![]()

![]()

![]()

![]()

- Interim Update 29th August 2018

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

There will be warnings!

If you rely on the mainstream

financial press for your information then you could be forgiven for

believing that financial crises happen with no warning. However, there are

always warnings if you know where to look.

Here are four leading

indicators of financial stress and/or economic confidence that are both

easy to monitor and worth monitoring. It's likely that all four of these

indicators will issue timely warnings prior to the next financial crisis

and a virtual certainty that at least two of them will.

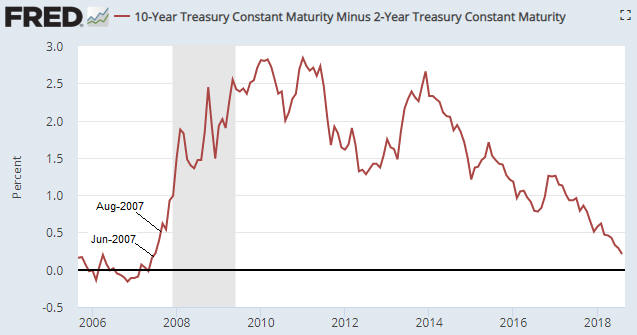

1) The

yield curve, as depicted on the following chart by the 10yr-2yr yield

spread.

As explained in many previous commentaries, the yield curve

'flattening' to an extreme and then beginning to steepen warns that an

inflation-fueled boom has begun to unravel. For example, the yield curve

reached its maximum 'flatness' in November-2006 and provided clear

evidence of a reversal in June-2007. That was the financial crisis

warning. By August of 2007 the 'steepening' trend was accelerating.

The yield curve's current situation looks more like Q4-2006 than

Q3-2007. It is nothing like 2008.

2) Credit spreads, as depicted on the following chart by the

difference between the Merrill Lynch US High Yield Master II Effective

Yield and the yield on the 10-Year T-Note.

Credit spreads start to

widen, indicating a decline in economic confidence and/or a rise in the

perceived risk of default at the junk end of the debt market, well before

a recession or crisis. For example, evidence of a new widening trend in

credit spreads emerged in July-2007 and by November-2007 it was very

obvious that trouble was brewing.

Note that when it comes to

warning of a coming crisis, credit spreads are far more likely to generate

a false positive signal than a false negative signal, that is, they are

far more likely to cry wolf when there's no wolf than to remain silent

when there is a wolf.

Right now they are silent.

3) The short-term interest rate at which banks lend to other banks

versus the equivalent interest rate at which the US federal government

borrows money, as depicted on the following chart by the LIBOR-UST3M

spread.

When trouble begins to brew in parts of the banking system

it gets reflected by higher interest rates being charged for short-term

inter-bank loans well before it becomes common knowledge. This causes the

spread between 3-month LIBOR (the average 3-month interbank lending rate)

and the 3-month T-Bill yield to increase. For example, the LIBOR-UST3M

spread was languishing at around 0.20% in early-2007, indicating minimal

fear within the banking system, but then began to rise steadily and

reached 0.75% in June-2007. This was an early warning sign of trouble. The

spread then pulled back into July-2007 before rocketing up to 2.25% in

August-2007. This constituted a very loud warning. After that the spread

became very volatile and moved as high as 4.5% at the peak of the Global

Financial Crisis in October-2008.

At the moment the LIBOR-UST3M

spread is languishing at around 0.20%.

4) The gold price relative to industrial metals prices, as depicted on

the following chart by the gold/GYX ratio (the US$ gold price divided by

the Industrial Metals Index).

The gold/GYX ratio acts like a credit

spread. This is because gold's performance relative to the industrial

metals sector tends to go in the same direction as economic confidence. In

particular, when confidence begins to decline in the late stage of a boom

or the early stage of a bust, the gold/GYX ratio begins to trend upward.

The following chart illustrates the long-term positive correlation

between gold/GYX and a credit spread indicator in the form of the IEF/HYG

ratio.

The gold/GYX ratio recently bounced from the bottom of its

7-year range. If the bounce continues and gold/GYX exceeds its early-2018

high it would be the first sign of a declining trend in economic

confidence.

Currently, none of the above indicators is warning that a financial

crisis is imminent or even that a financial crisis is starting to develop.

The probability could change as new information becomes available, but

based on the present values of the best leading indicators there is almost

no chance that a financial crisis will erupt within the next three months.

A stock market crash is a different 'kettle of fish', because while a

financial crisis always will be accompanied by a large decline in the

stock market it is possible for a large decline in the stock market to

occur in the absence of a financial crisis. The 1987 stock market crash is

an excellent example.

While the four indicators mentioned above

should issue timely warnings prior to a financial crisis, they may not

warn of a stock market crash that isn't part of a broader crisis. As is

the case with a financial crisis, though, a stock market crash won't

happen 'out of the blue'. In particular, the stock market won't make a new

all-time high one day and crash the next. This is because it takes time

from the ultimate price high to create the sentiment backdrop that makes a

crash possible. The amount of time is generally at least two months and

involves an initial decline, a rebound that retraces 50%-100% of the

initial decline and then a second decline that turns into a crash when the

initial low is breached. It's likely that until the low of the initial

decline is breached the price action will have the look of a routine

correction.

In summary, short-term stock market risk is high, but

there are no warning signs that a financial crisis is brewing or that a

stock market crash (as opposed to, say, a 10% correction) is a realistic

short-term possibility.

The cobalt

correction may be complete

The cobalt market's downward

price correction probably ended on 7th August at $54,500/tonne

($24.80/pound). The price rebounded quickly to about $63,000/tonne and has

since stabilised at $64,000-$65,000/tonne (about $29/pound), indicating

that supply is no longer overwhelming demand.

If the metal's price

correction ended earlier this month then the more severe corrections in

the stock prices of cobalt-focused companies also should be over, although

the initial price rebounds in these stocks could be followed by tests of

the August lows.

The Stock Market

Analysts at major banks and

brokerages have begun to compete to see

who can come up with the highest price targets for popular stocks such

as AMZN and GOOGL. This is a sign of dangerously optimistic sentiment.

However, it would be an understatement to say that there are no signs of

weakness in the price action at this time. On the contrary, the following

chart shows that the SPX has not only broken decisively above its

January-2018 high, but also broken above the top of its upward-sloping

channel. Furthermore, the chart shows that the strength has been confirmed

by the NYSE Advance-Decline Line.

This price action opens up the

possibility that there will be an upside blow-off over the next 2-4 weeks

-- along similar lines to what happened during the first three weeks of

January this year.

Note that the January-2018 high near 2870 is now

important support. This support should hold during any near-term pullback

to keep intact the potential for an upside blow-off.

The blow-off move that ended in January took QQQ (the NASDAQ100 ETF)

to the top of the channel drawn on the following daily chart. A similar

outcome over the coming few weeks would take QQQ up to around $195, or

about 5% above the 29th August close.

We won't attempt a new bearish speculation until there is either a

sign of weakness, such as the SPX breaking below 2870, or a sign of

extreme strength, such as the QQQ reaching its channel top.

Gold and the Dollar

Gold

By

moving up to around $1220 during the first half of this week and then

pulling back, the US$ gold price has defined a channel dating back to the

start of the short-term downward trend in April. The most important nearby

resistance lies at $1240, but closing above $1220 would now constitute a

significant breakout.

The gold market provided preliminary evidence of a short-term bottom

at the end of last week, with preliminary being the operative word. Until

there is a solid break above $1240 the risk of a plunge to new lows will

remain.

It's worth mentioning that in euro terms the gold price has

stopped falling, but is yet to show any sign of strength. This is

illustrated by the following daily chart of the euro-denominated gold

price (gold/euro). The line drawn on this chart is the bottom of the

long-term upward-sloping channel that contained the price from late-2013

to June of this year.

When gold is genuinely strong it will be

strong in terms of all major currencies.

Silver

Silver is yet to provide even

preliminary evidence that a short-term bottom is in place. Such evidence

would be a daily close above the 20-day MA, which is currently near

$15.00.

A solid break above resistance in the low-$15.60s would be

conclusive evidence of a silver reversal.

Gold Stocks

The gold-mining indices and ETFs

are in similar positions to silver in that they are yet to provide even

preliminary evidence that short-term bottoms are in place.

For GDX

(see chart below), the important resistance is at $21.00. This is too far

above the current price to be of use at the moment. It's a similar story

for the HUI. Consequently, for the gold-mining sector we must key-off the

bullion market. After all, it's reasonable to assume that if the gold

price embarks on a short-term upward trend then the gold-mining indices

and ETFs will do the same.

When an intermediate-term gold-mining rally eventually gets underway

it will be indicated early on by substantial strength in the gold-mining

indices/ETFs relative to gold. In particular, in its early stage there

will be a sharp rise in the HUI/gold ratio. On the other hand, a slow and

choppy rise in the HUI/gold rally, such as occurred between mid-March and

early-July of this year, will be suggestive of a counter-trend move.

As illustrated by the following chart, HUI/gold's rebound from its

mid-August low has been slow and choppy to date. This is evidence that we

are NOT dealing with the start of an intermediate-term rally.

In one respect the broad US stock market and the gold-mining sector

are in similar positions. They are both extended in one direction and have

the potential to make substantial moves in the opposite direction over the

months ahead, but reversals have not been signaled.

The

Currency Market

Below is an update of a chart that we

first showed about three months ago to make the point that the euro had to

achieve a weekly and monthly close below 1.156 to indicate that its 2017

rally was the bear-market variety. The euro made a weekly close below this

demarcation level on 10th August, but unless there is a sharp decline over

the final two trading days of this week it will avoid the confirming

monthly close for now.

Regardless of whether it ends 31st August above or below 1.156, we

suspect that the euro will rise to at least 1.20 within the next few

weeks. This is based on sentiment and the chart pattern.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.lme.com/

https://research.stlouisfed.org/

![]()