--

Weekly Market Update for the Week Commencing

4th November 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

|

Market |

True Fundamentals Model (TFM) |

|

Gold (US$ Price) |

Bullish (04 Oct 2019) |

|

US Equity (SPX) |

Bearish (04 Oct 2019) |

|

Currency (Dollar Index) |

Neutral (15 Mar 2019) |

|

Commodities (GNX) |

Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

There were no blog posts last week.

Summary of current

thinking/positioning

1) The Dollar Index (DX)

confirmed a short-term reversal to the downside four weeks ago, but must

end a week below 96 to confirm an intermediate-term reversal to the

downside. We are anticipating such a reversal, but we are uncertain as to

whether it will happen in the near future or during the first half of next

year.

2) The US$ gold price, the US$ silver price and the

gold-mining indices appear to have ended their corrections and embarked on

short-term upward trends that probably will result in new multi-year highs

within the next three months.

3) The Fed's new asset monetisation

program has increased the risk for bearish stock-market speculators and

clear signs of equity strength have started to emerge outside the US.

However, the senior US stock indices probably will reach short-term tops

during the first half of November.

4) There is a realistic chance

that the T-Bond will trade below its September low before bottoming on a

short-term basis, but we expect that major price weakness (yield strength)

in the Treasury market will be postponed until next year.

5)

Industrial commodities such as oil and copper could be in the process of

bottoming, but we expect that meaningful price strength won't show up

until next year.

6) We are holding a cash reserve of 25%-30%.

The Monthly

Closing Prices

At around this time every month

we review some of the most important (from our perspective) monthly

charts. We do this because monthly closing prices can confirm or deny

intermediate-term trend changes. For October-2019 we'll review the monthly

closes for gold, the Gold Miners ETF (GDX) and the S&P500 Index (SPX).

Regarding gold, this is part of what we wrote a month ago:

"...critical

monthly-closing support for gold's intermediate-term upward trend is

defined by the 8-month MA. That is, a monthly close below the 8-month MA

would confirm that an intermediate-term top (a top that holds 6-12 months)

is in place. This MA is now at $1383 and should rise to about $1400 by the

end of this month.

At this time we do NOT expect a monthly close

below the 8-month MA."

The following monthly chart shows that

the US$ gold price didn't come anywhere near its 8-month MA during October

and that at the end of the month this MA was at $1408. The MA is

continuing to rise, should reach $1450 by the end of November and should

not be breached on a monthly closing basis anytime soon.

Monthly

resistance lies at $1570. A monthly close above this resistance would

point to an upcoming test of the 2011 major peak, but let's not get ahead

of ourselves.

Shorter-term charts suggest that gold has completed

a 1-2 month correction. If so, a rally lasting at least three months has

begun and this rally should at least result in an intra-month spike above

$1570.

GDX tested its 2016 high at the beginning of September and then

reversed downward. As is the case with gold, it appears to have completed

a 1-2 month correction.

Monthly-closing support for GDX's

intermediate-term upward trend is now defined by the October-2019 low of

$26.18. However, there should be warnings in daily and weekly charts that

the intermediate-term upward trend is over well before such a reversal is

signaled by the monthly chart.

At this stage it's reasonable to

expect that GDX will trade above its 2016 high before topping on an

intermediate-term basis.

The SPX's price action during the period since September-2018 still

looks similar to the price action that followed the intermediate-term top

in 2011. The similar periods are indicated by the red boxes drawn on the

following monthly chart.

For the similarity to be maintained, the

12-month MA should not be breached on a monthly closing basis for a long

time to come. Although this not what we expect, we are not prepared to

rule out this possibility.

A monthly close below the 12-month MA

would be the first clear sign on the monthly chart that the bull market is

over.

US Recession

Watch

Our favourite leading indicators

of US recession are the ISM New Orders Index (NOI), Real Gross Private

Domestic Investment (RGPDI) and the yield curve.

Two months ago the

NOI became the first of the above-mentioned leading indicators to issue a

recession warning, meaning that the monthly NOI for August-2019 was below

the red demarcation line drawn on the following chart. The NOI remained

below the demarcation line in September.

The results of the latest

monthly ISM survey were published last Friday and revealed that in

October-2019 the NOI rebounded to slightly above the recession warning

level. However, this does not negate the earlier warning. It would take a

move to well above 50 to negate the warning.

There have been ten US

recessions since the early-1950s and for eight of these the time from the

NOI warning to the recession start was five months or less. The

August-2019 NOI signal therefore could be construed as a warning that a

recession will begin by January-2020. However, the NOI occasionally

generates a false signal. If the current NOI recession warning is valid

then it should be confirmed by our other favourite leading recession

indicators and also by an extension of its own downward trend within the

next few months, whereas if it is invalid it should be cancelled within

the next few months via a move to well above 50.

Note that over the

past 20 years there was only one false NOI recession signal. This was the

dip below the red line in March-April of 2003.

The latest quarterly RGPDI number (for Q3-2019) was published last

week. As illustrated below, RGPDI made a new all-time high in Q1 of this

year and turned down in Q2. The Q3 number was slightly below the Q2

number, thus increasing the probability that a trend reversal has

occurred.

A trend reversal in RGPDI from a Q1-2019 high would be

consistent with a recession getting underway in the final quarter of 2019

or the first half of 2020.

Note that the vertical red lines on the

following chart mark the starts of the last two official US recessions.

Finally there is the yield curve, which generates a recession warning

when it 'flattens' to an extreme (usually but not necessarily involving an

inversion) and then begins to steepen. A yield-curve reversal from

flattening to steepening was signaled last month (October-2019).

Consequently, all three of our favourite leading recession indicators have

now issued recession warnings. There is still some uncertainty, however,

because each of the warning signals is marginal at this time.

Based on the latest data, our rough estimates of recession start-time

probabilities are:

- Q4-2019: 30% (down from 35% a month

ago)

- H1-2020: 40% (not stated a month ago*)

-

H2-2020: 25% (not stated a month ago*)

- Later than 2020: 5%

(unchanged from a month ago).

Note that even if the US economy

doesn't slide into recession anytime soon, the weakness over the past

several months in the ISM NOI suggests that coincident indicators such as

industrial production will continue to deteriorate over the next few

months.

Also note that although the US economy has not been

officially in recession at any time over the past two years, the entire

period since H1-2018 could be viewed as an economic downturn. There has

been no growth in overall corporate profitability during this period, many

stock indices remain below their H1-2018 highs, and industrial production

has been declining since Q4-2018. This actually could be a positive as far

as the future is concerned, because it could mean that a downturn is in

its late stages rather than its early stages.

Finally, we can't

rule out the possibility that the Fed's attempts to extend the current

economic cycle will work. The reason is that unlike 2000 and 2007, this

time around the Fed has begun to pump money aggressively with the senior

stock indices at/near all-time highs. Due to the Fed's actions, this could

be more like 1998 or 2012 than 2001 or 2007.

*Last

month we indicated a 60% probability of a recession start sometime in

2020.

The Stock Market

During the week before last the

SPX broke above the top of its contracting triangle pattern. Last week it

went a step further by breaking into new all-time high territory.

Moreover, the upside breakout was confirmed by additional gains in the

NYSE Advance-Decline Line (ADL).

It isn't hard to find US stock indices that are yet to exceed last

year's highs. However, recently some of the lagging indices have shown

signs of strength. For example, although the NYSE Composite Index (NYA)

remains well below its January-2018 all-time high, last week it broke

above intermediate-term resistance defined by its September-2018 and

July-2019 highs.

Be aware, though, that last week's breakouts don't imply that

significant additional gains are in store. Instead, we explain below that

the market has reached a critical juncture that COULD lead to upward

acceleration over the coming several weeks, but more likely will lead to a

sell-off.

A week ago we wrote: "The [Fed's] new program has the

potential to extend the long-term equity bull market well into next year,

but there are two reasons, one technical and the other fundamental, to

believe that the market won't make much additional headway before

commencing its next significant correction.

The technical reason is

illustrated by the following weekly chart. The chart shows that over the

past 18 months the SPX has commenced a sizable multi-week decline soon

after making a new all-time high. If the pattern continues, the SPX won't

go higher than about 3070 before reversing course."

An updated

version of the same weekly chart is displayed below. Notice that last

week's gain took the SPX to the top of its 2-year broadening range.

Many traders will be drawing similar lines to the ones drawn on the

above chart. This means that there could be an immediate increase in

selling pressure and a downward reversal this week. It also opens up the

possibility that a solid break above the upward-sloping line on the chart

will lead to acceleration to the upside over the ensuing few weeks as a

large number of wrong-footed traders rush for the exit or shift from short

to long.

The most likely catalyst for the more bullish short-term

scenario is the signing of a US-China trade deal, but the Fed's money

pumping has been the root cause of the upward move of the past month and

would be the root cause of any meaningful price gains that happen within

the next few months.

At this stage we favour the more bearish

short-term possibility, which means that we expect a 1-3 month 'risk off'

trend to begin within the next couple of weeks without the SPX making

significant additional headway. As well as putting irresistible downward

pressure on the broad stock market, this trend probably would boost the

prices of gold, gold-mining stocks, T-Bonds and the Yen.

However,

although we have positions that will benefit from it, we aren't betting

heavily on the short-term 'risk off' scenario. In effect we are hedging

our bets, because the upward breakout scenario would boost the values of

our industrial-commodity-related equity positions.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday Nov-04 |

Factory Orders |

|

Tuesday Nov-05 |

International Trade Balance

ISM Non-Mfg Index |

|

Wednesday Nov-06 |

No important events scheduled |

|

Thursday Nov-07 |

Consumer Credit |

|

Friday Nov-08 |

Consumer Sentiment Index |

Gold and the Dollar

Gold and Gold Stocks

We are combining our Gold and Gold Stocks discussions today because they are

more inter-related than usual.

In the email sent to subscribers after the

close of US trading last Thursday, we wrote that Thursday's market action had

generated some persuasive evidence that the corrections in gold and gold mining

are over. Of particular significance:

1) The US$ gold price closed above

its short-term channel top and its 50-day MA.

This is illustrated below.

There was a small pullback on Friday that held the 50-day MA.

2)

Gold's upside breakout was confirmed by strength in the Yen (the major currency

that is most strongly correlated with gold).

The following chart

illustrates the strong positive correlation between the US$ gold price and the

Yen. The Yen had led gold at turning points since late last year, but it appears

that gold was the leader at the most recent turn. As shown more clearly in the

chart included in the Currency Market section of today's report, the Yen is yet

to confirm that a short-term bottom is in place; however, the Yen's 30th-31st

October turnaround from below the 200-day MA looks like the first step in a

trend reversal.

3) The HUI, GDX and GDXJ closed above their 50-day MAs.

The following

daily chart of the HUI shows Thursday's break above the 50-day MA and a trivial

pullback on Friday. GDX has been a little weaker than the HUI of late and ended

Friday's session exactly at its 50-day MA.

4)

The HUI/gold ratio continued to perform in a bullish manner.

As

illustrated below, the HUI/gold ratio bounced off its 150-day MA in the middle

of October and broke above its 40-day MA during the week before last. At this

point there was nothing to differentiate the rebound from a counter-trend move,

but the ratio then pulled back to its 40-day MA before rising to a new

multi-week high. As a result, the rebound from the mid-October low now looks

more like the start of an upward trend than a reaction within a downward trend.

We mentioned in the email that if the corrections have ended then they have

done so within the expected time-window, but at higher price levels than

originally expected. With regard to the HUI and GDX, we had expected that

200-day MA's would be tested before the correction was over. This would have

entailed the HUI dropping to the low-180s before resuming its intermediate-term

advance. With regard to gold bullion, we had expected that the price would fall

at least as far as support at $1450 and were prepared for a decline to as low as

the mid-$1300s.

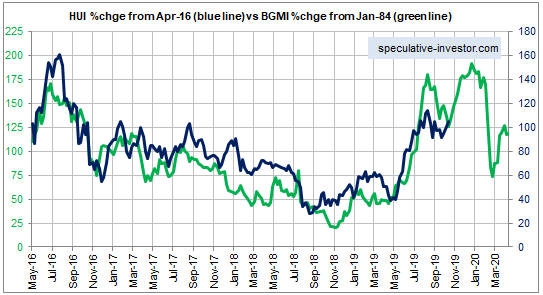

We also mentioned in the email that the recent upward

reversal in the gold-mining sector is roughly in line with the 1980s Model we've

been tracking. As illustrated below, this model suggests that the gold-mining

indices/ETFs will trend higher over the next three months.

By the way,

the spectacular plunge in the green line on the following chart is the 1987

stock market crash. In October of 1987 the gold mining sector crashed with the

stock market while the gold price rose, thus highlighting a major difference

between gold-mining stocks and gold bullion. The latter is a safe haven in times

of extreme turmoil/trouble, the former is not.

Unless the broad US stock

market starts to form a crash pattern before year-end, the current market should

start to diverge from the 1980s path early next year.

Something we've been harping on is that there has not been a proper

sentiment reset in the gold market. In fact, due to a surge in open interest

last Thursday it's possible that the total speculative net-long position in

Comex gold futures has returned to the vicinity of its September-2019 all-time

high. The lack of a sentiment reset means that the short-term risk is higher

than we would prefer, even though a rally to new multi-year price highs appears

to be underway.

The most reasonable assumption is that rallies to new

multi-year price highs have begun in both the bullion market (silver and

platinum as well as gold) and the associated mining indices/ETFs. If so, it's

likely that downward corrections will be limited by 20-day MAs. Therefore,

pullbacks to near 20-day MAs by the US$ gold price, the HUI and/or GDX should be

viewed as short-term buying opportunities.

The Currency Market

The Dollar Index (DX) ended last week slightly below its 200-day MA. This is

a downside breakout of sorts, but more important support is defined by the

channel bottom and lies about one point lower. Another test of the channel

bottom appears to be in store and could occur as soon as this week.

To

get a sustained break below the channel bottom the dollar's "true fundamentals"

will have to turn bearish. This will require additional strength in European

equities relative to US equities.

Our view at this time is that a 1-2

year period of US$ weakness either has begun already or will begin within the

next few months.

We

have been getting increasingly bullish about the Yen's short-term and

intermediate-term prospects, but prior to the past three trading days there was

no evidence that the currency had completed its downward correction. Preliminary

evidence that a short-term bottom is in place emerged during the second half of

last week.

The following daily chart shows that:

a) The Yen spiked

below its 200-day MA and an important lateral support level last Wednesday, but

recovered to end the day above support.

b) After recovering from below

support on Wednesday, the Yen gapped higher on Thursday.

c) There was a

pullback on Friday that left the bulk of Thursday's gain in place.

This

price action could have marked a trend reversal, but even if it didn't we expect

that a multi-month bottom will be put in place within the next two weeks due to

a downward reversal in the stock market and an associated shift away from risk.

As explained in last week's Interim Update, although the Yen is not a safe haven

it often trades like one because Yen carry trades tend to get closed en-masse

when economic and/or financial-market risk is perceived to be on the rise.

It would be reasonable to buy CurrencyShares Japanese Yen (FXY), a daily

chart of which is displayed below, for a short-term or an intermediate-term

trade with the Yen in the 92.0-92.5 range. To manage risk, an initial stop could

be placed slightly below last week's low.

As noted later in today's

report, our short-term bullish outlook for the Yen will be reflected in the TSI

List via an FXY call option.

The

Australian dollar (A$) has moved up to slightly below its 200-day MA. This is

interesting, because the following chart shows that every significant rebound in

the A$ since March of last year has ended at or slightly below the 200-day MA.

This means that for the A$ it's time to fish or cut bait. Will the current

rebound be the one that morphs into an intermediate-term upward trend, or are we

about to get another rally failure at/near the 200-day MA?

We

are neutral with regard to the A$'s short-term prospects and bullish with regard

to the A$'s 1-2 year prospects.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 1st November 2019:

Company

news/developments for the week ending Friday 1st November 2019:

[Note: AISC = All-In Sustaining Cost, EBITDA = Earnings Before Interest, Tax,

Depreciation and Amortisation (a measure of cash flow), EV = Enterprise Value or

Electric Vehicle, FS = Feasibility Study, FY = Financial Year, IRR = Internal

Rate of Return, ISR = In-Situ Recovery, JV = Joint Venture, MD&A = Management

Discussion and Analysis, M&I = Measured and Indicated, NAV = Net Asset Value,

NPV(X%) = Net Present Value using a discount rate of X%, NSR = Net Smelter

Return or Net Smelter Royalty, P&P = Proven and Probable, PEA = Preliminary

Economic Assessment, PFS = Pre-Feasibility Study]

*Africa

Oil (AOI.TO): At around this time last year AOI announced that it owned

25% of a consortium that had agreed to buy 50% of Petrobras Oil and Gas B.V.

(POGBV) for US$1.407B. This was a huge deal for AOI at the time, but the deal

has just become much bigger. Four times bigger, to be specific. The reason is

that prior to the start of trading last Friday AOI announced that its consortium

partners have pulled out and that AOI will be the sole acquirer of the 50%

interest in POGBV for US$1.407B.

POGBV owns 8% and 16% interests in

offshore Nigerian oil fields operated by Chevron and Total. At the time of the

original deal the combined production of these fields was 368K barrels/day (b/d)

and expected production within 12 months was 568K b/d, so we assume -- given

that there has been no new information -- that the production rate is now about

568K b/d.

POGBV's share of this production was 47K b/d in 2017 and should

now be about 79K b/d. Given that AOI will own 50% of POGBV, this implies that

AOI will have production of about 40K b/d after the deal is completed. The

reported production cost 12 months ago was only $10/barrel, so this should be

very profitable production at the current oil price.

At an oil price of

US$55/barrel, 40K b/d of oil production results in annual revenue of around

US$770M. And based on the reported production cost, this could result in a gross

margin of at least US$400M. That's massive for a company with a current market

cap of only US$415M.

The biggest question right now is: How will AOI

finance the purchase?

The company has about US$300M of cash and has just

arranged a US$250M bridge loan facility with BTG Pactual (the owner of the other

50% of POGBV). According to AOI's press release, "the bridge loan together

with the available cash provide the necessary funds for the company to cover its

POGBV deal completion payments and 2020 budget." This suggests to us that

the purchase involves staged payments.

We are surprised that there was

minimal reaction in the stock market to AOI's news. Trading volume was higher

than average on Friday, but the price was unchanged. In our opinion the news is

very positive and justifies an upward re-rating of the stock.

*Jervois

Mining (JRV.AX, JRV.V), an exploration/development-stage miner that

offers exposure to cobalt and nickel, issued its quarterly report for the

September-2019 quarter. The report contained no new information of significance.

JRV is well financed, with no debt and about A$17M of cash following the

recent receipt of A$3M for the sale of a gold royalty. We expect that the next

major milestones for the company will be the completion of the updated FS for

the Idaho Cobalt Operation (ICO) and the completion of a scoping study regarding

the construction of a refinery at the ICO. These are both due in Q1-2020. In the

meantime there will be drilling results from the ICO and the company's

early-stage exploration prospects in Uganda.

*Mineral

Resources (MIN.AX) announced that the "Albemarle transaction" has

overcome its final regulatory hurdle (approval from Australia's Foreign

Investment Review Board) and is now complete. The transaction involves the sale

to Albemarle Corporation (NYSE: ALB) of 60% of the Wodgina Lithium Project

(leaving MIN with 40%) in exchange for US$820M (A$1,188M at the current exchange

rate) in cash plus the transfer to MIN of a 40% interest in the first two 25,000

dry-tonnes-per-annum lithium hydroxide conversion units currently being built by

Albemarle in Kemerton, Western Australia. Regarding the Kemerton units MIN is

free-carried to production, which is expected in 2021.

This is very good

news.

MIN subsequently announced that the MIN-ALB JV had placed the

Wodgina project on care and maintenance pending a recovery in the lithium price.

This does not affect MIN's 2020 financial guidance.

The lithium market

became over-supplied during 2017-2018 as miners aggressively increased

production in reaction to a large price rise during 2016-2017, leading to a

major downward trend in the price during 2018-2019. The price is still being

weighed down by excess supply and there is no turnaround in sight, but we expect

that increasing demand from the Electric Vehicle industry will cause the

supply-demand situation to become price-supportive within 12 months.

MIN

is positioned to benefit in a big way from an eventual recovery in the lithium

market, but thanks to its mining services and iron-ore businesses it doesn't

need a higher lithium price to be profitable. Consequently, we continue to

believe that MIN is the safest way to obtain long-term exposure to lithium.

Our intermediate-term valuation-based target is A$20/share, which is about

40% above the current price.

*Premier Gold (PG.TO)

reported two pieces of good news related to the South Arturo gold project in

Nevada. This project is a JV between PG (40%) and Nevada Gold Mines (the

Barrick-Newmont JV). The PG-NGM JV has been developing two new mines at South

Arturo -- the El Nino underground mine and the Phase 1 open pit.

The

first piece of good news is that El Nino has achieved commercial production on

budget and well ahead of schedule. Consequently, this mine will contribute

significantly more than planned to PG's 2019 gold production. The Phase 1 pit

remains on track for production next year.

The second piece of good news

is that drilling at El Nino and at the Phase 3 pit (a future development)

returned exceptional intercepts, including 24.4 m of 20.60 g/t Au, 50.3 m of

6.36 g/t Au, 39.6 m of 8.75 g/t and 32.0 m of 10.09 g/t Au at El Nino, and 112.8

m of 7.29 g/t Au and 62.5 m of 7.93 g/t Au at Phase 3. These results indicate

the potential for very high-margin gold production.

Separately, PG

reported 14.5K ounces of gold production during the September quarter from its

Mercedes mine in Mexico. This was a disappointing below-plan result as the mine

continues to struggle with lower-than-expected grades.

Due to having

several 'irons in the fire', including current production from two mines, PG is

a relatively low-risk stock to average into for exposure to gold.

List

of candidates for new buying

From within the ranks of TSI stock

selections the best candidates for new buying at this time, listed in

alphabetical order, are:

1) AOI (last Friday's closing price: C$1.16)

2) JRV.AX, JRV.V (last Friday's closing price: A$0.20, C$0.19)

3) OIH

(last Friday's closing price: US$11.71)

4) PG.TO on a pullback to the

low-C$2 area (last Friday's closing price: C$2.22)

5) SBB.TO on a

pullback to the mid-C$1.60s (last Friday's closing price: C$1.76)

The

above list is limited to five stocks. It sometimes will contain less than five,

but it never will contain more than five regardless of how many stocks are

attractively priced for new buying.

Option

Trades

1) GDX 15-November-2019 $27.00

Put Option

The above put option was added to the TSI List on 24th

September in anticipation of a correction-ending plunge to the 200-day MA. The

potential for such an outcome has not been totally eliminated, but it very much

looks like the gold-sector correction is over and a new multi-month upward trend

has kicked off. Therefore, although for hedging purposes it could make sense to

retain this position for at least a few more days, the put option is no longer a

valid speculation and has been removed from the TSI List. It will go into the

record books as a loss of about 64% and will thus cut into the 428% profit

achieved on the GDX put option exited in September.

2)

FXY (CurrencyShares Yen) January-2020 $90.00 Call

Option

Further to the comment earlier in today's report, our

short-term bullish outlook for the Yen will be reflected in the TSI List via the

addition of the above FXY call option. The last trade for this option was

US$0.40 and it ended last Friday's session with a bid-ask spread of $0.35-$0.45,

so we will use $0.40 as our starting price for record purposes.

This is a

risk-off play, not an anti-US$ play.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/