![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 5th February 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bearish (12 Jan 2018) |

| US Equity (SPX) | Neutral (12 Jan 2018) |

| Currency (Dollar Index) | Bullish (15 Dec 2017) |

| Commodities (GNX) | Bullish (29 Dec 2017) |

Last week's posts at the TSI Blog

What everyone is missing about the US tax cuts

Summary of current

thinking/positioning

1) Thinking that the US$ gold

price will trend downward over the next several weeks but will go on to

make new highs for the year during the second quarter.

2) Still not

expecting anything more bearish than a normal (5%-10%) correction in the

US stock market, but recognising that short-term stock market risk will

ramp up if bond yields continue to rise.

3) Thinking that

industrial commodities such as oil and copper will make short-term price

highs during the first two months of 2018.

4) Expecting the Dollar

Index (DX) to rebound over the next few weeks.

5) Thinking that the

T-Bond will build on last week's downside breakout over the next few

months.

6) Holding a cash reserve of 25%-30% and looking for

opportunities to increase it.

T-Bond Breakdown

By far the most important

financial-market development over the past week was the downside breakout

in the 30-year T-Bond price illustrated by the following weekly chart. The

breakout was expected, although we thought it might wait until the second

quarter.

The T-Bond's weekly close below support at 146-147 completes a

multi-year topping pattern and projects more downside over the next few

months. There probably won't be a major T-Bond decline this year, but

there's a good chance of the T-Bond trading at least 10% below its current

price before reaching an intermediate-term bottom.

Last week's

downside breakout by the T-Bond price has far-reaching implications

because it is further evidence that the generational decline in interest

rates ended in 2016. That being said, the waters have been muddied by the

fact that the downside breakout in the T-Bond price has not been confirmed

by an upside breakout in the T-Bond yield (the 30-year interest rate). A

lot of market participants care more about the bond yield than the bond

price, and the following weekly chart shows that the bond yield has not

yet broken out to a new multi-year extreme.

We are confident that a confirming upside breakout in the bond yield

is coming, if not in the next three weeks then in the next three months.

US Recession

Watch

The previous edition of our

monthly "US Recession Watch" feature was in the 3rd January Interim

Update. At that time we concluded:

"Taking into account the NOI

[New Orders Index] surge (bullish), the fact that the yield curve is still

in a flattening trend (bullish) and the decline in the monetary inflation

rate (bearish), we think that:

a) The probability that a US

recession will start in Q1-2018 is 0%.

b) The probability that a US

recession will start in Q2-2018 is 10%.

c) The probability that a

US recession will start in Q3-2018 is 30%.

d) The probability that

a US recession will start in Q4-2018 is 50%."

Considering

subsequent data, the probabilities haven't changed. In particular, the

latest iteration of the quarterly Real Gross Private Domestic Investment

(RGPDI) number was a new all-time high. Refer to the first of the

following charts for details. RGPDI tends to reverse downward at least 2

quarters prior to the start of a recession, so the fact that it made a new

high in Q4-2017 points to H2-2018 as the earliest time for the start of

the next recession. Secondly, although the latest iteration of the monthly

ISM Manufacturing New Orders Index (NOI), which was reported on Thursday

1st February, was lower than the 13-year high achieved in the preceding

month, it was still near the top of its long-term range. Refer to the

second of the following charts for details. Thirdly, the yield curve is

not yet close to signaling a reversal from flattening to steepening. There

is little chance that a recession will begin prior to such a signal.

There is almost no chance of a recession beginning during the first

half of this year, but there's a high risk of a recession getting underway

before year-end. The reason is the slow rate of US monetary inflation.

It's likely that at some point within the next 12 months the 'bubble

ventures' that were incentivised by the rapid monetary inflation of

2009-2016 will begin to collapse.

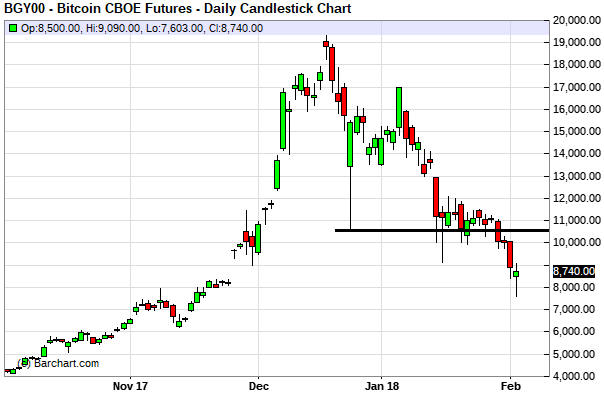

Cryptomania

Update

Our most recent "Cryptomania

Update" was in the 22nd January Weekly Update, at which time we wrote:

"There's a good chance that within the next few weeks the Bitcoin

price will close below its 22nd December low, removing most of the

remaining doubt that the price top on 18th December (the day that futures

trading commenced on the CME and a week after futures trading commenced on

the CBOE) was the ultimate top. It just hasn't happened yet."

Last week the Bitcoin price closed below its 22nd December low. Therefore,

there is little remaining doubt that the price top on 18th December was

the ultimate top.

It's testament to the rapidity of last year's rally that the 60%

plunge of the past 6 weeks has done no more than take the price back to

where it was in November-2017. This means that every current holder of

Bitcoin who bought before November-2017 still has a substantial profit,

albeit nowhere near as substantial as it was several weeks ago.

Although the Bitcoin bubble has burst, the 'cryptocurrency' concept is not

going to die. Also, distributed ledger technology, the first successful

attempt at which is the "blockchain" developed for Bitcoin, looks set to

become extremely important in many industries over the years ahead.

The Stock Market

Mind-Boggling Valuation

We thought we understood the extent of the US stock market's

over-valuation, but we were wrong. The valuation-related information

contained in the article posted

HERE, which was sent to us by a friend, blew us away. The market

appears to be much more expensive than we thought.

The above-linked

article focuses on the combined valuation of four blue chip stocks:

McDonald's, Caterpillar, Boeing and 3M. Between 1997 and the end of 2015,

the price/revenue ratio of an index comprising these four stocks (MCBM)

oscillated between 1.5 and 2.5. Then, in 2016 the index broke out of this

range and now trades at almost twice the HIGHEST valuation of the

1997-2015 period.

Moreover, today's extraordinarily high valuation

for MCBM can't be explained by investors extrapolating unusually-fast

revenue growth. This is because the average 5-year revenue growth of MCBM

is at a 20-year low!

The following chart from the article

illustrates what we've described above. Notice the spectacular rise in

valuation (the blue line) in parallel with declining revenue growth (the

red line) over the past two years.

'Investors' are prepared to pay such high prices for the shares of

these large and relatively staid companies because in most cases they

aren't buying the shares directly. Instead, they are buying ETFs that hold

these shares and paying no attention to the valuations of the individual

stocks in the ETFs. As pointed out in the article, there are 32 ETFs that

count McDonald's among their top 15 holdings, 25 ETFs that count

Caterpillar among their top 15 holdings, 83 ETFs that overweight Boeing to

this degree and 44 ETFs that overweight 3M.

This is passive

investing run amuck. The stage is now set for conservative investors to

lose as much as aggressive investors, because ETFs that hold

supposedly-safe, blue-chip stocks are going to collapse in price during

the next bear market.

Marijuana Stocks Update

When we wrote about the enthusiasm for marijuana stocks in the 8th

January Weekly Update, the Horizons Marijuana ETF (HMLSF) had just pulled

back in reaction to a decision by US Attorney General Jeff Sessions to

rescind the "Cole Memo", leading to some concern that there would be a

federal crackdown on marijuana sales and consumption. However, the

pullback was minor and the ETF was still trading near its high. Here's how

we summed up the situation:

"[Speculation in marijuana-related

equities]...is yet another stock-market bubble. Marijuana production is

essentially a low-margin commodity business deserving of a relatively low

valuation, but most marijuana-related stocks now have extremely high

valuations. Therefore, buying these stocks should not be called investing;

it should be called betting on future sentiment. As long as the industry

continues to grow rapidly and market participants fixate on this growth

while ignoring the realistic earnings potential of the companies involved,

the bull market could continue.

Although the downward price-spike

prompted by Jeff Sessions' burst of idiocy was largely retraced on Friday,

there's a high risk that the marijuana sector will soon commence a

substantial correction. This is partly because the sector has just

experienced what appears to be an upside blow-off and partly because the

speculation in this sector would be interrupted by weakness in the broad

stock market.

A substantial correction may create a new speculative

buying opportunity."

As illustrated by the following daily

chart of HMLSF, a substantial correction has since begun. In our opinion,

it's too soon to view the price decline as a buying opportunity.

Current Market Situation

The S&P500 Index

(SPX) has fallen by 4% from the all-time high it hit during the week

before last. A 4% decline isn't much and at this stage the index hasn't

even dropped far enough to reach its 50-day MA, so there hasn't been a

significant correction yet. However, the recent decline feels significant

because it has been well over a year since the SPX experienced a

run-of-the-mill 5% pullback from an all-time high. In other words, the

extraordinary lack of volatility over the past 12-18 months makes the

recent up-tick in volatility seem more meaningful than it is.

We continue to expect that there will be a 5%-10% correction during

the first quarter of the year followed by a move to new highs. This would

be consistent with the momentum extremes that were reached over the past

few weeks. It would also be consistent with the sentiment backdrop, which

is already becoming constructive thanks to our put/call indicator

generating a buy signal (the first buy signal since January of last year)

at the end of last week, and with the neutral fundamental backdrop.

However, last week's downside breakout in the bond market has increased

the risk that something more bearish than a 5%-10% correction will occur

in the stock market within the next couple of months.

There will be

a further increase in the stock market's short-term risk if the downside

breakout in the T-Bond price is confirmed by an upside breakout in the

T-Bond yield. In fact, if the T-Bond yield breaks above 3.20% and

continues to surge then the probability of something resembling a stock

market crash will become uncomfortably -- or comfortably, depending on

your perspective -- high.

Almost regardless of what's in store over

the next two months, a multi-week bottom probably will be put in place

this week. There should then be a rebound that recoups at least half of

the loss from the January high followed by a drop to new lows for the

move.

If you want to establish or add to a bearish/hedge position

then the aforementioned rebound -- assuming it happens -- will create the

best opportunity to do so. If you currently have no hedges or bearish

speculations it also could make sense to take an initial position now, via

either an inverse index fund or options with an expiry date of April or

later. The reason is that even if we are dealing with nothing more than a

short-term correction, the decline is probably less than half complete.

The most ridiculous price action yet?

Many

absurd things have happened in the stock market over the past 12 months.

The latest absurdity worth highlighting is the price action of Amazon.com

(AMZN) since the beginning of the year. This large-cap low-margin retailer

was already trading at a nosebleed valuation when 2017 came to a close,

but it has risen in almost a straight line since the start of this year

and at Friday's high was up 28% year-to-date. That is, it was up by 28% in

less than 5 weeks.

This could be written off as just another in a long line of upside

blow-offs, but adding to the absurdity of the situation is that AMZN's

stock price accelerated upward last week as the broad market retreated. It

seems, therefore, that 'investors' are viewing AMZN as a safe haven -- a

place to take shelter in times of increasing financial-market instability.

AMZN is the new gold!

We assume that the logic, or what passes for

logic these days, is that AMZN has a) no dividend yield, b) no chance of

having a dividend yield within the next couple of years, and c) almost no

earnings yield*. Consequently, as stocks that provide a significant yield

are made less attractive by rising interest rates, liquid stocks that

provide almost no yield become relatively attractive.

The

'investors' who jumped into AMZN shares last week to escape the

consequences of rising interest rates can look forward to large losses.

*The earnings yield is the reciprocal of the

P/E ratio. A stock such as AMZN that has a P/E ratio of about 360

therefore can be said to have an earnings yield of about 0.28%.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Feb-05 | ISM Non-Mfg Index |

| Tuesday Feb-06 | International Trade Balance |

| Wednesday Feb-07 | Consumer Credit |

| Thursday Feb-08 | No important events scheduled |

| Friday Feb-09 | No important events scheduled |

Gold and the Dollar