|

- Interim Update 30th November 2005

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Copper Market Manipulation

IF

market manipulation by hedge funds is largely responsible for the

current high level of the copper price then it's reasonable to conclude

-- as Veneroso and Hunt have done -- that at some point over the next

few months the price will tank.

Two interesting reports on the machinations in the copper market have

been produced over the past few weeks, one by Frank Veneroso and the

other by Simon Hunt. Both of these analysts are experienced and

knowledgeable, and both have arrived at the same conclusion: the copper

price is headed for a big fall.

Frank Veneroso, in his 6th November report entitled "Copper: The

Manipulation", lays out the evidence that hedge funds have been

stocking-up on copper over the past year, thus creating the appearance

of a shortage in a market that would otherwise have experienced a

substantial surplus. He begins his analysis by explaining that official

data on copper demand is based on "apparent consumption", which is

calculated by summing domestic production, net imports and the change

in visible stocks. Taking the specific example of China, the country

whose industrial demand has supposedly driven the copper price to its

current heights, there is a huge discrepancy between data on actual

copper consumption and the "apparent consumption" figures on which most

supply/demand analyses are based. This discrepancy, according to Mr

Veneroso, is around 30,000 tonnes per month, which if correct would

means that 30,000 tonnes per month of copper were going into

non-visible stocks.

Mr Veneroso goes on to explain a) why it is very likely that the

additional copper -- the amount that is going into non-visible stocks

each month -- is being accumulated for speculative, rather than

industrial/commercial, purposes, b) how the manipulation is probably

being conducted, c) the manipulators' exit strategy, and d) the risks

for the manipulators.

One of the main risks facing the manipulators is that the surplus in

the market will increase to the extent that it is no longer

economically feasible for them to purchase enough physical copper to

maintain the illusion of a tight market. The surplus is probably

increasing every month, but this risk would really come to the fore if

an entity that held a large stock of non-reported copper -- China's

Government, for example -- were to decide to dump a lot of copper onto

the market with the intent of bringing down the price.

According to both Frank Veneroso and Simon Hunt, the potential for

China's Government to suddenly increase the supply of copper is a clear

and present danger to those who are attempting to push the price higher

by removing copper from visible inventories. A lot has been written in

the press over the past month about a 100K-200K tonne short position in

copper built-up by a trader working for China's State Reserve Bureau

(SRB) -- an agency responsible for the stockpiling of strategic

materials. However, if recent statements by Chinese officials can be

believed -- and Mr Hunt asserts that they SHOULD be believed -- then

this short position is small compared to the 1.3M tonnes of copper held

by the SRB. In other words, Mr Hunt thinks that the SRB has the ABILITY

to end the manipulation and bring about a substantial fall in the

copper price. And given that the high copper price is causing problems

for China's manufacturing industry the SRB also has the INCENTIVE to

supply enough additional copper to the market to bring down the price.

In summary, Mr Veneroso's conclusion is that the current high copper

price is the result of an old-fashioned 'short squeeze' and that the

price will collapse to below $1/pound when the squeeze ends. Mr Hunt's

conclusion is similar, although he doesn't mention a specific price

target.

Our view is that the manipulation theory is plausible. In fact, during

the first half of this year we said that copper's relentless price

strength was probably due more to manipulation by hedge funds than

genuine supply/demand dynamics. Our opinion wasn't based on a detailed

analysis of supply and demand in the copper market; rather, it was

based on the fact that some of the most important underpinnings of

copper's intermediate-term upward trend were either disappearing or had

already disappeared, and yet the price was still moving higher. In

particular, we noted the following:

a) The support that had been provided by a weakening dollar during 2002-2004 was no longer in place

b) The plunge in ocean freight rates was indicating that Chinese demand for raw materials was falling

c) Liquidity, whilst remaining at a fairly high level, was expanding at

a significantly slower rate than had been the case during 2003-2004

IF market manipulation by hedge funds is largely responsible for the

current high level of the copper price then it's reasonable to conclude

-- as Veneroso and Hunt have done -- that at some point over the next

few months the price will tank. However, the idea of betting against

the copper market doesn't appeal to us right now. We made a couple of

attempts to bet against copper earlier this year via positions in

Phelps Dodge put options, but these put options will almost certainly

have to be written off because the manipulation -- if that's what is

actually going on in this market -- has been more successful than we

had expected. We are more confident now than we were then that

manipulation is the major driving force behind the price move and that

a large price decline lies in the future, but we have no way of

estimating when this large decline will begin. We'll therefore stay

away for now.

When the copper squeeze ends and the price plunges the other industrial

metals will almost certainly be adversely affected, but we suspect that

the bulk of the damage will be confined to the copper market. It is

probable that the gold market will also be adversely affected for a

while because it is likely that some of the hedge funds that are

heavily 'long' copper are also 'long' gold futures, although we don't

think a large downturn in the copper price would be a longer-term

negative for gold. In fact, to the extent that a large decline in the

copper price helped push the US yield-spread higher it would be a

longer-term positive for gold.

The Stock Market

Current Market Situation

There were downward reversals in many of the world's stock markets

during the first half of this week, but it's unlikely that these

reversals will evolve into anything more serious than routine

consolidations. The first quarter of next year is a more likely time

for major peaks to occur.

With respect to the US market, the following weekly chart of the

NASDAQ100 Index (NDX) shows the important support that exists at around

1630. As long as this support is not breached during any further

corrective activity over the coming fortnight we will assume that at

least one more push to a new multi-year high lies ahead of us.

Gold and

the Dollar

Gold Stocks

The Keys

The keys to breaking the AMEX Gold BUGS Index (HUI) upwards out of the

range in which it has traded over the past two years are the gold/CRB

ratio and the US yield-spread (the difference between yields on

long-term and short-term US Treasury debt).

A breakout to new multi-year highs by gold relative to the CRB Index

would point towards a surge in profit margins for gold mining companies

because the CRB index is a proxy for the costs incurred by these

companies (gold miners purchase commodities such as energy and steel in

order to produce gold). If this happened we would expect the biggest

winners to be the exploration-stage stocks and the stocks of low-margin

producers such as DRDGOLD (NASDAQ: DROOY), Golden Star Resources (AMEX:

GSS), and Resolute Limited (ASX: RSG).

The yield-spread is important because a widening yield-spread

(long-term rates rising relative to short-term rates) indicates that

monetary policy is becoming 'easier' and that inflation is going to be

higher in the future than it is in the present. Furthermore, the

gold/CRB ratio trends with the yield-spread, so it would be unlikely

for gold/CRB to make a sustained upside breakout unless the

yield-spread began to widen in sustainable fashion.

The inter-relationship between the HUI, the gold/CRB ratio and the yield-spread is shown below.

Current Market Situation

A couple of weeks ago we mentioned that some bearish divergences were

potentially developing within the gold sector. The following chart of

the HUI, two momentum indicators for the HUI (the RSI and the MACD),

and the HUI/gold ratio, shows that these bearish divergences have

continued to develop. Specifically, note that last week's higher high

in the HUI was accompanied by lower highs in the aforementioned

momentum indicators and the HUI/gold ratio. That this is happening at a

time when a cyclical turning point is due is a reason to be especially

wary. We will therefore retreat to a short-term "neutral" view on the

HUI.

Interestingly, the

HUI peaked at the beginning of December-2003 on the day the gold price

first traded above $400 and this week's peak and subsequent downward

reversal in the HUI has coincided with the nearest gold futures

contract trading at $500 for the first time since 1987. Following the

December-2003 peak in the HUI the gold price continued to move higher

and by January of 2004 it was in the 420s, yet the HUI was unable to

exceed its early-December peak at any time.

It's quite possible that the HUI has just made a peak of similar

importance to its December-2003 and November-2004 peaks, but even if

this is the case we doubt that a large decline will occur over the next

several weeks. As discussed below, the public does not appear to be

bullish enough on gold to allow for anything more than a routine

pullback at this time. This is obviously a time to be cautious, but

even if an intermediate-term peak has just been put in place we think

the most likely short-term outcome is for the HUI to hover near its

highs for another 1-2 months. This is the type of scenario that would

allow for some of the more speculative gold/silver stocks to make new

highs early next year.

Long-Term Outlook

If

the HUI of today duplicates the performance of the BGMI of the 1960s

and 1970s then it will peak at around 1400 towards the end of the next

decade.

In the "Big Picture View" included at the top of every Weekly Market

Update we say that the peak of gold's secular bull market will likely

occur during 2008-2010. We are going to take things one decade at a

time, but actually it would be unusual for a secular bull market to

only last 10 years. A more typical duration would be 15-20 years.

If you only looked at the performance of the gold price you would

probably come to the conclusion that the previous secular bull market

in gold lasted only 9 years (from 1971 through to the beginning of

1980), but the picture is distorted by the fact that the gold price was

fixed prior to 1971. By looking at the performance of gold stocks we

can, however, get an undistorted view of what happened.

The following chart shows that a secular bull market in the Barrons

Gold Mining Index (BGMI) extended from the first half of the 1960s

through to 1980. Not coincidentally, the secular bull market in gold

stocks of the 1960s and 1970s coincided with secular bear markets in

most other sectors of the stock market.

If the HUI of today

duplicates the performance of the BGMI of the 1960s and 1970s then it

will peak at around 1400 towards the end of the next decade. In this

case the total gain from its November-2000 bottom would be around

3500%, which is not an unusual achievement for a secular bull. For

example, from its 1982 bottom to its 2000 peak the NASDAQ Composite

Index gained 3100%.

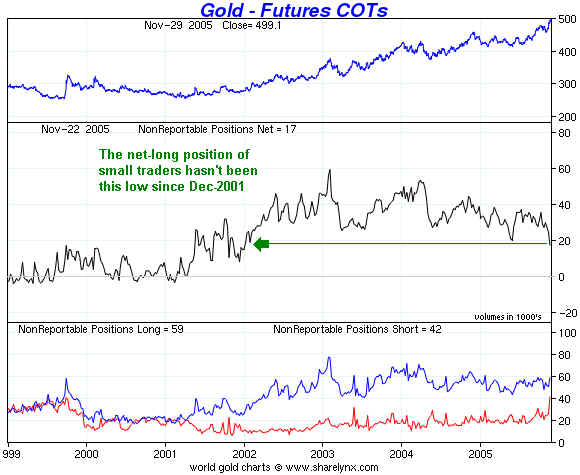

Gold

December gold has just tested round number resistance at $500 and has

begun to pullback (see chart below). If this is just a routine

consolidation then support at 480-485 should not be breached.

The probability that

any pullback at this time will be "routine" is enhanced by the public's

lack of enthusiasm towards gold. Large speculators have been very

bullish for a while, but the following sharelynx.com

chart shows that the net-long position of small traders in COMEX gold

futures has just hit its lowest level since December-2001. This

suggests that small traders are now less bullish regarding gold's

short-term prospects than they have been at any time over the past 4

years.

Currency Market Update

The euro is presently mid-way between short-term support and

intermediate-term resistance (see chart of December euro futures

below). We expect short-term support to be breached over the coming

weeks.

The Yen has a lot

going for it. In particular, Japan runs a large current account surplus

and the Japanese stock market has, over the past several months, become

a world leader. However, with the Fed continuing to push US short-term

interest rates upward and the Bank of Japan retaining its "zero

interest rate" policy there is a huge incentive for speculators to

borrow Yen and invest the proceeds in short-term dollar-denominated

debt. This is known as the "Yen carry trade", and so far this year the

putting-on of these carry trades has swamped any other considerations

(when someone borrows Yen in order to buy dollars they are, in effect,

shorting the Yen versus the US$). At some point in the future all of

these carry trades will have to be unwound and there will be a

spectacular surge in the Yen, just as there was during the second half

of 1998 when some large hedge funds attempted to exit similar trades

(refer to the weekly Yen chart below). This WILL happen, but it's

anyone's guess WHEN it will happen.

The Yen will probably bounce over the next few weeks, but at this stage

we don't see a good reason to expect an imminent reversal in the

intermediate-term trend.

Update

on Stock Selections

Desert

Sun Mining (TSX: DSM, AMEX: DEZ) announced on Monday that it had raised

C$30M by issuing 12M units at C$2.50 per unit, with each unit

consisting of one common share and one-quarter of one common share

purchase warrant. Taking into account the value of the warrants, the

new shares were issued at a discount of around 15% to last Friday's

closing price, or a discount of around 10% to the average price over

the preceding week. As is invariably the case when a substantial number

of new shares are issued at a discount to the current market price, the

stock market reacted negatively to this news. Desert

Sun Mining (TSX: DSM, AMEX: DEZ) announced on Monday that it had raised

C$30M by issuing 12M units at C$2.50 per unit, with each unit

consisting of one common share and one-quarter of one common share

purchase warrant. Taking into account the value of the warrants, the

new shares were issued at a discount of around 15% to last Friday's

closing price, or a discount of around 10% to the average price over

the preceding week. As is invariably the case when a substantial number

of new shares are issued at a discount to the current market price, the

stock market reacted negatively to this news.

We were surprised by management's decision to issue more equity at this

time given that the company has plenty of cash in the bank, no debt,

and a mine that should now be cash-flow positive. However, if companies

have to issue more equity then the best time for them to do so is when

market conditions are favourable and the stock price is near an

all-time high. In this respect the timing of the issue was good.

The main use of the funds will be to finance the development of the

Morro do Vento deposit. Currently, DSM's Jacobina Mine in Brazil is

producing gold at the annual rate of around 100K ounces and with this

week's financing the company should now have enough money to increase

production to 150K ounces/year over the coming 12 months by bringing

Morro do Vento on line.

In our opinion, DSM would be suitable for new buying in the C$2.20s. It

is one of the stocks with a good chance of making a new high during the

first quarter of next year even if the HUI has just made an

intermediate-term peak. Also, this week's pullback has taken the DSM

warrants (TSX: DSM.WT) back to levels where new buying might be

appropriate (the warrants closed at C$0.71 on Wednesday).

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.futuresource.com/

|