![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 6th February 2017

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in early-2015, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020. (Last update: 29 June 2015)

A secular BEAR market in the US Dollar began during the final quarter of 2000 and ended in July of 2008. This secular bear market will be followed by a multi-year period of range trading. (Last update: 09 February 2009)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak sometime between 2018 and 2020. (Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

|

Market |

Short-Term (1-3 month) |

Intermediate-Term (6-18 month) |

Long-Term (2-5 Year) |

| Gold | N/A |

Neutral (21-Nov-16) |

Bullish |

| US$ (Dollar Index) | N/A |

Neutral (17-Aug-16) |

Neutral (19-Sep-07) |

| US Treasury Bonds (TLT) | N/A |

Neutral (21-Nov-16) |

Bearish |

| Stock Market (DJW) | N/A |

Neutral (14-Nov-16) |

Bearish |

| Gold Stocks (HUI) | N/A |

Neutral (21-Nov-16) |

Bullish |

| Oil | N/A |

Neutral (26-Oct-15) |

Bullish |

| Industrial Metals (GYX) | N/A |

Neutral (10-Oct-16) | Bullish |

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

Loosening is the new tightening

A pro-business government does NOT lead to a stronger stock market

Summary of current

thinking/positioning

1) Thinking that the financial

world is heading for an important February-March turning point involving a

correction low in the US$ and highs in equity and commodity markets.

2) Thinking that the short-term rallies in gold, silver and the

associated mining indices are not yet complete.

3) Expecting

intermediate-term tops in non-gold commodities and the associated equities

later this quarter. Looking for profit-taking opportunities, but planning

to maintain some long-term exposure to relatively low-risk stocks. Hedged

via EEM and USO put options.

4) Thinking that the US Treasury Bond

has significant additional short-term upside (within a long-term bearish

trend).

5) Expecting an extension of the US equity bull market and

expecting a generally-bullish global equity trend. Concerned about

short-term downside risk, but acknowledge that a significant correction

might not begin before March.

6) Thinking that the Dollar Index is

immersed in a 2-3 month correction, after which its longer-term upward

trend will resume.

7) Maintaining a large cash reserve to hedge

downside risk in equities (current cash percentage is about 35%).

US Recession

Watch

The latest iteration of the

monthly ISM Manufacturing New Orders Index (NOI) was reported last

Wednesday. This is the most reliable short-term leading indicator of US

recession, which is why it is one of the few economic numbers we pay

attention to and regularly discuss at TSI.

The latest NOI (the

number for January-2017) was almost identical to the previous NOI (the

number for December-2016), meaning that it remains at a 2-year high and

well above the level it would have to drop below (the red line on the

following chart) to warn of an imminent start to a recession. The message,

in a nutshell, is that the US economy is expanding and will probably keep

doing so for at least a few more months.

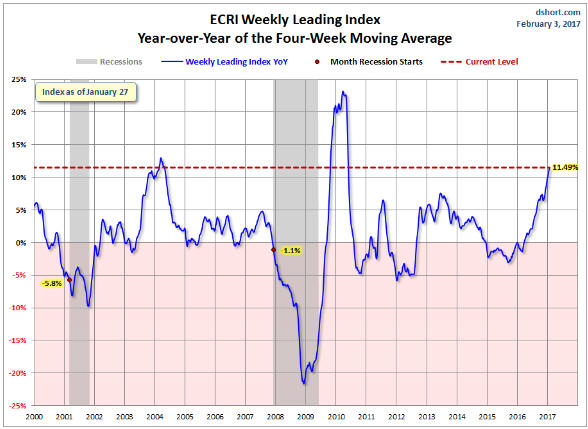

Although it is not one of our primary economic indicators, the Weekly

Leading Index (WLI) calculated by the Economic Cycle Research Institute

(ECRI) is worth mentioning because its growth rate is now at one of the

highest levels of the past 15 years. The situation is illustrated below.

Chart Source:

Doug Short

Taking into account the ISM Manufacturing NOI, the

ECRI's WLI and the upward reversal over the past two quarters of Real

Gross Private Domestic Investment (RGPDI), we now think that the

probability of a US recession beginning during the first half of 2017 is

close to zero. This is consistent with our assessment that the fundamental

backdrop remains bearish for gold and conducive to relative strength in

industrial commodities.

Monetary

Inflation Update

From a practical

investing/speculating standpoint the most useful money-supply indicator is

the combination of US$ and euro supply, a monetary aggregate that we call

"G2 True Money Supply (TMS)". We created G2 TMS in response to what

happened during 2005-2006, when accelerating monetary inflation in the

euro-zone delayed the end of an economic boom in the US.

The global

booms that ended in 2000 and 2006-2007 did so a few months after the G2

monetary inflation rate dropped below 6% (the red line on the following

chart). We therefore view 6% as a boom-bust demarcation level.

The

following chart's overarching message is that the current investment booms

are yet to run out of monetary fuel, although there was an interesting

down-tick in December (the latest month for which data is currently

available). The down-tick will shift from interesting (a curiosity) to

concerning if it continues and takes the growth rate below last year's low

of 8%.

Commodities

Copper Update

Last week the copper price again reversed downward after probing

resistance in the low-$2.70s. It fell sharply on Friday but managed to

hold above its 50-day MA.

The huge speculative net-long position in

copper futures remains a risk. This risk will eventually materialise,

resulting in a substantial price decline. However, a surge above the

$2.70s and potentially to $3.00 will remain a reasonable short-term bet as

long as pullbacks hold at the 50-day MA.

Platinum Update

The platinum price bottomed

slightly below US$900 in December and has since rebounded to its 200-day

MA. As illustrated by the bottom section of the following chart, platinum

has also rebounded in gold terms.

A near-term pullback to the $950s

wouldn't be surprising and would probably create another good entry point

for either a short-term or a long-term trade.

Platinum is the precious metal with the most bullish intermediate-term

reward/risk ratio. This is partly because despite the rebound of the past

few months it remains very cheap relative to gold. It is also because of

the potential for a supply shortage to develop. There is currently no

evidence of a platinum supply shortage, but as a market that essentially

lives from hand to mouth such a shortage can arise due to a disruption in

the mining industry or unexpectedly-high consumption.

There's a

realistic chance of the platinum price moving up to at least parity with

the gold price over the coming 12 months.

The Stock Market

The US

Valuation Risk

We have generally

been too bearish on the US stock market for about 20 years. Although it

isn't an excuse, we think that the following chart qualifies as a

mitigating factor. The chart was prepared by Ned Davis Research and shows

total stock market capitalisation as a percentage of Gross Domestic

Income. We'll call it the TSMC/GDI ratio.

Notice that apart from a

brief period during 2008-2009, the TSMC/GDI ratio has spent the entire

past twenty years in "bubble territory" and above the 1929 peak.

Furthermore, it's not like there's a particular issue with the TSMC/GDI

ratio that has caused it to paint a distorted picture. Other long-term

valuation indicators have generated similar messages.

As has been clearly demonstrated by the US stock market, an

over-valued market can always become more so and can remain in over-valued

territory for an unpredictably long time. We are therefore not predicting

a collapse to 'normal value' in 2017, but it is still prudent to take the

valuation risk into account. A collapse to the long-term valuation average

or lower WILL eventually happen.

Two influences that could become

catalysts for the start of a major shift back to 'fair value' appear to be

in their early stages of development. The first is an increase in the rate

of "price inflation".

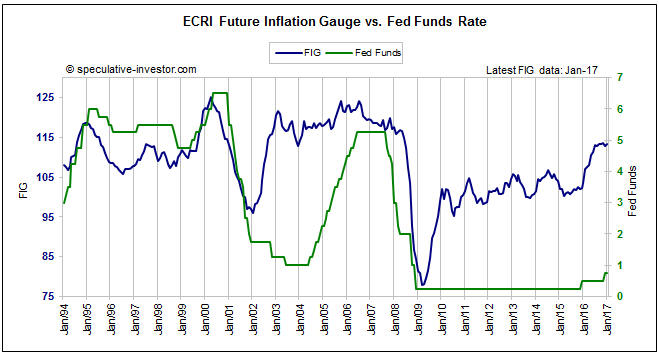

If the ECRI's Future Inflation Gauge (FIG) is

anything to go by (the following chart shows that the FIG has risen

sharply since early last year), the rate of US price inflation as measured

by the CPI will trend upward throughout this year. When the rate of price

inflation is on the rise, the stock market's average P/E ratio tends to be

on the decline.

The second potential catalyst for the start of a major shift back to

'fair value' is "regime uncertainty" in the US.

"Regime

uncertainty" is the name given to the tendency of private investors to

pull back from making long-term financial commitments due to uncertainty

about what the government will do next. According to

an essay

by Robert Higgs, it was one of the factors that prolonged the Great

Depression of the 1930s. Government intervention is generally bad for the

economy, but it tends to be even worse when it happens in an ad hoc way.

It is becoming apparent that government by ad-hoc command is the

method favoured by the new US president, in which case "regime

uncertainty" is likely to rise and the amount that investors are willing

to pay for a dollar of corporate earnings is likely to fall.

We'll

do a TSI blog post about "regime uncertainty" in the next day or so.

Current Market Situation

The

Volatility Index (VIX) has worked itself into a discussion-worthy

position.

The VIX is a much better indicator of stock market

bottoms than stock market tops. This is because the urgency to sell or

hedge invariably spikes after the market has taken a tumble and is nearing

a bottom, whereas stock-market peaks tend to be preceded by prolonged

periods of complacency. This results in a dramatic upward spike in the VIX

as the market approaches a bottom and a tedious downward grind in the VIX

for months or even years prior to a top.

Currently, the VIX is less

than 1 point from a 20-year low. This doesn't necessarily mean that the

stock market is near an important peak, but it almost certainly does mean

that volatility is not going to get significantly lower.

The S&P500, the Dow Industrials and the NASDAQ100 moved back to near

their highs for the year (and all-time highs) on Friday 3rd February. This

simply means that there is no evidence, yet, that any sort of top is in

place. As previously advised, recent divergences between the

aforementioned indices and market internals opens up the possibility that

an intermediate-term peak (a peak that holds for more than 6 months) will

be put in place this quarter.

The stock index with the most

interesting current position is the Dow Transportation Average (TRAN).

This is because its January-2017 close was slightly below its

November-2014 close, leaving the November-2014 close of 9198 as the

monthly closing all-time high.

At this stage we don't know why the

TRAN has been unable to break out on the monthly chart (see below), but

the ability/inability of this index to break out on a monthly basis is

something we'll be paying attention to in the future.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday February 06 | No important events scheduled |

| Tuesday February 07 |

International Trade Balance Consumer Credit |

| Wednesday February 08 | No important events scheduled |

| Thursday February 09 | No important events scheduled |

| Friday February 10 |

Import and Export Prices Consumer Sentiment Treasury Budget |

Gold and the Dollar