![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 5th March 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bearish (12 Jan 2018) |

| US Equity (SPX) | Neutral (12 Jan 2018) |

| Currency (Dollar Index) | Bullish (15 Dec 2017) |

| Commodities (GNX) | Bullish (29 Dec 2017) |

Last week's posts at the TSI Blog

The

warning shots of 2007

Summary of current

thinking/positioning

1) Thinking that the US$ gold

price will go on to make new highs for the year during the second quarter,

but that a short-term correction low is not yet in place.

2)

Favouring a drop in the stock market to test the early-February low during

March, but assigning a very low probability that the decline from the

January peak is something more bearish than a short-term correction.

3) Thinking that industrial commodities such as oil and copper are in

downward trends that will end in March.

4) Expecting the rebound in

the Dollar Index (DX) to continue for a few more weeks before the

longer-term downward trend resumes.

5) Expecting that the T-Bond

will rebound for a few weeks and then resume its downward trend.

6)

Holding a cash reserve of 25%-30% and looking for opportunities to

increase it.

Economic Numbers

G2 Monetary Inflation

The ECB got around the publishing its January-2018 money-supply data

last week, enabling us to update our calculation of the G2 (US plus

euro-zone) monetary inflation rate. The G2 monetary inflation rate has a

closer relationship to the overall financial-market and economic backdrop

than does the US monetary inflation rate in isolation.

The

following chart shows that the year-over-year rate of growth in G2 money

supply was essentially unchanged in January and remains in the bottom

quartile of its 20-year range. The monetary backdrop is therefore not

supportive of equity prices or Keynesian measures of economic performance

such as GDP, although we aren't yet seeing evidence in the monthly

economic numbers and other high-frequency data that the tightening of

monetary conditions has begun to matter.

US Recession Watch

The latest iteration of the

ISM New Orders Index (NOI), one of our three primary leading indicators of

US economic recession, was reported on Thursday 1st March. It was down a

little from the preceding month but remains near the top of its 20-year

range.

As a result, there has been no change in our expectations regarding

the timing of the next US recession. The probability of a recession

beginning during the first half of this year remains close to zero, but

due to the tightening of monetary conditions there is a realistic chance

that a recession will begin before year-end.

Commodities

Gains in the Grains

We don't know how to assess the fundamentals of the grain markets, but

we've noticed that grain prices have turned upward from very depressed

levels on long-term monthly charts and that the grains are cheap relative

to many other commodities. Given that global grain consumption will almost

certainly be higher in the future than it is in the present, the price

up-turns from levels that are low by historical standards in both absolute

and relative terms suggests to us that these commodities have bullish

intermediate-term and long-term risk/reward ratios.

Here are the

long-term monthly charts that have piqued our interest:

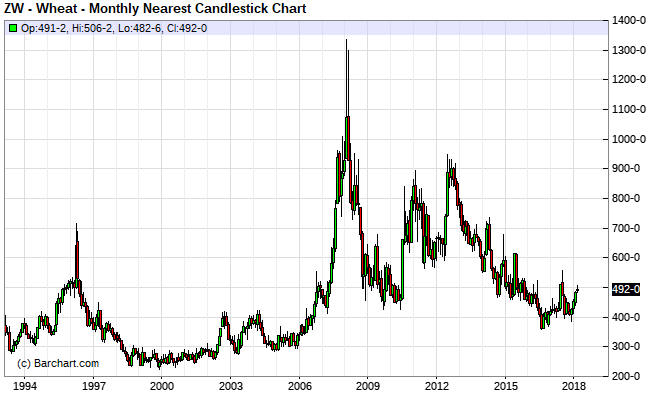

1) The

wheat price made a 10-year low in mid-2016. It then rebounded for about 12

months, quickly retraced the bulk of its rebound, and then, in

December-2017, resumed what could be a new long-term bullish trend.

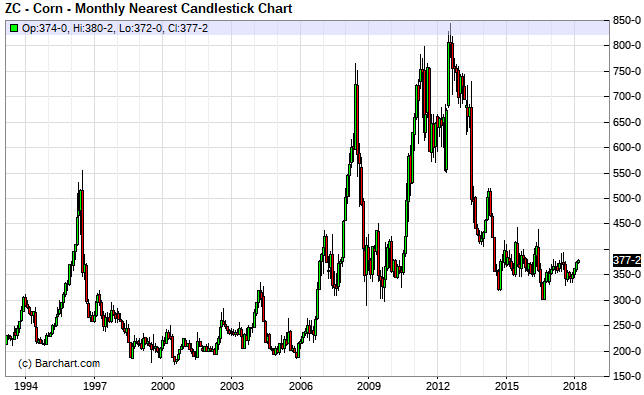

2) Corn is in a similar position to wheat, except that the corn

market's mid-2016 low was a successful test of the 2008-2009

financial-crisis low.

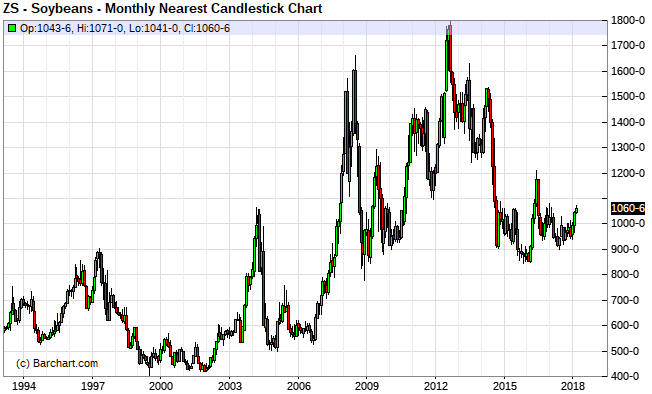

3) The soybean market has been stronger than the wheat and corn

markets, in that the 2016 bottom for the soybean price was above the

financial-crisis low. Also, over the past two years the soybean market has

led the wheat and corn markets by several months.

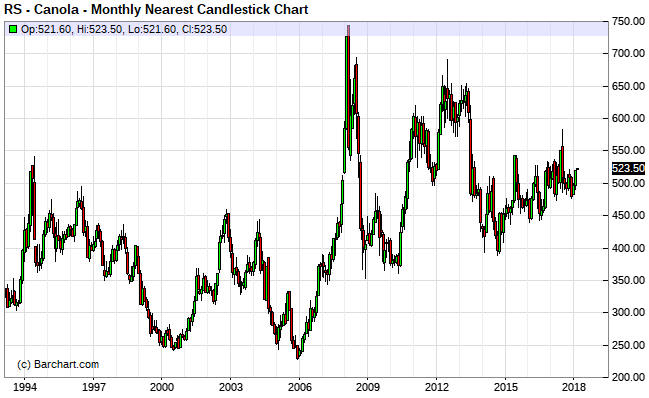

4) Canola has been the strongest of the grain markets that we keep an

eye on. It has been working its way higher since late-2014 and is now in

the middle of its 10-year range.

And here are charts showing the recent reversals in the strength of

the iPath Grains ETN (JJG) relative to the SPDR Gold ETF (GLD) and the

iPath Copper ETN (JJC):

For us, a problem with being long-term bullish on the grains is that

we don't know of a good way to participate in a grains bull market. JJG is

fine for short- or intermediate-term trades, but due to contango-related

value leakage it will tend to underperform the associated commodities by a

wide margin over the long term. Displayed below is a chart showing the

long-term performance of JJG.

Input Capital (INP.V), a stock we mentioned a few weeks ago, does

canola streaming deals with farmers in Canada and should profit from a

continuing upward trend in the canola price, but over the past few years

there has been no relationship between the INP share price and the canola

price.

At this stage we view the nascent long-term upward trends in

grain prices mainly as supports for our view that bond yields have

commenced long-term upward trends. The reason is that rising food prices

will contribute to increasing concern about "inflation".

Platinum completes a routine correction

In late-January

the platinum price was testing the bottom of its $1025-$1050 resistance

range. At that time (in the 22nd January Weekly Update) we wrote:

"We

will be surprised if the platinum price manages to break above $1050

before experiencing a multi-week correction. Note that a routine

correction would retrace about half of the rally from the December low,

implying that the mid-$900s would be a realistic target for the next

tradable low if a correction were to begin near the current price."

Platinum traded as low as $956 last week, so the "realistic target for

the next tradable low" has been reached. There's no evidence that the

correction is complete, but the mid-$900s is a reasonable place for

investors with a 6-12 month or longer timeframe to do some buying.

Due to falling demand for catalytic converters associated with the

rising popularity of EVs, platinum's long-term supply/demand relationship

is bearish for the price of the metal. A consequence could be that a

platinum/gold ratio of 1 will transform from a signal that platinum is

near a major price bottom to a signal that platinum is near a major price

top. That is, what was major support for platinum relative to gold in the

past will, in the future, be major resistance. However, assuming -- as we

are -- that the gold price will move into the $1400-$1500 range later this

year, there will be a lot of scope for platinum to rally while remaining

cheaper than gold.

We are bullish on platinum with regard to the

next 6-12 months.

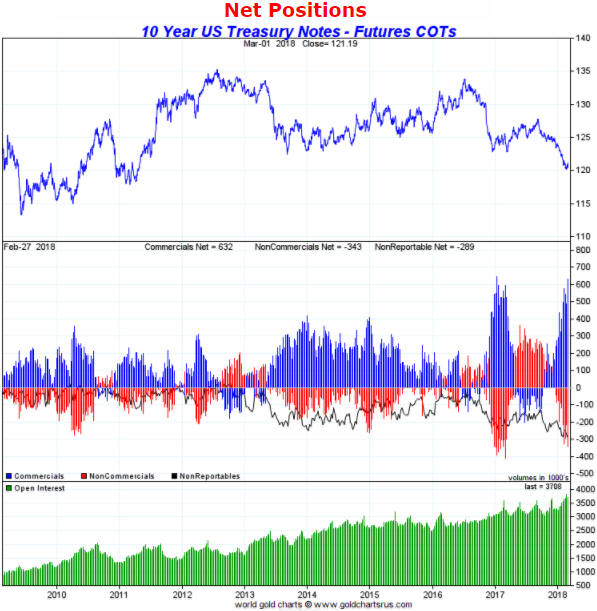

Speculators get

even more bearish on the T-Note

The total speculative net-short

position in 10-year T-Note futures surged during the latest week and is

now within a whisker of its all-time high. Refer to the following weekly

chart for details.

The all-time high for the speculative net-short

position occurred in January of last year and set the scene for an 8-month

upward consolidation in the 10-year T-Note. The rise to a similar level

over the past week means that this is not a good time to be placing

short-term bets on lower bond prices (higher bond yields), although this

time around we aren't expecting anything more than a multi-week upward

consolidation.

The Stock Market

Is the high level of

margin debt a problem?

The following chart was extracted

from the article posted

HERE and shows that US stock-market margin debt, which is reported

monthly with a lag of about one month, moved sharply higher in

January-2018 from an already-high level. Is this a problem?

According to FINRA (the Financial Industry Regulatory Authority) it is

a problem. The above-linked article notes that FINRA issued an alert in

January, warning: "...many investors may underestimate the risks of

trading on margin and misunderstand the operation of, and reason for,

margin calls." And: "Investors who cannot satisfy margin calls

can have large portions of their accounts liquidated under unfavorable

market conditions. These liquidations can create substantial losses for

investors."

There is no doubt that the liquidation of margin

debt will magnify and accelerate the next intermediate-term stock market

decline or bear market, but there won't be a bear market as long as

leverage continues to increase. To put it another way: regardless of how

large the pile of margin debt becomes, the start of a bear market won't be

imminent as long as the pile is still growing.

The debt pile would

have shrunk a little in February, but it will take more than one month of

shrinkage in margin debt to warn that the equity bull market is on its

last legs.

Tariffs and the Stock Market

One

of the few concepts that almost all economists agree on is that tariffs

are bad for the economy. The reason for the agreement is that a deep

understanding of how the economy works is not required to know that

artificially raising the price of a good to help the local producers of

the good will hurt the local consumers of the good. Since the number of

local consumers will always be much greater than the number of local

producers of a protected good, it is obvious that the price-boosting

intervention will be harmful to the overall economy.

It will be

harmful even if there is no retaliation from other governments, but

retaliation in some form will often happen. The risk, therefore, is that

the initial tariff will turn out to be the first shot in a trade war and

an economic downward spiral.

That being said, the US tariffs on

steel and aluminium that were announced last week by the Trump

Administration were not the reason for last week's stock market downturn.

To believe that they were you would have to believe at least one of the

following fallacies:

1) The level of the stock market is first and

foremost a reflection of the state or expected state of the economy. Note

that if this were true then the S&P500 Index (SPX) would now be at least

30% lower.

2) In the absence of policy error there would never be a

downward correction in the stock market.

3) If news event A is

followed by market event B, then A must have caused B.

The third of

the above fallacies forms the basis of most explanations of market action

found in the mainstream press.

The reality is that at the

late-January peak the US stock market was more stretched to the upside in

both momentum and valuation terms than it had ever been. At that time the

stage was therefore set for a significant correction, with the main

unknowns being exactly when the correction would start and why the market

had managed to rise for so long without a significant correction.

When the initial leg of a correction is large and fast, which is the

situation we are currently dealing with, there will typically be a rebound

and then a decline to test the low of the initial leg REGARDLESS of the

news.

Current Market Situation

The US

The SPX broke above minor

resistance at 2750 last Monday and then negated the breakout the next day.

This was a bearish signal.

Last Tuesday's downward reversal was

followed by additional weakness on Wednesday and Thursday that took the

SPX below its 50-day and 20-day MAs. Friday's rebound did no more than

take the index back to its declining 20-day MA and therefore wasn't

significant.

The SPX's price action suggests that a test of the

early-February low remains a good bet.

Last week's performance by the SPX has short-term bearish

implications, but the waters are muddied by the performance of the NDX.

After testing its January peak on Monday 26th February, the NDX did no

more than pull back to test its rising 50-day MA.

Despite the resilience of the NDX, we expect that most US stock

indices will test their early-February lows during March. The test could

occur as soon as this week or wait until the second half of the month.

Our plan is to exit all short-term bearish speculations if the SPX

tests its early-February low this week. Also, we will be stopped out of

all short-term bearish speculations if the SPX closes above 2781.

Europe

Equities have been much

weaker in Europe than in the US. This is evidenced by the fact that for

the EURO STOXX 50 Index (STOX5E) last week's downward reversal has already

led to a test of the early-February low. It is also evidenced by the

STOX5E ending last week near a 12-month low.

The STOX5E has

long-term support at 3100-3150. This is the most likely area for a

multi-month bottom.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Mar-05 | ISM Non-Mfg Index |

| Tuesday Mar-06 | Factory Orders |

| Wednesday Mar-07 |

International Trade Balance Consumer Credit Fed's Beige Book |

| Thursday Mar-08 | No important events scheduled |

| Friday Mar-09 | Monthly Employment Report |

Gold and the Dollar