops, one

plausible short-term scenario involves a 1-3 week correction followed by a

rally that results in a new high for the gold price and a lower high (for

the year) for the silver price.

Gold Stocks

The gold sector still appears to be headed for a multi-month top

between early-August and early-September in line with a yearly cycle

established over the past five years. Some corrective activity over the

coming fortnight probably would have the effect of extending the upward

trend into early-September, but if the HUI were to make a new high for the

year next week then the odds would shift in favour of an August top.

The Currency Market

The Dollar Index (DX)

extended its relentless short-term decline over the first three days of

this week and has reached a 2-year low.

If the DX ends this week below its March-2020 low of 94.5 there will

be little remaining room for doubt that the US$ has commenced a cyclical

bearish trend. At the same time, the DX is now almost as 'oversold' on a

short-term basis as it ever gets.

Due to the extent to which the

DX's short-term trend is stretched to the downside, a significant rebound

lasting at least a few weeks should begin in the near future regardless of

whether or not we get conclusive evidence of a US$ bear market at the end

of this week. We will consider rebound targets for the DX after a reversal

is signalled.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() The

Alkane (ALK.AX) spin-off starts trading

The

Alkane (ALK.AX) spin-off starts trading

Australian

Strategic Materials (ASM) commenced trading on the ASX today and averaged

A$1.35-$1.40 over the course of the day, giving us an extreme example of

stock market inefficiency.

To explain, ALK's stock price was

unchanged on the day (21st July) that it began trading 'ex' the ASM

spin-off. This means that someone could have bought ALK shares on 20th

July, sold the shares the next day and received ASM shares for free. Each

eligible ALK shareholder received one ASM share for every five ALK shares

held on 20th July and ALK ended the 20th July trading session at A$1.22,

so on 21st July ALK effectively went 'ex' a 0.28/share, or 23%, capital

return with no change in price. According to the proponents of the

efficient market hypothesis, this should not be possible.

The Dubbo

Specialty Metals Project owned by ASM is complex and difficult to value,

mainly because it is designed to serve commodity markets where supply,

demand and pricing are opaque. For example, the markets for zirconium,

hafnium and rare earth elements. We previously came up with a very rough

valuation of A$0.70 per ALK share ($3.50 per ASM share), but thought that

the stock market was valuing the project at only A$0.20 per ALK share

($1.00 per ASM share). At its closing price of A$1.40 in Australian

trading earlier today (30th July) there appears to be plenty of upside

potential, but due to the complexity of the project we have decided not to

follow the stock at TSI. However, in our own account we will hold the ASM

shares received in the recent spin-off, at least for a while.

The

current price of ASM suggests that ALK shareholders who weren't eligible

to receive ASM shares in the spin-off will instead receive a cash payment

of around A$0.28 per ALK share held on 20th July. Based on this

distribution amount, the gain on ALK from the time it was added to the TSI

List in 2016 to the time it was removed last week was around 600%.

New TSI stock selection: Arafura Resources (ASX: ARU). Shares:

1168M. Recent price: A$0.067

New TSI stock selection: Arafura Resources (ASX: ARU). Shares:

1168M. Recent price: A$0.067

ARU has been a member of the

TSI Small Stocks Watch List for more than two years. Over this period the

stock's liquidity has improved and the company has made significant

progress on the ground, but the market cap remains very low. It is still a

rank speculation, but the risk/reward is very attractive and it offers a

reasonable way to obtain exposure to Rare Earth Elements (REEs).

Therefore, we are adding it to the TSI List as a trading position with an

expected duration of about 12 months.

ARU is focused on the

fully-permitted Nolans REE project in the Northern Territory (NT). A

Feasibility Study for the project was completed in February-2019 and an

update to this study is underway. In addition to completing this update,

the company is engaged in Front End Engineering and Design (FEED) work and

offtake/financing negotiations. It is adequately funded, with no debt and

about A$22M of cash at the moment.

About 80% (by revenue) of the

forecast Nolans production will be neodymium-praseodymium (NdPr), a

critical raw material in the manufacture of the high-performance permanent

magnets used in the electric components of cars. An average ICE (internal

combustion engine) car uses about 0.7 kg of NdPr, whereas an average

electric or hybrid car uses about 1.7 kg of NdPr. Therefore, ARU is a play

on the shift to an all-EV (Electric Vehicle) world.

According to

the February-2019 FS, it will cost about A$1B to develop Nolans into a

mine with average annual production of 4,357 tonnes of NdPr over 23 years.

At "base case" NdPr pricing (US$47/kg in 2020 up to US$90/kg in 2030) the

after-tax NPV(10%) and IRR are estimated to be A$729M and 17.4%,

respectively.

At base-case prices the economics are OK, but not

great. However, with every US$5/kg increase in the NdPr price the

estimated NPV increases by A$130M, meaning that the economics of the

Nolans project will improve rapidly if a new NdPr bull market gets

underway.

However, there are no signs that a new NdPr bull market

is underway. On the contrary, the NdPr price hit a 10-year low of around

US$37/kg in March of this year and has rebounded to around US$44/kg.

The Nolans project probably isn't economic at current commodity

prices, but that is why ARU's market cap and enterprise value are only

A$78M and A$56M, respectively. If the NdPr price rises to the point where

the Nolans project is economically robust, ARU will be worth a multiple of

its current market cap.

ARU is far too small to raise the money

needed to put Nolans into production. Ideally, it will do a JV deal with a

much larger company.

At the moment ARU should be viewed as a

long-term call option on the NdPr price. The risk is high, but the

potential reward is huge.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

http://bigcharts.marketwatch.com/

https://research.stlouisfed.org/

![]()