-- Weekly Market Update for the Week Commencing

1st August 2016

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Neutral

(27-Jun-16) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Bullish

(29-Feb-16) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Bearish

(19-Oct-15)

|

Bearish |

|

Stock Market

(DJW)

|

N/A |

Neutral

(04-Jul-16) |

Bearish

|

|

Gold Stocks

(HUI)

|

N/A |

Neutral

(04-May-16) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Bullish

(04-July-16) |

Bullish |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

Helicopter Money

Summary of current

thinking/positioning

1) Concerned about short-term

downside risk in gold, silver and the associated mining stocks, but

comfortable maintaining substantial 'core' exposure in anticipation of

large additional gains over the next two years. Continuing to pick away at

'special situations' -- small/illiquid gold stocks that could generate

large gains independently of sector-wide performance.

2) Planning

to increase exposure to non-gold commodity-related stocks (primarily

base-metals producers/explorers, but also energy and agriculture

companies) during periods of price weakness over the next four months in

anticipation of 2017-2018 being a very bullish period for commodities.

3) Thinking that the US stock market is unlikely to do much on either

the upside or the downside over the coming month, but also thinking that

the time has arrived to START preparing for the possibility/risk of

significant downside during September-October.

5) Speculating on

short-term downside in the 'safe haven' government bonds, but the trade is

not working. This trade will be a failure unless the T-Bond drops sharply

within the coming six weeks.

6) Starting to suspect that the

commodity currencies have completed the downward corrections that began in

late-April.

7) Maintaining a large cash reserve in recognition of

the downside risk in almost all equities, although the cash percentage has

been reduced over the past month via the accumulation of non-gold

commodity stocks. Current cash percentage is around 45%.

Economics and

Monetary Stuff

The Fed did what was

expected

The statement issued by the Fed at the conclusion

of the 26th-27th July FOMC Meeting was exactly what everyone SHOULD have

been expecting. In particular, the Fed a) made no monetary changes, b)

opined that the US economy was doing fine, and c) kept alive the

possibility of a rate hike before year-end while remaining non-committal

with regard to timing.

Based on the fairly minor market reaction to

the Fed's statement it is clear that almost everyone was expecting what

they should have been expecting.

That being said, there was a small

change in interest-rate expectations. For example, the Fed Funds Rate

(FFR) implied by the January-2018 Fed Funds futures contract dropped 3

basis points (0.03%) on the day of the FOMC announcement. This would

normally be a irrelevant fluctuation, but in today's environment almost

any change in the expected FFR provokes noticeable changes in the major

financial markets.

Although under more normal circumstances it

would still be a trivial fluctuation, there was a more significant decline

in the expected level of the FFR on Friday 29th July in reaction (it

seems) to an unexpectedly-low first estimate for Q2 GDP growth. As

illustrated by the following daily chart of the January-2018 Fed Funds

futures contract, there was a decline of around 6 basis points in the

expected level of the FFR on Friday (the implied interest rate is 100

minus the price of the futures contract). Furthermore, over the course of

the week the expected level of the FFR in January of 2018 fell 12 basis

points, which means that last week the market went from assigning a 100%

probability of a Fed rate hike by the end of next year to only a 50%

probability of such an event.

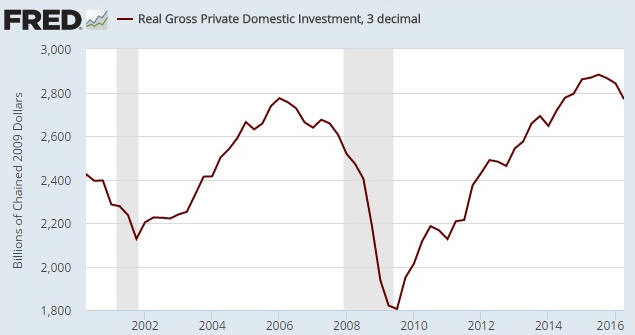

The next US recession

Real Gross Private

Domestic Investment (RGPDI) is the most reliable leading indicator of US

economic recession. Its trend has always reversed from up to down in

advance of a recession (there have been no false negatives) and only in

advance of a recession (there have been no false positives). The latest

iteration of this economic indicator became available on Friday 29th July.

RGPDI peaked in Q3-2015 and -- assuming there isn't a sizable upward

revision to the Q2-2016 number reported last week -- has now fallen far

enough from its peak to confirm that a trend reversal has taken place.

This doesn't tell us that the US economy is currently in recession or that

a recession is imminent. In fact, we know from shorter-term indicators

that the US economy is not currently in recession and is unlikely to enter

recession within the next two months. What it tells us is that the most

important precondition for a recession is now in place and that the meter

is effectively running.

Over the past 60 years, the longest time

from a peak in RGPDI to the start of a recession occurred during

2006-2007. In that historical case, RGPDI peaked in Q1-2006 and a

recession began in Q4-2007. If the delay that occurs this time around

matches the 2006-2007 delay, a recession will begin in Q2-2017.

Based on RGPDI and shorter-term indicators such as the ISM Manufacturing

New Orders Index, our guess is that the next US recession will begin no

earlier than Q4-2016 and no later than Q2-2017.

The T-Bond has

been resilient

Despite emerging signs of "price

inflation", the T-Bond is refusing to buckle. As illustrated by the

following chart of TLT (a proxy for the long end of the US government bond

market), a pullback during the first three weeks of July failed to gain

traction and more than half the loss from the early-July peak was quickly

recouped.

We have some TBT call options (TBT is a fund that moves in the

opposite direction to TLT at twice the pace) that will expire worthless in

September unless there's a sharp decline in the T-Bond price within the

next few weeks. We would exit these call options to salvage their

remaining value now if not for the fact that the T-Bond price and the US$

gold price are tracking each other closely.

The fact that the

T-Bond and gold are currently trading as if they were joined at the hip

means that we can use TBT calls to partially hedge our long exposure to

gold. We are therefore going to retain the TBT call options, although we

will consider switching from the September to the October series. The

extra 5 weeks of time to expiry could be critical.

The Stock Market

The US

The S&P500 Index (SPX) spent the past 11 trading days oscillating within a

narrow horizontal range near its high.

Unlike the gold-mining sector, which, as far as we know, has never

topped on an intermediate-term basis via several days of horizontal

trading within a narrow range, important tops in the SPX sometimes do

involve periods of low-volatility, horizontal trading. That doesn't mean

that the recent 2+ weeks of sideways movement is probably marking a

multi-month top; it means that the price action doesn't preclude such an

outcome.

Turning to the transportation sector, this is what we

wrote in the 20th July Interim Update:

"We will be interested

to see if there's enough strength in the overall market prior to the start

of a correction to push the Dow Transportation Average (TRAN) above

resistance.

TRAN has trend-line resistance very near its current

price, but the most important nearby resistance is defined by the April

high (8150). An ability to close above this resistance, even if only for a

single day, would remove a bearish non-confirmation -- one of the few

remaining pieces of evidence supporting the short-term bearish case."

1.5 weeks later and TRAN is still in roughly the same position.

Although we have a bearish non-confirmation by TRAN and a put/call

sell signal on our hands, we doubt that there will be anything more

serious on the downside over the coming few weeks than a routine pullback

in the SPX to short-term support at 2110-2130. The main reason is that

market internals such as the number of individual stocks making new

highs/lows are not yet warning of significant weakness.

With the

market 'overbought' and sentiment complacent, there remains a small chance

of a traditional September-October crash this year. However, for a crash

to happen during September-October a certain price pattern will have to

unfold over the weeks ahead and there will have to be a pronounced

weakening of market internals.

Europe

The

results of Europe's bank stress tests were released after the markets

closed on Friday 29th July, so we'll have to wait until Monday to see the

market reaction. In general, however, the results appeared to be no worse

than expected, with

most banks having survived the test. Furthermore, the Tier 1 capital

ratio of Deutsche Bank, Europe's most systemically-important bank, was

apparently better than many analysts had feared.

The Europe 600

Banks Index (FX7) ended the week slightly below resistance at 135. It will

be interesting to see if the reaction to the stress-test results is

sufficiently positive to get the FX7 above this resistance and generate a

preliminary signal of an intermediate-term bottom.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday August 01 |

Construction Spending

ISM Mfg Index |

| Tuesday

August 02 |

Motor Vehicle Sales

Personal

Income and Spending |

|

Wednesday August 03 |

ISM Non-Mfg Index |

|

Thursday August 04 |

Factory Orders |

|

Friday August 05 |

Monthly Employment

Report

International Trade Balance

Consumer Credit |

Gold and the Dollar

Gold and Silver

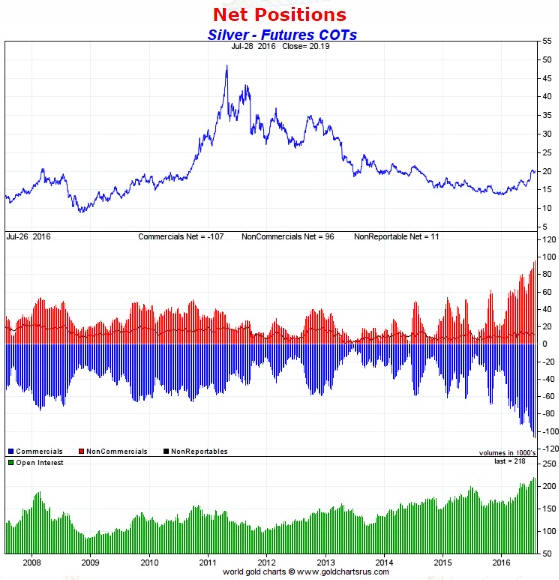

The Commitments of Traders (COT) Situation

The COT situations for both gold and silver are sounding loud warning bells,

but they've been doing so for months and nothing bad has happened to bullish

speculators. It's therefore tempting to just ignore the warnings and assume that

the current set of circumstances makes the unusually-large size of the

speculative net-long position irrelevant.

However, the fact that a risk

hasn't yet materialised is not evidence that the risk doesn't exist or can

safely be ignored. For example, it would be unwise to conclude that the risk of

playing Russian Roulette was not what it was cracked up to be just because you

were lucky enough to play every day for a week without blowing your brains out.

As we've mentioned many times in the past, an unusually-large speculative

net-long position will never be the cause of a trend reversal from up to down.

What it does is exacerbate the decline that follows a trend reversal. That is,

the risk -- or opportunity, as the case may be -- of an extremely lopsided COT

situation will only materialise when the price-trend reverses course for reasons

that have nothing to do with the COT situation.

During the latest period

for which there are COT numbers (the 5-day period ending 26 July), the total

speculative net-long position in COMEX gold futures dropped a little in parallel

with a $12 price decline. This is normal and leaves gold's COT situation

unchanged. Silver's COT situation, on the other hand, has become more extreme

despite a decline in the silver price. As illustrated below, the total

speculative net-long position (the mathematical offset of the commercial

net-short position) in silver futures has moved further into uncharted territory

over the past couple of weeks despite a pullback in the silver price.

The

recent shift in silver's COT situation adds to the downside price risk and is

evidence that the underlying physical market is weak (it suggests that upward

price pressure caused by speculative buying of futures is being counteracted by

selling of the physical commodity), but at the same time it improves the chances

of a 1-3 week surge to a new high prior to the start of a serious decline. This

is because it shows that speculators, as a group, are becoming increasingly

confident in the upward price trend.

Chart source:

http://www.goldchartsrus.com/

Current

Market Situation

In the 20th July Interim Update we noted that it

isn't normal for minor changes in expectations regarding the Fed Funds rate to

consistently have meaningful effects on gold's fundamentals or price action, but

it's happening now. It's happening now for two reasons. First, the entire

financial world has come to be dominated by monetary policy. Second, gold's

price action since February of this year has been dominated by speculators in

the futures market and these speculators have, as a group, been buying/selling

in response to small changes in the expected actions of the Fed. For example,

during the first three weeks of July the gold price pulled back as the expected

level of the Fed Funds Rate (FFR) drifted upward, and last week the gold price

rose in parallel with a slight decline in the expected level of the FFR. Refer

to the Fed Funds futures chart included earlier in today's report for more

information.

Small changes in the expected level of the FFR are also

being captured by the currency market, the bond market, and, of special

relevance to gold, the bond/dollar ratio (the T-Bond price divided by the Dollar

Index). For example, in response to last week's fairly minor decline in the

expected FFR there was a pronounced upward reversal in the bond/dollar ratio and

a predictable -- based on the strong positive correlation between this ratio and

the US$ gold price -- rally in the gold market.

During the decline from its July peak the gold market generated a warning

signal in the form of a break below the 20-day MA, but at no time did the gold

price breach trend-defining support at $1308. As noted in the 25th July Weekly

Update: "There will be a realistic chance of a surge to $1400 prior to a

multi-month top as long as this support [at $1308] holds on a daily closing

basis."

Last week the gold price not only managed to stay above

$1308, it rallied far enough in response to a down-tick in the expected FFR to

move back above its 20-day MA. The chance of a near-term rise to $1400 has

therefore improved.

Gold Stocks

Last week we wrote:

"There has

been an early warning of a top in the form of a daily close below the 20-day MA,

but the price action does not have the look of a meaningful top. Let's put it

this way: If the HUI's intermediate-term rally ended earlier this month it would

-- as far as we can tell -- be the first time ever that a gold-mining-sector top

was put in place via several days of horizontal trading within a narrow range.

Normally, intermediate-term tops in the gold-mining indices take the form of an

inverted V.

As things stand, there is still a decent chance of a surge to

a new high within the next 1-3 weeks. This will likely remain the case as long

as the HUI holds above 235 on a daily closing basis."

Last week the

HUI not only managed to hold comfortably above support in the 235-240 range, it

reversed upward and made a marginal new high for the year. This has potentially

set the stage for a final surge and a top during August.

Last week's reversal kept the HUI in synch with the 1982-1983 rally in the

Barrons Gold Mining Index (BGMI). Here's the updated comparison.

From a fundamental perspective we aren't keen on the comparison between this

year's rally and the 1982-1983 bear-market rebound, but the historical record

contains no other gold-mining rally from a multi-year low that comes as close to

matching this year's price action.

If the HUI continues to track the

BGMI's 1982-1983 rally then it will surge to a high of around 300 by mid-August

and then drop back to the low-200s over the ensuing two months. But regardless

of whether it continues to follow the 1982-1983 pattern and regardless of

whether we are dealing with a new bull market or an incredibly-strong

bear-market rebound, the HUI's decline from the coming intermediate-term peak is

likely to be at least 25% and could be as much as 40%.

The

Currency Market

Last week's action in the currency market threw

the proverbial spanner into the works. Prior to Friday the Dollar Index was

holding at its 200-day MA and appeared to be completing a routine pullback.

However, Friday's combination of Japan's central bank not acting as stupidly as

expected and a much lower-than-expected estimate for US second-quarter GDP

growth transformed a normal-looking pullback into something more significant.

As illustrated below, the Dollar Index plunged below its 200-day MA on

Friday and appears to be headed for channel support at 94.5-95.0.

From our perspective, the Canadian Dollar (C$) put in the currency market's most

interesting performance last week. Although it didn't make a big move, the C$

piqued our interest because it began to rally shortly after breaking below

important support at 76 (refer to the following chart).

The false

downside breakout is an early warning that the C$'s correction is over, which,

if so, would have implications for other markets. Of greatest significance, if

the C$'s correction is over then the correction in the oil market is probably

close to being over.

A daily close above 78 would be a more conclusive

warning that the C$'s correction is over.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 29th July 2016:

Company

news/developments for the week ending Friday 29th July 2016:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, MD&A = Management Discussion and Analysis,

M&I = Measured and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value

using a discount rate of X%, P&P = Proven and Probable, PEA = Preliminary

Economic Assessment, PFS = Pre-Feasibility Study]

*Endeavour

Mining (EDV.TO) published its quarterly report for the June quarter.

EDV's latest quarterly results show the benefit of not being reliant on any

single or even any two mining operations, as lower-than-expected output from two

mines (Nzema and Tabakoto) and teething problems associated with the startup of

the Karma gold mine (Burkina Faso) were offset by better-than-expected

performance from two other mines (Agbaou and Ity). Overall, it was an in-line

production result that keeps the company on track to achieve its

upwardly-revised (due to the acquisition of True Gold Mining) 2016 guidance of

590K-600K ounces.

EDV's balance sheet has undergone a large and very

positive transformation over the past year. After having well in excess of

US$200M of net debt a year ago, including the recently-completed equity

financing the net debt figure has dropped to only US$24M. EDV is now

conservatively geared and well positioned to complete the construction of its

Hounde mine in Burkina Faso over the coming 12 months.

Despite the

tripling of its stock price since the beginning of this year, EDV still offers

reasonable long-term value in absolute terms and good value relative to many of

its peers. However, regardless of how high the stock price moves over the next

few weeks an opportunity to buy the shares at a much lower price will probably

arrive in the midst of a sector-wide correction during September-October.

*Premier Gold (PG.TO) announced that it has agreed

to buy Yamana Gold's Mercedes gold-silver mine in Sonora, Mexico, for US$122.5M

of cash plus 6M PG shares plus 3M PG 2-year warrants with an exercise price of

C$4.75. Excluding the warrants, at a PG stock price of C$4.60 and a C$/US$ rate

of 0.76 the purchase price equates to about US$143M.

Mercedes is an

underground mining operation that is forecast to produce around 86K-ounces of

gold per year over the next few years at an AISC of around US$935/oz. This means

that PG has agreed to pay about US$1660 per ounce of annual gold production,

which is reasonable for an asset of this type in the current market. Also, the

current M&I resource is about 870K ounces and there is apparently a lot of

exploration-related upside potential.

This is a positive development for

PG, but from our perspective the good news was partly offset by

lower-than-expected 2017 production guidance for the company's South Arturo

project. According to the information released with the Mercedes acquisition

news, PG's 40% share of South Arturo's 2017 production is forecast to be 50K

ounces, which is about half of what we were expecting. PG's total production

guidance for 2017 is now 138K ounces.

PG will be able to finance the

Mercedes purchase with existing financial resources and perhaps some new debt,

although we won't be surprised if the company does an equity financing to cover

part of the cost.

Due to the Mercedes acquisition it is now reasonable to

compare PG with companies such as Richmont Mines (RIC). Such comparisons suggest

that PG is worth about 50% more than its current stock price, although what PG

is actually worth will be influenced to a large extent by the

soon-to-be-released FS for the Trans-Canada project.

PG has been a

relatively strong stock over the past few years. For example, if the HUI had

matched PG's performance over the past three years then it would now be trading

at around 500. However, PG has been a relatively poor performer this year,

although on a relative basis it has turned around over the past month. The lower

section of the following chart shows PG relative to GDXJ.

For

the first time this year PG has risen to a price where partial profit-taking

could be appropriate for those with substantial exposure to the stock. We have

substantial exposure to PG and sold 25% of our shares on Friday 29th July, but

this shouldn't be viewed as a bearish shift of opinion. The sale was a routine

money-management action designed to reduce the stock's weighting in our

portfolio to a more comfortable level.

*Ramelius Resources

(RMS.AX) published its quarterly report for the June quarter.

The report confirmed that the company was strongly cash-flow positive during the

latest quarter, boosting its cash by A$12M to around A$50M. Furthermore, FY2017

production guidance of 135K ounces at an AISC of A$1050 (US$787) per ounce

suggests that the company will be strongly cash-flow positive over the coming 12

months.

Operationally, RMS continues to perform very well.

Also,

RMS announced that it has raised A$25M by issuing 50M new shares at A$0.50/share

to institutions in North America and Australia. The funds will be used to

accelerate the development of deposits at/near the company's Mt Magnet gold mine

with the aim of growing production to 150K ounces in FY2018 (from the 135K

ounces expected to be produced in FY2017) and extending the mine life.

This equity financing came as a big surprise, because the work that is being

funded by the newly-raised money could have easily been funded by existing

financial resources (the $50M of cash mentioned above plus an undrawn $10M

credit facility). However, with the stock price near a multi-year high and a

gold correction in the offing, the financing was well timed.

By slightly

reducing both risk and reward, the financing doesn't significantly change our

opinion of the stock.

*Resolute Mining (RSG.AX)

published its quarterly report for the June quarter. This report's salient

details were previously announced by the company and outlined at TSI in the 11th

July Weekly Update.

As is the case with EDV, RSG's balance sheet has

undergone a large and very positive transformation over the past year. Without

issuing any new shares, over the past year the company has gone from having net

debt of A$64M to having net cash of A$75M.

*Taseko Mines

(TGB) published its quarterly report for the June quarter. TGB is a

moderately-high-cost producer of copper and the copper price is within 10% of a

7-year low, so it isn't surprising that the company just reported another poor

quarterly performance in terms of bottom-line profit (the bottom-line loss was

C$19.3M).

Production costs were down slightly from the preceding quarter

(from US$2.11/pound to US$2.07/pound) and are expected to drop a little more

over the coming two quarters, but near the current copper price of US$2.20/pound

this company will not do any better than break even. At US$2.50/pound it would

probably be able to generate a reasonable profit and at US$3.00/pound it would

probably be very profitable (and the stock price would be much higher). We are

interested in owning TGB and accumulating the stock on weakness in anticipation

of a rise in the copper price to $3/pound next year.

TGB's balance sheet

is not in great shape. In particular, at 30th June the company had net debt

(long-term debt minus working capital) of C$271M, which is up from C$260M at the

end of the previous quarter. This means that there was an $11M balance-sheet

deterioration during the latest quarter.

However, due to its $88M of

working capital the company does not have a short-term financial problem.

Provided that the copper price is in the process of basing, TGB won't experience

a cash crunch.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.barchart.com/

http://bigcharts.marketwatch.com/

http://research.stlouisfed.org/