--

Weekly Market Update for the Week Commencing

4th June 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in mid-2016, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. A major decline in government bond prices will

unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom

in 2020 or later.

(Last update: 11 September 2017)

A cyclical BEAR market in the

US

Dollar

began in 2016-2017.

(Last

update: 11 September 2017)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak in 2020

or later.

(Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

|

Market |

True Fundamentals Model (TFM) |

|

Gold (US$ Price) |

Bearish (12 Jan 2018) |

|

US Equity (SPX) |

Bearish (25 May 2018) |

|

Currency (Dollar Index) |

Bullish (27 Apr 2018) |

|

Commodities (GNX) |

Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

Why

it's different this time

Summary of current

thinking/positioning

1) The Dollar Index and the euro

may have just competed multi-month counter-trend moves (up for the DX,

down for the euro), but more evidence is required to confirm this.

2) Gold has broken out to the upside in euro terms, but in US$ terms it

has not yet negated the 15th May downside breakout. This creates

uncertainty regarding the bullion market's short-term prospects.

3)

The SPX likely will make a new all-time high by the end of this month. The

risk/reward is not bullish, though, because a move to well above the

January high is unlikely and because there is a realistic chance of a

large decline during the second half of 2018.

4) There is no

evidence that the Swiss Franc has bottomed against the US$, but taking a

3-6 month view this currency's risk/reward looks very attractive.

5) New lows in bond prices (new highs in bond yields) are likely before

year-end, but the T-Bond price should have an upward bias over the coming

2-3 months.

6) Holding a cash reserve of around 30%.

Monthly Closing

Prices

The monthly closing prices for

May didn't signal any changes, but did provide useful information. For

example, by rebounding to end the 31st May session comfortably above

critical support the euro kept alive the possibility that it's recent

decline was just a sharp correction within a multi-year upward trend.

Apart from the euro, the monthly closes of greatest interest to us were

the US$ gold price, the T-Bond price and the SPX/euro ratio (the US stock

market in euro terms).

When gold is in a bull market, short-term

corrections within intermediate-term upward trends generally hold the

8-month MA (on a monthly closing basis) and intermediate-term corrections

generally hold the 21-month MA (on a monthly closing basis). However, when

gold is in a bear market or a long-term basing pattern these monthly

moving averages will tend to either act as resistance or be less

significant.

The following monthly chart shows that since making a

long-term bottom in December-2015 the US$ gold price has oscillated around

its 8-month and 21-month MAs. It also shows that the 31st May close was

below the 8-month MA and above the 21-month MA. This is consistent with

our view that gold is immersed in a long-term basing pattern, not a bull

market.

The 30-year T-Bond just achieved another monthly close below its

84-month MA, which means that another piece of evidence supporting the new

long-term bear market scenario has been added to the pile. However, bond

bulls could still argue that the T-Bond's current position is similar to

late-1999.

A rebound followed by a decline to below the May-2018

low would be the final nail in the bond bull market's coffin.

A monthly close by the SPX/euro ratio below its 24-month MA should

provide a reliable and timely signal that an equity bear market has begun.

For example, such a signal was generated in November-2007 -- one month

after the start of the last equity bear market.

Such a signal was

not generated during the 2015-2016 decline and also was not generated

during the H1-2018 decline. Furthermore, SPX/euro traded above its

January-2018 high during May-2018. This indicates that an equity bear

market has not begun.

US Recession

Watch

As regular TSI readers would

know, the three leading indicators of US recession that we care about are

the ISM New Orders Index (NOI), Real Gross Private Domestic Investment

(RGPDI) and the yield curve. It's still the case that not one of these

indicators is close to giving a recession warning.

The NOI, for

instance, has pulled back since making a 13-year high in December-2017,

but remains far above the level that it would have to drop below (the red

line on the following chart) to warn of a recession. Furthermore, the

latest data revealed an uptick for May.

The next quarterly calculation of RGPDI won't be available until

late-July, but the yield curve constantly updates and at the end of last

week it was near its flattest in more than 10 years. This is evidenced by

the following chart of the spread between the 10-year yield and the 2-year

yield. Therefore, we are yet to witness the trend reversal in the yield

curve from flattening to steepening that generally PRECEDES a recession.

Refer to last week's Interim Update for an explanation of why the yield

curve reverses course in this way prior to a recession.

Based on the latest data, our rough estimates of recession start-time

probabilities are unchanged from a month ago. Here they are:

-

Q2-2018: 0%

- Q3-2018: 10%

- Q4-2018: 30%

- Some time in 2019:

>80%

As previously explained, the main reason for our high 2019

recession probability estimate is the decline in the G2 (US plus

euro-zone) monetary inflation rate. It appears that the G2 monetary

inflation rate has fallen far enough to bring the artificial boom to an

end, with the only unknown being the timing of the boom-bust transition.

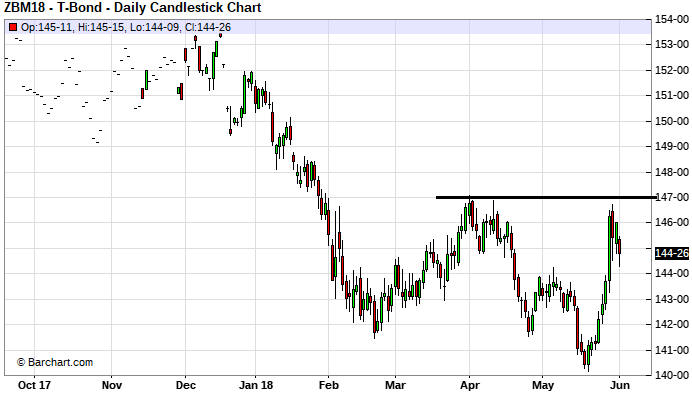

What to expect

from the T-Bond rebound

It was late April when we

started speculating that the T-Bond was close to a multi-month bottom and

it was one week ago that we identified 18th May as the date of the bottom.

It was also one week ago that we mentioned lateral resistance at 147 as an

upside target for a short-term T-Bond rebound. We guessed that this target

would be reached within three months, but thanks to the 'flight to safety'

prompted by Italy's political situation the target was almost reached

within two days.

The 29th-30th May spike up to near resistance at

147 likely created a top that will hold for at least two weeks, but at the

same time it probably means that the ultimate top for the rebound will be

above 147.

The COT data also suggest that the T-Bond's rebound will extend beyond

147. We are referring to the fact that despite the quick rebound in the

Treasury market, the latest COT report shows that speculators increased

the size of their collective bearish bet in 10-year T-Note futures to a

new all-time extreme.

We now have 149-150 in mind as an upside

target for the T-Bond rebound.

The Stock Market

Last week we wrote that in the

short-term the stock market would be helped by a pullback in market

interest rates, but that the upside would be limited because the monetary

backdrop was tight and likely to get tighter as the Fed ramped up the pace

of its balance-sheet reduction (its QT program).

Referring to an

article posted

HERE

and the Fed's portfolio

HERE, we also wrote that an immediate impact of the Fed's QT program

should be felt on the days when a large quantity of the Fed's holdings are

scheduled to mature. We pointed out that the last such date was 15th May,

when there was a sharp decline in the T-Bond and a 20-point decline in the

SPX, and that the next such date was 31st May.

With regard to the

SPX's performance a similar effect occurred on 31st May (there was a

20-point decline), but there was no noticeable adverse effect on the bond

market. Also, the 31st May decline was more than fully offset by the 1st

June advance, so it seems that if the Fed's balance-sheet reductions are

having an immediate and direct effect then the effect lasts only one day.

The next three big maturity dates for the Fed's bond holdings are 30th

June, 31st July and 15th August.

Turning to the recent price

action, a week ago we wrote:

"We won't be surprised if the NDX

tests its 2018 high during the first two trading days of this week, but we

will be surprised if it makes a solid break into new-high territory within

the next two weeks. Our guess is that more choppiness lies in store over

the coming fortnight."

The NDX didn't test its 2018 high last

week, but it has a good chance of doing so this week given that it broke

upward from a 3-week sideways consolidation last Friday.

Indications are that the US stock market will maintain an upward bias

for at least another month, but we suspect that downside volatility will

re-emerge during the third quarter.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday Jun-04 |

Factory Orders |

|

Tuesday Jun-05 |

ISM Non-Mfg Index |

|

Wednesday Jun-06 |

International Trade Balance |

|

Thursday Jun-07 |

Consumer Credit |

|

Friday Jun-08 |

No important events scheduled |

Gold and the Dollar

Gold

No Bull

Displayed below is a weekly

chart of the gold/SPX ratio. The blue line on the chart is the 200-week MA and

the rectangle drawn on the chart covers the period from the December-2015 low.

This is when the gold price made a multi-year low in US$ terms.

It's

possible that the December-2015 low will turn out to be the bear-market bottom

in nominal dollar terms, but whether or not gold is in a bull market isn't

determined solely by its performance in terms of fiat currency. It's also

determined by its performance relative to industrial commodities and financial

assets, with the S&P500 Index (SPX) being the best proxy for financial assets.

Gold's performance relative to the SPX makes it clear that a gold bull

market did not begin in December-2015. In SPX terms, the bearish trend that

began in 2011 appears to be intact.

A solid break by gold/SPX above its

200-week MA will provide confirmation of a major trend reversal. This is likely

to happen during the first year of the next cyclical gold bull.

At the moment we appear to be in the midst of either a long-term basing

pattern or a multi-year rebound within a bear market.

Current Market Situation

Despite some

wild action in the bond and currency markets, the gold market was quiet last

week. The price was down a few dollars over the course of the week.

With

regard to the recent performance of gold in US$ terms, what we have is a

downside breakout on 15th May followed by a rebound to 'test' the breakout. At

this stage the test has been successful, meaning that former support (now

resistance) has limited the rebound.

As previously advised, preliminary

evidence that gold has made a sustainable turn to the upside would be a daily

close above the 200-day MA while decisive evidence of such a turn would be a

weekly close above the 200-day MA. The 200-day MA now coincides with important

lateral resistance at $1309, so gold must achieve a weekly close above $1309 to

indicate that its short-term trend has changed from down to up.

The sentiment backdrop (as indicated by the COT data) remains slightly

supportive while the fundamental backdrop remains bearish. However, it likely

would take only a modest amount of additional strength in the T-Bond price to

shift the fundamental backdrop in gold's favour.

Silver

Apart from a 3-day period in April when there was a failed upside breakout

attempt, the silver price has now spent 4 months oscillating between $16.10 and

$16.90. This is remarkable stability for a market that tends to be volatile.

Sentiment remains neutral and as far as we can tell there is no basis for a

prediction about the direction of the coming breakout from the $16.10-$16.90

range. What we can say is that a downside breakout from the 4-month horizontal

range could establish a much more constructive sentiment backdrop and thus set

up a good buying opportunity.

Gold Stocks

The gold-mining indices and ETFs have been

in consolidation mode since early last year. As if that wasn't enough to lull

speculators to sleep, they have also been consolidating on a short-term basis.

Recently, volatility in the gold-mining sector has been about as low as it ever

gets.

For the XAU, there is some resistance at 84.5 but the first

important resistance is at 86. Going the other way, there is trend-line support

at 82 and then lateral support at 80.

We therefore view the short-term

consolidation range as 82-86. A daily close above 86 would suggest that the

index was on its way to at least 92 (near the top of the intermediate-term

consolidation range) and to possibly as high as 115 (the 2016 peak).

For

GDX, a "flag" pattern has developed over the past 6 weeks. This pattern suggests

resistance at $22.90 and support at $21.90 for the coming week. A breakout from

this range would be an early warning of the likely direction of a much larger

move.

We

suspect that a quick and sizable move in the gold-mining sector will begin this

month, but the price action is not yet providing clues about the direction of

the move. The gold-bearish fundamental backdrop suggests that the direction will

be down, but at this point it wouldn't take much to turn our gold model from

bearish to bullish. It's likely that a rise in the T-Bond price to around 146

(on a weekly closing basis) combined with a modest amount of weakness in the

stock market would do it. In any case, while a gold-bullish fundamental backdrop

is a prerequisite for a substantial multi-quarter upward trend, it isn't

essential for a 1-2 month surge.

Due to the high probability of a sizable

short-term move combined with the lack of clues regarding the likely direction

of the move, it would be reasonable for option traders to simultaneously buy

out-of-the-money calls and puts on a gold-mining ETF such as GDX. This was

discussed in last week's Interim Update. The subsequent two days of sideways

trading obviously haven't changed anything.

Investors with substantial

current exposure to the gold-mining sector already have the short-term rally

scenario covered and could consider doing some hedging in case the short-term

plunge scenario plays out. For example, they could buy some GDX September put

options or raise some cash.

The Currency Market

The Euro

The euro plunged last Tuesday

(29th May) due to the perception that it was facing another existential threat.

The threat emanated from Italy, where for a brief time it seemed like the

country would be forced back to the polls for an election that in effect would

be a referendum on remaining within Europe's monetary union.

The fear

that Italy could be on its way out of the monetary union caused Italian

government bonds to crash on Tuesday, driving bond yields sharply higher across

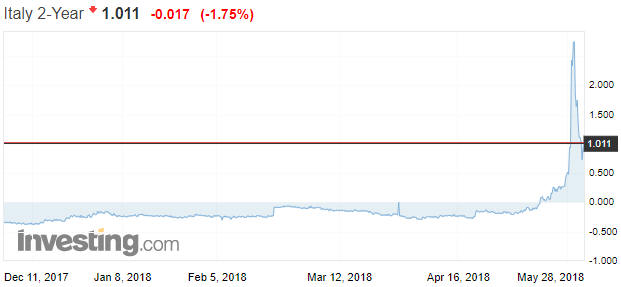

the curve. The most dramatic action occurred at the short end of the curve, with

the yield on the 2-year Italian government bond rocketing up from around 0.3% to

2.8% within the space of several hours.

The threat dissipated over the

rest of the week, though, as Italy's political situation appeared to stabilise.

This caused Italian government bond yields to plunge, although the 2-year yield

still ended the week well above where it began the week.

Here's a picture

showing last week's dramatic turn of events. Notice that Italy's 2-year

government bond yield was drifting along in NEGATIVE territory until mid-May.

From last week's Interim Update:

"If the euro closes below 1.156

on either Thursday or Friday of this week, and especially if it closes below

1.156 on both Thursday and Friday, the odds will shift in favour of the euro's

2017 rally being an intermediate-term upward trend within an on-going bear

market. Alternatively, if the euro manages to avoid a weekly and monthly close

below 1.156, as appears likely at this time, then the market action during the

first half of this week could turn out to be the climax of a multi-month

correction."

The euro broke below critical support on Tuesday but

then recovered to end both the month and the week comfortably it. Therefore, at

this stage it looks like Italy's political situation resulted in a euro selling

climax and a bottom that will hold for at least a few weeks.

The Australian Dollar (A$)

The A$

generated a bullish signal in the form of a false downside breakout in early

May, but it hasn't yet confirmed that a short-term bottom is in place. Such

confirmation will require a daily close above the 50-day MA (currently at 76.1)

and lateral resistance at 76.5.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 1st June 2018:

Company

news/developments for the week ending Friday 1st June 2018:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, MD&A = Management

Discussion and Analysis, M&I = Measured and Indicated, NAV = Net Asset Value,

NPV(X%) = Net Present Value using a discount rate of X%, NSR = Net Smelter

Return, P&P = Proven and Probable, PEA = Preliminary Economic Assessment, PFS =

Pre-Feasibility Study]

*Alio Gold (ALO) reported

the final set of results from the surface drill program at its Ana Paula gold

project in Guerrero, Mexico. The 3,800m program was initiated in January 2018

and consisted of six drill holes of 600 to 700 metres each targeting the complex

breccia extension below the proposed open-pit. Additionally, two 300m holes were

drilled into the near surface hydrothermal breccia to test its southern

extension.

Overall, these latest results were neutral at best. The

intercepts from the near-surface, low-grade hydrothermal breccia were positive,

but the intercepts from the below-pit, high-grade breccia were disappointing.

ALO has been performing poorly on the ground and in the stock market.

However, we expect that it will rebound strongly in response to a sector-wide

rally during the second half of this year, providing a much better opportunity

to exit.

*Almaden Minerals (AAU) reported the

assay results from holes drilled 1.2 kms from the PFS pit at its Ixtaca

gold-silver project. The results included an intercept averaging 0.83-g/t gold

over 89.5m and suggest the potential for significant resource expansion. This is

good news.

Our continuing interest in AAU is due to it being a very

under-valued junior gold miner that likely will attract a takeover bid after

completion of the Ixtaca FS late this year.

*Cobalt 27

Capital Corp. (KBLT.V) published its financial results for the

March-2018 quarter.

A week ago, we wrote: "At current metal prices and

taking into account the HIG [streaming] deal, our estimate of KBLT's net asset

value (NAV) is C$14.50-$15.00. Our estimated NAV will rise to C$17.00-C$17.50 if

the deal with the two local Ramu stakeholders is completed as mentioned above."

Based on the balance sheet included with the latest quarterly financial

results, KBLT's NAV prior to the HIG streaming deal was C$10.70/share. Adding

the value that we estimate is contributed by the streaming deal takes the NAV to

C$14.50/share, so our earlier calculation was close to the mark.

A stock

such as this would normally trade at a 10%-30% premium to NAV, but KBLT is

presently trading at a 15% discount. This most likely reflects market concerns

about the reliability of the cash flow that the streaming deal will generate.

*Energold Drilling (EGD.V) published its financial

results for the March-2018 quarter.

Revenue for the quarter was about

C$24M, which constitutes a 26% improvement on a year-over-year basis. It was the

highest quarterly revenue in 4 years, indicating that the improvement in EGD's

business that began during the March quarter of 2017 continues.

EGD's

top-line improvement hasn't yet resulted in bottom-line profitability, in that

the company reported a net loss of C$1.9M for the quarter. Importantly, however,

about C$6M was added to the balance sheet, with working capital rising from

C$51.5M to C$57.5M while long-term debt remained the same.

Near its

current low price of C$0.38/share, EGD is a relatively low-risk way to obtain

leveraged exposure to the prices of metals and oil.

*Golden

Arrow Resources (GRG.V) published its financial report for the

March-2018 quarter. The report shows working capital of C$12.9M at 31st March,

down by C$3.4M since the end of the preceding quarter.

GRG's financial

position remains strong for a company of its size, but it will have to raise

additional money within the coming 6 months to fund its share of the capex for

the Chinchillas silver mine in Argentina. We previously thought it would have to

raise about C$10M, but the amount required may be closer to C$15M.

The

Pirquitas-Chinchillas project is owned 25% by GRG and 75% by SSR Mining. It is

expected to have average annual production of 6.1 million ounces of silver, 35

million pounds of lead and 12.3 million pounds of zinc.

List

of candidates for new buying

From within the ranks of TSI stock

selections the best candidates for new buying at this time, listed in

alphabetical order, are:

1) ALK.AX (last Friday's closing price: A$0.28)

2) CLQ.AX or CLQ.TO (last Friday's closing price: A$1.03)

3) EGD.V

(last Friday's closing price: C$0.38)

4) PG.TO (last Friday's closing

price: C$2.70)

5) PRQ.TO (last Friday's closing price: C$1.22)

The

above list is limited to five stocks. It will sometimes contain less than five,

but it will never contain more than five regardless of how many stocks are

attractively priced for new buying.

EV&V

Stocks Table

"EV&V" stands for Electric Vehicle and Vanadium,

and "EV&V Stocks" are stocks that provide exposure to the commodities that will,

we think, experience a substantial increase in demand due to the proliferation

of electric vehicles or growth in the use of Vanadium Redox Batteries (VRBs).

One way or another we are currently covering nine such stocks.

For ease

of reference, here is a table of the EV&V stocks that we are covering in some

way (this is an update of the table that was originally included in the 7th

March 2018 Interim Update). In the table we have noted the specific EV&V-related

commodity exposure provided by each stock and whether the stock is a member of

the TSI Stocks List or the

Small

Stocks Watch List (SSWL). To give an indication of company size, we have

also noted the current market cap.

Two of the SSWL stocks included in the above table had important news within

the past three weeks.

First, Arafura Resources (AUR.AX)

reported on 14th May that it had received environmental approval from the

Australian Government for its 100%-owned Nolans Neodymium-Praseodymium (NdPr)

project in the Northern Territory. This was the final step in the project's

environmental approval process.

Completion of the Nolans project FS is

the next major milestone for ARU. This is scheduled for December-2018.

Note that NdPr is used to make the permanent magnets that go into EV motors.

Regardless of how battery technology evolves, NdPr should remain an essential EV

material.

Second, Prophecy Development Corp. (PCY.TO)

published the results of a PEA for its Gibellini vanadium project in Nevada. The

plan is to develop Gibellini into an open-pit, heap leach mine.

The

Gibellini deposit is low grade (the average vanadium pentoxide (V2O5) grade of

the estimated resource is less than 0.30%) and the average metallurgical

recovery is low at around 60%, but on the plus side the strip (waste/ore) ratio

is very low at 0.17 and the mine plan is straightforward.

According to

the PEA, at anywhere near the current V2O5 price it would be possible to develop

Gibellini into a very profitable mine that paid back its US$116M initial capex

in quick time. For example, at $12.73/pound for V2O5 (about 10% below the

current market price) it is estimated that the Gibellini mine would have a

post-tax NPV(7%) of US$338M, a post-tax IRR of about 51% and a payback period of

1.7 years.

The above NPV compares very favourably with PCY's current

sub-US$20M market cap.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.investing.com/

http://www.barchart.com/