--

Weekly Market Update for the Week Commencing

2nd July 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in mid-2016, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. A major decline in government bond prices will

unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom

in 2020 or later.

(Last update: 11 September 2017)

A cyclical BEAR market in the

US

Dollar

began in 2016-2017.

(Last

update: 11 September 2017)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak in 2020

or later.

(Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

|

Market |

True Fundamentals Model (TFM) |

|

Gold (US$ Price) |

Bullish (29 Jun 2018) |

|

US Equity (SPX) |

Bearish (29 Jun 2018) |

|

Currency (Dollar Index) |

Bullish (27 Apr 2018) |

|

Commodities (GNX) |

Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

Can

silver rally without gold?

Summary of current

thinking/positioning

1) With the euro and the Dollar

Index (DX) having again held above/below critical levels (1.156 for the

euro, 95 for the DX) on a weekly closing basis, the stage is set for

another multi-week euro rally and DX decline.

2) Gold and silver

prices either bottomed last week or will bottom during the first half of

July.

3) There is still a realistic chance that the SPX will make

a new all-time high in July, but risk is increasing and there are

preliminary signs that the US stock market is rolling over into what could

be a substantial decline.

4) The commodity markets are mixed, with

some stretched to the downside on a short-term basis while others, most

notably oil, are stretched to the upside.

5) The T-Bond price

should have an upward bias for at least another 2-3 months.

6)

Holding a cash reserve of around 30% and looking for opportunities to

build up this reserve.

A very

interesting monthly close

As expected, the closing prices

on Friday 29th June (the end of the week, the month and the quarter)

provided useful information about the gold and currency markets.

With regard to the gold market, in last week's Interim Update we wrote:

"Unless the gold price gains at least US$16 over the final two

trading days of this week it will end the month of June below its 21-month

MA and generate more evidence that gold is NOT in a bull market (not that

we need more evidence). Of greater significance as far as the next few

months are concerned, a Friday 29th June close below the 21-month MA would

suggest that there will be a spike low to create a multi-month bottom in

July, whereas a rebound over the coming two days that enables the gold

market to avoid a monthly close below the 21-month MA would suggest that a

multi-month bottom is already in place."

As illustrated by the

following monthly chart, the US$ gold price ended Friday's session well

below its 21-month MA. This warns that there may be a spike to a new low

for the year prior to the start of a rally worth trading and constitutes

additional evidence that gold is not in a bull market.

In last week's Interim Update we also wrote that the Dollar Index (DX)

has both intermediate-term lateral resistance and monthly moving-average

resistance (the 20-month MA) near 95 that should not be breached on a

weekly or monthly closing basis IF the DX commenced a bear market in

January-2017.

As illustrated by the following monthly chart, the DX

failed to end last month above the aforementioned resistance. Also, on

Friday 29th June the euro again managed to avoid a weekly close below

critical support at 1.156. Therefore, the 29th June closes kept alive the

possibility that the DX's recovery from its Q1-2018 bottom is nothing more

than a rebound within a bear market.

Developing the

right shoulder

In the 14th May Weekly Update we

wrote: "The bond market is probably close to a multi-month bottom, but

new lows in bond prices (new highs in bond yields) are likely during the

second half of this year." The T-bond bottomed later that week and

has since rebounded. The rebound has been significant, although for the

reason discussed below we expect that it will continue for at least

another 2-3 months.

Rather than look at the T-Bond itself, today

we'll look at our favourite T-Bond proxy: the iShares 20+ Year Treasury

Bond ETF (TLT). Our interpretation of the following chart is that over the

past 18 months TLT has been developing the "right shoulder" of a long-term

"head and shoulders" top. Therefore, when we write that the T-Bond rebound

probably will continue for at least another 2-3 months we mean that TLT

probably will spend more time developing its "right shoulder" before

embarking on the decline that completes the long-term topping pattern.

The main reason to expect T-Bonds (and TLT) to have an upward price

bias for at least a couple more months is that speculators, as a group,

are still massively short note and bond futures. Of particular

significance, the following chart shows that although the speculative

net-short position in 10-year T-Note futures has pulled back a little over

the past several weeks, it is still close to the record high reached in

May.

We expect that there will be a lot of short covering on the

part of speculators before the Treasury market commences its next

substantial downward trend. Therefore, even though much lower bond prices

(much higher bond yields) are likely within the coming 12 months, it is

too soon to return to the bearish side of the T-Bond trade.

Oil and copper go

their separate ways

Two weeks ago we thought that

the oil price correction still had a way to go, with $58 being a likely

target for a correction low. However, the correction ended prematurely and

the price then rose in a virtual straight line to a new multi-year high.

News that OPEC was going to increase production by less than expected

was the catalyst for the turnaround. Ordinarily news of this nature

wouldn't result in more than a 1-2 day bounce, but in this case it set in

motion a near-vertical 2-week price rise. The reason is that the physical

supply-demand situation in the oil market was already bullish. As pointed

out in many previous TSI commentaries, the oil futures curve tells us that

oil's physical supply-demand situation turned bullish last November and

has remained so.

Right now both the West Texas Intermediate and

Brent Crude markets are strongly 'backwardated', meaning that near-term

futures contracts are priced well above later-dated contracts. This

indicates that supply is tight relative to demand.

At the same

time, the surge of the past fortnight has left the market short-term

'overbought'. Consequently, we doubt that the price will make significant

additional headway before pulling back by a few dollars.

While the

oil price was rallying strongly over the past two weeks the copper price

was building on its early-June downward reversal. And whereas oil is now

short-term 'overbought', copper is now short-term 'oversold'. Therefore,

we won't be surprised if a near-term pullback in the oil price goes along

with a rebound in the copper price.

Both of the copper scenarios mentioned in the following excerpt from

our 18th June commentary remain plausible at this time:

"...the

extremely aggressive speculative positioning indicated by the latest COT

report combined with Friday's decisive breach of $3.20 suggests that we

are dealing with something more bearish than a routine 1-2 week

correction. It suggests that either the previous week's move up to around

$3.30 created an intermediate-term double top, in which case a decline to

as low as the $2.50s could precede the next substantial rally, or the

price will chop around between $2.95 and $3.30 for a few more months

before resuming its multi-year upward trend."

However, it goes

without saying (but we will say it anyway) that if support at $2.95 is

breached then the second of the above-mentioned scenarios will be ruled

out.

The Stock Market

The price action leaves the door

open for new all-time highs in some US stock indices this month. For

example, the NASDAQ100 Index and the Russell2000 Index have possibly

completed routine pullbacks to their respective 50-day MAs. Also, the

following daily chart shows that the SPX made a marginal new all-time high

in gold terms last week. This is a short-term bullish development given

that the SPX usually peaks in gold terms before it peaks in US$ terms.

However, other indices are already showing signs of rolling over to

the downside. For example, both the Dow Industrials Index (chart included

below) and the Dow Transportation Average ended last week below their

200-day MAs, and the Bank Index (chart also included below) is

precariously poised at the edge of a virtual cliff.

Once a large stock market decline gets underway the root cause will be

tighter monetary conditions, but the proximate cause, or catalyst, could

be the increasingly heavy-handed attempts by governments to 'manage'

international trading/investing. The so-called "trade war", which involves

threats, counter-threats, backtracking, new threats and a few actual

policy measures, is creating uncertainty and could be the pin that bursts

the confidence bubble.

Happening in the background, but related to

the "trade war", is a recent sharp decline in China's currency. This sharp

decline is indicated by the sharp rise over the past month of the line on

the following US$/Yuan chart (the line on the chart rises when the Yuan is

weakening relative to the US$).

Now, it should be understood that

the bulk of what happened to the US$/Yuan exchange rate over the 2-year

period covered by this chart was mostly due to US$ strength/weakness. For

example, the Yuan's strength relative to the US$ during 2017 was due to

US$ weakness and the Yuan's weakness relative to the US$ during April-May

of this year was due to US$ strength. We know this because of the way the

Yuan performed against the euro. However, the June-2018 surge in the

US$/Yuan exchange rate was driven primarily by Yuan weakness.

We won't know for sure until China's central bank publishes its

international currency reserve figure for June, but the recent weakening

of the Yuan does not appear to be the result of a deliberate move by

China's government. However, regardless of its cause, if the Yuan weakness

persists it could be the catalyst for a fast stock-market decline that

drags commodity and gold stocks downward along with most other stocks.

This would be similar to what happened in reaction to a sudden bout of

Yuan weakness in August-2015.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday Jul-02 |

ISM Mfg Index

Construction

Spending

Canadian markets closed for public hol |

|

Tuesday Jul-03 |

Motor Vehicle Sales

Factory

Orders |

|

Wednesday Jul-04 |

US markets closed for public

hol |

|

Thursday Jul-05 |

ISM Non-Mfg Index

FOMC

Minutes |

|

Friday Jul-06 |

Monthly Employment Report |

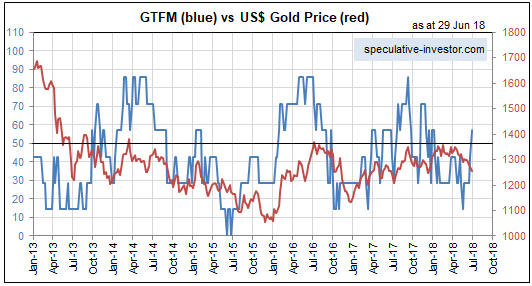

Gold and the Dollar

Gold

The Fundamentals

Our Gold True

Fundamentals Model (GTFM) turned bearish on 12th January 2018 and remained in

bearish territory until the end of last week, when it turned bullish. Here is

the chart comparing the GTFM (in blue) with the US$ gold price (in red) from the

Charts & Indicators section of the TSI web site. The chart is updated at the end

of each week.

It

was a small widening of credit spreads that tipped the Model into bullish

territory last week. Be aware that the Model is vulnerable to being whipsawed at

the moment due to the credit spreads component being close to its demarcation

level, but as things currently stand the fundamental backdrop is a tailwind for

the gold price for the first time since mid-January.

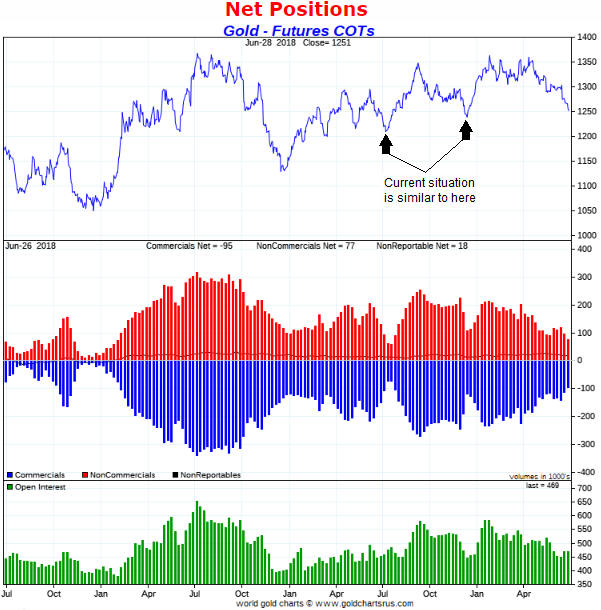

Sentiment

When assessing sentiment in

the gold and silver markets the only indicator that we need to concern ourselves

with is the Commitments of Traders (COT) information. Other sentiment indicators

just muddy the waters.

Below is a chart showing the net positions and

open interest (OI) in Comex gold futures. Taking into account both the net

speculative position and the OI, the COT situation now is much less supportive

than it was in December-2015, slightly less supportive than it was in

December-2016, and similar to what it was near the multi-month price bottoms in

July and December of last year.

Therefore, the message from the current

COT situation is that the stage is potentially set for a gold rally that lasts

about 2 months and adds $100-$150 to the price. To establish a sentiment

backdrop conducive to a larger/longer rally there probably will have to be some

additional price weakness.

The Price Action

We've been

anticipating a decline to test lateral support at $1240 (the December-2017 low)

prior to a short-term bottom. Last week the price traded as low as $1246.90,

which is close enough to the aforementioned support to be viewed as a test.

It's certainly possible that last week's low will turn out to have been a

successful test of support, but it's a little more likely that there will be a

decline to a new low during the first half of July prior to the start of a

tradable rally.

As

mentioned above, the sentiment situation suggests that if a short-term price

bottom is already in place then we may get a 2-month rise of $100-$150, but not

significantly more than that. However, additional price weakness during the

first half of July could enable a more substantial rally.

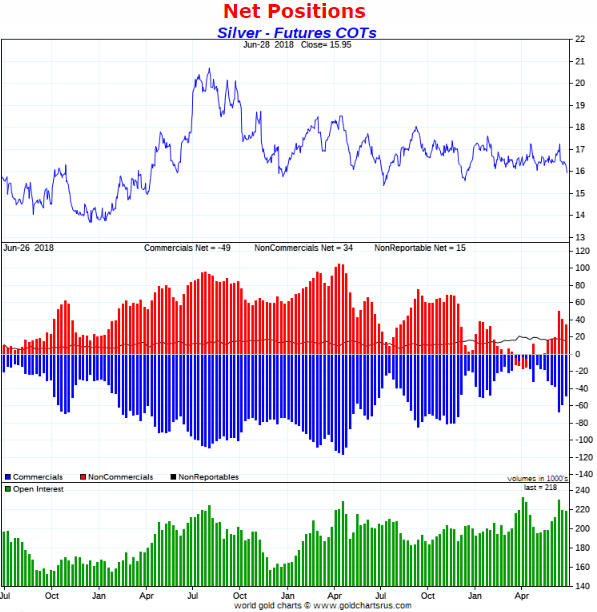

Silver

Silver traded below important support at $16.10 last Wednesday and then

quickly recovered to end the week above this support. This reversal was bullish,

but there are two reasons to be sceptical that a short-term price bottom is in

place.

The first reason is that there was minimal follow-through to the

upside after Wednesday's reversal. Specifically, after trading as low as $15.94

on Wednesday and then rebounding to end the day at $16.15, the price was able to

make an additional gain of only $0.05 by week's end. This means that the market

did the minimum it had to do to signal that a multi-month price bottom is in

place, but a more conclusive signal would have been generated by a weekly close

above $16.30.

The second reason is sentiment. Taking into account the net positions and open

interest in Comex silver futures as illustrated by the following chart, the

sentiment backdrop is no better than neutral for silver. In other words,

sentiment is neither a head-wind nor a tail-wind at the moment. The market is

not yet close to being 'sold out'.

As is the case with gold, there is a better than even money chance of

additional weakness in the silver market prior to a multi-month price bottom.

Gold Stocks

The HUI tested lateral support

defined by its March low on Thursday 28th June and then reversed course. This

reversal from near support may or may not have marked a short-term bottom. It's

too soon to make an educated guess either way.

The

ducks are now pretty well lined up for a sizable gold stock rally (a rally that

lasts at least two months and results in a HUI gain of at least 30%). One

concern, however, is that there hasn't been a sharp decline or capitulation that

'clears the deck'. A capitulation is not a prerequisite for the sort of rally

mentioned above, but the fact that it hasn't happened creates a risk. The risk

is that a trend-ending capitulation is yet to come. Another concern is the

likelihood, discussed above, that gold and silver will make new lows before

commencing tradable rallies.

In any case, it would be reasonable for

short-term traders to buy gold-mining ETFs and mitigate the above-mentioned

risks by placing daily-closing stops slightly below last Thursday's intra-day

lows. If stopped out it would be a matter of waiting for a new upward reversal

before re-entering.

The Currency Market

The Euro

Critical support for the euro

lies at 1.156. The euro ended last Thursday's trading session at 1.156, so even

a small decline on Friday would have resulted in a downside breakout. As it

turned out, the euro rebounded strongly on Friday and thus avoided the bearish

signal.

The fundamental backdrop strongly favours the US$ over the euro

at this time, so we aren't confident that the euro will continue to avoid a

weekly close below 1.156. As long as it does, though, it will be reasonable to

give the benefit of the doubt to the short-term euro-bullish scenario.

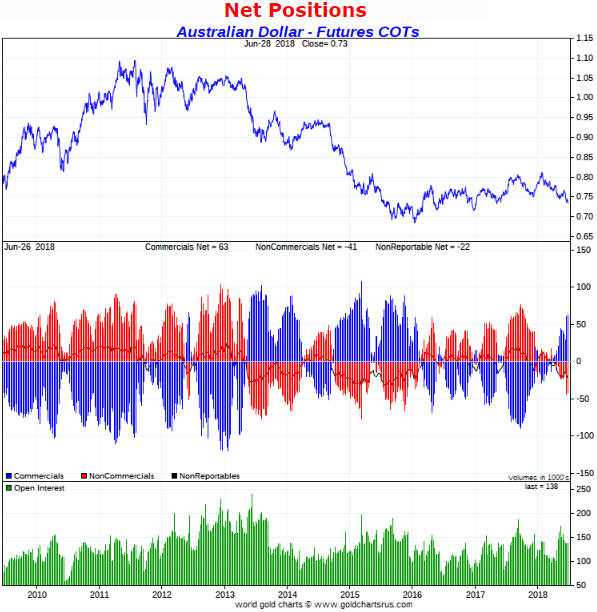

The Australian Dollar (A$)

The A$ has

been pressured downward by weakness in some commodity prices and speculation

that the 'trade war' will lead to a lot more commodity-price weakness in the

future.

The increasing popularity of anti-A$ speculation is illustrated

by the middle section of the following chart. The blue bars in this section of

the chart indicate the commercial net position, which is the inverse of the

total speculative net position.

The chart shows that speculators in A$

futures have done an about-face over the past 9 months. Last September they had

their largest net-LONG exposure in 4 years, but thanks to a wave of speculative

short-selling over the past two weeks they now have their largest net-SHORT

exposure in 2.5 years.

It is fair to say that speculative sentiment is

now very supportive of the A$, but there's a caveat: Based on the historical

record the total speculative net-short position in A$ futures could rise from

its current level of 63K contracts to as high as 100K contracts prior to the

start of the next multi-month rally.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 29th June 2018:

Company

news/developments for the week ending Friday 29th June 2018:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, MD&A = Management

Discussion and Analysis, M&I = Measured and Indicated, NAV = Net Asset Value,

NPV(X%) = Net Present Value using a discount rate of X%, NSR = Net Smelter

Return, P&P = Proven and Probable, PEA = Preliminary Economic Assessment, PFS =

Pre-Feasibility Study]

*Clean TeQ (CLQ.AX, CLQ.TO)

is developing the Sunrise nickel-cobalt-scandium project in New South Wales

(NSW), Australia, and was added to the TSI List in the 30th May Interim Update.

At that time all we had to go on -- as far as the economics of the project were

concerned -- was a PFS completed in October-2016, but the results of the

project's FS were expected within the ensuing month.

The results of the

FS were reported last week.

The FS was a disappointment because it

revealed substantially worse economics than the PFS. In particular, despite the

FS being based on significantly higher metals prices than the PFS, the estimated

post-tax IRR fell from 30% in the PFS to 19.1% in the FS.

An approximate

doubling of the pre-production capex was the reason for the deterioration in the

economics. The company explained the dramatic capex increase by referring to

improvements and additional capacity, but whoever did the PFS capex estimate

obviously made some mistakes.

Fortunately, although the numbers in the FS

were worse than expected they still point to the project being economically

viable at current metal prices. Furthermore, we like the fact that the

calculated NPV uses a discount rate of 8%. This is more conservative and far

more realistic than the 5% rate favoured by many junior mining companies.

Here are the salient figures from the PFS completed almost two years ago and

the just-completed FS:

1) Oct-2016 PFS:

a) Post-tax NPV(8%) and IRR = US$891M and 25%, resp., assuming $7.50/pound

for nickel (not including any sulphate premium), $12/pound for cobalt and no

scandium production.

b) NPV and IRR increase to US$1233M and 30% with

scandium-oxide byproduct.

c) Capex: US$680M.

d) Mine life: 20

years.

2) Jun-2018 FS:

a)

Post-tax NPV(8%) and IRR = US$1392M and 19.1% assuming $8.00/pound for nickel

(including $1/pound sulphate premium), $30/pound for cobalt and 10-tpa of

scandium-oxide production.

b) NPV and IRR increase to US$1670M and 21% at

current spot prices for cobalt and nickel.

c) Capex: US$1495M

d)

Mine life: 25 years.

e) FID (Final Investment Decision) expected

early-2019, assuming that off-take agreements and financing are arranged before

year-end.

It is worth noting that in terms of tonnes, nickel production

is expected to be about 5-times cobalt production. However, in terms of dollar

value, at current metal prices the Sunrise project's nickel and cobalt

production would be roughly the same. Therefore, Sunrise is not a nickel project

with a cobalt by-product, it is a project with nickel and cobalt co-products.

With regard to construction financing, instead of trying to finance the

US$1.5B capex on its own we think it would make sense for CLQ to bring in a

partner that funds the construction in exchange for part ownership of the

project. Considering the existing business ties of the company's co-chairmen

(Robert Friedland and Jiang Zhaobai), we wonder if there is an opportunity for

CLQ to enter a JV with a large Chinese company.

When CLQ was added to the

TSI List our suggestion was to buy half a position at around A$1.03 (the price

at that time) and wait for the FS before deciding whether, and at what price, to

buy more. A decision can now be made.

Based on the FS results, CLQ's

project is not as valuable as we thought. Also, the economics of CLQ's project

are more leveraged to metal prices than we thought. The greater leverage will

begin to work in favour of CLQ when metal prices resume their bull markets, but

will work against CLQ while metal prices remain in correction mode.

The

upshot is that we think it makes sense to stay with half a position pending

evidence that the cobalt correction has run its course.

*Cobalt

27 Capital (KBLT.V) advised that it has completed its C$300M equity

financing (by issuing new shares at C$9.75/share) and its US$300M purchase of a

cobalt stream associated with the Voisey's Bay project. Despite the dilution

caused by the equity financing, this should turn out to be a very good deal for

the company IF the cobalt price is $35/pound (the current price) or higher when

metal deliveries occur (deliveries begin in January-2021).

The

combination of the heavily discounted financing price and an intermediate-term

correction in the cobalt market has resulted in a large decline in the KBLT

stock price over the past few weeks. This has created an exceptional buying

opportunity in KBLT shares, but bear in mind that the EV (Electric Vehicle)

Metals story is a marathon, not a sprint.

Regarding the aforementioned

cobalt correction, the following chart shows that the price peaked in March at

US$95,000/tonne (about US$43/pound) and has since dropped to US$77,500/tonne

(about US$35/pound). We don't have an opinion on when or at what price level the

correction will end.

*Nevsun Resources (NSU) announced the initial resource estimate

for the Timok Lower Zone (TLZ) copper-gold project in Serbia. The TLZ is a JV

between NSU and Freeport McMoran (FCX), with FCX being on the way to earning a

54% stake by funding all work up to the completion of a Feasibility Study.

The TLZ deposit is massive. The initial estimate is 31.5 billion pounds of

copper in the Inferred category at an average grade of 0.86% copper or 0.96%

copper-equivalent (including the gold byproduct). The deposit is also very deep,

so unlike the Timok Upper Zone there is a big question as to whether it will

make economic sense to mine it. This question won't be answered until FCX

completes a lot more exploration and engineering.

At the moment the TLZ

is classic optionality play and therefore should be assigned a low valuation. In

our NSU valuation we are being very conservative and assigning it a valuation of

ZERO, although the fact that FCX is spending a lot of money on the project

indicates that it is worth substantially more than zero.

*Premier

Gold (PG.TO) advised that development of the next two mines at its

South Arturo JV (40% PG, 60% Barrick) has been accelerated. This is good news in

that it should result in these mines having some production this year, although

it will also result in greater capital spending this year.

*Tinka

Resources (TK.V) is an exploration-stage zinc miner that was added to

the TSI List only three weeks ago. Its flagship asset is the 100%-owned Ayawilca

project in central Peru.

As noted in our initial write-up:

"The

Ayawilca project has both size and grade going for it. The current Inferred

resource estimate, which was completed in November-2017, is 42.7M tonnes grading

6% zinc or 7.3% zinc-equivalent (ZnEq). This implies 5.6 billion pounds of zinc."

And:

"Step-out drilling by TK is continuing to hit wide

intercepts of high-grade zinc outside the boundaries of the existing resource.

This guarantees that the already-large resource will grow."

The

company announced last Tuesday that step-out drilling had hit a wide intercept

of exceptionally high-grade zinc. Specifically, a recent hole intersected 10.4

metres of 44.0% (!!) zinc and also had shallower intercepts of 21.2 metres at

9.0% zinc and 6.5 metres at 11.0% zinc. Due to this hole being outside the

boundaries of the existing resource it constitutes a new discovery and suggests

the potential for substantial resource expansion.

As explained in TK's

press release:

"The new discovery opens up significant areas of

untested potential, both beneath and adjacent to the existing mineral resource.

Most of the previous drill holes at Ayawilca were stopped a few metres into the

phyllite, which had been considered to be 'basement'. A new interpretation of

the geology at West Ayawilca indicated that the favourable limestone unit could

be repeated under low angle 'thrust' faults, a concept that is now corroborated."

We are bullish on zinc, but TK's deposit is evolving in a way that could

cause it to become far more valuable over the coming 12 months even if the zinc

price doesn't go up.

List

of candidates for new buying

From within the ranks of TSI stock

selections the best candidates for new buying at this time, listed in

alphabetical order, are:

1) AAU (last Friday's closing price: US$0.72)

2) CNL.TO (last Friday's closing price: C$3.79)

3) KBLT.V (last

Friday's closing price: C$8.83)

4) PG.TO (last Friday's closing price:

C$2.61)

5) PRQ.TO (last Friday's closing price: C$1.01)

The above

list is limited to five stocks. It will sometimes contain less than five, but it

will never contain more than five regardless of how many stocks are attractively

priced for new buying.

New

TSI Stock Selection: Sabina Gold and Silver (TSX: SBB). Shares: 252M issued,

269M fully diluted. Recent price: C$1.52

In the 18th June Weekly

Update we wrote that SBB would be added to the TSI List as a trade with an

expected duration of 3-9 months if the stock price dropped to C$1.53. It traded

as low as C$1.51 on Thursday 28th June and has therefore been added.

SBB

has three significant assets. From most to least important (in terms of dollar

value), they are:

1) The Back River gold project in Nunavut, northern

Canada.

Back River has a 7.1M-oz gold resource (5.3M ounces M&I, 1.8M

ounces Inferred) and a completed FS that indicates economic viability down to

US$1000/oz for gold. At a gold price of US$1250/oz the after-tax NPV(5%) and IRR

are C$606M and 28.3%, resp.

The project is almost fully permitted (there

is one water permit outstanding) and is construction ready.

The plan is

to build a mine (actually, a combination of open-pit and underground mines) with

average annual production of 200K ounces over an initial 12-year life. The cost

to build the mine is estimated to be C$415M and first production is currently

expected in 2021.

2) A silver royalty associated with Glencore's Hackett

River zinc-silver project in Nunavut.

The royalty entitles SBB to the

cash equivalent of 22.5% of the first 190M ounces of silver production and 12.5%

of silver production thereafter. The 22.5% rate likely would translate into the

cash equivalent of 3M silver ounces per year.

This royalty will become

extremely valuable if Glencore decides to move the project into the construction

phase.

Furthermore, there is a milestone coming up in October-2018 that

could motivate Glencore to move the project into construction. We are referring

to the fact that if Glencore hasn't announced a production decision by

October-2018 then SBB will have the right to buy the project for what Glencore

has spent on it over the past few years.

3) Cash of around C$89M.

As illustrated by the following chart, SBB traded as high as C$2.70 in September

of last year. This was due to anticipation of a takeover. A takeover bid never

materialised, but an eventual takeover remains likely due to the Back River

project's robust economics and the potential value of the Hackett River silver

royalty. These are high quality assets.

We think that SBB stands a good

chance of returning to the C$2.50-C$2.70 range as long as the gold price moves

back above $1310/oz during the second half of this year.

New

TSI Stock Selection: Osisko Gold Royalties (NYSE: OR). Shares: 156M. Recent

price: US$9.47

In the 18th June Weekly Update we wrote that OR

would be added to the TSI List as a trade with an expected duration of 3-9

months if the stock price dropped to US$9.10. It traded as low as US$9.10 on

Thursday 21st June and has therefore been added.

OR is like a hedge fund

that invests in gold/silver royalties, gold/silver streaming deals, and the

equity or debt of junior gold/silver mining companies. It has a large and

complex mix of assets that we are not going to attempt to value.

We have

added an OR trading position to the TSI List based on the price chart and the

expectation that the gold-mining sector is within a few weeks of commencing a

multi-month rally. The chart (see below) shows that over the past few years the

stock price has oscillated between US$8.50-$9.00 and US$14.00, with each move

from low to high or high to low lasting 6-9 months. Buying near the bottom of

this range has worked well in the past and we think it will work well again.

OR has been added to the List at US$9.10 on the expectation that it will

rebound to around US$14 over the coming 6-9 months.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.goldchartsrus.com/

Pacific

Exchange Rate Service