![]()

![]()

![]()

![]()

- Interim Update 30th November 2016

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

The Oil Market

Anticipation of and then

reaction to the outcome of an OPEC meeting caused significant two-way

volatility in the oil price over the past few days, with oil first

dropping back to its 200-day MA due to scepticism that the OPEC members

would manage to strike a deal on production cuts and then rising sharply

after it was announced that a production-cut deal had been done. The

volatility hasn't, however, altered the price pattern.

This week's OPEC news actually hasn't changed anything. To avoid

losing its remaining credibility OPEC had to announce some sort of

production-cut deal, but the deal that has been announced probably won't

have a significant effect on overall oil supply even in the unlikely event

that all parties to the deal meet their commitments. The reality is that

OPEC is no longer the swing producer in the oil market. That honour now

belongs to the US shale-oil industry.

In any case, the currency

market is the most important driver of the oil market and the currency

market continues to point to a lower oil price. Of particular

significance, the C$ has done nothing to suggest that its short-term

downward trend is over.

The C$ would have to achieve a daily close

above 75.25 to generate the first sign of an upward reversal in its

short-term trend.

We view the OPEC-inspired price surge as an opportunity to buy some

more USO put options, both as a speculation and a way of hedging long

exposure to commodity-related equities.

The Treasury Market

The following daily chart shows

that the iShares 20+ Year Treasury Bond ETF (TLT) has not yet begun to

rebound from its 'oversold' extreme, although it lost downward momentum a

couple of weeks ago and is possibly building a base.

The on-going weakness in the Treasury Bond is the main obstacle to a

short-term rebound in the gold price. It will be difficult for the gold

price to manage anything more than a modest multi-day bounce until the

T-Bond price reverses upward.

The Stock Market

The NASDAQ100 Index (NDX) tested

its September-October highs on Tuesday of this week and then pulled back

on Wednesday. It has therefore still not confirmed the breaks to new highs

by other important US stock indices.

We expect at least a 6-month extension of the equity bull market, but

at the same time we expect a significant 1-2 month correction.

Gold and the Dollar

Gold

Gold and Inflation Expectations

We've covered the relationship between the gold price and inflation

expectations in many TSI commentaries over the years, but it now makes

sense to revisit the topic. This is because a sharp rise in inflation

expectations since mid-September went hand-in-hand with a sharp decline in

the gold price. According to conventional wisdom, this is not supposed to

happen. A sharp rise in inflation expectations is supposed to be bullish

for gold.

In the financial markets it's not unusual for

"conventional wisdom" to be wrong, although in this case it is not so much

wrong as incomplete. It is certainly the case that all else remaining the

same, an increase in inflation expectations will be bullish for gold.

However, all else never remains the same.

Here is a more complete

and correct statement of the relationship between gold and inflation

expectations: It is bullish for gold when inflation expectations rise

relative to nominal interest rates and bearish for gold when inflation

expectations fall relative to nominal interest rates, regardless of

whether inflation expectations are rising or falling in absolute terms.

With the aforementioned statement of the relationship in mind, let's

take a look at what happened in the recent past.

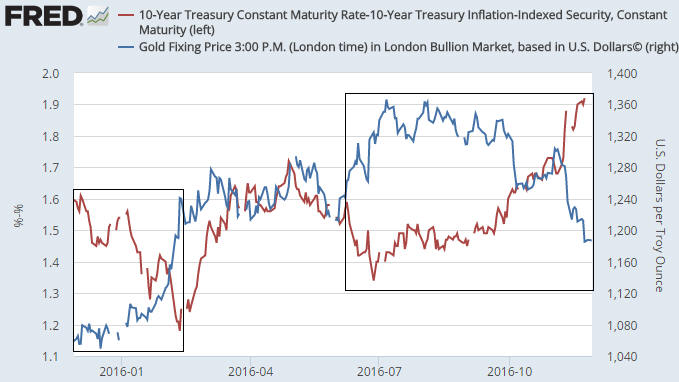

The following

chart shows the gold price (the blue line) and the yield difference

between the 10-year T-Note and the 10-year Treasury Inflation-Protected

Security (TIPS). We refer to this yield difference as the "Expected CPI",

because it is the average annual rate of CPI growth that the market

expects the US government to report over the next several years. Although

almost everyone knows that the CPI tends to understate the rate of

currency depreciation, the Expected CPI is a useful proxy for the

financial markets' inflation expectations.

If gold consistently

performed well during periods of rising inflation expectations and poorly

during periods of falling inflation expectations then the two lines on the

following chart would move in the same direction almost all of the time.

However, over the past 12 months they have actually spent more time moving

in opposite directions than moving in the same direction. It is especially

noteworthy that sharp declines in inflation expectations during the first

6 weeks of the year and during June were accompanied by a strong gold

market and that a sharp rise in inflation expectations since

late-September has been accompanied by a weak gold market.

It is

therefore fair to say that changes in inflation expectations cannot

explain gold's performance over the past 12 months.

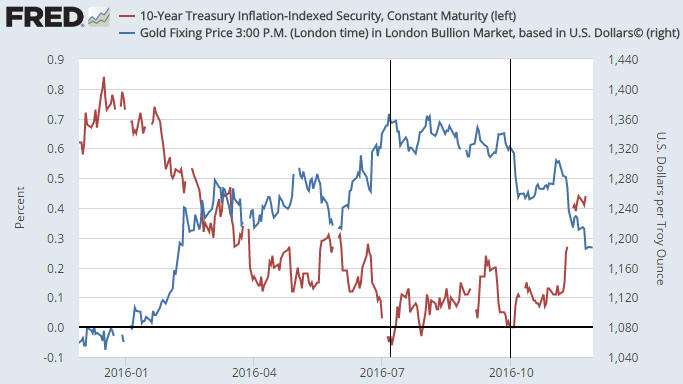

Gold's performance over the past 12 months can, however, be explained

by changes in the nominal 10-year yield minus the Expected CPI. The

difference between these quantities is the 10-year TIPS yield, a proxy for

the real interest rate.

The following chart shows the gold price

(the blue line) and the above-mentioned proxy for the real interest rate.

Notice that a) the gold price has consistently trended in the opposite

direction to the real interest rate, b) the gold price traced out a

topping pattern and the real interest rate traced out a bottoming pattern

from early-July through to late-September, and c) the sharp decline in the

gold price from late-September through to the end of last week coincided

with a sharp rise in the real interest rate.

The upshot is that the gold market was very weak in the face of

sharply-rising inflation expectations over the past two months because

nominal interest rates rose even faster than inflation expectations,

leading to a higher real interest rate.

Current Market Situation

With the T-Bond remaining weak and

the Dollar Index remaining strong it is not surprising that the US$ gold

price has not yet managed a rebound of any significance. However, we

continue to anticipate a short-term rebound, mainly due to the extent to

which the gold market and the markets that exert the greatest influence on

the gold price are stretched on a short-term basis.

As noted in the latest Weekly Update:

"A rebound could

begin as soon as this week and probably won't begin any later than

mid-December (within a few days of the 14th December FOMC announcement),

but for a rebound to have longer-term significance it must, at a minimum,

achieve a weekly close above $1210. It must also be accompanied by a

fundamental shift in gold's favour."

As also noted in the

latest Weekly Update, the Commitments of Traders (COT) report that gets

published at the end of this week will be very interesting in that it will

reveal the effects on speculative sentiment of gold's break below $1200.

The larger the decline in the speculative net-long position in reaction to

the break below $1200, the more constructive (for the bullish case) it

will be.

Gold's COT situation will of course be covered in the next

Weekly Update.

Gold Stocks

Aside from the

fact that the gold-mining indices have continued to show subtle signs of

strength relative to gold, nothing of significance happened over the first

three days of this week.

Over the past three days the HUI traded in

a narrow range near its low. This price action could be part of a small

base prior to a multi-week rally or it could be a consolidation prior to a

plunge below the 14th November low. We suspect it's the former, but we

aren't betting on any particular short-term outcome for this sector.

The Currency Market

The euro is still holding the line

The euro remains

precariously positioned slightly above major support as two important

political events and one important monetary event loom in Europe.

The two important political events are a referendum in Italy and a

presidential election re-run in Austria (the results of the Austrian

presidential election early this year were thrown out due to counting

irregularities), both of which are scheduled for Sunday 3rd December.

Italy's referendum is about the changes to the size and power of the

Senate (the upper house of parliament). A "yes" result, which would reduce

the Senate's size and power, has been vigorously advocated by Italy's

Prime Minister Renzi.

The polls point to a "no" result, but not

decisively. The outcome is therefore 'up in the air', especially

considering the poor recent track record of the political polling

industry.

A "no" result could -- but not necessarily will -- prompt

Renzi to resign, thus superficially making Italy's political situation

less stable.

The polls are also not decisive with regard to the

likely winner of Austria's presidential election, although the Freedom

Party's Hofer has a small lead. From the little we know about the

situation, the Freedom Party appears to be more anti-immigration than

pro-freedom. Austria's presidential election could therefore be viewed as

a referendum on the EU policy that allowed hundreds of thousands of

Middle-Eastern immigrants into Europe over the past two years.

The

outcomes of these political events could create currency-market volatility

next week, but it should be understood that regardless of the outcomes the

probability of either country leaving the EU within the coming 12 months

will be close to zero (zero in the case of Austria, slightly above zero in

the case of Italy).

The important monetary event is the ECB meeting

scheduled for next Thursday (8th December). It's likely that the ECB will

announce an extension of its asset monetisation program at the conclusion

of this meeting, thus highlighting the contrast with a Federal Reserve

that is set to take a tiny step towards a tighter monetary stance a week

later.

In the euro's favour are its 'oversold' condition and the

fact that almost everyone expects a rate hike from the Fed and extended

monetary easing from the ECB. This could enable the euro to rebound from

support over the weeks ahead regardless of the events mentioned above,

although we think it's too risky to bet on a euro rebound at this time.

The Chinese Yuan continues to slide

The first of the following charts shows the performance of the

Yuan/US$ exchange rate over the past 10 years using monthly average

prices. The second of the following charts zooms in on the Yuan's

shorter-term performance using daily closing prices.

Chart source: Pacific Exchange

Rate Service

The Yuan has been weak relative to the US$ for

almost 3 years. This weakness was predictable based on the Yuan's

over-valuation and will probably persist for many more months. What hasn't

been predictable is the financial-world's reaction to the Yuan's most

recent bouts of weakness.

We are referring to the fact that the

financial world outside China pretty much ignored the sharp declines in

Yuan/US$ that occurred during May-July and over the past two months.

Pronounced weakness in the Yuan was widely viewed as very important last

year, but this year it has generally been viewed as irrelevant.

China's government, however, is worried by the relentless decline of its

currency. It has been selling-off its US$-denominated reserves to offset

the downward pressure on the Yuan resulting from capital outflows and is

now

readying new restrictions on outbound foreign investment in an effort

to relieve the downward pressure.

This strikes us as a significant

short-term threat to stock and bond markets in the major economies, with

stocks being at greater short-term risk due to being 'overbought'.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/

![]()