![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 10th August 2015

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in early-2015, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020. (Last update: 29 June 2015)

A secular BEAR market in the US Dollar began during the final quarter of 2000 and ended in July of 2008. This secular bear market will be followed by a multi-year period of range trading. (Last update: 09 February 2009)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak sometime between 2018 and 2020. (Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

|

Market |

Short-Term (1-3 month) |

Intermediate-Term (6-18 month) |

Long-Term (2-5 Year) |

| Gold | N/A |

Bullish (26-Mar-12) |

Bullish |

| US$ (Dollar Index) | N/A |

Neutral (22-Jun-15) |

Neutral (19-Sep-07) |

| US Treasury Bonds (TLT) | N/A |

Neutral (18-Jan-12) |

Bearish |

| Stock Market (DJW) | N/A |

Bearish (28-Nov-11) |

Bearish |

| Gold Stocks (HUI) | N/A |

Bullish (23-Jun-10) |

Bullish |

| Oil | N/A |

Bullish (17-Dec-14) |

Bullish |

| Industrial Metals (GYX) | N/A |

Bullish (22-Jun-15) |

Bullish (28-Apr-14) |

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

Is the Fed privately owned? Does it matter?

The gold supply-demand nonsense is relentless

The amazing inability to see the Fed�s money creation

Can the US economy survive more of the Fed�s monetary support?

Commodities

Overview

An across-the-board sell-off in commodities began around the middle of last

year. For a while it looked like a sustainable bottom might have been put in

place during the first quarter of this year, but the selling pressure ramped up

in May and the prices of many commodities have made new bear-market lows over

the past three weeks. Is the bear market now almost over?

We can't answer that question other than to say it could be, but there is no

bottom-indicating evidence at this time apart from a rarely-seen 'oversold'

extreme. Our guess is that a strong rebound will soon begin, but with the EEM/SPY

ratio having not yet turned higher it's likely that the Q3-2015 price lows will

have to be tested prior to the start of a new cyclical bull market.

Before we discuss the situations of some individual commodities there are two

points we want to get across, the first being that the plunge in commodity

prices has nothing to do with deflation in the US (or anywhere else, for that

matter). Apart from the facts that the US money supply is still growing at 7%-8%

per year, economy-wide credit is still expanding, commercial bank credit is up

by 7.5% over the past 12 months, the median house price is in a multi-year

upward trend, junk bonds are still at high valuations by historical standards

and the cost of living is obviously still rising, we cite the performance of the

US stock market. An over-valued stock market would be acutely vulnerable to

deflation, but the US stock market has chopped back and forth over the past five

months near its all-time price and valuation high.

Inflation and deflation are, by definition, economy-wide outcomes. This means

that assertions to the effect that there is deflation in some parts of the

economy and inflation in other parts of the economy are always nonsense.

However, individual sectors can experience booms and busts at different times.

What we have seen in the commodity markets over the past year is the bust that

inevitably follows an inflation-fueled boom. More specifically, capacity was

expanded in response to monetary-inflation-generated price signals that tricked

commodity producers into believing that future demand would be much greater than

it was ever going to be.

Now, it is clear that the central bank's manipulation of money and interest

rates has falsified prices throughout the economy, causing mal-investment to

extend well beyond the commodity production/distribution industries. As a

result, it is certainly possible that deflation could occur in the future. The

thing is, when a bust affects the commodity world it is not usually viewed by

central bankers as a problem that requires a monetary response, but it's a very

different story when a bust affects the banking industry and the stock market.

The reality is that another bout of aggressive monetary inflation is likely to

accompany the first obvious signs that deflation is becoming something more than

a longshot, eliminating any genuine deflation threat soon after it emerges.

The other point we want to make before delving into the situations of some

individual commodities is that commodity fundamentals always look great near the

ends of bull markets and terrible near the ends of bear markets. Think back to

how bright the fundamental outlook for commodity producers appeared to be in

late-2010 and early-2011. Consequently, the fact that many commodity-producing

industries are now wallowing in over-capacity does not mean that a major price

bottom is not close at hand. The fundamentals always appear to be lousy at major

price bottoms. The question is: have prices already fallen far enough to fully

discount the lousy fundamentals?

Oil

In early May, soon after the end of a multi-week rebound in the oil price, we

wrote that one of two short-term scenarios was likely. The first was a pullback

to test the March low prior to the start of an intermediate-term rally. The

second was several weeks of sideways consolidation and then the resumption of

the upward trend that began in March. We thought the first scenario had the

higher probability, but the market made the situation as confusing as possible

by first trading sideways for a few weeks and then pulling back to the vicinity

of its March low.

A test of the March low is currently underway. If the test is successful then

oil will have bottomed in 2015 in a similar fashion to how it bottomed in 1986.

There is, of course, no guarantee that the test will be successful. If the oil

price holds above its March low on a weekly closing basis and then manages to

close a week above its 10-week MA, it will indicate that the test was successful

and that oil's bottoming process is complete.

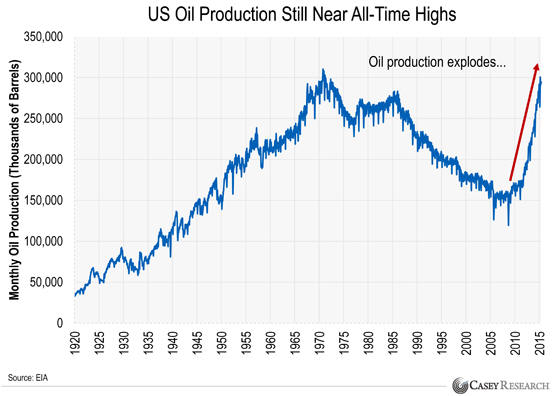

Oil's supply-demand fundamentals are obviously still bearish, partly thanks to

the continuing elevated production from the US shale-oil industry. In

particular, the following chart from a

Casey Research Dispatch shows that US oil production rose sharply over the

past five years from a 60-year low to near an all-time high and hasn't yet

reacted to the lower price. However, as we noted in the above "Overview", the

salient question is whether the price has already fully discounted the bearish

fundamentals, because we can be sure that the price will bottom in parallel with

bearish fundamentals.

Based on articles we've read in the recent past (such as the one posted

HERE), another point worth making (re-making, actually) is that the price of

a commodity futures contract does NOT represent the market's expectation about

where the commodity price will be at the time of contract expiry. For example,

if the price of the December-2016 oil futures contract is $65 it does not imply

that the market expects the price of oil to be $65 in December-2016. Futures

prices are based on CURRENT supply/demand (the urgency of buyers relative to the

urgency of sellers in the cash market) and arbitrage, taking into account the

cost of financing and the cost of storage. That, in a nutshell, is why a decline

in futures prices relative to the spot price is not a bearish sign.

Finally, the happenings of the past few years prove that the level of oil

production is limited more by price than geology. That is, contrary to the

beliefs of some "Peak Oil" alarmists, a large and sustained rise in the oil

price did what large and sustained rises in commodity prices have always done:

caused a large increase in supply.

Iron Ore

Other than checking its price about once per week and reading the occasional

iron-ore-related article, we don't follow the iron-ore market. We are only

mentioning it in today's report because a) its performance over the past 10

years is another classic example of the boom-bust cycle caused by monetary

inflation and interest-rate manipulation, b) it is being held up as the poster

child for everything that's wrong with the commodity-production industry and an

example of what can be expected (on the downside) from other industrial metals

over the months ahead, and c) there are tentative signs in the price action that

it has bottomed.

As illustrated by the following chart, the iron-ore price made a bottom in

early-April, rebounded for about two months and then dropped back to its April

low. It made a marginal new low in early-July, but instead of signaling the

resumption of the bear market the early-July downside breakout was quickly

negated by a sharp rebound.

Failed downside breakouts are reliable bullish signals. At least, they are more

reliably-bullish than upside breakouts. We therefore have tentative evidence

that a 'double bottom' is in place in the iron-ore market. A weekly close above

the early-June rebound peak would shift the evidence from tentative to

definitive.

Copper

Over the past two years the Commitments of Traders (COT) report has been by far

the most useful indicator of copper's likely short-term price performance. Most

recently, in early-May of this year the shift in the speculative position in

COMEX copper futures from net-short to net-long (as indicated by the COT data)

suggested that a short-term top was being put in place in the US$2.90s. We

guessed at the time that a decline to the vicinity of the January low ($2.40)

would happen over the ensuing two months.

The copper price ended up dropping below its January low, but until last week

the COT situation wasn't suggestive of a short-term price bottom. The reason is

that prior to last week the net positions of speculators and commercials hadn't

moved to levels that had been reached at or prior to every previous short-term

bottom over the preceding two years. More specifically, over the past two years

the copper price hasn't reached a short-term bottom until the net-short and the

net-long positions of speculators and commercials moved to the boundaries of the

rectangle drawn on the following chart.

As of the latest report, the COT numbers are now consistent with a short-term

price bottom for the copper market. The caveat is that there was a multi-week

overshoot in December-January that could also occur this time around.

On a longer-term basis copper looks expensive relative to other industrial

commodities, so at this stage we aren't anticipating a major rally -- just

another 2-4 month rebound.

Natural Gas

Natural gas completed its boom and its ensuing bust earlier than most other

commodities. Its bust probably ended during the first half of 2012 and it is

showing signs of having completed a secondary (higher) bottom during the first

half of this year. However, it needs to achieve a weekly close above US$3.10

(the May rebound peak) to confirm that a secondary bottom is, indeed, in place

and that a tradable rally is underway.

From a seasonal perspective, the period between now and early-September is the

most likely time for the start of a rally.

International Ocean-Going Freight Rates

The boom and bust in commodity prices led to a boom and bust in international

shipping rates as represented by the Baltic Dry Index (BDI). As commodity

producers were ramping up supply in response to false signals regarding the

level of future demand, the companies that build and operate the ships that

transport commodities between countries were doing the same. There was a huge

increase in shipping capacity, leading to a major decline in BDI.

Because the BDI's massive decline from a high of about 11800 in early-2008 to a

bottom of around 500 early this year -- a peak to trough decline of more than

95% -- was clearly related far more to shipping supply than the volume of global

trade, we stopped using the BDI as an economic indicator several years ago.

However, the following chart shows that there is a long-term correlation between

the BDI (the blue line on the chart) and the CRB Index (the green line on the

chart). The chart also shows that the BDI has led the CRB Index at important

turning points over the past 10 years.

Due to its tendency to lead at important turning points, the BDI's sharp rebound

from its Q1-2015 bottom is interesting. A sharp rebound in the BDI during 2013

proved to be nothing more than a counter-trend move within a continuing bear

market, but that doesn't mean that the current one won't have longer-term

importance.

We'll be paying closer attention to the BDI over the months ahead.

Commodity-related equities

When it comes to practical speculation we are generally more interested in

commodity-related equities than the commodities themselves.

As followers of and investors in the gold-mining sector would know, gold-mining

stocks have been much weaker than gold bullion and the weakness is persisting

despite the gold-stock indices being very stretched to the downside relative to

gold bullion. However, over the past few months the weakness in gold-mining

equities relative to gold bullion has paled in comparison with the weakness in

natural-gas equities relative to natural gas. Whereas natural gas has done no

worse over the past three months than trade sideways, natural-gas equities, as

represented on the following chart by FCG, have crashed.

FCG's performance is a reflection of "get me out at any price" sentiment.

Short-term traders should either not attempt to catch this falling knife or

should place stops to limit losses if the knife continues to fall, but traders

prepared to take a 6-18 month view could reasonably average-in during this

period of extraordinary relative weakness.

Copper equities, as represented on the following chart by COPX, have also

experienced a spectacular decline over the past three months, although in this

case the underlying commodity fell sharply. COPX is not quite as depressed as

FCG, but the same suggestions apply.

Bonds

The decline in the prices of

long-dated Treasury securities that began in the first quarter of this year

ended in May. The iShares 20+ Year Treasury Bond Fund (TLT) has since rebounded

by enough to break above the top of a well-defined price channel. Refer to the

following daily chart for details.

The market is now slightly 'overbought' on a short-term basis and will possibly

consolidate its recent gains, but additional gains are likely prior to the next

multi-month top.

T-Bonds should benefit from a 'flight to safety' over the coming 2 months IF

there's a significant decline in the stock market, but at this stage we don't

expect the T-Bond or TLT to do more in the short-term than test their respective

Q1-2015 peaks. The reason is that, like the Dollar Index, the T-Bond became

sufficiently extended to the upside during the first quarter of this year to

create either a cyclical peak or a peak that will hold for many months.

The Stock Market

The US

At this time the chance of a 2008-style collapse in the US stock market is

extremely small, to the point of being nonexistent. This is because economic

confidence and the monetary inflation rate are at levels that pretty much

preclude such an outcome. However, there's a good chance of a 10%-20% decline

within the coming 3 months. If such a decline materialises it could be the first

leg of a cyclical bear market or it could be the first significant correction

since 2011 in a continuing cyclical bull market. Based on what we know today our

guess is that it would be the former, but there is no point spending a lot of

time thinking about what such a decline implies about the future until it

actually happens.

At the moment the market is doing its best not to provide clues regarding the

likely short-term price direction. The S&P500 Index (SPX), which is by far the

most important US stock index, remains within the unusually-narrow horizontal

trading range that dates back to February (see chart below). It needs to break

out of this range to generate a meaningful price signal. The NASDAQ100 Index (NDX),

the second most important US stock index, also needs to do more -- in one

direction or the other -- to generate a meaningful price signal.

Some of the lesser indices have generated bearish signals and the weakness over

the past few months in measures of market breadth also points to a short-term

bearish outcome, but these bearish indications won't mean anything until/unless

they are confirmed by the price action of the SPX and the NDX.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Aug 10 | No important events scheduled |

| Tuesday Aug 11 | Q2 Productivity and Costs |

| Wednesday Aug 12 | Treasury Budget |

| Thursday Aug 13 |

Retail Sales Import and Export Prices Business Inventories |

| Friday Aug 14 |

PPI Industrial Production Consumer Sentiment |

Gold and the Dollar

By the way, according to the Fed Funds Futures market last Friday's employment

data and price action slightly increased the probability that the Fed's first

rate hike will happen in September. We are hoping it will happen in September so

that 'everyone' can stop talking about it and acting as if a 0.25% interest-rate

increase means something.

The COT

Gold's COT situation was unequivocally bullish during the week before last and,

according to last week's data, is now even more so by a small amount. The total

speculative net-long position remained unchanged at a 13-year low of 15K

contracts, but over the latest week there was an increase in the long exposure

of large speculators that was offset by an increase in the short exposure of

small traders. The net-short position of small traders (the proverbial dumb

money) in COMEX gold futures is now at its highest level since the early-1990s,

which suggests that small traders in COMEX futures haven't been this bearish on

gold in almost 25 years.

Silver's COT situation is also bullish, but not quite as bullish as gold's.

Gold Stocks

The superficial impression created by the price action is that although the

gold-mining indices are more 'oversold' than they have ever been, they are

incapable of rallying. This impression was supported by last Friday's price

action, when an upward reversal by the gold price failed to result in a

sustained rebound in the gold-mining sector. Instead, the HUI initially rose to

a new 4-day high on Friday and then promptly gave back its gain.

Has the sort of price action witnessed in the gold-mining sector over the past

few weeks ever happened before?

The answer is yes; the recent price action is similar to what happened during

the weeks leading up to the major bottom in November of 2000. As illustrated

below, the final three weeks of the bear market that ended in November of 2000

involved gold bullion trading sideways within a narrow range in parallel with

relentless weakness in the HUI.

There are some important differences between the present situation and

November-2000. In particular, in November-2000 the fundamental backdrop had

recently become unequivocally gold-bullish, thanks in part to clear evidence

that the US stock market's long-term bullish trend had ended. That's not the

case now. Our points are simply that the gold-mining sector can look dismal

right up to the day that a major rally begins and that the price action does not

imply significant additional short-term weakness.

The Currency Market

Based on the price action we have thought that the Dollar Index had a roughly

equal chance of rising to test its March high near 100 or pulling back to the

low-90s (a sustained move outside the 90-100 range is unlikely over the next few

months). It would take a daily close below 96.3 to definitively skew the odds in

favour of the latter outcome, although Friday's performance constitutes a

tentative sign that the next move of significance will be to the downside. The

reason is that Friday was an outside-down reversal day for the Dollar Index,

meaning that the Dollar Index a) reversed direction after first making a

marginal new high for the move, b) ended the day with a loss, and c) traded

outside the range of the preceding day.

Although US$ fundamentals are superficially bullish, the COT data suggest that

the fundamentals are fully discounted in the dollar's current exchange value.

What we mean is that currency speculators are positioned in a big way for

additional US$ gains. This limits the potential for new speculative buying to

boost the dollar and increases the potential for the unwinding of short-term

speculative positions to push the dollar downward.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ended Friday 7th August 2015:

Company

news/developments for the week ended Friday 7th August 2015:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, IRR = Internal

Rate of Return, MD&A = Management Discussion and Analysis, M&I = Measured and

Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value using a discount

rate of X%, P&P = Proven and Probable, PEA = Preliminary Economic Assessment,

PFS = Pre-Feasibility Study]

*Almaden Minerals (AAU) will begin trading 'ex' the Almadex

spinout on Monday 10th August. AAU shareholders of record on 7th August are now

also shareholders of Almadex, which should soon begin to trade on the TSXV under

the symbol AMZ.

We own AAU shares and intend to hold our AMZ shares for now. In fact, if they

trade at a low enough price we might even add to our AMZ position. However, AMZ

is too small and will almost certainly be too illiquid to go into the TSI Stocks

List, so for TSI record purposes we will assume that the AMZ shares are sold on

the market and treat the proceeds of the sale as a dividend. Also, we will put

AMZ in the TSI Small Stocks Watch List.

*Energy Fuels (EFR.TO, UUUU) published its financial report for

the quarter ending 30th June. The report shows that EFR's balance sheet remains

healthy, with US$41.5M of working capital. This means that the company added

about $7M to its working capital during the quarter, which is both a

satisfactory and an expected result following the $3M decline in working capital

during the March quarter. However, due to the takeover of Uranerz during the

quarter and the assumption of Uranerz's liabilities, EFR's long-term debt has

risen from $14M to $31M.

EFR offers substantial leverage to the uranium price and should be an

exceptional performer during the next cyclical advance in the uranium market,

but at an operational level the leverage won't start to kick-in until the

uranium price rises above $50/pound. In the meantime the company is in a holding

pattern, generating enough cash by selling into its long-term contracts (at

$59/pound) to maintain a healthy balance sheet.

*McEwen Mining (MUX) published its financial report for the June

quarter. There was nothing new of interest in the report as the important

information was announced in an earlier press release.

MUX's 100%-owned El Gallo gold mine in Mexico is operating very well and is

strongly cash-flow positive at the current gold price, whereas its 49%-owned San

Jose gold-silver mine in Argentina is struggling. The net result is a

gold-mining company that is doing slightly better than holding its financial

ground in today's challenging market environment.

The company has been adding cash to its balance sheet and presently has about

US$32M of working capital and no long-term debt.

*Pretium Resources (PVG) published its financial report for the

June quarter. The report showed that the company spent money rapidly during the

latest quarter, causing its working capital to plunge from C$103M at 31st March

to C$61M at 30th June. There was a $7M equity financing during the period, so

PVG managed to consume almost C$50M of working capital in a single quarter. This

is extraordinary given that mine construction hasn't yet begun.

Most of the spending came under the general category of "Mineral Interests" and

was spread between "Camp and surface activities", "Engineering and permitting"

and "Underground and surface exploration". Some of last quarter's spending

should be part of the Brucejack project's initial capex, but no details were

provided in either the financial statements or the MD&A.

Due to the surprisingly-large amount of money spent by PVG last quarter, the

company will probably have to do a larger equity financing than we were

anticipating (along with the expected debt financing) to fund the >$700M initial

Brucejack capex. We suggest holding off on any new buying of PVG shares until

the construction-financing package is put to bed.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI stock selections the best candidates for new buying

at this time, listed in alphabetical order, are:

1) DNA.TO (last Friday's closing price: C$0.84)

2) EDV.TO (last Friday's closing price: C$0.53)

3) EVN.AX (last Friday's closing price: A$0.94)

4) MUX (last Friday's closing price: US$0.70)

5) PG.TO at around C$2.00 (last Friday's closing price: C$2.12)

Note that the above list is limited to five stocks. It will sometimes contain

less than five, but it will never contain more than five regardless of how many

stocks are attractively priced for new buying.

Additional notes regarding the above list:

1) As stated at the top, the list is in alphabetical order. This means that the

order in which the stocks are displayed does not reflect priorities for new

buying. For example, we've made it clear in commentaries over the past few weeks

that Premier Gold (PG.TO) should have been the top priority for new buying for

anyone looking to increase their exposure to exploration-stage gold-mining

stocks during the sector-wide price collapse, but due to its symbol if it is on

this list it will usually be closer to the bottom than the top.

2) The list is based on relative appeal at current prices and takes into account

valuation, the price chart (including overbought/oversold indicators), and

potential catalysts. For example, Almaden Minerals (AAU) was in the list last

week because the stock was near the bottom of its price channel and was

scheduled to trade 'ex' the Almadex spinout at the end of the week. It is not in

the list this week because the opportunity to participate in the Almadex spinout

has passed and because the stock price is now close to the top of its price

channel having gained 24% last week.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.sharelynx.com/

http://www.barchart.com/