![]()

![]()

![]()

![]()

-- Weekly Market Update for 8th July 2019

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bullish (04 Jan 2019) |

| US Equity (SPX) | Bearish (19 Apr 2019) |

| Currency (Dollar Index) | Neutral (15 Mar 2019) |

| Commodities (GNX) | Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

There were no blog posts last week.

Summary of current

thinking/positioning

1) The Dollar Index (DX) has

commenced a downward trend, but it could be a few months before the new

trend becomes consistent. In the meantime the price action could be

choppy, possibly involving a test of the May high near 98.

2) The

US$ gold price has broken out to the upside on a monthly basis.

Significant additional gains are likely within the next three months --

after a correction has run its course. The correction was/is expected to

result in a test of former resistance (now support) in the $1350-$1380

range. The US$ silver price stands a good chance of making a catch-up move

over the months ahead.

3) The gold-mining indices/ETFs became

extremely 'overbought' late last month and are now in correction mode. The

correction most likely will end after either a decline to the 50-day MA or

a few more weeks of sideways movement.

4) The SPX probably will

commence a sizable multi-week decline within the next two weeks.

5)

An upside blow-off has set the stage for a large T-Bond decline. If the

decline didn't begin on Friday 5th July then it should begin very soon,

although it could be September-October before the market starts trending

downward with conviction.

6) Oil's correction is probably over,

although there is still a risk that stock market weakness during

July-August will push the oil price to a new multi-month low.

7) We

are holding a cash reserve of 25%-30%.

US Recession

Watch

A month ago we wrote that if

commonsense did not prevail within the next few months then the Trump

tariffs could be comparable to the Smoot-Hawley tariffs of 1930 in terms

of their economic cost (one of the few things that almost all economists

agree on is that the Smoot-Hawley tariffs exacerbated the Great

Depression). Over the intervening period the tariff-related risk to the US

economy was reduced by the withdrawal of the threats to a) impose a hefty

tax on all imports from Mexico and b) add a tax to another $300B of

imported Chinese products. In any case, regardless of whether the

proximate catalyst for an economic contraction is the "trade war" or

something else entirely, our favourite leading recession indicators should

generate timely warning signals. These indicators are the ISM New Orders

Index (NOI), Real Gross Private Domestic Investment (RGPDI) and the yield

curve.

The latest monthly NOI was reported on Monday 1st July and

revealed that there was a small but significant decline in this measure of

manufacturing-industry strength in June. The index is now at 50, a new

2-year low.

50 is the official demarcation line between economic

expansion and contraction, but interpreting a sub-50 NOI as a recession

warning results in too many false signals. For example, it would have

resulted in false recession signals in 2012, 2013, 2015 and 2016. Most of

the false signals are eliminated without causing significant delays to

genuine signals if we set the demarcation line at 48, which is why we

define an NOI decline to below 48 (the red line on the following chart) as

a recession warning.

The upshot is that the NOI hasn't issued a

recession warning yet, but it is close to doing so.

The next quarterly RGPDI number will be published late this month, so

by the time we do our next "US Recession Watch" we will have new RGPDI

information.

The yield curve generates a recession warning when it

'flattens' to an extreme and then begins to steepen, regardless of whether

or not the extreme entails an inversion.

The US yield curve is

represented on the first of the following charts by the 10yr-2yr yield

spread and on the second of the following charts by the 10yr-3mth yield

spread. The 10yr-2yr spread has increased a little since bottoming late

last year and recently made a failed break above its 200-day MA, whereas

the 10yr-3mth spread remains in a clear-cut downward trend and close to an

11-year low.

As an aside, we require that a reversal in the yield

curve be signaled by reversals in both the 10yr-2yr and 10yr-3mth spreads.

This reduces the risk of being whipsawed. For example, if we had been

focused on only the 10yr-2yr spread then we would have been whipsawed by

this spread's recent non-sustained upward reversal.

The 10yr-3mth

spread has dropped well into negative territory, meaning that this part of

the yield curve is decisively inverted. The fact that it remains in a

declining trend indicates that the boom has not ended yet, but the fact

that it is well below zero indicates that the boom almost certainly will

end within the next 12 months.

Based on the latest data, our rough estimates of recession start-time

probabilities are:

- Q3-2019: 10% (down from 15% a month

ago)

- Q4-2019: 30% (down from 35% a month ago)

-

2020: 50% (not specified a month ago*)

- Later than 2020: 10%

(not specified a month ago*)

*Last month we

had a 50% probability of a recession starting later than 2019. That has

increased to 60%.

Monetary

Inflation Roundup

Here is our monthly update on

what's happening on the monetary inflation front in a few different

regions/countries.

Over the past three months the G2 (US plus

euro-zone) monetary inflation rate moved sideways at a 10-year low of 4.3%

and now has spent 21 months below the boom-bust threshold of 6%. Refer to

the following chart for details.

The low rate of G2 monetary inflation stems from the very low rate of

money-supply growth in the US. The year-over-year (YOY) rate of growth in

US True Money Supply (TMS) is languishing at 2%, which is close to a

20-year low.

Despite the slow pace of growth in US money supply,

US monetary conditions are still quite easy thanks to the reduced demand

to hold cash. That's why the slow monetary inflation rate has not yet set

in motion an economic bust and brought the bull market in US equities to

an end.

It isn't possible to measure directly the demand to hold

cash balances, but there are financial-market indicators of money demand

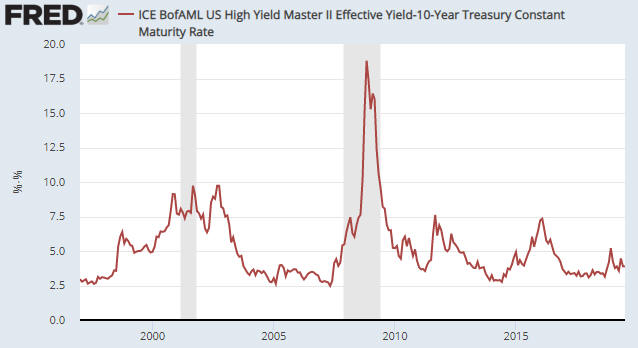

relative money supply. The average credit spread is one of the best.

Regardless of what's happening to the supply of money, when credit spreads

across the economy are narrow by historical standards it means that

monetary conditions are 'easy', and when credit spreads across the economy

are wide by historical standards it means that monetary conditions are

'tight'. The following chart shows that credit spreads currently are near

20-year lows.

Australia's monetary inflation rate has picked up a little over the

past few months, but the country remains on the verge of monetary

deflation.

The very slow money-supply growth has taken a

significant, albeit not yet substantial, toll on Australia's property

market. There are signs that a post-election boost to sentiment is

providing some price support, but house prices in Sydney and Melbourne,

the two largest Australian cities, are down by an average of 15% and 11%,

respectively, since their 2017 peaks.

Canada's monetary inflation rate bottomed at 2.8% (the lowest level in

more than 15 years) 12 months ago. It has since rebounded to a little over

5%, which is still very low based on the standards of recent decades.

On a nationwide basis the effects of the relatively slow pace of

money-supply growth have been minor to date. For example, house prices

have leveled off over the past 6-12 months, but a sizable price correction

has not occurred...yet.

The YOY rate of growth in Hong Kong's M2 money supply has languished

near a 10-year low in the 1%-4% range over the past year. Remarkably,

however, the low monetary inflation rate is yet to have a pronounced

effect on the world's most expensive real estate (the average house price

in HK is about 40% higher than the average house price in Singapore, the

world's second most expensive city to buy a house, and approximately

double the average house price in New York and London). Property prices

dropped in HK during August-December of last year, but they have since

made new all-time highs.

Due to the monetary backdrop we think

there's a high risk of a double-digit decline in HK property prices over

the next 12 months. That being said, it is notoriously difficult to

predict when a major investment bubble will burst.

In summary, the pace at which new money is being created around the

world remains unusually slow, but the effects of the monetary slow-down

have been surprisingly 'uninteresting' to date. As mentioned in relation

to the US, this could be due to a general decline in the desire to hold

cash.

Interest Rates

What the market expects

from the Fed

According to the prices of Fed Funds Futures

(FFF) contracts, over the past 1-2 weeks the market has dialed back its

expectations regarding Fed rate cuts.

Two weeks ago the market had

priced in three-and-a-bit 0.25% rate cuts before year-end, but now the

market is pricing in only two-and-a-half 0.25% rate cuts. Also, two weeks

ago the market had assigned a probability of around 50% that the Fed would

start its rate cutting with a 0.50% move at the end-July FOMC meeting, but

thanks largely to a positive surprise in the US employment numbers

reported on Friday 5th July the assigned probability of a 0.50% cut at the

end of July has dropped to zero. The expectation, now, is that the Fed

will cut by 0.25% at the end of this month and make 1-2 additional 0.25%

cuts before the end of the year.

Our current guess is that the Fed

will make two 0.25% rate cuts before the end of September and be on hold

for the remainder of the year.

A potential T-Bond reversal

Tentative signs have emerged of a downward trend reversal in the bond

market.

As illustrated by the following daily chart, the 20+ Year

Treasury ETF (TLT) made a new high for the year on Wednesday 3rd July and

then dropped sharply on Friday 5th July (the market was closed on

Thursday). In addition, the higher highs achieved by TLT since the end of

May have gone with a downward trend in the daily RSI shown at the bottom

of the following chart. This is a potentially bearish momentum divergence.

A daily close below last week's low would be preliminary evidence that

a top of at least short-term importance is in place.

The Stock Market

Current Market Situation

At this time last week the outcome of the Trump-Xi meeting had just

become known, prompting us to write: "Although the meeting outcome

appears to be in line with what most market participants were expecting,

the removal of a near-term source of uncertainty could give sentiment a

sufficient boost to push the senior US stock indices to new all-time highs

this week."

It turned out that sentiment was, indeed, given a

sufficient boost by the temporary winding-down of US-China government

conflict to push the SPX into new-high territory, with the breakout

confirmed and led by the Advance-Decline Line (ADL).

However, at this stage the S&P500 (SPX) is the only important US stock

index to break out to the upside on a weekly closing basis. Some indices

are testing their highs and therefore are close to breaking out to the

upside, while other indices are not remotely close to their all-time

highs. The following daily charts show an example of the former (the

NASDAQ100 - NDX) and the latter (the Dow Transports - TRAN). The NDX is

testing its April-2019 all-time. The TRAN, however, is well below its

April-2019 high, which, in turn, is well below the 2018 all-time high.

Given the TRAN's tendency to be a leader to the downside around

important stock market peaks, this index's relative weakness should be

viewed as a significant bearish divergence.

The on-going strength in the ADL indicates that a major decline is NOT

about to begin, but the combination of the recent put/call sell signal and

the divergences between the stock indices is a reason to think that a

tradable 1-2 month decline will get underway soon.

The tendency of

the US stock market to make an intermediate-term top during the first half

of July is also noteworthy. For example, intermediate-term tops occurred

at this time of the year in 1990, 1998, 1999, 2007, 2011 and 2015.

With regard to speculating ideas, over the past 1-2 weeks we wrote

that a boost from trade-related optimism would present an opportunity to

establish or add to short-term bearish speculations, with risk then

managed by placing an initial 'stop' slightly above whatever high is in

place by mid-July. We also mentioned an alternative tactic, which was to

wait for a downward reversal before entering or adding to a bearish

speculation. Specifically, we wrote that if the SPX closed at a new

all-time high (above 2964), then a subsequent daily close below 2940 could

be viewed as a reversal signal.

The SPX has closed at a new

all-time high, so a daily close below 2940 could now be viewed as a

reversal signal.

In summary, we think that the long-term bull

market is intact, but we are expecting that a tradable 1-2 month decline

will start by the middle of this month.

A brief comment on

the banking sector

On the following weekly chart there is

a note to the effect that the current position of the US Bank Index (BKX)

is similar to the position of this index at this time (early July) three

years ago. If the similarity persists then the BKX will perform very well

over the next 6 months.

One of the keys to how the banking sector

performs over the next several months will be the performance of the bond

market. In particular, if the T-Bond is about to embark on an

intermediate-term decline, which it was at this time three years ago, then

the BKX will be helped by an interest-rate tail-wind (bank stocks tend to

do relatively well when long-term interest rates are rising).

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Jul-08 | Consumer Credit |

| Tuesday Jul-09 | NFIB Small Business Index |

| Wednesday Jul-10 | FOMC Minutes |

| Thursday Jul-11 |

CPI Treasury Budget |

| Friday Jul-12 | PPI |

Gold and the Dollar