![]()

![]()

![]()

![]()

- Interim Update 31st May 2017

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Monetary support

continues to evaporate

With all the necessary

money-supply data for April-2017 now available we can report that the

year-over-year rate of growth in G2 (US plus euro-zone) True Money Supply

is now 7.2%, which is down from 7.8% a month earlier and a new 2-year low.

This is still comfortably above the boom-bust threshold of 6% (indicated

by the red line on the following chart), but the monetary backdrop is

nowhere near as supportive as it was just 6 months ago.

The Stock Market

The US

The stock market versus the economy

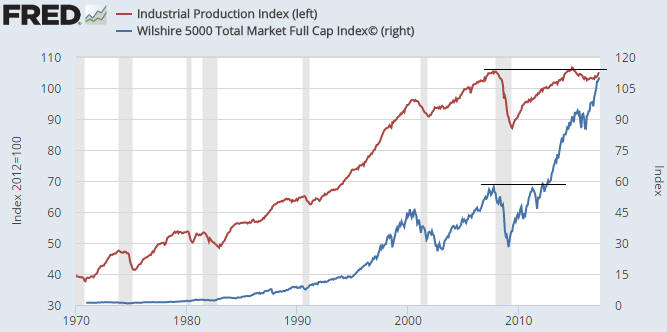

The following monthly chart shows the Wilshire5000 Index (an index

that covers the entire US stock market) and the US Industrial Production

Index (IP). We've drawn horizontal black lines on the chart to show where

each of these indices stands relative to its 2007 peak.

Notice

that the Wilshire5000 (the blue line) is currently almost double its 2007

level whereas IP is slightly below its own 2007 level.

The chart shows that there hasn't been a strong relationship between

the stock market and the economy over the past several years. There

actually never has been; it's just that the lack of a strong relationship

has been more obvious over the past several years than ever before. The

chart also shows the effectiveness of monetary stimulus at boosting asset

prices and the ineffectiveness of monetary stimulus at generating economic

progress.

Monetary stimulus (interest-rate suppression and money

pumping) falsifies price signals and therefore leads to more investing

errors than would otherwise occur. Projects and businesses that would

obviously not be viable in the absence of the new money get funded, but

since no new resources have been created these ventures -- sometimes aptly

referred to as bubble activities -- drain resources from other parts of

the economy. The economy is thus changed to become increasingly reliant on

'bubble activities', which, in turn, are reliant on the continuation of

artificial monetary support, but at some point the monetary support is

removed because the Keynesians in positions of influence finally begin to

notice an inflation problem. The longer it takes for the Keynesians in

charge to start worrying about price inflation, the greater the

distortions to the economic structure and the slower the rate of real

long-term progress. Also, the more severe the eventual recession.

The weak performance by US Industrial Production over the past 10 years

doesn't prove that monetary stimulus constitutes a long-term drag on the

real economy, but it is certainly consistent with this view.

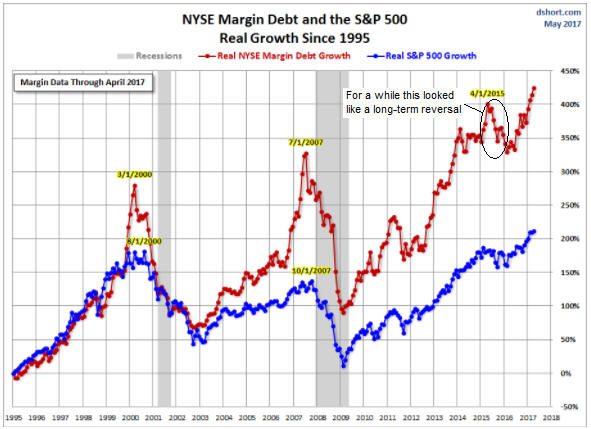

NYSE Margin Debt stays on its upward path

The cumulative NYSE Margin Debt as at the end of April was reported

earlier this week. As illustrated by the following

monthly chart prepared by Doug Short, it has extended its sequence of

new all-time highs in 'real' terms. In other words, stock-market leverage,

as measured by NYSE Margin Debt, is still increasing. This is important

because regardless of how over-valued the stock market becomes, a major

top won't occur while leverage is still increasing. To put it another way,

valuation risk will only come to the fore and cause a major bearish trend

after leverage stops increasing.

Based on the admittedly-sparse historical record, the next long-term

monthly-closing top for the S&P500 Index (SPX) will likely occur 3-5

months after the month that NYSE margin debt hits a long-term peak of its

own. However, the SPX's intra-day top could occur during the same month

that Margin Debt tops out.

It's worth mentioning that Margin Debt

temporarily gave a misleading signal during 2015 and the first half of

2016 that tricked us. We are referring to the fact that the decline in

Margin Debt from its April-2015 peak looked similar to the Margin Debt

declines from the 2000 and 2007 peaks. For a while, therefore, the

performance of Margin Debt suggested that the SPX's July-2015 top was the

long-term variety as opposed to the intermediate-term variety that it

turned out to be.

When Margin Debt resumed its long-term upward

trend in 2016 it was the first time that a sharp multi-quarter decline

from an all-time high did not mark a long-term peak. There was therefore a

difference this time around.

It was probably different because the

decline in Margin Debt from its April-2015 peak was accompanied by rapid

monetary inflation, whereas when Margin Debt turned down in 2000 and 2007

the monetary backdrop was much less accommodative. It seems that a

downturn in stock-market leverage won't 'stick' if central banks and/or

commercial banks are rapidly creating new money.

Current Market Situation

For about

a month after Trump was elected there was a frantic rally in the prices of

economically-sensitive equities, obviously based on the belief that

Trump's tax cuts and increased infrastructure-spending would lead to a

much stronger economy. It subsequently began to dawn on investors that the

'Trump stimulus' would either not happen at all or happen in a

watered-down fashion much later than originally anticipated. This caused

the economically-sensitive sectors to firstly stop rallying and to then

begin rolling over to the downside.

For example, the Bank Index

(BKX) began to form what appears to be an intermediate-term topping

pattern in December and is now very close to completing the pattern.

For another example, the Dow Transportation Average (TRAN) has traced

out a similar pattern to the BKX.

However, the realisation that the Trump stimulus theme was a dud

didn't discourage the bulls, it just prompted them to concentrate on a

small group of large-cap tech/internet/social-media stocks that apparently

are OK to buy at any price and will continue to grow rapidly regardless of

the economy. Consequently, the NASDAQ100 Index (NDX) hasn't just

maintained its post-election upward trend, it has accelerated upward.

Our conclusion is simply that the US stock market is behaving like it

is in the final phase of a long-term bullish trend.

Gold and the Dollar

Gold

The

US$ gold price broke upward from a multi-day consolidation pattern last

Friday and followed through to the upside over the first two trading days

of this holiday-shortened week. A test of the April high near $1300

appears to be on the cards.

Although the US$ gold price is nearing its 2017 high, the HUI/gold

ratio is nearing its 2017 low.

The fundamental backdrop is now gold-bullish, but the divergence

between gold and the HUI/gold ratio has short-term bearish implications

for both gold and the gold-mining sector. It's the main reason we don't

expect gold to do much more than test its April high before commencing a

sizable multi-week decline.

Note that if we get a significant

decline in the gold price within the coming 1-2 months in parallel with

the fundamental backdrop remaining gold-bullish, the set-up for a

long-side gold trade will be exceptional.

Gold Stocks

The HUI only had to move by a few points in one direction or the other

over the final two trading days of May to generate a breakout on the

monthly chart, but instead it moved sideways. Consequently, at the end of

May it remained between its 20-month and 50-month MAs. By the end of June

these MAs will have converged, so there will have to be a breakout this

month.

The following daily chart shows the choppiness of this year's price

action. There have been some significant multi-week moves, but there has

been virtually no net progress in either direction since early-January. To

be specific, the HUI was 192.3 at the close of trading on 4th January and

192.5 at the close of trading on 31st May.

The HUI could spike up

to around 210 in the near future without changing anything.

The Global X Silver Miners ETF (SIL) has performed similarly to the

HUI.

There's a decent chance that the HUI and SIL will decline to below

their December-2016 lows within the next two months, thus establishing a

very attractive risk/reward for a multi-month long-side trade.

The Currency Market

As noted on the following

weekly chart of the Dollar Index (DX), the current situation is possibly

equivalent to late-1999 (near the end of the correction that preceded the

final upward leg of a bull market) and is also possibly equivalent to

mid-2002 (a few months into the first downward leg of a bear market).

A reason to favour the former over the latter possibility is that the

overall financial-market environment has a lot more in common with

late-1999 than with mid-2002. For example, in late-1999 a US equity BULL

market was in its final speculative phase, as is probably the case today,

whereas in mid-2002 an equity BEAR market was nearing its completion. For

another example, in late-1999 the Fed was hiking interest rates and

monetary conditions were becoming less supportive of asset prices, as is

the case today, whereas in mid-2002 the Fed was easing aggressively and

monetary conditions were about as supportive as they ever get.

Note

that even under the late-1999 intermediate-term bullish scenario there

could be a spike down to the vicinity of the 150-week MA (the blue line on

the chart, currently at 95.5) in the near future before a reversal.

Updates on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Update

on Northern Empire Resources (NM.V), a recent addition to the

TSI Small Stocks Watch List (SSWL)

Update

on Northern Empire Resources (NM.V), a recent addition to the

TSI Small Stocks Watch List (SSWL)

NM has been

halted from trading on the TSXV since we first mentioned it in the 1st May

Weekly Update. In the 22nd May Weekly Update we wrote: "It's now

unlikely that the stock will trade near C$0.18 [its pre-halt price] when

the halt is finally lifted, but it may be possible to buy near the C$0.25

financing price and doing so would probably lead to a very good return

within 12 months."

The company has completed its asset

purchase deal and the associated financings, meaning that the reason for

the trading halt has been removed. The company now owns the Sterling gold

mine in Nevada and should have working capital of at least C$10M after

paying all costs associated with the mine purchase.

The stock will

resume trading on 1st June, but note that it has just undergone a 1:3

share rollback. Consequently, the C$0.25 (or thereabouts) buy level

previously mentioned is now equivalent to C$0.75.

Taking into

account the rollback, the shares issued in financings and other shares

issued as part of the asset purchase deal, we estimate that NM's total

share count is 46M.

Brief note on Asanko Gold (AKG)

Brief note on Asanko Gold (AKG)

AKG was mentioned

in the 24th May Interim Update as one of five gold-mining stocks that we

had short-listed for potential trades over the coming months. We wrote

that we hadn't yet decided on a buy level for the stock and that in this

regard a lot would depend on the FS results scheduled to be released on

5th June.

AKG's price collapsed on Wednesday 31st May in response

to a report from well-known short seller Carson Block.

Here's the link to a 4-minute Bloomberg interview with Block in which

he outlines his reasons for betting against the stock.

AKG has now

fully retraced last year's huge rally and is back to its early-2016 bear

market low. Is it worth buying near this price?

Possibly. There's a good chance that the company will provide some

positive information on 5th June and the stock price could rebound

strongly, but the unknowns are too large for our taste. AKG is therefore

unlikely to be one of the gold stock trading positions we add to the TSI

List within the next couple of months.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/

![]()