--

Weekly Market Update for the Week Commencing

5th December 2016

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Neutral

(21-Nov-16) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Neutral

(17-Aug-16) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Neutral

(21-Nov-16)

|

Bearish |

|

Stock Market (DJW)

|

N/A |

Neutral

(14-Nov-16) |

Bearish |

|

Gold Stocks

(HUI)

|

N/A |

Neutral

(21-Nov-16) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Neutral

(10-Oct-16) |

Bullish |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

An economy can't be modeled by simple equations

Every central bank wants a weaker US$

Summary of current

thinking/positioning

1) Continuing to expect that the

overall corrections/downturns for gold and the associated mining indices

will extend into Q1-2017, but anticipating an intervening rebound.

2) Expecting that 2017 will be a bullish year for commodities. Maintaining

long-term exposure to non-gold commodities while acknowledging that the

early-2016 lows could be tested in Q1-2017 prior to the start of the

aforementioned bullish period.

3) Expecting a decline in the oil

price to a January-February bottom and positioned for this outcome via USO

put options expiring in February. Took advantage of last week's

OPEC-inspired surge in the oil price to add to the position. Note that in

addition to being a speculation, these options have been purchased as a

hedge against short-term weakness in the commodity markets.

4)

Thinking that government bonds have commenced a long-term bear market, but

that the US Treasury Bond is close to a short-term price bottom.

5)

Expecting a further 6-12 month extension to the equity bull market and

looking for opportunities to add to general non-US equity exposure, but

maintaining a very small short-term bearish speculation via QID (leveraged

NDX bear fund) call options expiring in January-2017.

6) Thinking

that the Dollar Index is close to a 1-2 month top, but that it will move

to new multi-year highs during the first quarter of 2017 and won't reach a

major top before the second quarter of 2017.

7) Maintaining a large

cash reserve in recognition of the downside risk in almost all equities

(current cash percentage is about 40%).

US Recession

Watch

The latest iteration of the

monthly ISM Manufacturing New Orders Index (NOI) was published last

Thursday. It was for the month of October and came in at 53, which is 0.9

points higher than the September reading and 5 points above the level that

it would have to fall below (the red line on the following chart) to

signal an imminent recession.

The NOI's message is that a US

economic recession will not begin within the next two months, while the

message of our favourite long-term indicator (Real Gross Private Domestic

Investment - RGPDI) is that a recession will begin by the second quarter

of next year. Taken together the indicators suggest that a recession will

begin no earlier than February-2017 and no later than June-2017.

That being said, we acknowledge the possibility that it could be different

this time, meaning that the lag between a downward reversal in RGPDI and

the start of a recession could be longer, this time around, than it has

ever been before. This is mainly due to the unprecedented behaviour of the

Fed during the current business cycle, but it's a possibility that has

been given a higher probability by the new US President's plan to

immediately implement aggressive fiscal 'stimulus' in the form of a large

deficit-funded (meaning: unfunded) tax cut.

As an aside, it's

extraordinary that the US looks set to have the combination of ultra-easy

monetary policy and aggressive fiscal stimulus more than 7 years into an

economic recovery. In essence, the US government and central bank are

going to be acting as if the economy were in the grip of a severe

recession at the same time as they report that the economy is perfectly

fine.

A record-long recession lag would potentially pave the way

for the strength in commodity prices and the additional weakness in bond

prices that we've forecast for 2017.

The limitations

of sentiment

Most participants in the

financial markets get swept up by the general mood. As a result, after

valuations have become very high they buy into the idea that prices are

going much higher despite the high valuations, and after valuations have

become very low they buy into the idea that prices will continue to slide

despite the attractive valuations. This causes them to be very optimistic

near important price tops and either very pessimistic or totally

disinterested near important price bottoms.

It must always be this

way because a major price/valuation trend can't end until it has been

fully embraced by 'the public'. There is therefore no chance that the

investing public will ever collectively enter or exit any market at an

opportune time.

That's why it is helpful to track the public's

sentiment and use it as a contrary indicator.

However, sentiment is

not the Holy Grail of investing/speculating. There are, in fact, two

potential pitfalls associated with using sentiment to guide buying/selling

decisions, the first of which is linked to the reality that sentiment

generally follows price.

Because sentiment generally follows the

price, it is a near certainty that the overall mood will be at an

optimistic extreme when the price is near an important top and a

pessimistic extreme when the price is near an important bottom. However,

just as all poodles are dogs but not all dogs are poodles, an important

price top will always be associated with a high level of optimism but a

high level of optimism won't always mean that an important price top is at

hand. Similarly, while an important price bottom will always be associated

with a high level of pessimism, a high level of pessimism won't always

indicate that the price is near an important bottom. This means that it is

dangerous to take large positions based solely on sentiment.

The

second potential pitfall associated with using sentiment to guide

buying/selling decisions is that what constitutes a sentiment extreme will

vary over time, meaning that there are no absolute benchmarks. Of

particular relevance, what constitutes dangerous optimism in a bear market

will often not be a problem in a bull market and what constitutes extreme

fear/pessimism in a bull market will often not signal a good buying

opportunity in a bear market. In other words, context is critical when

assessing sentiment. Unfortunately, the context is always a matter of

opinion.

The gold-mining sector's performance over the past

several years provides a good example. By the first quarter of 2013 there

were enough signs of fear and pessimism within this sector to indicate

that an important price bottom might not be far away, but the downward

trend continued for almost three more years. The view that sentiment was

pointing to an important price bottom for the gold-mining sector in

Q1-2013 would most likely have been right if the decline from the 2011

peak had been a bull-market correction, but the long-term trend had

changed. The sentiment levels that indicate attractive buying

opportunities in a bull market do not work the same way in a bear market.

The bottom line is that sentiment can be a useful indicator, but it

does have serious limitations.

Copper Update

The copper price spiked up to

the mid-$2.70s three weeks ago and then pulled back. It again spiked up to

the mid-$2.70s last week and might have just made a 'double top' in that

area.

As we wrote three weeks ago, even if copper has commenced a

major rally there is likely to be a significant short-term correction. A

decline to the $2.30s to 'test' the breakout would be normal even if we

are dealing with a new bull market, but a deeper decline is possible given

that the speculative net-long position in Comex copper futures hit an

all-time high early last week.

The Stock Market

The US

Oh how the narrative has changed!

The change in the dominant narrative over the past few weeks is remarkable

and also a little funny. Prior to the US Presidential Election the popular

story was: Clinton is probably going to win and it will be business as

usual, but in the unlikely event of a Trump victory all hell will break

loose. There will be a big decline in the stock market and a rush into

safe havens.

Now here we are, four weeks and a 'surprising' Trump

victory later, and the popular story is: Due to the combination of tax

cuts, infrastructure spending and de-regulation that he will bring about,

there's no doubt that the Trump Presidency will be very bullish for both

the stock market and the economy.

In the meantime, Trump's message

hasn't changed at all. It's just that as soon as the stock market started

to rally the commentariat's interpretation of the message suddenly

changed. It changed for no reason except that prices were rising.

Which goes to show that much of what passes for fundamental analysis is

not genuine fundamental analysis. Instead, it's the concoction of a story

to match the price action.

Current Market

Situation

We are fixating on the NASDAQ100 Index (NDX) due

to its importance and the fact that it did not confirm the recent upside

breakouts in many other US stock indices. The NDX is at the same level now

as it was 4 months ago. It is also at the same level now as it was 12

months ago.

Over the past few months it oscillated within the

rectangle drawn on the following daily chart. It tested the top of the

rectangle early last week and then reversed direction.

If the NDX breaks upward from the 4650-4900 range it will confirm the

upside breakouts achieved by the SPX and the Dow Industrials, but if it

breaks downward from this range it will warn that the upside breakouts by

the other indices were false signals.

The probabilities of an

upside breakout and a downside breakout are roughly the same, but we are

positioned to benefit from a downside breakout via QID call options.

Europe

The EURO STOXX50 Index (STOX5E) is

Europe's equivalent of the Dow Industrials Index.

Like the NDX,

STOX5E has oscillated within a horizontal range over the past few months

and is at the same level now as it was 4 months ago. However, that's where

the similarities with the NDX end, because STOX5E is a long way below its

level of 12 months ago and is also below the high reached in April of this

year.

STOX5E is possibly building a long-term base with a double bottom in

February and June. A weekly close above the April high (3150) would

suggest that the base was complete and that a major rally was in progress,

but even if the long-term base interpretation is correct there could be

significant short-term weakness.

A daily close below 2950 would

warn of a short-term decline to 2800 or lower.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday December 05 |

ISM Non-Mfg Index |

| Tuesday

December 06 |

Q3 Productivity and Costs

(revised)

Factory Orders |

|

Wednesday December 07 |

Consumer Credit |

|

Thursday December 08 |

No important events scheduled |

|

Friday December 09 |

No important events scheduled |

Gold and the Dollar

Gold

Gold Sentiment

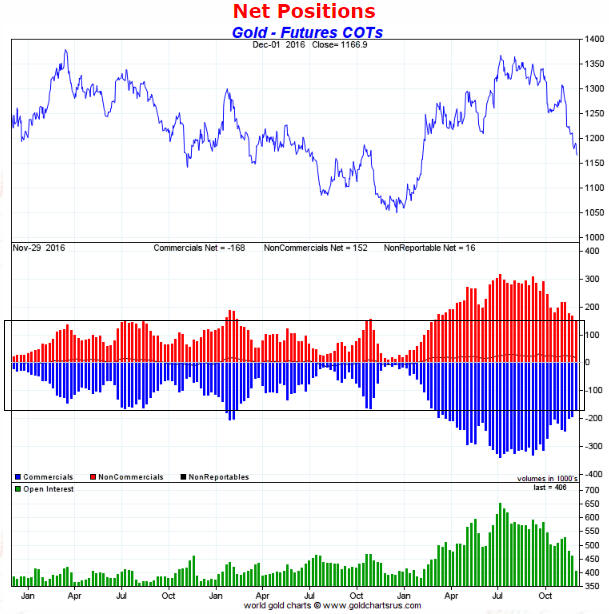

a) The COT (Commitments

of Traders) Situation

There was a sizable decline in the total

speculative net-long position in Comex gold futures during the latest period

(the period ending Tuesday 29th November). The total speculative net-long

position fell by 24K contracts (from 192K to 168K contracts) during the latest

1-week period and has fallen by almost 80K contracts since 8th November.

It's reasonable to view the liquidation of speculative long positions as both an

effect and a cause of the recent weakness in the gold price. Downward pressure

stemming from fundamental deterioration probably caused support levels to give

way, prompting a rush for the exits by technically-oriented speculators that

added to the downward pressure.

The gold price is now $13 lower than it

was on 29th November, so it's likely that there has since been a further

reduction in the total speculative net-long position. In fact, it potentially

reached 150K contracts late last week.

150K contracts is the level that

we previously wrote (in at least 4 commentaries) would probably be reached prior

to the end of the overall correction. So, are we there yet?

The answer to

the above question gets back to the context issue with sentiment indicators that

we discussed earlier in today's report. If a new cyclical gold bull market began

last December then a 150K-contract speculative net-long position would be

consistent with a price bottom. However, fundamental factors currently suggest

that a new gold bull market has NOT yet begun.

If a new gold bull market

has not yet begun then the speculative net-long position has not yet reached

price-bottoming territory. As illustrated below, what we currently have is a

speculative net-long position that has dropped back to near the TOP of its

bear-market range (the range that was established during 2013-2015).

Our

assessment, in a nutshell, is that gold's COT situation has greatly improved,

but given the fundamental backdrop it is not yet consistent with the overall

decline being complete.

b) The GLD (gold bullion ETF) Inventory

The relationship between the

gold price and GLD's inventory of physical gold is generally misunderstood and

misreported. At best, the change in GLD's inventory is an indicator of

gold-market sentiment, and like most measures of sentiment it is a contrary

indicator. Also like most measures of sentiment, it typically follows the price.

Consequently, the change in the GLD inventory usually tells you what

happened to the gold price in the past while telling you very little about what

is likely to happen to the gold price in the future.

The only time it

has the potential to provide useful information about the future is after it has

risen sharply or fallen sharply, in which case it could be warning that the

market price is stretched to the upside (if the GLD inventory has risen sharply)

or stretched to the downside (if the GLD inventory has fallen sharply) on a

short-term basis. Interestingly, however, most commentary on the GLD inventory

portrays the information in the opposite way. For example, it will usually

portray a large/sharp rise in the GLD inventory as bullish, rather than as a

warning that the risk/reward has become skewed towards risk in the short-term.

A final point worth making (reiterating, actually) before we take a look at

the recent changes in the GLD inventory is that a rise in the amount of physical

gold held by GLD and other bullion ETFs does NOT reflect increasing demand for

physical gold; it reflects disproportionately-aggressive buying of 'paper gold'

(GLD shares). This is because physical gold only gets added to GLD's inventory

-- via the arbitrage trading of Authorised Participants -- when the price of a

GLD share rises relative to the price of physical gold. In effect, a rising GLD

inventory indicates rising demand for a type of 'paper gold' relative to

physical gold.

The following chart shows the long-term positive

correlation between the gold price and GLD's physical gold inventory. The

correlation is not perfect, but what it indicates is that traders of GLD shares

generally become more bullish when the gold price is trending upward and less

bullish when the gold price is trending downward.

Zooming in on the past

12 months we see that the GLD inventory bottomed with the gold price last

December and then began trending upward with the gold price. It peaked with the

gold price in early-July and then began to trend downward with the gold price,

hitting a new multi-month low late last week in response to a new multi-month

low in the gold price.

This unfortunately tells us nothing useful,

because there have been no disproportionately-large moves by the GLD inventory

in either direction (meaning: no indications of extreme sentiment) and no

significant divergences between the GLD inventory and the gold price. It simply

tells us that GLD traders became more optimistic as gold trended upward from its

December-2015 bottom and less optimistic as gold worked its way downward from

its early-July peak.

In summary, the GLD inventory is an indicator of the sentiment of GLD

traders that generally doesn't provide useful clues about the future gold price.

In terms of ability to provide clues about what the future holds in store or

warnings based on risk/reward, it is definitely less useful than the COT data.

That's why we rarely mention it.

c) Market Vane

Unlike the COT

data, at no time this year has Market Vane's sentiment survey indicated extreme

enthusiasm for gold. According to Market Vane, the proportion of traders who are

bullish on gold peaked at a fairly modest 63% in early-July. The bullish

percentage has since dropped to 48%.

48% would be consistent with the end

of an intermediate-term correction within a bull market, but would not be

consistent with the end of an intermediate-term decline within a bear market.

The Price Action

The Dollar Index

has edged downward since reaching some sort of a peak during the week before

last, but the US$ gold price has remained under pressure due to relentless

weakness in the bond market. Due to a declining T-Bond price, the bond/dollar

ratio made a new low for the year on Thursday 1st December before rebounding a

little on Friday. The US$ gold price often moves with the bond/dollar ratio

(refer to the following chart for an illustration of the relationship), so in

this respect it wasn't surprising that the gold price made a new multi-month low

on Thursday before bouncing on Friday.

By the way, based on the current

level of the bond/dollar ratio the gold price should now be near its 2015 low of

around $1050/oz. In other words, an argument could be made that the gold price

has held up remarkably well considering the fundamental backdrop. However, the

bond/dollar ratio is a better indicator of gold price direction than absolute

gold price level. Also, the bond/dollar ratio tends to experience bigger swings

than the gold price in both directions.

The downward pressure on the gold

price currently being applied by a declining bond/dollar ratio should soon

switch to upward pressure thanks to a rebound in an extremely 'oversold' T-Bond

market.

The small divergence between the gold price and the HUI became more

significant last week. As illustrated by the following chart, there has now been

about three weeks of a downward-trending gold price combined with a slight

upward bias in the HUI/gold ratio.

Regardless of whether they are

superficially bullish or bearish based on conventional wisdom, any sort of

divergence between the bullion market and the gold-mining indices after prices

have been trending strongly for a few months is a warning to be ready for a

short-term trend reversal.

We continue to anticipate a short-term rebound in the gold market. This view

is now supported by sentiment, divergences, and the extent to which prices in

both the gold market and the T-Bond market are stretched to the downside on a

short-term basis. At the same time, due primarily to the gold-bearish

fundamental backdrop we see no good reason to believe that the intermediate-term

declines are almost over.

Gold Stocks

The HUI

essentially bottomed back on 14th November when the gold price was $1211. It has

since traded a little lower, but has never closed below its 14th November

intra-day low and is now showing incipient signs of strength. This means that

the gold-mining sector pretty much ignored the decline in the gold price from

the $1210s to the $1170s.

An

implication of the gold-mining sector's recent stability in the face of a steady

decline in the gold price is that both the gold price and the gold-mining sector

will soon rally.

The first clear signal that a significant short-term

rally is underway will be a daily close above 196 by the HUI. The top of a

very-well-defined channel lies just above 200 and could temporarily halt any

advance, but we suspect that once a rally gets going it will continue until at

least the 200-day MA.

The Currency Market

The

euro managed to 'hold the line' (major support near 105) over the past two

weeks. It is therefore yet to confirm to upside breakout in the Dollar Index.

A downside breakout followed by a drop to parity (100) or lower is likely

within the next few months, but in the meantime there is the potential for a

euro rebound to as high as 110.

Whether a rebound gets underway from near

the current level or is preceded by a downward spike will depend on the general

perception of the European political and monetary events mentioned in last

week's Interim Update. There is the Italian referendum scheduled for Sunday 3rd

December, the Austrian presidential election scheduled for the same day, and the

ECB meeting scheduled to take place on Thursday 8th December. Although

officially a vote on the power of Italy's upper house of parliament, the Italian

referendum has the greatest potential to move the markets in the near-term

because it has been portrayed as a vote of confidence/no-confidence in Italy's

Prime Minister.

The Canadian Dollar (C$) has our attention at the moment.

The recent rise

in the oil price has led to what is, to date, a weak rebound by the C$. As

illustrated below, the C$ has rebounded by about one point to channel resistance

at around 75.25. This is similar to its position in mid-October -- just prior to

the start of a decline to new multi-month lows.

A daily close above 75.25

would indicate that a larger-degree rebound was underway and that a rise to the

more important resistance near 76.5 was probably on the cards.

We

use the C$ as an oil-price indicator. A daily close above 75.25 by the C$ would

warn that oil's OPEC-inspired rally has more staying power than we currently

perceive, while a solid break by the C$ above 76.5 would largely remove the

oil-C$ divergence on which our short-term oil bearish bearishness is based. By

the same token, if the C$ were to reverse downward early this week without

making additional headway it would be evidence in support of our short-term

bearish outlook for the oil price.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 2nd December 2016:

Company

news/developments for the week ending Friday 2nd December 2016:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, MD&A = Management

Discussion and Analysis, M&I = Measured and Indicated, NAV = Net Asset Value,

NPV(X%) = Net Present Value using a discount rate of X%, P&P = Proven and

Probable, PEA = Preliminary Economic Assessment, PFS = Pre-Feasibility Study]

*Alkane Resources (ALK.AX) provided an update on its

progress.

The company is in the process of securing offtake arrangements

for the various outputs from the Dubbo Zirconia Project (DZP). This involves

providing samples of some of the products to potential customers and must be

done before construction financing can be finalised. Construction financing is

expected to be a mixture of debt and equity, including a possible strategic

investment at project level.

Also, an updated engineering/economic study

using a modular construction method is in progress and is now scheduled to be

completed in April of 2017 (was previously Q1-2017). The updated study should

confirm that the initial capital cost can be substantially reduced, possibly by

as much as half. If so, this will make it easier to arrange the construction

financing.

ALK's recent stock-market performance has been surprising, to

put it mildly. We were surprised when the stock price gained more than 50% for

no apparent reason over a 2-week period in October and then even more surprised

when the stock price lost almost 50% for no apparent reason over a 3-week period

in November.

Near its current price in the low-A$0.30s ALK is back to a

level where new buying would be reasonable.

*Solitario

Exploration and Royalty (XPL) has decided to pay for a PEA to be done

for the Bongara zinc project in Peru. Bongara is 30%-owned by XPL and 70%-owned

by Milpo, a large mining company.

XPL is carried to production at

Bongara, meaning that it isn't obligated to pay anything for the project's

exploration and development until commercial production is achieved. At that

point, XPL would be obligated to start paying-off its 30% share of the

construction cost by using 50% of its share of the net proceeds of production.

In other words, there is no requirement for XPL to fund a PEA or do anything

else to move the Bongara project forward. So, why is XPL spending money it

doesn't need to spend?

The crux of the matter is that whereas Bongara is

the flagship asset of XPL, it is just one of many assets for Milpo. Milpo

obviously likes the asset but does not view its development as a top priority.

Consequently, for XPL to highlight the value of the project within what it

considers to be a reasonable time, it will have to pay for its own economic

analysis. XPL's intention is to have a completed PEA by mid next year.

This is probably a smart move, although much will depend on the cost of doing

the PEA.

*Sprott Resource Corp. (SCP.TO) has

struck a deal to merge with Adriana Resources (ADI.V), a small company with a

40% stake in the Lac Otelnuk Iron Ore Project ("LOM Project") located in

Nunavik, Quebec. Or, to put it more accurately, Arthur Richards Rule IV (a.k.a.

Rick Rule) has put together a deal that involves combining SCP and ADI.

The proposed merger involves SCP shareholders receiving three shares of ADI for

each of their SCP shares and ADI being renamed "Sprott Resource Holdings" (SRH)

after completion of the merger.

The first time we read the press release

announcing the merger we got the impression that it was a bad deal for SCP

shareholders, because the LOM project is a long way from being economic at the

current iron-ore price and there is no good reason to be long-term bullish on

iron-ore. Our initial impression was that SCP was selling almost one-third of

itself to a company with an asset that was almost worthless. However, by the

time we had read the rather complicated press release four times we liked the

deal.

ADI's main contribution to the combined company will actually be

its C$28M of cash, with the 40% stake in the LOM project appropriately being

assigned almost no value. Furthermore, Sprott Inc. and a company controlled by

Rick Rule will be investing C$15M in the combined company at a substantial

premium to the current market price. Specifically, it is expected that the

Sprott/Rule investments will be made at the equivalent of about C$0.70 per

current SRC share.

The post-merger company (SRH) is expected to have

about C$55M of cash, no debt, and a net asset value (NAV) of about C$0.30/share

(equivalent to about C$0.90 per current SCP share). It will also have Rick Rule

as its CIO (Chief Investment Officer), which is important.

Rick Rule is

the ideal person to be making the decisions at a resource-investment company.

This is not only because he is good at identifying high-potential investing

opportunities, but also because he doesn't get sucked-in by the stock market's

manic-depressive swings (he is adept at scaling-in during the depressions and

scaling out during the manic phases). With Rule as CIO, both the selection and

the timing of investments by SRH in the future should be much better than was

the case with the old SCP.

The post-merger company is likely to be one of

the go-to vehicles for investors wanting broad-based exposure to natural

resources. Furthermore, although the price of SCP shares gained a little in

response to last week's news, it is still a long way below both the current NAV

and the implied post-merger NAV. As a result of the planned changes to the

company's management and balance sheet, the large discount to the implied

post-merger NAV seems unjustifiable.

SCP is a good candidate for new

buying near its current price of C$0.54. However, ADI is possibly an even better

buy near its current price of C$0.18. The reason is that even though three new

ADI shares will be paid for each SCP share, the existing ADI shares are worth

slightly more than one-third of an SCP share due to the fact that pre-merger ADI

shareholders will receive one-quarter of a 5-year warrant with an exercise price

of 33.3c to go along with each of their shares. We calculate that fair value for

these warrants would be about C$0.05 at ADI's current price of C$0.18, which

means that they would add about 0.01 to the value of each existing ADI share

(since each existing share would be entitled to one-quarter of a new warrant).

This is obviously not much, but the warrant value will rise exponentially,

making the warrants relatively more important, if the stock price rises. For

example, if the ADI stock price were to rise about 70% to its

currently-estimated post-merger NAV of C$0.30 then our calculated fair value for

the warrants would rise 160% to around C$0.13.

So, to get the warrants we

would be inclined to favour ADI over SCP for new buying as long as ADI is

trading at one-third of SCP or lower. Note, though, that there is slightly

greater risk associated with buying ADI rather than SCP due to the small chance

of the merger not being completed. Due to this risk it wouldn't be wise to pay

more for ADI shares than C$0.19 or one-third of the SCP share price, whichever

is lower.

*Timmins Gold (TGD) announced that its

C$20M equity financing was 'done and dusted'. The company issued about 36M units

at C$0.55/unit, with each unit comprising a share of the company and one-half of

a warrant. The warrants, which have an exercise price of C$0.70 and an expiry

date of 30th May-2018, have been listed on the TSX under the symbol TMM.WT.

At the current Timmins share price we estimate fair value for the warrants

to be C$0.05. They are a high-risk/high-reward speculation. There's at least a

50% probability that they will expire worthless in 18 months' time, but they

have '10-bagger' potential.

List

of candidates for new buying

From within the ranks of TSI stock

selections the best candidates for new buying at this time, listed in

alphabetical order, are:

1) AAU (last Friday's closing price: US$1.05)

2) BLK.AX (last Friday's closing price: A$0.47)

3) EVN.AX (last

Friday's closing price: A$1.89)

4) PG.TO (last Friday's closing price:

C$2.26)

5) SCP.TO (last Friday's closing price: C$0.535)

Note that

the above list is limited to five stocks. It will sometimes contain less than

five, but it will never contain more than five regardless of how many stocks are

attractively priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.goldchartsrus.com/