--

Weekly Market Update for the Week Commencing

10th October 2016

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Bullish

(10-Oct-16) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Neutral

(17-Aug-16) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Bearish

(19-Oct-15)

|

Bearish |

|

Stock Market (DJW)

|

N/A |

Bearish

(19-Sep-16)

|

Bearish |

|

Gold Stocks

(HUI)

|

N/A |

Bullish

(10-Oct-16) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Neutral

(10-Oct-16) |

Bullish |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

Inflation has always been about theft

Wearing blinders when analysing China

Summary of current

thinking/positioning

1) No longer hedged via put

options against short-term downside in gold and the associated mining

stocks (due to options having been exited in response to last week's price

plunge), but still hedged via a substantial cash reserve. Expecting large

gains in gold-related investments over the next two years, but not

expecting much with regard to the next 6 months.

2) Gradually

increasing exposure to non-gold commodity-related stocks during periods of

price weakness in anticipation of 2017-2018 being a very bullish period

for commodities. Thinking that the early-2016 lows could be tested prior

to the start of the aforementioned bullish period.

3) Still betting

(via options) on a near-term decline in the US stock market while

continuing to acknowledge that October-2016 could produce a stock-market

high (as per 2007) rather than the short-term low we are positioned for.

The market will almost certainly 'tip its hand' this week.

4)

Thinking that the Yen is topping, that the commodity currencies are still

in consolidation mode with a risk of testing their early-2016 lows, and

that following last week's breakdown the British Pound will soon (within

the next few months) make a low of similar magnitude to the major bottom

of early-1985.

5) Maintaining a large cash reserve in recognition

of the downside risk in almost all equities (current cash percentage is

around 50%), but looking for opportunities to reduce cash and add to gold

plus commodity exposure.

The ECRI's

Leading Indicators

A private organisation called

the Economic Cycle Research

Institute (ECRI) has been making economic growth and "inflation"

forecasts for decades. Its forecasting record is far from perfect, but it

is vastly superior to that of the Federal Reserve.

Here is a chart

from the ECRI's web site showing an index designed to predict the rate of

US GDP growth. The index has just moved to an 8-year high, although in its

commentary the ECRI cautions that this optimistic growth prediction should

not be taken at face value due to the distortions caused by Fed policy.

For example, thanks to the desperate grab for yield prompted by the Fed,

credit spreads are generally much narrower than they should be. According

to the ECRI, when all data are taken into account the expectation is for

continuing lacklustre economic performance.

And here is a chart that we created to compare the ECRI's Future

Inflation Gauge (FIG) with the Fed Funds Rate target. This chart's message

is that "price inflation" will soon begin to pick up and that the Fed is

now so far 'behind the curve' that 'the curve' cannot even be seen from

where the Fed is positioned.

If the FIG is correct then the T-Bond

yield will be a lot higher in a year's time than it is today.

The T-Bond

Whipsaw

In September, the iShares 20+

Year Treasury ETF (TLT) broke below lateral support at 137 and plunged to

around 133. It then rebounded. A counter-trend rebound within an on-going

downward trend 'should' have ended at or below 137, which means that TLT

signaled an end to its downward trend when it rose to around 139 in

late-September. However, it has since dropped sharply and tested its

September low of 133 last Friday.

If 133 gives way in the near

future then the short-term target will be support at 127-128.

We will be surprised if TLT does any worse than test the 127-128

support range over the remainder of this year, but the potential exists

for it to trade a lot lower within the coming 12 months.

The Stock Market

The US

Valuation is the elephant in the room

The absence of earnings growth for almost 2 years and the likelihood

that earnings growth will remain weak over the quarters immediately ahead

would not be a good reason to shun the US stock market if the lack of

growth was factored into current prices. The problem is that according to

the most reliable measures, the current valuation of the US stock market

is near an all-time high.

On a market-wide basis one of the best

valuation measures is the price/sales (or price/revenue) ratio. The

price/sales ratio is much better than the popular price/earnings ratio for

three reasons.

First, earnings can be manipulated by accounting

tricks to a far greater extent than sales.

Second, earnings are

strongly influenced by profit margins, which are mean-reverting. To

further explain, unusually-high profit margins will result in earnings

being unusually-high relative to sales and will therefore make

price/earnings ratios look more attractive than price/sales ratios, but

unusually-high profit margins are NEVER sustainable.

Third, in

extreme situations such as occurred during 1930-1932 and 2008-2009, a

collapse in stock prices can go hand-in-hand with an even greater collapse

in earnings. This causes the average price/earnings ratio to spike upward,

creating the impression that valuations are becoming much higher at the

very time they are actually becoming much lower.

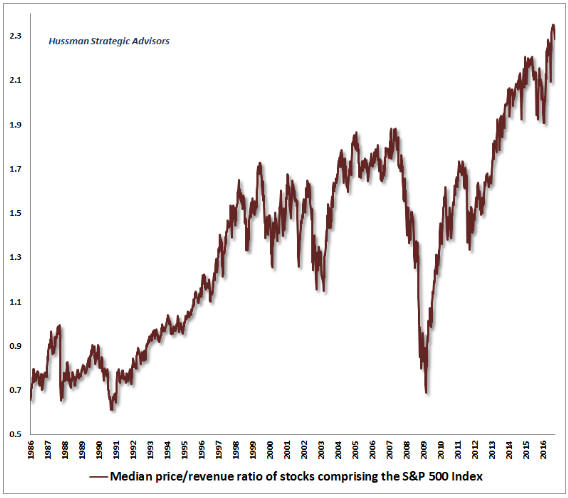

The following

chart from a

recent article by John Hussman shows that the median price/sales ratio

of the stocks that comprise the S&P500 Index (SPX) is at an extreme. In

particular, it shows that the median SPX stock is much more expensive now

than it was at the major stock market peaks of 2000 and 2007.

Current Market Situation

Although the senior US stock indices only had to move by small amounts to

the upside or the downside last week to effect breakouts, they managed to

avoid breaking out. While it is technically possible that they will also

avoid breaking out this week, they will have to trade sideways to do so.

The Dow Industrials Index, for example, will have to remain very close to

its current level of 18240 on a daily closing basis throughout this week

to avoid breaking above the downward-sloping trend-line from the August

high or the upward-sloping trend-line from the September low.

The Dow Transportation Average (TRAN) remains close to important

resistance at 8150. If it can achieve a weekly close above 8150 it will

remove the US stock market's only significant bearish divergence.

Naturally, a downward reversal from near the current level will leave this

divergence intact.

We expect that there will be quick 1-2 week moves in the senior stock

indices in the direction of the eventual breakout. After the breakout

occurs we will consider the implications.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday October 10 |

No important events scheduled |

| Tuesday

October 11 |

No important events scheduled |

|

Wednesday October 12 |

FOMC Minutes |

|

Thursday October 13 |

Import and Export Prices

Treasury Budget |

|

Friday October 14 |

PPI

Retail Sales

Business Inventories

Consumer Sentiment |

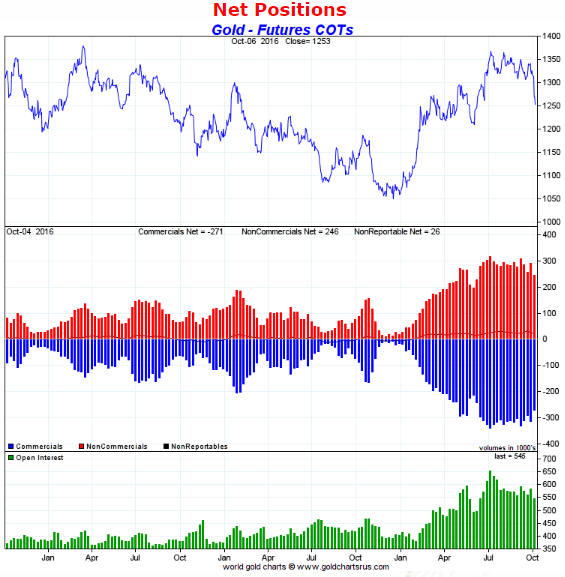

Gold and the Dollar

Gold

Last week's quick decline by the US$ gold price to the vicinity of its 200-day

MA wasn't a surprise. It certainly wasn't a guaranteed outcome (there were other

realistic possibilities), but it was the most likely outcome. Importantly, it

has significantly reduced both the short-term and the intermediate-term risk.

Support in the low-$1200s defines the short-term downside risk, in our

opinion. This is only about 3% below Friday's low of $1243.

Our view is that the gold price either made a short-term bottom at $1243 on

Friday or will make a short-term bottom somewhere in the $1200-$1243 range

within the next two weeks. A 1-2 month rebound will probably then get underway,

but we expect that the overall correction will extend into the first quarter of

next year.

One reason to expect that there will be several more months

of corrective activity is that there has not yet been a meaningful improvement

in the Commitments of Traders (COT) situation. As illustrated below, at this

stage there has been only a modest tapering of the speculative net-long

position.

Chart source:

http://www.goldchartsrus.com/

Another reason is discussed in some

detail in the Gold Stocks section below, which is that corrections following

strong intermediate-term advances usually take a certain amount of time in

addition to a certain amount of price weakness. A typical amount of price

weakness (the decline to the 200-day MA) has already occurred, but there has

been insufficient time since the peak for a new intermediate-term advance to

begin.

Silver

Silver is in a similar position to

gold, having broken below critical support last week and plunged to the 200-day

MA. We think that support at $16 defines the short-term downside risk, although

it's possible that a short-term bottom is already in place.

Platinum

The $1200 support level for gold and the $16

support level for silver are equivalent to the $950 support level for platinum.

The following chart shows that platinum has already reached this support.

At current prices platinum is a better investment than either gold or

silver. This is partly because the platinum price has already dropped back to

support defined by its May low, but mainly because the platinum price is near

the bottom of its 30-year range relative to both gold and silver. Here's a

long-term weekly chart of the platinum/silver ratio.

The long-term risk with platinum is lower demand from the automotive

industry as the increasing popularity of electric cars reduces the production of

catalytic converters (platinum's use in autocatalysts accounts from about 40% of

the metal's global consumption), but other sources of demand will potentially

offset reduced demand from the auto industry. For example, if inflation-fear

starts to pick up then increasing speculative demand for platinum as an

inflation play could swamp any decline in the auto industry's use of the metal.

Also worth mentioning is that the platinum market lives hand to mouth

(demand is mostly satisfied by current mine output) and that more than 70% of

the world's platinum supply comes from South Africa. This creates the potential

for something that is impossible in the gold and silver markets: a supply shock.

Gold Stocks

Current Market

Situation

Our view was that a gold-market correction would likely

result in the gold price dropping back to its 200-day MA and that this would

cause the HUI to drop back to support in the 190s. As illustrated by the

following chart, the most likely level for a HUI correction low was touched on

Friday 10th October. Does this mean that a multi-month price bottom is in place

and that the correction is over?

A

multi-month price bottom could be in place, but there are other realistic

possibilities and we don't have a strong opinion on the matter. More

importantly, even if a multi-month price bottom is in place it's unlikely that

the overall correction is complete. We'll now explain what we mean.

First, a strong employment report and a resultant sharp decline in the gold

price last Friday would have greatly increased the probability that the

short-term sell-off was over and that a tradable 1-2 month rally was about to

begin. Instead, there was a 'so-so' employment report and a flat day for gold

bullion and the gold-mining indices. This leaves the door open for the HUI to

spike to a new correction low before making a short-term bottom -- either

immediately or following a multi-day consolidation. That being said, if a

short-term bottom is not already in place then it will probably be put in place

within a few percent of last Friday's low.

Second, while corrections that

follow the sort of gold-sector rally that occurred during January-August of this

year can make their price lows within two months of the top, it usually takes at

least 6 months for the overall period of corrective activity to end. The two

most relevant examples from history are the 2001 and the 2002-2003 corrections.

If this year's rally was the first intermediate-term upward trend in a new

cyclical bull market then the most relevant comparison is with the correction

that began at the May-2001 peak. As illustrated below, for all intents and

purposes the 2001 correction bottomed in price terms within two months of the

peak, but it didn't end until about 6 months after the peak (November-2001).

Furthermore, it was almost 9 months after the May-2001 peak before the bull

market made a new high.

The most relevant comparison may well be with the 2001 correction, but the

price action since the August-2016 peak is more similar to the price action

following the June-2002 peak than the price action following the May-2001 peak.

In particular, whereas it took 6 months for the HUI to reach its 200-day MA

after peaking in May-2001, as has occurred this time around the 200-day MA was

reached during the 2002-2003-correction's initial 2-month decline.

The

following chart shows that the price low of the 2002-2003 correction was put in

place within 2 months of the June-2002 peak, but that corrective activity

continued until March-2013 and that it took almost a year for the bull market to

make a new high.

The lesson from 2001-2003 is that the HUI's next intermediate-term upward

trend won't begin until at least the first quarter of 2017 and that a sustained

break above the August-2016 peak won't happen until at least the second quarter

of 2017. In the meantime there will probably be one or two tradable 1-2 month

rallies followed by pullbacks to the 200-day MA or lower.

That's

assuming we are dealing with a new cyclical bull market, which is the most

likely scenario but far from a certainty.

The case against the

new-bull-market scenario has two supports. First, gold's 'true fundamentals'

have not yet turned definitively bullish. There have been times over the past 12

months when the fundamental scales were tipped in the bullish direction, but the

bullish skew was never decisive and never sustained beyond 2-3 months. Second,

of all the gold-mining rallies from multi-year price lows, in terms of raw price

action the one that began in January of this year continues to most closely

resemble the one that began in 1982. This is a cause for concern because the

1982-1983 rally was a rebound within a bear market.

Here's our updated

chart comparing the HUI from its January-2016 bottom (the blue line) with the

Barrons Gold Mining Index (BGMI) from its 1982 bottom. In percentage terms, this

year's rally didn't quite match the rally from the 1982 bottom, but the timing

of the peaks was nearly identical. If the timing of a multi-month price low is

also identical then the HUI will achieve it lowest weekly close on 21st October.

The best thing about the current situation is that regardless of whether we

are dealing with an intermediate-term bull-market correction or a bear-market

rebound along the lines of 1982-1983, a tradable 1-2 month up-move will probably

soon begin.

What are we doing?

We are hoping for some additional near-term weakness in the gold-mining sector.

The reason is that we had several under-the-market buy orders in place for

gold-mining stocks last week and only one of these orders was filled. However,

we have no intention of being aggressive in our efforts to boost our gold-mining

exposure, because if the prices at which we want to buy aren't reached over the

coming 1-2 weeks then they will probably be reached when the October low is

tested late this year or early next. Furthermore, we have our 'core' exposure to

cover us in the unlikely event that an intermediate-term rally begins without

the expected additional corrective activity.

The Currency Market

Foreign exchange reserves, what are they good for?

Absolutely nothing! Well, that's not entirely true. They can be used to

manipulate exchange rates, but they serve no genuinely-useful purpose.

Many commentators speak of the US dollar's reserve status as if it is bestowed

upon the US currency by governments, central banks and/or supranational

organisations, and as if the so-called reserve status causes the international

demand for the US$ to be much greater than would otherwise be the case. However,

this line of thinking is back-to-front. The cause-effect relationship is

actually the other way around.

The fact is that the US$ is by far the

most popular reserve currency BECAUSE it is by far the most widely used/accepted

currency for international trading and investing. Official institutions have no

say in the matter. In other words, the cause is the US dollar's popularity

within the private sector as an international medium of exchange and the effect

is the US dollar's domination of foreign exchange (FX) reserves in the coffers

of central banks.

The situation is easier to understand if the true

purpose of FX reserves is appreciated.

Under the monetary system in place

for the past few decades, FX reserves are not held for the purpose of backing a

currency (the value of a country's money has nothing to do with the amount of FX

reserves held by the country's central bank). Furthermore, FX reserves will not

automatically accumulate at the central bank of a country running a trade

surplus.

What happens is that FX reserves are bought by central banks as

part of a misguided effort to obtain a trade advantage. Specifically, FX

reserves are purchased using local currency created out of nothing, which puts

downward pressure on the exchange rate of the local currency and supposedly

gives the local economy an advantage by cheapening its products on international

markets. The theory behind this course of action is completely wrong, because

even if there were no detrimental knock-on effects the action would only

transfer wealth to exporters from the rest of the economy. There could not

possibly be an economy-wide benefit. However, the knock-on effects of the action

are more than a little detrimental, with the main issue being that the creation

of local currency out of nothing eventually and inevitably causes mal-investment

and an inflation problem.

At some point the inflation problem stemming

from the earlier efforts to lower the exchange rate via the accumulation of FX

reserves becomes the central bank's top priority. At this point the local

currency's exchange rate will be in a major downward trend and the central bank

will start selling FX reserves (and buying the local currency) as part of an

effort to address the inflation problem.

The process repeats over and

over again, with FX reserves first bought using newly-created local currency in

an attempt to gain a trade advantage and then sold in an effort to support the

local currency after the earlier monetary inflation naturally leads to major

economic problems. For a specific example, refer to Brazil's experiences over

the past 12 years.

As long as they remain guided by wrongheaded Keynesian

and Mercantilist theories, central banks will have no choice other than to

denominate most of their FX reserves in the most commonly-used currency for

international trade. All other considerations, including the composition of the

SDR, will be irrelevant.

The Pound gets pounded

The British Pound broke below the bottom of its 3-month range early last

week, with the catalyst for the breakdown being confirmation that Britain's

formal separation process from the EU would begin at the end of the first

quarter of next year. The selling then fed on itself, especially after German

Chancellor Merkel suggested that the EU would take a hard line in the

negotiations with Britain.

To add insult to injury there was even a

"flash crash" in the Pound during early Asian trading on Friday, with the

currency falling 8 cents in a matter of minutes and momentarily trading below

120 before rebounding. The "flash crash" doesn't appear on the following daily

chart, but it can be seen in a chart included in the article linked

HERE.

The following long-term monthly chart from Moore

Research Centre puts the current situation into perspective. Apart from a

few months during 1984-1985, the Pound is now trading at its lowest level

(relative to the US$) in history.

In early-1985, a waterfall decline in the Pound ended at around 104. Before

the end of 1985 the price had recovered to 140 and by early-1988 the price was

around 190.

Considering the extent to which the Pound has been driven

downward by sentiment, the speed of recovery from the next bottom could be

similar to the speed of recovery from the 1985 bottom. However, a bottom first

has to be found.

A few months ago we accumulated a long-term position in

the Pound (via a currency deposit) in the low-130s. We are interested in

doubling this position, but our plan is to wait for evidence of a turnaround

before doing so.

The way things are going, a major bottom for the Pound

will align with the prediction of a remarkably consistent 8-year cycle that

dates back to the 1976-1977 low. The cycle lows are marked by green arrows on

the above chart. The next cycle low is due in early-2017, but a low anytime

between now and mid-2017 would be a reasonable fit.

The Dollar Index

The Dollar Index broke

above short-term trend-line resistance last week, but the bigger picture is that

the choppy upward trend from the May-2016 low has done no more than take the US$

back to the middle of its 20-month horizontal trading range.

We will

remain intermediate-term neutral on the Dollar Index pending a clue as to the

direction of the eventual breakout from the horizontal range.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 7th October 2016:

Company

news/developments for the week ending Friday 7th October 2016:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, MD&A = Management

Discussion and Analysis, M&I = Measured and Indicated, NAV = Net Asset Value,

NPV(X%) = Net Present Value using a discount rate of X%, P&P = Proven and

Probable, PEA = Preliminary Economic Assessment, PFS = Pre-Feasibility Study]

*Premier Gold (PG.TO) has completed the acquisition

of the Mercedes gold mine (Sonora State, Mexico) from Yamana Gold. We discussed

the details of this acquisition in the 1st August and 8th August Weekly Updates.

The Mercedes mine has a P&P gold reserve of 400K ounces (within a 782K-oz

M&I resource) and is expected to produce 85K-90K ounces of gold per year. With

this mine and its 40% stake in the South Arturo mine operated by Barrick Gold,

PG is now a 140K-oz/year gold producer.

At the current gold price we

roughly estimate that PG's gold-producing assets are worth C$3.50/share. The

rest of PG's value is associated with its undeveloped gold-mining assets, by far

the most important of which is its 50% stake in the Trans-Canada (TC) project in

Ontario.

Based on the PEA completed way back in early-2014 and the amount

that Centerra Gold agreed to pay for the other 50%, we estimate that the TC

project is worth at least C$1 per PG share. However, it could be worth a lot

more than that. The results of the FS for this project should be published

within the next two months, enabling its value to be more accurately quantified.

List

of candidates for new buying

From within the ranks of TSI stock

selections the best candidates for new buying at this time, listed in

alphabetical order, are:

1) AAU near US$1.00 (last Friday's closing

price: US$1.22)

2) ESM.TO near C$1.00 (last Friday's closing price:

C$1.14)

3) EVN.AX near A$2.00 (last Friday's closing price: A$2.23)

3) PG.TO (last Friday's closing price: C$3.41)

4) PRQ.TO (last

Friday's closing price: C$2.05)

Note that the above list is limited to

five stocks. It will sometimes contain less than five, but it will never contain

more than five regardless of how many stocks are attractively priced for new

buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html