![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 9th July 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bullish (29 Jun 2018) |

| US Equity (SPX) | Bearish (29 Jun 2018) |

| Currency (Dollar Index) | Bullish (27 Apr 2018) |

| Commodities (GNX) | Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

Gold's true fundamentals turn bullish

Summary of current

thinking/positioning

1) Anticipating a Dollar Index

(DX) decline to 92 and a euro rally to 1.20 within the next 2 months, but

unsure regarding the 6-12 month prospects.

2) Gold and silver

prices may have bottomed in early-July, but the bottoms haven't been

confirmed.

3) Some US stock indices are set to make new all-time

highs in July, but risk is increasing and there are preliminary signs that

the market as a whole is rolling over into what could be a substantial

decline.

4) The industrial metals markets have weakened across the

board and in some cases are now very stretched to the downside. At the

same time the oil market looks stretched to the upside on a short-term

basis. We are anticipating counter-trend rebounds in metal prices and a

downward correction in the oil price.

5) The T-Bond price should

have an upward bias for another 2-3 months.

6) Holding a cash

reserve of around 30% and looking for opportunities to build up this

reserve.

Another look at

the US yield curve

The US yield curve, as indicated

by the spread between the 10-year and 2-year T-Note yields, made a new

10-year extreme last week, meaning that it is now the 'flattest' it has

been in more than 10 years. While this possibly indicates that the boom is

nearing its end, it definitely indicates that the transition from boom to

bust has not yet begun.

As explained numerous times in the past,

the 'flattening' of the yield curve (short-term interest rates rising

relative to long-term interest rates) is a characteristic of a

monetary-inflation-fueled economic boom. It doesn't matter how flat the

yield curve becomes or even if it becomes inverted, the signal that the

boom has ended and that a bust encompassing a recession is about to begin

is the reversal of the curve's major trend from flattening to steepening.

To put it another way, the signal that the proverbial chickens are coming

home to roost is short-term interest rates peaking RELATIVE TO long-term

interest rates and then beginning to decline relative to long-term

interest rates. This generally will happen well before the Fed sees a

problem and begins to cut its targeted short-term interest rate.

The following chart highlights the last two major reversals of the US

yield curve from flattening to steepening. These reversals were confirmed

about 6 months prior to the recessions that began in March-2001 and

December-2007.

The fact that the yield curve is still hitting new

extremes in terms of 'flatness' suggests that the next US recession will

not begin before 2019.

The above is essentially a repeat of what we've written in the past,

but there is a new point we want to cover. The new point is that while it

would be almost impossible for the US economy to transition from boom to

bust without a timely reversal in the yield curve from flattening to

steepening, there is a realistic chance that the next yield-curve trend

reversal from flattening to steepening will not signal the onset of an

economic bust/recession. That's why we do not depend solely on the yield

curve when determining recession probabilities.

The reason that

the next yield-curve trend reversal from flattening to steepening will not

necessarily signal the onset of an economic bust/recession is that there

are two potential drivers of such a reversal. We are referring to the fact

that the reversal could be driven by falling short-term interest rates or

rising long-term interest rates. If it's the former it signals a boom-bust

transition, but if it's the latter it signals rising inflation

expectations.

As an aside, regardless of whether a major

yield-curve reversal from flattening to steepening is driven by the

unravelling of an artificial boom or rising inflation expectations, it is

bullish for gold. By the same token, a major reversal in the yield curve

from steepening to flattening is always bearish for gold.

With the

T-Bond rebound likely to continue for at least 2 more months there is

little chance that rising long-term interest rates will drive a yield

curve reversal during the third quarter of this year, but it's something

that could happen during the fourth quarter.

Commodities

Copper breakdown

Here's how we described the two most plausible copper scenarios in our

18th June commentary:

"...the extremely aggressive speculative

positioning indicated by the latest COT report combined with Friday's

decisive breach of $3.20 suggests that we are dealing with something more

bearish than a routine 1-2 week correction. It suggests that either the

previous week's move up to around $3.30 created an intermediate-term

double top, in which case a decline to as low as the $2.50s could precede

the next substantial rally, or the price will chop around between $2.95

and $3.30 for a few more months before resuming its multi-year upward

trend."

Last week the copper price broke below support at

$2.95, so the second of the above-mentioned scenarios has been ruled out.

This means that a decline to support near $2.50 is now the

highest-probability outcome, although given that the market is stretched

to the downside and that there is support near the current price it is

reasonable to anticipate a multi-week rebound prior to any significant

additional weakness.

Note that former support in the mid-$2.90s is

now resistance and is the most likely place for a near-term rebound to

peak.

We've been mentioning since early this year that the copper price

could revisit support at around $2.50 before resuming its bull market. The

early-June surge to test the December-2017 high was deceptive, but it's

not exactly a shock that the drawn-out period of sideways trading between

the $2.90s and the $3.20s turned out to be a topping pattern.

It's

unlikely, in our opinion, that a major top was put in place by the copper

market late last year. It's far more likely that the December-2017 price

high marked the top of the first leg of a cyclical bull market.

Across-the-board weakness in industrial-metals prices

Over the first 5 months of this year there were widely varying

performances among the base metals. For example, the first of the

following charts shows that zinc has been trending downward since February

while the second chart shows that nickel made a new high for the year as

recently as last month. However, over the past three weeks all the

high-profile base metals experienced sizable price declines.

Copper

and zinc have been the weakest base-metal markets since early-June.

Copper's recent weakness can be explained by the preceding rapid build-up

of speculative long positions, but we don't have an explanation for the

sell-off in the zinc market. Regardless of the reason behind it, the

recent downward acceleration of the zinc price means that we are dealing

with a larger-degree correction than originally envisaged.

In addition to the declines in base-metal prices, there recently has

been a plunge in the platinum price and a rolling-over of the iron-ore

price. It is therefore fair to say that there is currently

across-the-board weakness in the prices of industrial metals. This

weakness is most likely occurring within the context of an on-going

multi-year bullish trend, but it could be a warning sign that the

relatively slow G2 monetary inflation rate is starting to 'bite' and that

the coming few months will involve a shift away from growth-oriented

investments and speculations.

Soybean crash

The following daily chart of the Teucrium Soybean Fund (SOYB) shows

that there was a mini-crash in the soybean price from late-May through to

last Thursday and then a rebound on Friday. This crash was at least partly

a response to the China government's retaliation to tariffs imposed by the

US government.

The weakness in the soybean market seems to be overdone, because China

will not be consuming less soybeans due to the "trade war"; it will be

consuming less soybeans produced in the US and more soybeans produced

elsewhere. Therefore, the soybean price is probably close to a very

important low.

The Stock Market

Leverage continues to

expand

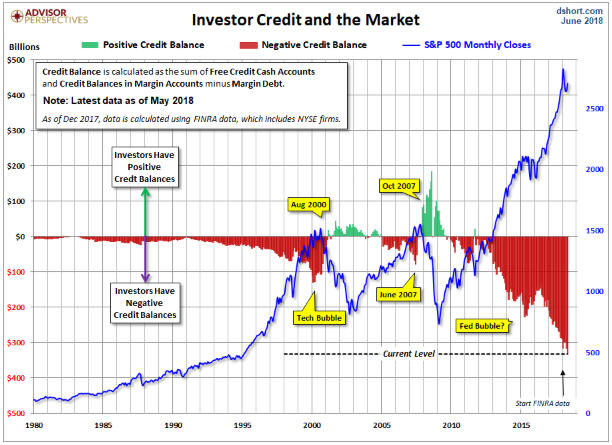

"Investor Credit" is calculated by subtracting

margin debt from the available spending power (cash plus unused credit) in

margin accounts. It is a measure of stock market leverage that tends to

reach a maximum negative value (indicating maximum leverage) PRIOR to

major peaks in the US stock market. For example, the negative value of

Investor Credit hit a cyclical high in February-2000, one month prior to a

major peak in the NASDAQ and six months prior to a major peak in the broad

market, and in June-2007, four months prior to a major peak in the S&P500.

The following chart shows that during the current cycle the expansion

of the negative credit balance in margin accounts has dwarfed anything

that happened in the past. It also shows that the negative credit balance

was still expanding as of May-2018 (the latest month for which data are

available).

It's a short-term positive for the stock market that

leverage was still expanding at the end of May, but the amount of leverage

now built into the market is a major long-term negative.

Chart source:

Advisor Perspectives

Current Market Situation

At the January-2018 stock market high, virtually all stock indices

were stretched to the upside. The entire market then began to decline,

which led to a rise in the Volatility Index (VIX) and a spectacular

blow-up of the 'short volatility' trade.

Currently, some US stock

indices are stretched to the upside while others look 'oversold'.

Consequently, if the stock market is close to another top, which it may

well be, it's a far more complex top than the one that occurred in

January. It's a top that's rife with divergences.

The set of four

daily charts displayed below is an example of the performance divergence

mentioned above. The first chart shows that since the January-2018 peak

the NASDAQ100 Index (NDX) has made two higher highs, with the most recent

high occurring in June. The June high was followed by what appears to be a

routine pullback to the 50-day MA, and a new all-time high is now in

reach. The second chart shows that the January-2018 peak for the

Russell2000 SmallCap Index (RUT) was followed by a 3-month consolidation

and then a very strong rally into new-high territory. As is the case with

the NDX, the RUT's June high was followed by what appears to be a routine

pullback to the 50-day MA, with another push into new-high territory now

on the cards. In contrast, the third chart shows that the Bank Index (BKX)

is consolidating near its low for the year. And the fourth chart shows

that although the Dow Transportation Average (TRAN) has begun to rebound

from an 'oversold' level, it has done serious technical damage by breaking

below the bottom of a 2.5-year channel.

The divergences are largely the result of the "trade war" started by

the Trump administration earlier this year. It seems that many 'investors'

are operating under the illusion that the dampening economic effect of

tariffs and quotas can be avoided by purchasing the extremely expensive

shares that populate the NDX and the RUT. It's likely that these investors

will experience a rude awakening within the next few months.

In

addition to the "trade war", there are many reasons to believe that the US

stock market's risk/reward is now bearish with regard to both the

short-term and the intermediate-term. These reasons include:

1.

Monetary conditions are tight by the standards of the past several years.

2. Credit spreads have begun to widen.

3. Bank stocks are

relatively weak.

4. Industrial commodities are breaking down.

5. The put/call ratio remains close to a sell signal, although it

isn't quite there yet.

6. China's currency is weakening.

7.

The Bitcoin price continues to trend downward.

8. Equity indices

are diverging as discussed above.

One positive is that market

internals are yet to signal a problem.

We suspect that both the NDX

and the RUT will soon make new all-time highs, but that the new highs in

these indices will be marginal and will not be confirmed by the rest of

the market. Therefore and as mentioned in last week's Interim Update, it

would be reasonable to start averaging into bearish stock market

speculations or stock market hedges via options or bear funds.

We

aren't going to make any specific suggestions today, although we may add

one or two index put options to the TSI List within the coming week.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Jul-09 | Consumer Credit |

| Tuesday Jul-10 | No important events scheduled |

| Wednesday Jul-11 | PPI |

| Thursday Jul-12 |

CPI Treasury Budget |

| Friday Jul-13 | Consumer Sentiment |

Gold and the Dollar

Finally, the chart displayed below shows gold's performance relative

to the basket of industrial metals represented by GYX. Relative to GYX,

gold has just bounced after making a 7-year low.

Almost regardless

of how gold performs in US$ terms we expect that it will strengthen

relative to industrial metals over the coming 2-4 months. This is due to

the depressed level of the gold/GYX ratio and the recent shift in the

fundamental backdrop in gold's favour.

Silver

The silver price broke below support at

$16.10 early last week and traded as low as $15.80 before rebounding. The

rebound wasn't impressive, though, as it did no more than take the price

back to the breakout level.

A daily close above $16.30 would be a preliminary sign that the price

has turned upward on a sustainable basis, but to signal conclusively that

a meaningful rally is underway the market will have to end the pattern of

declining tops that is now almost 2 years old. To do so the silver price

will have to close above $17.30.

Gold Stocks

Just for a change, today we'll

focus on the Junior Gold Miners ETF (GDXJ).

The following daily

chart shows that GDXJ sprang to life last week, breaking above

moving-average resistance and trading at its highest level since the first

half of May.

The next daily chart covers a longer period and puts last week's

strength into perspective. It indicates that nothing significant happened

last week.

Since 2016, GDXJ's overarching pattern has entailed

declining tops, rising lows, and declining volatility. Furthermore, over

the past few months the ETF's price volatility has shrunk to the point

where additional shrinkage does not seem possible.

To indicate that the period of tedium has ended and that a move of

substance is underway, GDXJ will have to break the post-2016 pattern of

declining tops and rising lows. This means that it will have to close

above $36.08 or below $29.83. An upside breakout is more likely than a

downside breakout, but not decisively so at this time.

From a

bull's perspective, the ideal price action over the days ahead would

involve a 1-2 day consolidation followed by a daily close above Friday's

high ($33.65).

The Currency Market

The

Dollar Index (DX) dropped to its 50-day MA last Friday and then bounced.

This has possibly set the stage for some minor strength during the next

couple of days, but the following excerpt from last week's Interim Update

is still applicable:

"Regardless of whether we are dealing with a

DX bull or bear market, a pullback to near the 200-day MA (around 92) is

likely within the next 1-2 months. This would coincide with the euro

rising to around 1.20."

The Australian dollar has rebounded to resistance defined by its May

low (0.745). There is more resistance at 0.75, but the most important

nearby resistance may be defined by the trend-line that connects the highs

of the past 5 months. This trend-line capped the May-June rebound and

currently is at 0.755-0.760.

Of the major currencies, the Swiss franc (SF) has the most bullish COT

situation.

The historical record suggests that the SF could make a

new low for the year before commencing a sizable advance. However, the

historical record also suggests that regardless of whether or not there is

an intervening decline to a new low for the year, the SF will be

significantly higher two months from now.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 6th July 2018:

Company

news/developments for the week ending Friday 6th July 2018:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery,

MD&A = Management Discussion and Analysis, M&I = Measured and Indicated,

NAV = Net Asset Value, NPV(X%) = Net Present Value using a discount rate

of X%, NSR = Net Smelter Return, P&P = Proven and Probable, PEA =

Preliminary Economic Assessment, PFS = Pre-Feasibility Study]

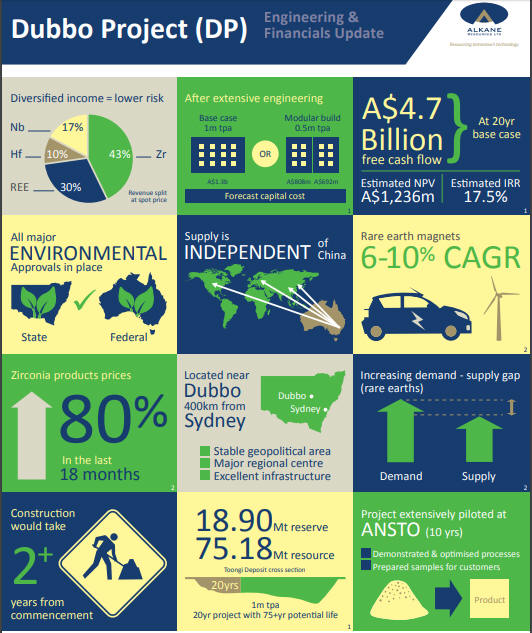

*Alkane Resources (ALK.AX) distributed an infographic

highlighting some of the important aspects of its Dubbo specialty metals

project. We thought that the graphic was a useful summary and include it

below without further comment.

*Alio Gold (ALO) took responsibility for a

$15M project loan from Macquarie Bank when it acquired Rye Patch Gold

(RPM). At the time of the RPM acquisition it was envisaged that repayment

of the loan would be renegotiated to occur via 12 quarterly instalments.

It was announced last week that what was expected has come to pass and the

loan will be repaid via 12 quarterly instalments of $1.25M beginning in

September of this year. This is positive, although, as we said, it was

expected.

*Clean TeQ (CLQ.AX, CLQ.TO)

advised that Robert Friedland, its co-chairman, has increased his stake in

the company to 12.91% through the on-market acquisition of 1,385,830

shares at a price of approximately A$0.92 per share. This is positive.

*Resolute Mining (RSG.AX) was added to the TSI

list last November as a short-to-intermediate-term trading position. This

is part of what we wrote about RSG at that time:

"RSG's most

important assets are the Syama gold mine in Mali (West Africa) and the

Ravenswood gold mine in Queensland, Australia. Syama is currently

producing gold at the rate of 220K-ounces/year and Ravenswood is currently

producing gold at the rate of 80K-ounces/year, but in-progress development

plans are expected to increase the production rates to 240K-ounces/year

and 120K-ounces/year, respectively. RSG also owns the Bibiani gold project

in Ghana. It is expected that Bibiani will be brought into production

within the next year or so and will produce gold at the rate of 100K

ounces/year over an initial 5-year life.

With 741M shares

outstanding and estimated net cash of A$187M, at the current share price

(A$1.025) RSG has an enterprise value of A$573M (US$435M). This is low for

a profitable gold miner with 300K-ounces/year of current production (at an

AISC of US$960/oz), a 12-13 year mine life at its two most important

assets, and built-in growth to a production rate of 460K-ounces/year over

the coming two years. The current valuation suggests the potential for at

least a 50% increase in the stock price with no increase in the gold

price, although it's likely that an upward-trending gold price will be

required to push the share price up to the A$1.50-$2.00 range that we have

in mind as a target for this trade."

Since RSG was added to

the List its stock price has gained 40% in a flat gold market. Due to this

price gain and the company having invested some of its cash, we estimate

that RSG's enterprise value is now about 54% higher at US$670M.

We

think that RSG is now fairly valued based on the current gold price and

the company's current production. However, we also think that RSG's stock

price stands a good chance of rising to near A$2.00 within the next 6

months in response to a higher gold price and the discounting by the

market of growth in the company's production and profitability.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI

stock selections the best candidates for new buying at this time, listed

in alphabetical order, are:

1) AAU (last Friday's closing price:

US$0.72)

2) CNL.TO (last Friday's closing price: C$3.84)

3)

KBLT.V (last Friday's closing price: C$8.82)

4) PG.TO (last

Friday's closing price: C$2.76)

5) SBB.TO (last Friday's closing

price: C$1.63)

The above list is limited to five stocks. It will

sometimes contain less than five, but it will never contain more than five

regardless of how many stocks are attractively priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.kitco.com/