--

Weekly Market Update for the Week Commencing

6th August 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in mid-2016, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. A major decline in government bond prices will

unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom

in 2020 or later.

(Last update: 11 September 2017)

A cyclical BEAR market in the

US

Dollar

began in 2016-2017.

(Last

update: 11 September 2017)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak in 2020

or later.

(Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

|

Market |

True Fundamentals Model (TFM) |

|

Gold (US$ Price) |

Bearish (20 Jul 2018) |

|

US Equity (SPX) |

Bearish (29 Jun 2018) |

|

Currency (Dollar Index) |

Bullish (27 Apr 2018) |

|

Commodities (GNX) |

Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

Have the Chinese pegged the gold price?

Summary of current

thinking/positioning

1) Despite numerous attempts,

the Dollar Index (DX) has failed to close above resistance at 95. This

leaves us expecting a DX decline to 92 and a euro rally to 1.20 within the

next 1-2 months.

2) There is a good set-up for counter-trend

rallies in the gold and silver markets, but upward reversals have not been

signaled. This leaves the door open to new 2018 lows prior to meaningful

rallies getting underway.

3) The gold-mining indices extended their

downward trends into August, but are yet to experience a capitulation.

This creates the risk that a speculative capitulation lies ahead. We have

substantial exposure to the gold-mining sector and have hedged against

this short-term risk via GDX put options.

4) There are numerous

divergences within the US stock market. With monetary conditions

tightening, the short-term downside risk appears to be high.

5)

Most industrial commodities probably will remain in correction mode for

another 1-3 months.

6) The T-Bond price should have an upward bias

(meaning: the T-Bond yield should have a downward bias) for at least the

next two months.

7) We are holding a cash reserve of around 30% and

looking for opportunities to build up this reserve.

The Fed, the

yield curve and "inflation"

The following chart shows that

over the past fortnight the 10yr-2yr yield spread came within 0.24% of

zero. This means that the US yield curve recently came within 0.24% of

inverting. Based on speeches made over the past couple of months we know

that senior Federal Reserve officials are worried that the yield curve

will soon invert.

The Fed's senior people are obviously aware that the yield curve has

inverted prior to recessions in the past and are concerned that an

inversion would bring on the next recession. Therefore, at some point over

the next few months the Fed may take actions designed to steepen the yield

curve. If so, will this reduce the risk of recession?

The answer is

yes and no. The Fed could reduce the risk that a recession will begin in

2019, but only by setting the stage for an even more painful economic

decline to begin in 2020. Also, the Fed representatives who are concerned

about the historical relationship between yield-curve inversion and

recession are assuming that correlation implies causation. However, a

yield curve inversion has never been the cause of a recession. A yield

curve inversion is just a symptom that a credit-fueled boom is 'long in

the tooth'. The boom itself is the cause of the bust and it's the reversal

of the curve from flattening to steepening that signals the death of the

boom.

That being said, at this point a reversal in the US yield

curve from flattening to steepening would be a reliable signal that the

boom is over only if it were driven by the market. If, instead, it were

driven by the Fed, for example, by the Fed prematurely ending its

rate-hiking due to fear of a yield-curve inversion, then it more likely

would be a signal that the boom was going to enjoy a 'final fling'. In

this case, the final fling would involve rising inflation expectations --

gradually at first and then rapidly.

When we look at the 10-year

and 2-year T-Note yields individually it isn't hard for us to imagine the

US yield curve becoming inverted within the next few months. In

particular, the 10-year T-Note yield appears to be completing a short-term

topping pattern on the chart (see below) at a time when speculators in

10-year T-Note futures have a record-high net-short position (meaning:

there is presently a record-high speculative bet that the yield will

rise). The combination of the chart and speculative positioning suggests

the short-term potential for the 10-year yield to pull back to 2.5%-2.6%.

At the same time, the 2-year T-Note yield remains in a strong upward

trend (see below), and with the Fed set to increase its targeted overnight

interest rate to 2.00-2.25% in September there does not appear to be much

short-term downside potential.

If the 2-year yield stays where it is and the 10-year yield achieves

the objective suggested by its short-term topping pattern, then the US

yield curve will invert. This could happen within two months.

Based on what has been said by several Fed officials, an inversion of the

yield curve likely would provoke some panic within the halls of the

central bank that would manifest initially as a temporary cessation of the

rate-hiking program. Therefore, it's very possible that the September rate

hike will be the last rate hike for many months.

If the Fed signals

the temporary cessation of its rate-hiking program within the next two

months the likely consequences would include a small decline in rates at

the short end of the curve and, in response to higher inflation

expectations, the start of a multi-quarter upward trend in rates at the

long end of the curve. In other words, it's likely that the Fed would set

in motion a substantial steepening of the yield curve driven by rising

inflation expectations.

The metals

'correction' continues

Only the commodity markets will

be adversely affected by the reduction of international trading and

economic growth that will result from the protectionist measures and

counter-measures that have been implemented or are under consideration. At

least, that's the message from the market action of the past two months.

During this period the industrial metals markets were pummeled while stock

markets were calm.

For example, the copper market completed a

deceptive intermediate-term topping pattern in early-June and then tanked.

It appears to be on its way to major support near US$2.50, with or without

an intervening rebound to test resistance in the mid-$2.90s.

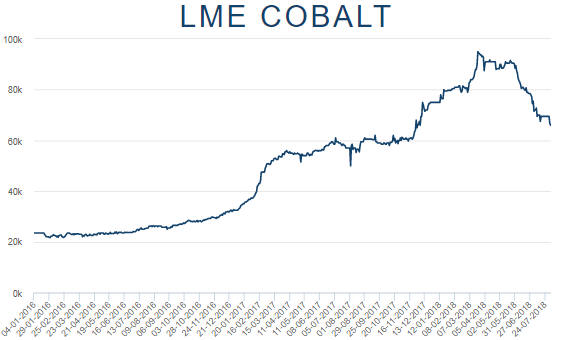

For another example, the cobalt price ran up to a high in March,

leveled off for about three months and then plunged over the past two

months. It is now down by about 30% from its Q1 high.

We think that this year's price declines in copper, cobalt and most of

the other important industrial metals are intermediate-term corrections

within major bullish trends that will resume before year-end. The major

bullish trends are powered by a very compelling fundamental story in the

form of exponential growth in EV production and by the likelihood that the

Fed will veer off its monetary tightening course at early signs of

trouble. Until recently we thought that it would be a sizable stock market

decline that pushed the Fed off its tightening course, but it is beginning

to look more like a yield curve inversion will be the disruptive force.

The Stock Market

Tesla Update

When it comes to Tesla (TSLA), the bad news is always the actual

results of the business while the good news is always what the company's

CEO promises the business will achieve in the future. In the minds of the

many diehard TSLA bulls, it's irrelevant that these promises have usually

amounted to nothing in the past.

It was the same story last week.

The company announced that it had made a record-breaking quarterly loss of

US$717M and burned through about $700M of cash during the latest quarter,

but the stock price rocketed upward following this news because Elon Musk

was polite to analysts on the conference call and promised that future

quarters would be profitable.

Perhaps TSLA will be able to report

positive net earnings for a quarter or two, but it will take a lot more

than a shift to nominal profitability to justify the company's $64B

enterprise value. Also, even if TSLA is able to sort out its manufacturing

issues and begin producing more cars at a lower cost per car, it is about

to a) lose the benefit of the tax credit that encouraged a lot of the

early Model 3 purchases and b) face a rapid rise in competition from the

likes of Volkswagen, BMW, Mercedes, Jaguar, Audi and Porsche.

It's

extremely improbable that TSLA will ever sell enough vehicles with a

sufficient profit margin to justify its current market valuation.

Bankruptcy is a far more likely outcome. However, a large herd of

investors remains committed to the TSLA story and prepared buy/hold

regardless of valuation. At the same time, the stock's downside risk is

well known and, as a result, TSLA is the most 'shorted' stock in the US

market.

Due to the large number of shares sold short there are

periodic bursts in the stock price fueled by short covering. As

illustrated by the following weekly chart, such a burst occurred last

week. Almost all of last week's 17% gain occurred on the day after the

announcement of the record quarterly loss.

We may attempt another

bearish TSLA speculation in the future, but at the moment we have this

stock in the 'too hard basket'.

Current Market Situation

The S&P500 Index

(SPX) reversed course after touching its channel top during the week

before last, but last week it returned to the vicinity of its July high.

The top of its rising channel now coincides with the January high, meaning

that there is now a confluence of resistance at around 2875. This

resistance may be tested within the next few days, but it shouldn't be

exceeded on a daily closing basis and mustn't be exceeded on a weekly

closing basis if we our overarching market view is correct.

The NASDAQ100 Index (NDX) has been stronger than the SPX over the past

few months, but, as mentioned in last week's Interim Update, is closer

than the SPX to confirming a downward reversal. That's because it would

have to do no more than close below last Monday's low of 7158 to suffer a

potentially significant downside breakout.

The upshot is that the US stock market has large short-term downside

potential, but the potential is yet to be confirmed by the price action.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday Aug-06 |

No important events scheduled |

|

Tuesday Aug-07 |

Consumer Credit |

|

Wednesday Aug-08 |

No important events scheduled |

|

Thursday Aug-09 |

PPI |

|

Friday Aug-10 |

CPI

Federal

Budget |

Gold and the Dollar

Gold

The Fundamentals

When most market

analysts state whether the fundamental backdrop is bullish or bearish for gold,

they are stating their opinion and their opinion is most likely based on gut

feel. They have no way of objectively quantifying the fundamental situation.

Instead, they look around and come to a conclusion based on what they see.

The most obvious problem with this approach is that any conclusions will be

strongly influenced by personal biases. Another problem is that the fundamental

drivers of the gold price aren't statistics such as the money supply and the

amount of government debt, but the general PERCEPTIONS of what these statistics

mean for economic growth, the financial system, "inflation" and interest rates

in the future.

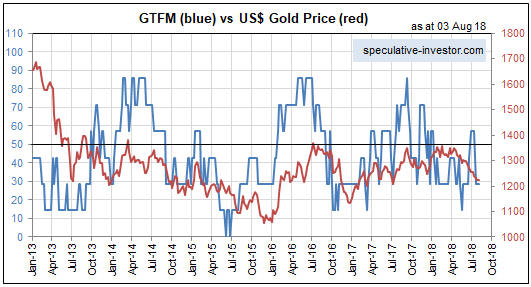

Our Gold True Fundamentals Model (GTFM) is not influenced

by our personal biases. The Model's output is what it is, regardless of what we

think of the economic and financial-market situations. Also, the Model's inputs

are largely based on how market participants collectively view the economic and

financial-market situations. For example, we may very well think that the

economy is 'skating on thin ice', but if credit spreads are very narrow then we

know that our view is an outlier and that economic perceptions are not

supportive of the gold price.

When constructing the GTFM we considered --

based on the general idea that gold's value is the reciprocal of confidence in

the financial system and the economy -- what should be the main influences on

the gold price. This gave us a list of potential price drivers. We then tested

each of these potential drivers against the price data to confirm that there was

a significant correlation. For example, it can be shown that there is a strong

and consistent relationship between the TIPS yield and the US$ gold price and

between credit spreads and the US$ gold price, but no consistent relationship

between the US$ gold price and either the CPI or the level of federal government

debt. The result was a list of seven factors whose inclusion in a gold model was

justified both logically and empirically.

The GTFM is sensitive to shifts

in the fundamental backdrop. This makes it quick to signal significant new

trends, but also makes it susceptible to being 'whipsawed'. For example, it got

whipsawed between late-June and mid-July of this year when it went from bearish

to bullish and back to bearish. It will continue to get whipsawed from time to

time, but over the past 15 years the intermediate-term trends in the gold price

have always been consistent with where the GTFM has spent the bulk of its time.

The GTFM remained in bearish territory last week.

In

the short term, the most likely cause of a positive shift (from gold's

perspective) in the fundamental backdrop is a T-Bond rally combined with a

decline of at least a few percent in the S&P500 Index. However, looking beyond

the next few months we can envisage a very gold-bullish fundamental backdrop

emerging on the back of rising US inflation expectations. Rising inflation

expectations are bullish for gold to the extent that they reduce real interest

rates, steepen the yield curve and weaken the US$.

A substantial rise in

inflation expectations probably won't be a factor in the financial markets over

the remainder of this year, but it could be the most important factor during

2019-2020.

Sentiment

There won't

be something more than a short-term rebound in the gold price until the GTFM

makes a sustained shift into bullish territory. However, the sentiment backdrop

is now very supportive of the gold price, so the next short-term rebound should

be strong.

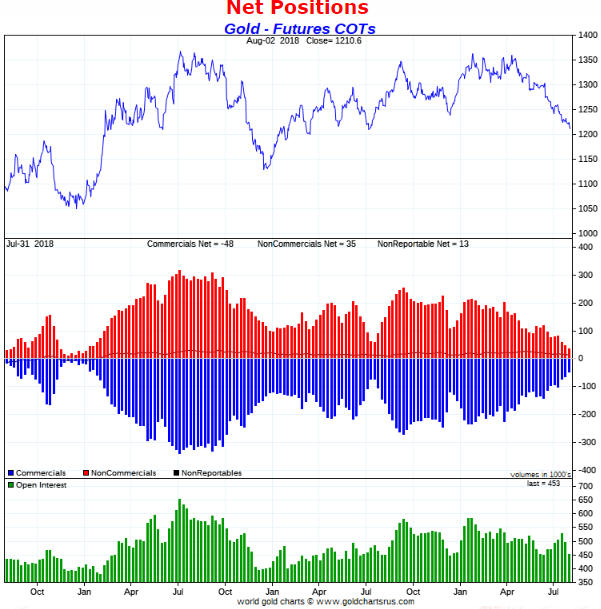

A week ago we wrote: "The COT situation is supportive, but

not decisively so because the open interest in gold futures is too high.

Important lows in the gold price tend to go with relatively low open interest."

As illustrated by the green bars in the bottom section of the following

chart, there was a significant decline in the gold futures open interest (OI)

last week. We now have OI in the bottom third of its 3-year range and the total

speculative net-long position at its lowest level since early-2016.

Consequently, for the first time this year the COT situation is decisively

supportive of the gold price.

As illustrated by the chart included in last week's Interim Update, the

Consensus-inc sentiment survey is also decisively supportive.

The upshot

is that sentiment is now a strong tail-wind for the gold price.

The Price Action

The US$ gold price

tested its July low last Friday and then rebounded. The price action was

slightly bullish, but a reversal has not been signaled yet.

The following

paragraph from last week's commentary remains applicable:

"Until an

upward reversal is signaled via a daily close above $1240 there will be a risk

of a final decline to a new 12-month low. As illustrated by the following daily

chart, no upward reversal has been signaled yet. A decline to a new low probably

would take the form of a downward spike to the $1190s, but there's a risk of a

larger decline. The most likely catalyst for a larger decline would be an upside

breakout in the Dollar Index."

Summing up, in the gold market we have unequivocally bearish fundamentals,

unequivocally bullish sentiment, and price action that could be either a base

(an upward reversal in the making) or a consolidation within an on-going

decline. The sentiment situation could enable a sizable ($100+) short-term

rebound even if the fundamentals remain bearish, but until an upward reversal is

signaled there will be a high risk of a decline to new 12-month price lows.

Silver

Relative to support/resistance, the US$

silver price is in a very similar position to the US$ gold price. Like gold,

silver recently broke below intermediate-term support defined by its

December-2017 low. Also like gold, silver tested its July low last Friday and

then rebounded.

Unlike the situation in the gold market, current sentiment in the silver market

does not constitute a strong tail-wind for the price. In fact, thanks to

persistent optimism on the part of the dumbest money (the "NonReportable"

traders) and the relatively high open interest in silver futures, silver's

current COT situation is no better than neutral. However, the silver price

almost certainly will rebound when the gold price rebounds.

Gold

Stocks

Both the HUI and GDX (the Gold Miners ETF) ended the week

before last at major support levels, prompting us to write:

"The

gold-mining sector has reached a critical juncture. The indices/ETFs will either

hold support near their current levels and soon commence 2-4 month rallies OR

break below support and accelerate downward. The former outcome has the higher

probability, but due to last week's decline in the HUI/gold ratio and the fact

that the bullion market hasn't generated any evidence of a bottom we should be

prepared for the possibility that the latter outcome will happen."

Last week support held, but there was no rebound to speak of so the situation is

virtually unchanged. The gold-mining sector remains at a critical juncture.

The following daily chart shows that the lateral support level currently

being tested by GDX has been tested numerous times over the past 18 months. When

a support level has been tested this many times it usually will have to be

breached prior to the start of a substantial rally. This is because the

capitulation that happens in reaction to the violation of the obvious support

'clears the decks'. Therefore, ideally there will be a brief plunge by GDX to

well below $21 in the near future.

In the absence of a 'deck clearing'

plunge the best that we probably will get from GDX is a 1-3 month rebound to

$23-$25.

The Currency Market

Perhaps not surprisingly, the Dollar

Index (DX) is in the opposite situation to gold. Whereas the gold market is

facing bearish fundamentals and bullish sentiment, the DX is facing bullish

fundamentals and bearish (dangerously optimistic) sentiment.

The bullish

fundamental backdrop for the DX is due to the strength in US equities relative

to European equities and the expanding gap between US and European interest

rates (specifically, the increase in the US 10-year government bond yield

relative to the German 10-year government bond yield).

Regarding

sentiment, the following chart shows that over the past 10 years all of the

major peaks in the Consensus-inc bullish sentiment for the DX were in the

75%-80% range and that at the end of the week before last the DX's bullish

sentiment was 75%.

Last week the DX stayed inside its "rising wedge" and again failed to

achieve a weekly close above lateral resistance at 95. For details refer to the

daily chart displayed below. This week it could trade as high as 95.5 while

remaining within its "wedge", but it shouldn't give a weekly close above 95 if

we are dealing with a topping pattern rather than a mid-trend consolidation.

Interestingly, the following weekly chart shows that over the past 10 weeks

the DX has repeatedly risen to its 200-week MA (the blue line) without managing

to achieve a weekly close above this MA. It should continue to hold below its

200-week MA if we are dealing with a topping pattern.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 3rd August 2018:

Company

news/developments for the week ending Friday 3rd August 2018:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, MD&A = Management

Discussion and Analysis, M&I = Measured and Indicated, NAV = Net Asset Value,

NPV(X%) = Net Present Value using a discount rate of X%, NSR = Net Smelter

Return, P&P = Proven and Probable, PEA = Preliminary Economic Assessment, PFS =

Pre-Feasibility Study]

*Blackham Resources (BLK.AX)

published its quarterly activities and cash-flow reports for the June quarter.

Given that the company had announced its production results and net debt level

about two weeks earlier, the most important information in these reports was

already known.

The only new information of real interest to us was the

section titled "Controlled Placement Agreement". This section contained the

following:

"During July 2018, the Company entered into a Controlled

Placement Agreement (CPA) with Acuity Capital. The CPA provides BLK with up to

$10 million of standby equity capital over the coming 29 month-period.

Importantly, Blackham retains full control of all aspects of the placement

process, having sole discretion as to whether or not to utilise the CPA, the

quantum of shares issued, the minimum issue price of shares and the timing of

each placement tranche (if any). There are no requirements on Blackham to

utilise the CPA and Blackham may terminate the CPA at any time, without cost or

penalty. If Blackham does decide to utilise the CPA, Blackham is able to set a

floor price (at its sole discretion) and the final issue price will be

calculated as the greater of that floor price set by Blackham and a 10% discount

to a Volume Weighted Average Price over a period of Blackham's choosing (again

at the sole discretion of Blackham)."

This means that BLK's

management has given itself the flexibility to raise money (up to A$10M) by

selling new BLK shares in the stock market over the next 29 months at whatever

price it deems appropriate.

We view this news as negative, because the

"CPA" makes it easy for BLK's management to dilute the stock.

*Premier

Gold (PG.TO) reported drilling results from the Rey de Oro deposit (a

zone that will be brought into production this year) at its Mercedes gold-silver

mine in Mexico. The drilling confirmed the extension of a high-grade vein system

and included some excellent intercepts, with the best one being 36.65 g/t Au and

171.30 g/t Ag across 21.95 metres in Hole UG-R018-006.

This is obviously

good news.

Also in the good news department, PG advised that after a poor

first half production performance by the Mercedes mine, production is now

increasing as planned with July being the best month so far in 2018.

*Tinka Resources (TK.V) reported drilling results that extend

the high-grade zinc mineralisation at the company's Ayawilca project in Peru. It

appears that there are substantial widths of high-grade zinc below the

currently-defined resource and also that it will be possible to connect the

200m+ gap between mineral resources at the West and Central Ayawilca deposits.

This is good news. The Ayawilca deposit is already of sufficient size

and grade to be of interest to a large industrial-metals mining company and

looks set to get even better.

List

of candidates for new buying

From within the ranks of TSI stock

selections the best candidates for new buying at this time, listed in

alphabetical order, are:

1) AAU (last Friday's closing price: US$0.66)

2) CNL.TO (last Friday's closing price: C$3.74)

3) PG.TO (last

Friday's closing price: C$2.50)

4) PRQ.TO (last Friday's closing price:

C$0.93)

5) SBB.TO (last Friday's closing price: C$1.46)

The above

list is limited to five stocks. It will sometimes contain less than five, but it

will never contain more than five regardless of how many stocks are attractively

priced for new buying.

Osisko

Gold Royalties Warrants (TSX: OR.WT) added to the TSI List at C$1.05

Osisko Gold Royalties (OR, OR.TO) is like a hedge fund that invests in

gold/silver royalties, gold/silver streaming deals and junior gold/silver mining

stocks. Its current market cap is around C$1.9B, as is its book value.

We

previously wrote that the OR warrants (OR.WT on the TSX) would be added to the

TSI List if they traded at C$1.05. They traded at this price last week.

The warrants have an exercise price of C$36.50, meaning that they are a very

long way out of the money (OR ended last week at C$11.92, which is close to the

bottom of its 3-year range). However, they don't expire until 18th February

2022, so there is a lot of time for the sort of increase in the stock price that

would inject substantial value into the warrants.

Note that our interest

in these warrants isn't based on a belief that OR shares will trade well above

C$36.50 by February-2022. It's possible that they will, but that's not a bet we

would make. Our bet is simply that there will be a large-enough rally in the

stock price at some point over the coming year or two to cause the warrants to

trade at least 200% above their current price. A 50% gain in the stock price

probably would be enough if it happened within the next 12 months.

Update

to TSI

Small Stocks Watch List (SSWL)

Northern Empire

Resources (NM.V) is a small, exploration-stage gold miner that was

added to the SSWL in May of last year. Its speculative merits were subsequently

discussed four times in TSI commentaries, most recently in the 11th December

2017 Weekly Update.

Last Thursday it was announced that NM had agreed to

be acquired by Coeur Mining (CDE) in an all-stock transaction that initially

valued NM at C$1.64/share. Due to a post-announcement pullback in CDE's stock

price, NM shares ended the week at C$1.52.

At last week's closing price

NM was up by almost 200% from the time it was added to the SSWL. This is a good

result considering that the HUI was down by about 10% over the same period.

If you own NM shares you should take your profit by selling into the market

unless you want to own CDE shares. We don't want to own CDE shares.

NM

has been removed from the SSWL.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.goldchartsrus.com/

http://www.lme.com/