![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 1st February 2016

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in early-2015, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020. (Last update: 29 June 2015)

A secular BEAR market in the US Dollar began during the final quarter of 2000 and ended in July of 2008. This secular bear market will be followed by a multi-year period of range trading. (Last update: 09 February 2009)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak sometime between 2018 and 2020. (Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

|

Market |

Short-Term (1-3 month) |

Intermediate-Term (6-18 month) |

Long-Term (2-5 Year) |

| Gold | N/A |

Bullish (26-Mar-12) |

Bullish |

| US$ (Dollar Index) | N/A |

Neutral (22-Jun-15) |

Neutral (19-Sep-07) |

| US Treasury Bonds (TLT) | N/A |

Bearish (19-Oct-15) |

Bearish |

| Stock Market (DJW) | N/A |

Bearish (30-Dec-15) |

Bearish |

| Gold Stocks (HUI) | N/A |

Bullish (23-Jun-10) |

Bullish |

| Oil | N/A |

Neutral (26-Oct-15) |

Bullish |

| Industrial Metals (GYX) | N/A |

Neutral (09-Nov-15) |

Bullish (28-Apr-14) |

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

How much longer will the gold-mining bear market last?

The

original Fed versus today's Fed

What do changes in GLD's bullion inventory tell us about the future gold price?

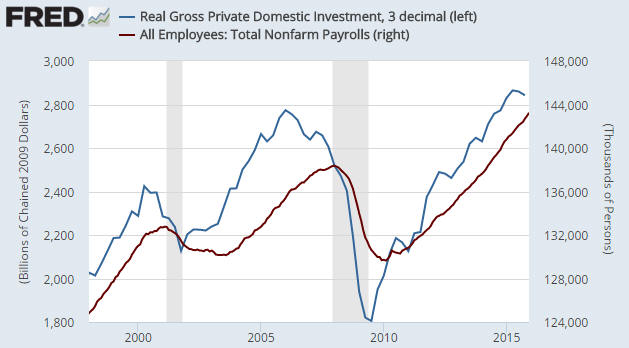

US Recession Watch

The following chart shows Real

Gross Private Domestic Investment (RGPDI) and Total Non-Farm Payrolls

(employment). Notice that RGPDI reversed downward in advance of the 2001 and

2007-2009 recessions. This is normal, as it also reversed downward in advance of

every other recession of the past 50 years. And notice that employment continued

to trend upward until after the 2001 and 2007-2009 recessions were underway.

This is also normal, in that employment is almost always still in an upward

trend at the start of a recession. Why, then, does the Fed focus on employment

as an economic indicator and why have so many commentators pointed to the strong

December-2015 employment report as evidence that the US economy is neither in

recession nor in imminent danger of entering recession? We don't know; you'd

have to ask them.

RGPDI turned down during the third quarter of last year and fell a little

further during the fourth quarter. This opens up the possibility that a

recession will soon begin (based on the historical record, if RGPDI had

continued upward there would be no chance of a short-term slide into recession),

but the reversal is not yet decisive.

The next significant piece of the puzzle will arrive on Monday 1st February. We

are referring to the latest calculation of the monthly ISM New Orders Index. A

decline in this index to below 48 will skew the odds heavily in favour of a

recession having just begun or being about to begin.

The unravelling of the

greatest boom ever

"It has fashioned itself into

an incendiary volcano of unpayable debt and wasteful, crazy-ass overinvestment

in everything. It cannot be slowed, stabilized or transitioned by edicts and new

plans from the comrades in Beijing. It is the greatest economic trainwreck in

human history barreling toward a bridgeless chasm."

The above is a colourful description of China's economic situation included in "Red

Ponzi Ticking", a recent article by David Stockman. We concur, although we

would replace the word "barreling" with "crawling". Due to centralised

government control of money, the banking industry (the quantity of bank lending,

the quality of bank lending (who gets the loans), the interest rates on deposits

and the interest rates on loans are all based on government command) and the

press (public criticism of the government risks imprisonment or worse), we

expect China's collapse to happen gradually.

Stockman's article cites a number of facts that highlight the breathtaking

extent of China's monetary-inflation-fueled boom and resultant mal-investment.

Here are some examples:

1. The PBOC expanded its balance sheet from $40 billion to $4 trillion during

the course of only two decades.

2. In the mid-1990s China had about $500 billion of public and private credit

outstanding. Today that number is $30 trillion or even more.

3. China's steel industry grew from about 70 million tons of production in the

early-1990s to 825 million tons in 2014. Moreover, annual crude steel capacity

now stands at nearly 1.2 billion tons, and nearly all of that capacity, which

amounts to about 65% of the world total, was built in the last ten years.

Evidence of the spectacular over-build is now obvious, given that 2016 steel

production is likely to be less than half of the steel industry's capacity.

4. In 1994, China produced about 1.4 million units of what were bare-bones

communist-era cars and trucks. Last year it produced more than 23 million mostly

western-style vehicles, or 16X more, and is now estimated to have annual vehicle

production capacity of around 33 million units. As is the case with the steel

industry, production in 2016 is going to be far below capacity.

5. In three recent years China used more cement than did the United States

during the entire 20th century.

6. It is estimated that there are about 70 million apartments in China that have

never been occupied.

We turned long-term bearish on China's economy in 2007, at which time it was a

very lonely position to take. It is now a much less lonely position, although we

wouldn't go as far as to say that it has become the mainstream view. The more

popular view is that although China is going through a rough patch, its

long-term prospects remain bright.

The sombre reality is that not only are China's long-term economic prospects not

bright, they are much bleaker today than when we turned long-term bearish back

in 2007. The reason is that the Keynesian stimulus measures and other policies

implemented since 2008 in an effort to keep the boom going have wasted an

extraordinary amount of wealth and dramatically magnified the imbalances. It is

therefore not possible that China's economy is experiencing only a 2-3 year

interruption to a secular up-trend. The secular trend is down.

That being said, it is certainly possible to overstate the global importance of

China's economic travails. China's economy is a mess, but China is not the

primary reason that the economies of the US and Europe are deteriorating. It's

more appropriate to view China's economic problems as a convenient -- from the

viewpoint of Western policy-makers -- excuse for the economic problems caused by

central-bank and government machinations in the West.

The Fed, the ECB, the US federal government and the governments of most European

countries have been following the same playbook as China's government and

central bank; it's just that by necessity (they don't have as much power) they

have been acting in a less draconian manner and have therefore created

relatively minor -- relative, that is, to what's happened in China -- economic

distortions and imbalances.

The point is that the local policy-induced economic distortions and imbalances

in the US and Europe would inevitably lead to severe and/or prolonged economic

weakness with or without China.

The Stock Market

The US

Current Market Situation

The risk/reward parameters are different depending on which US stock index we

consider.

For the S&P500 Index (SPX), the short-term upside potential noted in the 20th

January Interim Update remains applicable. Specifically, back then we said that

the market was sufficiently oversold to allow for a rebound that took the SPX to

either 1990 or the 50-day MA, whichever was lower.

The following chart shows that lateral resistance at 1990 is still below the

50-day MA, but the MA is declining and the two are likely cross within the

coming fortnight.

Short-term downside risk for the SPX is defined by the 20th January intra-day

low (1812). A test of this low is possible in February, but a solid/sustained

break below it probably won't happen until later in the year.

As advised in previous commentaries, a weekly SPX close below the August-2015

low (1867) is still needed to remove any remaining doubt that a bear market is

underway.

For the Dow Industrials Index, short-term upside potential is probably limited

by the declining 50-day MA, which is currently just above 17000.

The Dow hasn't yet traded below its August-2015 low, having reversed upward from

slightly above this critical level on 20th January. The August-2015 low (15370)

should therefore limit the downside until after the recent oversold extreme has

been fully worked off.

Unlike the SPX and the Dow Industrials, the Dow Transportation Average (TRAN)

has left no doubt that a bear market is in progress. In TRAN's case, the price

decline of the past two months was so severe that the August-2015 bottom now

defines the short-term upside potential. In other words, the best that TRAN is

likely to do over the next few weeks is return to the vicinity of its

August-2015 low near 7400.

As is the case with the other indices, short-term downside risk is defined by

the 20th January intra-day low (6403).

In last week's Interim Update we cautioned against being in a hurry to establish

new bearish speculations. Due to the sizable gains made by the stock indices

over the final two days of the week the risk/reward for a new bearish position

-- in the form of either put options or inverse ETFs* -- has improved, although,

as noted above, the indices are probably not going to do any worse during the

weeks immediately ahead than test their January lows.

The current plan with regard to our own money management is to stay out of put

options on the US stock indices until the SPX gets close to its 50-day MA.

Getting close to the 50-day MA will possibly take a few weeks.

*We much prefer put options to inverse ETFs or bear funds,

but many other traders prefer the ETFs and mutual funds. When attempting to

profit from a trend, stick with the method you are most comfortable with as long

as it works for you.

Oil and the Stock

Market

At the beginning of last year there was a lot of chatter about how the decline

in the oil price was going to boost the US economy by freeing-up money to fund

consumption of non-oil-based products. It would work like a tax cut, we were

told. However, the following chart shows that over the past 12 months the SPX

and the oil price have tended to move up and down together, which superficially

suggests that a rising oil price has come to be viewed as an economic plus and a

falling oil price has come to be viewed as an economic minus.

What's actually happening, we think, isn't that a falling oil price has gone

from being perceived as an economic stimulant to being perceived as an economic

depressant, it's that both the stock market and the oil market are responding

similarly to changes in global growth expectations. When speculators, as a

group, become less optimistic about global economic growth, they sell oil and

equities. And when speculators become more optimistic about global economic

growth, they buy oil and equities.

We think that the positive correlation between oil and equities will persist,

although oil is probably a lot closer than the SPX to its ultimate price bottom.

In fact, the scenario we favour involves the SPX dropping well below its Q1 low

later this year while the oil price does no worse than test its Q1 low.

The Emerging Markets

The Emerging Markets Equity ETF (EEM) has rebounded along with everything else

in the equity world since 20th January. And like almost everything else in the

equity world it will probably make some additional gains, or at least spend some

more time working off its 'oversold' extreme, before commencing a decline to

well below its January low.

However, the short-term risk/reward looks more bearish for EEM than for the US

stock indices. The reason, as outlined in previous commentaries, is the

potential for EEM to suffer a rapid price decline that would bring it into line

with industrial commodities.

Due to the risk that EEM will suffer a large and fast decline within the next

couple of months, we are presently keener to establish a new bearish EEM

position than to open a new bet against any of the US stock indices. We might

therefore start averaging back into the June-2016 $25 EEM put options if EEM

moves up to resistance at $31-$32 this week. An alternative, for those who want

to speculate and aren't comfortable with options, would be to buy the ProShares

UltraShort Emerging Markets Fund (EEV) if it drops to around $24 this week. Keep

in mind, though, that losses on any leveraged ETF positions should be kept in

check via the use of 'stops' or another risk management technique.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Feb 01 |

Personal Income and Spending ISM Mfg Index Construction Spending |

| Tuesday Feb 02 | Motor Vehicle Sales |

| Wednesday Feb 03 | ISM Non-Mfg Index |

| Thursday Feb 04 |

Q4 Productivity and Costs Factory Orders |

| Friday Feb 05 |

Monthly Employment Report International Trade Balance Consumer Credit |

Gold and the Dollar