![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 6th January 2020

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bullish (27 Dec 2019) |

| US Equity (SPX) | Bullish (20 Dec 2019) |

| Currency (Dollar Index) | Neutral (15 Mar 2019) |

| Commodities (GNX) | Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

There were no blog posts last week.

Summary of current

thinking/positioning

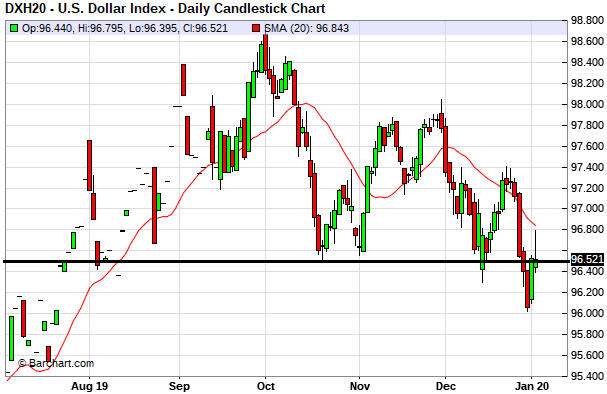

1) The Dollar Index (DX) remains

range-bound, needing a weekly close below 96.5 to signal an

intermediate-term reversal to the downside or a weekly close above 99.5 to

signal an intermediate-term rally.

2) For gold, silver and the

gold-mining indices/ETFs, we expect a multi-month top in January.

3) The senior US stock indices probably will make multi-month tops during

the first half of January. Sentiment indicators are flashing warning

signs, but breadth indicators are saying that the coming decline will be

limited to around 10%.

4) The T-Bond is at risk of downward

acceleration over the coming month or two, but regardless of what happens

in the short-term there's a good chance that major price weakness will be

seen in 2020. In other words, it looks like higher interest rates are on

the way.

5) We expect the oil price to trend upward over the next

12 months, but the stage is now set for a multi-month price high in

January.

6) We are holding a cash reserve of 25%-30% and are

looking for opportunities to increase this reserve.

TSI Schedule

Reminder

This is the third week in a row

that we will not be doing an Interim Update, but thereafter we will be

back to our usual two reports per week format.

Revisiting the

Fed's potential game-changer

Over the past four months the

Fed has added about $400B to its balance sheet. To put this into

perspective, since early September the Fed has expanded its balance sheet

at an annualised rate of around 30%. According to the Fed, the purpose of

this dramatic monetary expansion was to address a temporary liquidity

issue in the "repo" market. The question is: If the Fed is dealing with

only a temporary shortage of liquidity in the market for short-term money,

why did it introduce a program in mid-October to supplement the temporary

injections of "repo" money with $60B/month of permanent money?

The

answer is that the Fed is dealing with something more than a temporary

shortage of liquidity in the market for short-term money. The fact that

the Fed sees the need to remove $60B/month of Treasury supply from the

market in addition to the Treasury supply that is being removed on a

temporary basis via "repo" operations implies that the overall demand for

Treasury debt is falling short of Treasury supply at the Fed's targeted

interest rates. Looking from a different angle, it is clear that at

current interest rates the global financial system wants more dollars and

less Treasury debt. The Fed is accommodating this desire by increasing the

supply of dollars to the market and reducing the supply of government debt

that must be absorbed by the market.

The key phrase in the above

paragraph is "at current interest rates". If the supply of and the demand

for money and credit were permitted to balance naturally then interest

rates would now be much higher. However, the Fed doesn't want supply and

demand to strike a natural balance; the Fed has decided that it wants the

price of credit at a certain level and that it will use its power to

create and destroy money to override natural market forces. In this regard

the current situation is unusual only in degree, because the Fed has been

attempting to override market forces for more than 100 years.

The

US Federal government is not about to slow the pace at which it emits new

debt. On the contrary, the rate of growth in government debt supply looks

set to rise. Therefore, one of two things will have to happen if interest

rates are to stay near current low levels: The Fed will have to keep

absorbing Treasury supply at a rapid pace or the market's desire to hold

Treasury debt will have to increase substantially. The latter could occur

in response to a sizable decline in the US stock market or a crisis

outside the US.

Within a week of its mid-October announcement we

wrote that the Fed's promise to inject $60B/month of new 'permanent' money

was a potential game-changer, in that it could extend the current cycle

(prolong the equity bull market) and lead to more "price inflation" than

earlier programs. We continue to think that a cycle extension could be on

the cards, but if so the recession warnings that were generated by leading

indicators during the second half of last year must disappear within the

next couple of months.

US Recession

Watch

Our favourite leading indicators

of US recession are the ISM New Orders Index (NOI), Real Gross Private

Domestic Investment (RGPDI) and the yield curve. Subsequent to our last

discussion of US recession risk the only new information worth mentioning

is an updated NOI (the latest ISM Report was published last Friday).

As mentioned previously, the NOI occasionally generates a false

recession warning. When the signal proved to be false in the past, for

example, in March-April of 2003, the move below the recession line (the

red line on the following monthly chart) was marginal and quickly

reversed. By the same token, when the signal proved to be correct the

initial break below the recession line was followed by a significant

extension to the downside.

Since issuing a recession warning the

NOI has chopped around near the red line, meaning that the signal is

intact. In this respect nothing has changed over the past month. However,

time is running out for the NOI to invalidate its recession warning.

The situation now is similar to what it was a month ago, in that all

three of our favourite leading indicators are warning of recession.

Based on the latest data, our rough estimates of recession start-time

probabilities are:

- H1-2020: 60% (unchanged from a month

ago)

- H2-2020: 20% (unchanged from a month ago)

-

Later than 2020: 20% (up from 10% a month ago).

Note that even if

the US economy doesn't slide into recession anytime soon, the weakness

over the past several months in the ISM NOI suggests that some coincident

economic statistics will continue to deteriorate during the first few

months of 2020. Industrial production is an example.

Also note that

the Fed's recent actions are why 2020 recession risk is skewed towards the

first half of the year. If the Fed's actions are too little too late to

prolong the monetary-inflation-fueled boom, then a recession should get

underway before the middle of this year. Alternatively, if the Fed has

done enough to prolong the boom then a recession probably won't get

underway until 2021.

The Monthly (and Yearly)

Closing Prices

At around this time every month

we review some of the most important (from our perspective) monthly

charts. We do this because monthly closing prices can confirm or deny

intermediate-term trend changes. For December-2019 we'll review the

monthly closes for gold, GDX, the HUI, the S&P500 Index (SPX) and the

T-Bond.

As stated in earlier commentaries, critical monthly-closing

support for gold's intermediate-term upward trend is defined by the

8-month MA. That is, a monthly close below the 8-month MA would confirm

that an intermediate-term top (a top that holds for 6-12 months or longer)

is in place. The following monthly chart shows that this MA was tested in

each of the past two months and has risen to $1460.

We expect that

there will be another test of the 8-month MA during the first quarter of

this year, most likely following a January spike to a new multi-year high.

Note that a monthly close above resistance at $1570 would point to a

test of the 2011 major peak.

GDX and the HUI completed 2-3 month corrections in November and then

resumed their upward trends. They are in different positions on the

monthly chart, though, because the HUI made a new multi-year high in

December whereas GDX has stayed well below its August-2019 high.

Although the chart patterns suggest that the 2016 highs will be tested

prior to an intermediate-term peak, there are reasons to be cautious about

the gold sector's 2-4 month prospects. One reason is the 1980s comparison,

which projects a substantial decline from a January top.

The SPX's price action during the period since September-2018 still

looks similar to the price action that followed the intermediate-term top

in 2011. The similar periods are indicated by the red boxes drawn on the

following monthly chart.

For the post-2011 similarity to be

maintained, the 12-month MA should not be breached on a monthly closing

basis for a long time to come. This is not what we expect, but clearly the

long-term US equity bull market was intact at the end of December-2019.

That's despite the complete lack of earnings growth over the past year and

the high risk that the US economy will slump into recession in 2020.

A monthly close below the 12-month MA (currently at 2938 and rising)

would be the first clear sign on the monthly chart that the bull market is

over.

The T-Bond rocketed up to a top in August-2019 and then fell during

each of the ensuing four months. It is tracing out a long-term top.

The Stock Market

On 27th December a US contractor

was killed in Iraq by a rocket attack that the US blamed on an Iran-backed

Iraqi militia called Kataeb Hezbollah (KH). In retaliation, on 29th

December the US launched airstrikes in Iraq that killed 25 KH fighters. In

retaliation, on 31st December the US embassy in Iraq was attacked by KH

supporters. In retaliation, on 2nd January the US launched a drone attack

in Iraq that killed a high-profile Iranian general, prompting the threat

of harsh retaliation from the Iranian government.

There is a risk

that the sequence of retaliatory actions will spiral out of control and

lead to outright war, but according to the stock market it is a

low-probability risk. We know that's the stock market's assessment because

on 3rd January, in response to the news of the US attack that killed the

Iranian general and the Iranian government's promise to seek a "forceful

revenge", the SPX didn't even fully retrace the preceding day's advance.

The reaction to last week's bearish news was remarkably mild

considering that the market is both 'overbought' in momentum terms and

'overbullish' in sentiment terms (the dangerous sentiment situation was

discussed in our previous two Weekly Updates). In fact, Friday's pullback

is barely noticeable on the 1-year daily SPX chart displayed below. This

implies that a short-term top has not been signaled yet.

The lower section of the above chart shows the NYSE Advance-Decline

Line (ADL). The ADL made a new all-time high last Thursday and then

dropped a little on Friday.

The US stock market has never commenced

a bear market with the ADL at/near an all-time high, but the ADL's

strength does not preclude a correction of up to 10%. We are anticipating

a correction of up to 10% from a January high.

It's still the case

that the obvious lack of strength in the Dow Transportation Average (TRAN)

is the only noteworthy bearish divergence or non-confirmation. As

illustrated below, the TRAN remains below its early-November high and

continues to trade in a lacklustre manner.

The concluding comment from the Stock Market discussion in the

previous Weekly Update remains applicable. Here it is again:

"It

would be reasonable to accumulate new or add to existing bearish

speculations over the coming fortnight. These speculations could take the

form of put options with expiry dates of March-2020 or later that are

5%-10% out of the money, or bear funds such as QID."

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Jan-06 | No important events scheduled |

| Tuesday Jan-07 |

ISM Non-Mfg Index International Trade Balance Factory Orders |

| Wednesday Jan-08 | Consumer Credit |

| Thursday Jan-09 | No important events scheduled |

| Friday Jan-10 | Monthly Employment Report |

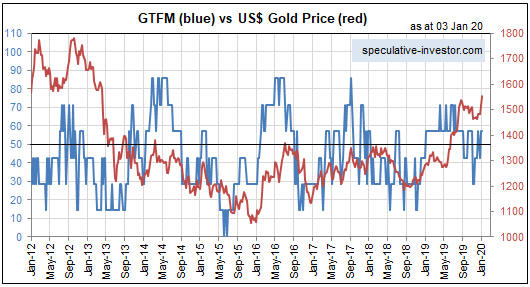

Gold and the Dollar