![]()

![]()

![]()

![]()

-- Weekly Market Update for 6th May 2019

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bullish (04 Jan 2019) |

| US Equity (SPX) | Bearish (19 Apr 2019) |

| Currency (Dollar Index) | Neutral (15 Mar 2019) |

| Commodities (GNX) | Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

Gold, Commodities, and Bob Moriarty's New Book

Summary of current

thinking/positioning

1) The Dollar Index (DX) held

its upside breakout last week, but the price action kept alive the

possibility of a bearish signal in the form of a failed breakout.

2) Gold, silver and the associated mining indices should begin to rebound

very soon. The coming rebounds probably will be counter-trend reactions

rather than new multi-month upward trends, although a downward reversal in

the DX could lead to tradable strength in the gold sector.

3) The

US stock market and many other stock markets are now very stretched to the

upside on a short-term basis. This should mean that multi-week pullbacks

begin soon, but the intermediate-term rallies probably aren't over.

4) There's a good chance that a large T-Bond decline will commence

before mid-year, possibly following a test of the March high.

5) We

are holding a cash reserve of 30%-35%.

Global Monetary

Inflation Update

Here is our monthly update on

what's happening on the monetary inflation front in a few different

regions/countries.

The G2 (US plus euro-zone) monetary inflation

rate dropped to a 10-year low in March-2019 and has now spent 19 months

below the boom-bust threshold of 6%. Refer to the following chart for

details.

The low rate of G2 monetary inflation stems from the very

low rate of money-supply growth in the US. During March the year-over-year

(YOY) rate of growth in euro supply was 7.6%, which although well down

from a 2014 peak of 14% is still quite high. The rate of growth in US$

supply, however, was only 1.8%.

The slow (by modern standards)

rate of G2 money-supply growth boosts the risk that a global recession

will begin in 2019, but, as noted in the past, the monetary inflation rate

is a long-term indicator that leads economic and financial-market

conditions by amounts of time that can vary substantially from one cycle

to the next. When attempting to predict the start time of the next

recession we therefore rely on other leading indicators, three of which

were discussed in last week's Interim Update.

Australia's monetary inflation rate has picked up a little over the

past few months, but the country remains on the verge of monetary

deflation.

The very slow money-supply growth has had an effect on

Australia's property market, in that over the past 12 months residential

property prices have fallen by an average of 6.9% on a nationwide basis

and 10.9% in Sydney (the largest and most expensive city in Australia).

Refer to the article posted

HERE for more detail.

Actually, the decline to near zero in

Australia's monetary inflation rate is both a cause and an effect of the

slight (to date) deflation of the property investment bubble. Commercial

banks have been making it more difficult for house buyers to obtain

credit, leading to a pullback in prices and a slowdown in the pace at

which new money is created.

In January-2019 the year-over-year (YOY) growth rate of China's M1

money supply dropped to its lowest level since 1989. There was an

insignificant up-tick in February, but the recent attempts by China's

government to promote credit expansion started to 'bear fruit' in March.

Refer to the following chart for details.

We wonder if this is too

little too late to kick-start a new surge in the demand for industrial

commodities.

Hong Kong hasn't escaped the general monetary-inflation slowdown. As

illustrated below, the YOY rate of growth in HK's M2 money supply has

languished near a 10-year low in the 1%-4% range over the past several

months.

Remarkably, HK's low monetary inflation rate is yet to have

a pronounced effect on the world's most expensive real estate. Property

prices dropped in HK during August-December of last year, but they rose in

January and the

majority view is that a rise to new highs is in store.

Due to

the monetary backdrop, we think there's a high risk of a double-digit

decline in HK property prices over the next 12 months.

Almost everyone knows that the Bank of Japan (BOJ) has pumped a huge

amount of money into the Japanese economy, so the lack of "price

inflation" in Japan is something of a quandary. Analysts have let their

imaginations run wild in an attempt to explain this strange set of

circumstances, and the situation in Japan has even been cited as proof

that increasing the money supply doesn't cause prices to rise. However,

anyone who didn't blindly assume that the BOJ's actions were leading to

rapid money-supply growth and instead took the trouble to check what was

actually happening to Japan's money supply would quickly realise that

explaining Japan's lack of "price inflation" requires no stretch of the

imagination. The fact is that Japan's monetary inflation rate over the

past 25 years has been consistent with an "inflation" rate of

approximately zero.

The persistently low rate of monetary inflation

in Japan is illustrated by the following chart. The chart shows that the

YOY rate of increase in Japan's M2 money supply averaged about 2% over the

past 27 years and about 2.5% over the past 10 years. It is currently about

2.4%. Assuming productivity growth of 2%-3%, these money-supply figures

are consistent with a flat general price level.

Note that QE in Japan is different from QE in the US. When the Fed

implements QE it boosts the supply of bank reserves and the supply of

money on a one-for-one basis (bank reserves aren't counted in the money

supply), but the BOJ's QE adds far more to bank reserves than to the money

supply. Note also that the Fed's QE created a lot less "price inflation"

than many people were expecting for the reasons outlined

HERE.

The Japanese economy has benefited from the persistently

slow rate of monetary inflation and the resulting stability of the

currency, but at the same time it has been hurt by the massive diversion

of resources to the government. The net result is an economy that isn't

exactly vibrant, but also isn't that bad.

To summarise the above

information, the pace at which new money is being created around the world

remains unusually slow.

Commodities

The Platinum Group

Metals (PGMs)

In the 8th April Weekly Update we noted that

platinum had finally begun to demonstrate the outperformance justified by

its extremely low price relative to other precious metals. We also noted

that the US$ platinum price was a little stretched to the upside on a

short-term basis and could soon commence a correction, but that

significant additional gains were likely prior to the next multi-month

top.

The price topped at $920 during the next trading day and then

commenced a correction. The correction may have ended at $847 last week.

Ideally (from a bull's perspective) the price will remain above the

20-week MA (the black line on the following chart) on a weekly closing

basis over the next few months.

We think that platinum is a buy in

the mid-$800s.

Turning to another of the PGMs, it is fair to say that the palladium

market was well and truly into bubble territory in March-2019. This is

evidenced by the near doubling of the palladium price over the preceding 7

months and palladium's extremely rich valuation relative to almost all

other commodities.

It's possible that the sharp decline in the

palladium price from its March-2019 high marked the bursting of the

bubble, but as mentioned in the 1st April Weekly Update it's more likely

that the decline is the start of a multi-month correction. This is based

on a comparison with the palladium rally of 1997-2000 and the fact that

the end of the first parabolic move in a cyclical advance generally

doesn't mark the end of the cycle.

If we are dealing with a

multi-month correction rather than the start of a bubble collapse then the

palladium price should not give a weekly close below its 50-week MA (the

blue line on the following chart).

Oil remains in correction mode

The knee-jerk

reaction to the news that the US government was removing waivers on

sanctions against buyers of Iranian two weeks ago pushed the oil price

above resistance at $64-$65 and created at least a multi-week top. The

price has since pulled back to moving-average support at around $61.

The test of the 50-day and 200-day MAs could lead to a price bounce,

but we doubt that the correction is over.

The Oil Services ETF (OIH) has dropped a lot further (in percentage

terms) than the oil price over the past two weeks. Although its correction

probably isn't over, it has almost reached the 'buy zone'.

We think

that OIH would be a good candidate for new buying at $15.50-$16.00.

The Stock Market

The NASDAQ100 Index (NDX) has

risen for 8 weeks in a row and on 18 of the past 19 weeks, which means

that it is immersed in one of the most relentless rallies in its history.

The following weekly chart shows that it has just achieved consecutive

weekly closes above last year's high, so we can be certain that this is

not a bear-market rally. It is an extension of the cyclical bull market

that commenced in 2009.

The S&P500 Index (SPX) has just achieved its first weekly close above

last year's high, but the new high is too marginal to be viewed as a

breakout. It is a test of the 2018 high. However, the NYSE Advance-Decline

Line (ADL), which is shown in the bottom section of the following daily

chart, broke into all-time-high territory almost three months ago and

continues to trend upward.

Prior to last Friday there was a minor bearish

divergence/non-confirmation in the form of the Russell2000's inability to

close above its February-2019 high, but that divergence was eliminated on

Friday. The RUT closed at a new high for the year on Friday, although it

remains well below last year's high.

The relative weakness in the banking sector could be viewed as a

bearish divergence, but we suspect that the Bank Index (BKX) is in the

process of becoming relatively strong. That is, we suspect that the

up-turn in the BKX/SPX ratio from its March low (refer to the bottom

section of the following chart) has staying power. This is linked to our

expectation that long-term interest rates will rise over the next 6-12

months and to bank stocks being attractively valued, on average, relative

to the broad market. Consequently, although it is not a trade we plan to

do we like the idea of simultaneously going long KBE (the Bank ETF) and

short SPY.

This is a topic we plan to revisit within the next

couple of weeks.

Due to the small additional gains made by most US stock indices last

week, the market's position today is similar to what it was a week ago.

Therefore, although the market has shown more near-term resilience than

expected, the following paragraphs from last week's commentary still

apply:

"The US stock market is very 'overbought' on a

short-term basis and moderately 'overbought' on an intermediate-term

basis. Considering the SPX's position relative to major resistance this

probably means that a correction will begin within the next few days,

perhaps following a spike by this index to a new all-time high. Supporting

this conclusion are the recent downward reversals in the oil price and

China's stock market.

The coming multi-week decline could be steep,

but due to the performance of the NYSE Advance-Decline Line it is more

likely to be a correction within an on-going intermediate-term upward

trend than the start of a new intermediate-term downward trend."

Two events could have an influence on how the US stock market trades

over the next few weeks. The first and lesser important of these events is

Uber's IPO, which is scheduled to happen late this week. The IPO a few

weeks ago of Lyft, Uber's main ride-sharing competitor in the US, was a

flop, with the shares now trading about 15% below the IPO price. We

suspect that Uber will perform better post-IPO, but in any case the event

could mark a short-term turning point for the overall market.

The

more important event is the potential US-China trade deal. There's a good

chance that a deal will be signed by presidents Xi and Trump in June,

simply because both men want it to happen.

Anticipation of an end

to the "trade war" was not the main driver of the rally from the

December-2018 low. The main drivers were the Fed's aboutface and the

extent to which the market was stretched to the downside at the time of

the 26th December upward reversal. However, optimism that the

government-imposed restrictions on international trade (and hence on

economic growth) would soon be eliminated or reduced has been a

significant part of the bullish narrative.

We think that the big

event will be the announcement of a specific date for a Xi-Trump meeting

rather than the actual signing of a document confirming the details of a

trade agreement, because once a meeting is scheduled it will be known that

a deal has been done.

If the announcement of a Xi-Trump meeting

happens with the SPX near an all-time high then the knee-jerk reaction to

the news could establish a top that holds for a few months.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday May-06 | No important events scheduled |

| Tuesday May-07 | Consumer Credit |

| Wednesday May-08 | No important events scheduled |

| Thursday May-09 |

Trade Balance PPI |

| Friday May-10 |

CPI Treasury Budget |

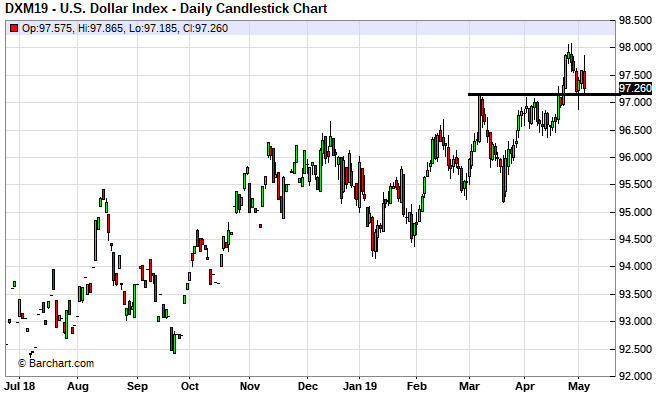

Gold and the Dollar

As mentioned in last week's Interim Update, a sustained break in the

Dollar Index below 97 could spur a more substantial rebound in the

gold-mining sector than currently appears likely.

The

Currency Market

The COT data indicate that speculators, as

a group, are betting aggressively on an extension of the US dollar's

upward trend against most other major currencies, with the biggest bets

being on further weakness in the Swiss franc (SF), the Australian dollar

and the Yen. No market ever reversed course simply because speculative

sentiment became lopsided, but this means that there will be plenty of

fuel to support a downward move in the US$ if the trend reverses for some

other reason.

Last week the DX pulled back to support at 97.0-97.2.

It briefly traded below support on Wednesday in anticipation of a further

'dovish' tilt by the Fed and then rebounded in the aftermath of the Fed's

latest words of wisdom. This price action was slightly positive as it

implied that the preceding week's upside breakout had been successfully

tested, but Friday's price action was slightly negative. On Friday the DX

reversed downward despite a strong Employment Report.

Friday's

downward reversal left the DX precariously poised near support at the end

of the week. Consequently, the potential for a failed upside breakout

still exists.

The Swiss franc (SF) has begun to recover from the 'oversold' extreme

reached during the week before last. As mentioned a week ago, the most

likely path from here is a rebound to the 50-day MA (the blue line on the

following chart) and then a decline that tests or undercuts the April low.

This would set the stage for a longer and stronger rebound.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 3rd May 2019:

Company

news/developments for the week ending Friday 3rd May 2019:

[Note: AISC = All-In Sustaining Cost, EBITDA = Earnings Before

Interest, Tax, Depreciation and Amortisation (a measure of cash flow), EV

= Enterprise Value or Electric Vehicle, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, JV

= Joint Venture, MD&A = Management Discussion and Analysis, M&I = Measured

and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value using a

discount rate of X%, NSR = Net Smelter Return or Net Smelter Royalty, P&P

= Proven and Probable, PEA = Preliminary Economic Assessment, PFS =

Pre-Feasibility Study]

*Alkane Resources (ALK.AX)

published its quarterly report for the March-2019 quarter (the

third quarter of FY2019). The report revealed another above-plan

performance from the Tomingley Gold Operation (TGO), with production of

10.7K ounces at an AISC of A$956/oz. The on-going better-than-expected

performance of the TGO has prompted another increase in FY2019 gold

production guidance. Originally it was 30K-35K ounces, then three months

ago it was boosted to 35K-40K ounces, and now it is 42K-47K ounces. The

company produced 37.4K ounces during the first three quarters of FY2019,

so the expected production during the final quarter is 5K-10K ounces.

The Tomingley open pit is depleted and the current production is

solely from the processing of stockpiles. That's why the amount of gold

produced has been trending downward. However, plans are in place to extend

the life of the operation by developing an underground mine and exploring

for additional resources. Initial production from the underground mine is

on track to begin during the December-2019 quarter and recent drilling

results suggest the potential to establish a new pit within a few

kilometres of the existing plant.

The company's efforts to arrange

financing and offtake agreements for the Dubbo specialty metals project

have continued, but no tangible progress was reported.

ALK has a

strong balance sheet, with no debt and cash, bullion plus listed

investments of A$78.8M. This constitutes a quarter-over-quarter decline of

A$1.7M.

*Clean TeQ (CLQ.AX, CLQ.TO)

published its quarterly report for the March-2019 quarter. The report

stated that the company had cash of A$100M at the end of the latest

quarter, which amounts to a reduction of about A$17M over the course of

the quarter and A$52M over the past three quarters. This means that CLQ

continues to spend rapidly as it ploughs ahead with the front end

engineering and design (FEED) for the Sunrise nickel-cobalt project in New

South Wales, Australia.

The FEED is being done by Metallurgical

Corporation of China Ltd (MCC) and is scheduled to be complete in Q3-2019.

It is envisaged that an output of the FEED will be a fixed price

procurement and construction contract for MCC.

From our

perspective, the key to CLQ's long-term risk/reward is how the US$1.5B

estimated pre-production capex is financed. This will determine whether

the more appropriate course of action is to 'cut and run' or average down.

Ideally, financing will involve a project-level investor along similar

lines to the deal that was done by Kidman Resources (KDR.AX) to fund the

development of its Mt Holland lithium project. We were therefore pleased

to read the following in CLQ's latest report:

"Clean TeQ is

actively engaging with a number of project financiers and potential

offtake/joint venture partners in order to secure an equity financing

package for the project. The drive for end-users to secure high-quality,

long-term supply of nickel and cobalt sulphates remains strong."

*Golden Arrow Resources (GRG.V) published its

financial report for the quarter and year ending 31st December 2018. The

report shows working capital of roughly zero, down by C$2.7M since the end

of the September quarter. It also shows the addition of C$11.2M of

long-term debt due to a US$8M draw-down on the US$10M credit facility

provided to GRG by SSR, its JV partner. This effectively means that GRG

spent about C$14M during the December-2018 quarter.

The large

quarterly cash drain was due to GRG's share of the costs of Puna

Operations Inc. (POI), the JV that is owned 25% by GRG and 75% by SSR

Mining. The JV owns the Pirquitas-Chinchillas silver-lead-zinc project in

Argentina, which was in the process of being ramped up during the

December-2018 quarter.

The Pirquitas-Chinchillas project is now

producing metal at near its design rate, so GRG should now be cash-flow

positive or close to it. Furthermore, GRG raised C$4.7M via an equity

financing during the March-2019 quarter, so the next quarterly report

should contain a stronger balance sheet.

GRG is a leveraged play on

silver and should perform extremely well once the market embarks on a

major rally.

*Cobalt 27 Capital (KBLT.V)

published its financial results for the quarter and year ending 31st

December 2018.

At 31st December the company had no long-term debt,

US$46M of working capital (down from US$50M at the end of the preceding

quarter) and US$200M of undrawn credit. This means that it had US$246M of

available financing.

The latest balance sheet doesn't include the

purchase of Highland Pacific (HIG.AX), the owner of 8.56% of the Ramu

nickel-cobalt mine in Papua New Guinea. The purchase should be completed

by mid-May at a cost of about US$70M, an amount that can be comfortably

funded using KBLT's existing financial resources.

The HIG purchase

will give KBLT part ownership of a profitable mining operation and could

enable the company to start paying dividends.

*Mineral

Resources (MIN.AX), a Western Australia based company that

produces lithium and iron-ore and that provides pit-to-port mining

services, published its quarterly report for the March-2019 quarter (the

third quarter of FY2019).

The highlight of the quarter was a 41%

increase in the amount of iron-ore shipped by the company. This was done

to take advantage of the relatively high iron-ore price.

Also worth

mentioning is that submissions were lodged during the quarter with the

relevant regulatory authorities in Australia and China in relation to

MIN's sale of a 50% interest in the Wodgina Lithium Project to Albemarle

Corporation (NYSE: ALB), the world's largest lithium producer, for

US$1.15B in cash. The sale is expected to be completed before the end of

the 2019 calendar year.

As noted in previous TSI commentaries, the

deal with ALB values Wodgina at A$17 per MIN share. This implies that just

one of MIN's assets is worth more than the company's current market cap.

Separately, MIN upwardly revised its FY2019 EBITDA guidance from the

A$280M-$320M estimate provided last November to A$360M-$390M. The reason

for the improved guidance wasn't mentioned in MIN's press release, but we

assume it has a lot to do with the higher iron-ore price and production.

*Premier Gold (PG.TO) reported the

discovery of high-grade gold mineralization in the first hole drilled at

the McCoy-Cove project's Antenna target. The drilling was funded by

Barrick Gold (GOLD) as part of an earn-in obligation (GOLD can earn 60% of

the project by spending US$22.5M on exploration).

The discovery

hole contained a 118.9m intercept grading 4.12 g/t gold. Furthermore, the

drill hole was lost at a depth of 725.4m in mineralisation grading 5.59

g/t Au. Barrick liked this result enough to exercise its option to become

the operator of the joint venture.

This is obviously very good

news.

Separately, PG reported March-quarter gold production from

its Mercedes mine (Mexico) of 17.6K ounces. According to the company, this

is in line with its plan. Annual production guidance of 75K-85K ounces of

gold has been maintained.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI

stock selections the best candidates for new buying at this time, listed

in alphabetical order, are:

1) AAU (last Friday's closing price:

US$0.51)

2) KBLT.V (last Friday's closing price: C$4.17)

3)

PG.TO (last Friday's closing price: C$1.60)

4) SBB.TO (last

Friday's closing price: C$1.02)

5) TK.V (last Friday's closing

price: C$0.33)

The above list is limited to five stocks. It

sometimes will contain less than five, but it never will contain more than

five regardless of how many stocks are attractively priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.barchart.com/