|

-- Weekly Market Update for the Week Commencing 10th December 2012

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

In nominal dollar terms, the BULL market in US Treasury Bonds

that began in the early 1980s will end by 2013. In real (gold)

terms, bonds commenced a secular BEAR market in 2001 that will continue

until 2014-2020. (Last

update: 23 January 2012)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2014 and 2020.

(Last update: 22 October 2007)

A secular BEAR market in the Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2014 and 2020.

(Last update: 22 October 2007)

Commodities,

as represented by the Continuous Commodity Index (CCI), commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2014-2020. In real (gold) terms,

commodities commenced a secular BEAR market in 2001 that will continue

until 2014-2020.

(Last

update: 09 February 2009)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-12 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

Bullish

(17-Oct-12)

|

Bullish

(26-Mar-12)

|

Bullish

|

|

US$ (Dollar Index)

|

Bearish

(29-Oct-12)

|

Neutral

(09-Jan-12)

|

Neutral

(19-Sep-07)

|

|

Bonds (US T-Bond)

|

Neutral

(12-Nov-12)

|

Neutral

(18-Jan-12)

|

Bearish |

|

Stock Market

(DJW)

|

Bearish

(30-Jul-12)

|

Bearish

(28-Nov-11)

|

Bearish

|

|

Gold Stocks

(HUI)

|

Neutral

(05-Dec-12)

|

Bullish

(23-Jun-10)

|

Bullish

|

|

Oil |

Neutral

(30-Jul-12)

|

Neutral

(31-Jan-11)

|

Bullish

|

|

Industrial Metals

(GYX)

|

Neutral

(30-Jul-12)

|

Neutral

(29-Aug-11)

|

Neutral

(11-Jan-10)

|

Notes:

1. In those cases where we have been able to identify the commentary in

which the most recent outlook change occurred we've put the date of the

commentary below the current outlook.

2. "Neutral", in the above table, means that we either don't have a

firm opinion or that we think risk and reward are roughly in balance with respect to the timeframe in question.

3. Long-term views are determined almost completely by fundamentals,

intermediate-term views by

fundamentals, sentiment and technicals, and short-term views by sentiment and

technicals.

Economic Numbers Update

The only two regular sets of US economic

data that we pay close attention to were published last week: the monthly ISM

data on Monday and the monthly employment data on Friday. The ISM report is a

useful coincident indicator of the US economy. The employment report is a

lagging indicator that is primarily of interest to us because the financial

markets and the Federal Reserve assign great importance to it.

The Headline ISM Index dropped to slightly below 50 (suggesting contraction)

after spending a couple of months slightly above 50. This is neither here nor

there, although it is consistent with our view that the US economy is in

recession.

The New Orders component of the ISM report tends to lead the Headline index. As

a result, we pay closer attention to the New Orders index than to the Headline

index. The following chart shows the performance of the New Orders Index since

2000, with the shaded areas marking the periods when the US economy was

officially in recession. Note that a recession is usually only officially

acknowledged 6-12 months after it begins. For example, the "great recession" of

2007-2009 began in December of 2007, but it wasn't officially acknowledged by

the NBER (National Bureau of Economic Research) until late-2008. Note also that

during the first several months of a recession it is common for the vast

majority of economists and financial-market commentators to be blissfully

unaware of the recession's existence.

It turned out that the initial plunge below 50 by the New Orders index marked

the official start of the 2007-2009 recession. However, over the ensuing 6

months the New Orders index had a slight upward bias and had recovered to around

50 by June of 2008, after which it collapsed. If this pattern is repeating then

the plunge below 50 by the New Orders index in June of this year will eventually

mark the official start of a recession.

The following chart showing Real Gross Private Domestic Investment (the blue

line) and Total Non-Farm Employees (the red line) contains the most significant

evidence AGAINST our view that a recession is in progress. Notice that the blue

line made a pronounced downward reversal prior to the start of every US

recession of the past 40 years, but that the upward trend dating back to the

2009 trough was intact as at November of 2012 (the most recent point on the

chart).

An argument could be made that it is different this time, because it really is

different this time. The decline in private investment that occurred during

2007-2009 was clearly far greater than any of the earlier recession-related

declines, and 3.5 years after the official end of the 2007-2009 recession the

amount of private investment is still a long way below where it was 6 years

prior. This is different.

The bottom line is that the US economy is weak and has been weak for many

months, but the jury is still out as to whether 2012 will officially be

acknowledged as a recession year.

Looking ahead, there's no reason to expect a genuine economic recovery to begin

in the US any time soon. A genuine recovery can't begin until the Fed stops

distorting prices via its monetary machinations, but the Fed has promised that

it won't stop distorting prices until it sees evidence that a genuine recovery

has begun. A classic "Catch 22".

The outcome of this week's

FOMC meeting will be interesting

In the 29th October Weekly Update, we wrote:

"Whereas last week's FOMC statement was almost an exact copy of the preceding

one, there's a good chance that the next statement, which will be published on

12th December, will contain some significant changes. This is because the Fed's

"Operation Twist" (selling short-dated Treasury securities and using the

proceeds to purchase long-dated securities) is scheduled to conclude at the end

of this year and probably can't be extended due to a lack of short-dated

securities. That is, one string of the Fed's 'policy accommodation bow' will

soon be no more. The question is: will the Fed find a new string to replace the

one that can no longer be used? The answer is: probably, but we should know for

sure on 12th December."

When the Fed introduced a new inflation program in mid-September the main

inflation plays (gold, silver and gold-mining stocks) were 'overbought'. This

paved the way for a post-news decline, even though the bulls got what they

wanted from the Fed. The current situation is different, in that gold and silver

are neutral (neither 'overbought' nor 'oversold') and the gold-mining sector is

very 'oversold'. This means that there is likely to be a strong upward reaction

in these markets IF the Fed announces a new inflation program or the expansion

of its existing program at the conclusion of this week's FOMC meeting.

We wish we knew what the Fed was going to do. The only thing we can be certain

of is that Bernanke and Co. will not take any steps to tighten monetary policy.

Money Supply Instability

According to a recent comment by a

well-respected analyst, one of the problems with using gold as money is that the

supply of gold could experience large swings due to changes in mine production.

The ignorance reflected by this comment is simply breathtaking. The usual

complaint about using gold as money is that the supply of gold doesn't increase

fast enough to facilitate strong economic growth, as if producing more stuff

requires more of the general medium of exchange. To know why the 'insufficient

rate of supply growth' complaint is bogus you must have a basic understanding of

good economic theory, which most people don't have. However, to know why the

'large swings in gold supply' complaint is bogus you only have to take a cursory

glance at some charts. It seems that the analyst mentioned above didn't even

bother to take a cursory glance at some charts before spreading what is, to put

it politely, misinformation.

The charts of relevance show what tends to happen to money supply under the

current global monetary system, that is, under a system where the money supply

is primarily determined by a central bank. But before we get to these charts,

let's briefly consider the global supply of gold.

Over the past 100 years the total aboveground supply of gold increased at

1.5%-2.0% per year, year in year out*. On the occasions when the growth rate

moved out of this range, it was only ever by a small amount. There were periods

of larger increases in gold production during the 1800s and early-1900s due to

major high-grade gold discoveries and the invention of the cyanide leaching

process, but the current trend is towards marginally lower global gold

production. In any case, even if we make the unrealistic assumption that an

amazing new technological advance will allow the global gold mining industry to

double its annual output, the result would only be an increase in the gold

inflation rate from around 1.5%/year to around 3%/year.

So, the global gold supply will probably continue to increase at around

1.5%/year, but under an absurd scenario could possibly increase as rapidly as

3%/year. It will never decline, because for the same reason that gold can't be

created out of thin air it can't disappear into thin air. How does this compare

with our fiat money?

Here are a bunch of charts that show how it compares, beginning with a chart

prepared by

Mike

Pollaro that reveals the year-over-year (YOY) rates of growth in the

supplies of the US$ (identified as TMS2 on the chart), the euro, the British

Pound and the Yen. The chart shows that with the exception of the Yen, the

annual rate of supply growth in the world's major currencies has, since 2000,

oscillated between -3% to 2% at the low end and at least 18% at the high end.

The Yen has been more stable in that its growth rate has oscillated between -1%

and 5%.

Turning to some other currencies, the following charts show that:

1) Since the beginning of 2000 the YOY rate of growth in the Australian True

Money Supply (TMS) has gone from 15% down to 0% up to 26% down to 7% up to 26%

down to -3% (a brief period of monetary deflation) and finally up to the 5%-10%

range where it remains today. And the Reserve Bank of Australia is generally

considered to be one of the most prudent central banks!

2) The YOY rate of growth in the Brazilian TMS has swung wildly between 0%-7% at

the low end and 20%-30% at the high end.

3) The YOY rate of growth in China's M1 money supply spent the first seven years

of the last decade oscillating between 10% and 20%. The swings then became even

larger, with a decline to 6% in late-2008 and then a moonshot to almost 40% in

early-2010 followed by a decline to 3% in early-2012.

4) The YOY rate of growth in South African TMS has been all over the place. The

South African economy has been careening between monetary deflation and rapid

monetary inflation.

And some people have the nerve to claim that money-supply instability is a risk

posed by a gold standard!

Large changes in the money supply get in the way of economic progress and always

end up occurring when central banks and/or governments have the power to

determine the money supply.

*As we've explained in many previous commentaries, this is

why changes in mine production can safely be ignored when attempting to predict

the future performance of the gold price.

The Stock

Market

Germany's stock market broke above its

September-2012 high last week and is now slightly below resistance defined by

its 2011 high. It is short-term 'overbought', having risen in almost a straight

line from its mid-November low.

France's stock market also broke above its September-2012 high last week, but

remains well below last year's high.

In the US, the period of uncommonly-low volatility that began in August shows no

sign of ending. As illustrated by the following chart, the VIX remains near the

bottom of its 4-year range.

Periods of low volatility are followed by large increases in volatility, so we

can be sure that a volatility surge is coming. The timing is the big unknown.

Based on what had happened during 2010 and 2011 we thought that the next

volatility surge would have commenced by now. That it hasn't commenced yet

doesn't mean that the danger has passed. It means that the danger still lies

ahead.

This week's

important US economic events

| Date |

Description |

| Monday Dec 10 |

No important events scheduled

| | Tuesday Dec 11 |

International Trade Balance | | Wednesday

Dec 12 |

FOMC Statement and Bernanke Press

Conference

Import and Export Prices

Treasury Budget | | Thursday

Dec 13 |

PPI

Retail Sales

Business Inventories

|

| Friday Dec 14 |

CPI

Industrial Production

|

Gold and

the Dollar

Gold and Silver

By late November the silver market had become 'overbought' on a short-term

basis. It has since been working off this 'overbought' condition via what looks

like a routine correction.

It's a similar story with the silver/gold ratio. Silver/gold had become

short-term 'overbought' by late November and is now in the process of

'correcting'. There is nothing in the price action to indicate a trend reversal.

To put it another way, the decline of the past two weeks looks more like a

counter-trend move within a continuing short-term upward trend than the first

leg of a new downward trend.

Silver and gold have 'corrected' in normal fashion up until now. Unfortunately,

the same cannot be said for the gold-mining sector.

Gold Stocks

The difficult market for junior gold miners

From Canaccord's latest "Junior Mining Weekly" letter:

"We track a group of 40 non-producing junior gold companies with NI 43-101

compliant resource bases to estimate an average in situ market value per ounce

of gold resource. Today, the average in situ value per ounce is US$67.12/oz. In

late 2010, the average in situ market value per ounce was US$161.98/oz. So from

December 31, 2010 to November 30, 2012, the average in situ value per ounce has

dropped 58.6%, despite a 19.0% increase in the price of gold over the same

period of time. This is an average in situ value; however, every deposit is

different and not all discoveries are created equal. In December 2010, the in

situ market value per ounce ranged from a low of US$6.75/oz to a high of

US$399.56/oz with 16 out of 38 companies trading above US$100/oz. Today, the in

situ value per ounce ranges from a low of US$5.52/oz to a high of $226.64/oz

with only seven out of 40 companies trading at an in situ value of more than

US$100/oz. We are simply not seeing the same level of market response to drill

results and resource expansion in the current risk averse environment. This

year, it has been more common for positive drill results to be met with a ho hum

response in the market."

Displayed below is Canaccord's chart illustrating what was described above.

Notice the divergence between the gold price (the orange line) and the average

per-ounce market value of in-ground gold (the vertical bars) that commenced in

early-2011.

What caused this divergence and when is it likely to end?

There are many answers to the first part of this question, including rising

production and capex costs. For exploration/development-stage juniors, the large

increase in the cost of building a new mine, as exemplified by the massive

increase in the cost budgeted by Barrick Gold to build the Pascua Lama mine, has

become a major issue. That's why a number of juniors with large low-grade

deposits are changing tack. Two years ago they were focused on maximising the

deposit size and the scope of the proposed mining operation. Now they are

focused on maximising profit per ounce and minimising initial capex. Keegan

Resources (KGN) is a good example. Keegan's Esaase project would only have a

small chance of progressing to the construction phase based on the mine plan

that was envisaged at the time of the 2011 PFS, but based on the new plan

involving a smaller-scale higher-margin operation there's a high probability of

a mine being built within the next few years. However, not all projects are

amenable to such a change. The Donlin Creek project of NovaGold/Barrick and the

Caspiche project of Exeter Resources, for example, have little hope of entering

the mine-construction phase in the foreseeable future. Other projects, such as

those controlled by International Tower Hill Mines and Volta Resources, could

still be viable under the challenging market environment of today, but more

engineering work will be required to determine if this is the case.

Another answer is that most of the senior producers haven't been able to

translate the higher gold price into meaningfully better financial performance.

This is related to the increase in production and capex costs mentioned above.

In particular, due to the sharply higher cost of building a new mine the senior

producers now have to invest a lot more money to replace previous production (as

mines get depleted, new mines must be built to prevent a decline in production).

It is also related to management errors, such as drastically overpaying for new

assets.

A third answer is that there are too many junior gold miners vying for investor

attention. Many of these companies don't have genuinely valuable assets, but

they all have good stories to tell.

A fourth answer is that there hasn't been a spectacular discovery to excite the

market. A few months ago it looked like GoldQuest had made such a discovery, but

subsequent drilling indicated that the deposit was nowhere near as impressive as

it initially seemed.

The overarching answer to the first part of the question, however, isn't

specifically related to gold mining. The reality is that although there have

been a few shifts towards risk during the period in question, the dominant theme

since early-2011 has been "risk off". This is evidenced by a series of declining

tops in the RUT/SPX ratio (small-cap US stocks relative to large-cap US stocks)

and a general widening of credit spreads.

The answer to the second part of the question is unknowable. As mentioned below

under "Current Market Situation", a 'seasonal' rally in the juniors is due to

begin during the second half of this month. It's a good bet that we'll get the

seasonal rally, but the price action of the past week has introduced a lot more

uncertainty as to what's likely to happen thereafter. Economically robust gold

deposits WILL eventually get priced closer to their true values, but

'irrational' valuations could persist for longer than expected. They already

have persisted for longer than expected.

It is said that the market can remain irrational for longer than you can remain

solvent, but this is only true if you are over-extended. If you are 'unmargined'

with a comfortable cash cushion then the limitation is probably your patience,

not your ability to remain solvent.

Current Market Situation

As discussed in last week's Interim Update, the HUI's 5th December break below

its mid-November low was a significant deviation from our favoured scenario. We

must now seriously consider the possibility that there will be a re-test of the

May-2012 low prior to the start of the next major upward leg.

A counter-trend rebound in the HUI would likely end at or below resistance in

the 460s (the horizontal green line drawn on the following daily chart).

Consecutive daily closes above this resistance could therefore be interpreted as

a signal that something more substantial than a counter-trend rebound was in

progress.

The following daily chart of the TSX Venture Exchange Composite Index (CDNX)

reflects the dismal state of affairs in the world of junior resource stocks. The

recent decline has taken the CDNX back to near its 2012 low, which was also its

low of the past three years.

A period of seasonal strength for the juniors begins during the second half of

December. This seasonal strength can last until April or May when "risk on" is

dominating, but even when the markets are in "risk off" mode the strength

usually lasts until February.

Currency Market Update

There was more than the usual amount of volatility in the currency market on

Friday. The Dollar Index initially surged in reaction to a bearish assessment of

the euro-zone economy and better-than-expected US employment data, then gave

back all of its gains and finally strengthened a little to end the day slightly

higher than where it had been 24 hours earlier.

Sentiment indicators suggest the potential for the Dollar Index to move to a new

multi-month low and the euro to move to a new multi-month high before we get the

next meaningful shift in relative strength. Of particular relevance: although

the speculative net-short position in euro futures has fallen a long way from

its early-June high, speculators are still betting against the euro.

The Dollar Index has nearby support at 79.5. A daily close below this support

would suggest that it was on its way to 77-78.

Update

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ended Friday 7th December 2012: Company

news/developments for the week ended Friday 7th December 2012:

[Note: FS = Feasibility Study, IRR = Internal Rate of Return, MD&A =

Management Discussion and Analysis, M&I = Measured and Indicated,

NAV = Net Asset Value, NPV(X%) = Net Present Value using a discount

rate of X%, P&P = Proven and Probable, PEA = Preliminary Economic

Assessment, PFS = Pre-Feasibility Study]

*Clifton Star Resources (CFO.V) reported drilling results from its

Duparquet project in Quebec. The results were generally good. They

suggested the potential to expand the pits in the current mine plan

and to add resources between the currently-proposed pits. Of

particular note were an exploration hole that intersected 3.51-g/t

gold over 18.9m and an in-pit hole that intersected 4.77-g-t gold

over 14.1m. Two drills continue to operate at Duparquet with the

primary objective to convert Inferred resources to M&I resources.

The first indication of the economics of the Duparquet project will

come by way of a PEA early next year.

*Dragon Mining (DRA.AX) advised that it had received the revised

environmental permit for its Svartliden gold mine in Sweden.

According to the company's press release, this means that

underground mining can commence as scheduled this month.

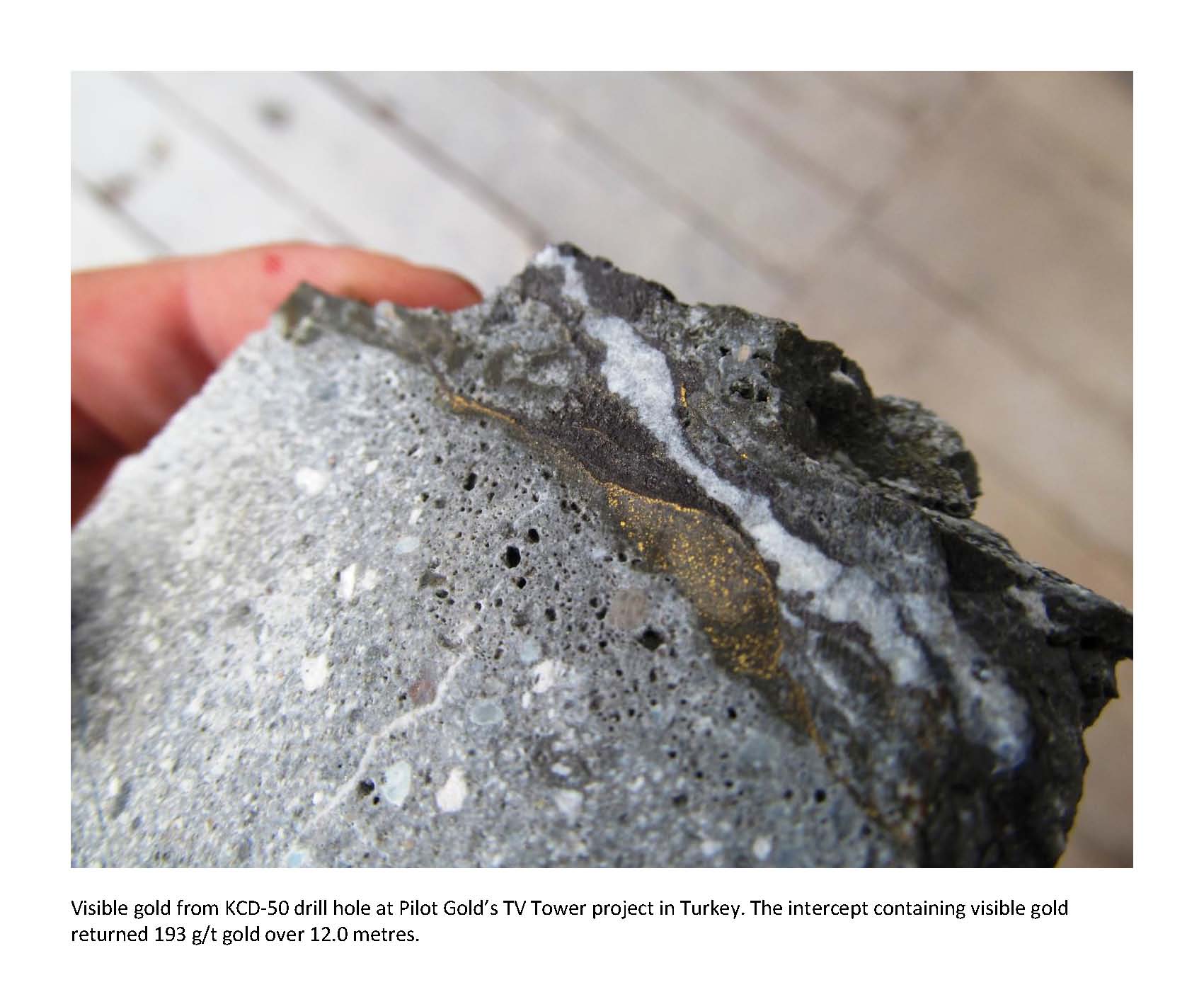

*Pilot Gold (PLG.TO) reported more drilling results from its TV

Tower gold project in Turkey. Included in these results was an

extraordinary gold intercept grading

193-g/t

over 12m in hole KCD-50. Hole KCD-50 was collared 70m to the

northwest of hole KCD-39, which also contained an extraordinary gold

intercept (5.94 g/t gold over 137m, reported in September). Other

notable intercepts in the latest batch of results were 2.11 g/t gold

over 43.1m and 2.69 g/t gold over 22.5m in hole KCD-58.

The TV Tower project is shaping up to be something special.

Drilling is on-going at TV Tower and assay results are currently

pending for 24 holes, so there will be a steady stream of drilling

news from PLG over the weeks and months ahead.

The TSI Stocks List has exposure to PLG via the $2.20 warrants that

expire in 2014, but at current prices (C$1.88 for the stock, C$0.53

for the warrants) the stock offers the better value. The value

difference isn't enough to justify selling the warrants and buying

the stock, but for new buying at this time the shares would be

better than the warrants.

More

on the proposed merger between Keegan Resources (KGN) and PMI Gold (PMV.TO)

Last week's most important event involving a TSI stock was the announcement that

KGN, a long-time member of the TSI Stocks List, has agreed to merge with PMV.

Last week's Interim Update contained our initial discussion of this news.

Most of our readers should be familiar with what KGN brings to the table, so

we'll now take a look at PMV's contribution to the combined company. Aside from

its $130M of cash, PMV's contribution is the Obotan project. This project's

salient details are included in a Feasibility Study completed in August-2012 and

summarised in the following table.

|

Project Name |

Obotan |

|

Location |

Ghana, West Africa |

|

Planned Mine Type |

Open Pit |

|

M&I Resource (oz) |

3.11M |

|

Avg Resource Grade |

2.16 g/t |

|

P&P Reserve (oz) |

2.4M |

|

Metallurgical Recovery |

93% |

|

Strip Ratio |

5.6:1 |

|

Avg Annual Production (oz) |

200K |

|

Cash Cost (per oz) |

$626 |

|

Mine Life |

11 years |

|

Initial Capital Cost ($M) |

300 |

|

Assumed Gold Price (US$) |

1600 |

|

NPV ($M) |

686 |

|

IRR |

43% |

|

Project Ownership Percent |

90% |

|

NPV of Company Stake ($M) |

617 |

|

Current Stock Price (US$) |

0.85 |

|

Share Count (M) |

412 |

|

Current Market Cap ($M) |

350 |

|

Net Cash ($M) |

130 |

|

Current Enterprise Value ($M) |

220 |

|

EV/NPV |

36% |

|

Current Discount to NPV |

64% |

|

EV + Capital Cost (COM) |

520 |

|

COM/NPV |

0.84 |

From a valuation perspective the

final three rows of the above table are the most important. The third row from

the bottom shows the discount to the project's NPV at which the stock is

currently trading. The discount should be substantial (at least 50%), but in

today's ultra-challenging market it is not enough to trade at a large discount

to NPV. Dozens of juniors are now trading at large discounts to their NPVs.

That's why we've added the last two rows.

The second row from the bottom shows the stock's enterprise value plus the

estimated initial capital cost of its flagship project. This, in effect, would

be the total cost to an acquiring company of developing a new mine, because the

acquirer would first have to buy the current owner of the project and then pay

for a mine to be built. We refer to this as Cost of Mine (COM).

The last row compares the COM to the project's NPV. The lower this figure the

better the value and the more attractive the company will appear to potential

acquirers. If a company has a COM/NPV ratio of less than 1 at a conservative

gold price, then on a purely quantitative basis it is very attractively priced.

Note that a company could be trading at a huge discount to its NPV, but due to a

relatively high initial capex estimate its COM/NPV ratio could be well above 1.

Another company could be trading at a smaller discount to its NPV, but due to a

relatively low initial capex estimate its COM/NPV ratio could be less than 1.

All else being equal, in today's market the second company would be the better

investment.

At Friday's closing price of C$0.85/share, PMV's COM/NPV ratio was 0.84 at a

gold price of $1600/oz. This suggests that the Obotan project is attractively

valued, which is good from a KGN shareholder's perspective (our perspective). We

won't be able to do the same calculation for KGN's flagship project until the

revised PFS is issued in Q1-2013.

One final point worth mentioning is that the announcement of the KGN-PMV merger

effectively put both companies into play. A third company could enter the fray

with a bid for KGN or PMV.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.economagic.com/

http://research.stlouisfed.org/

|

{kind=link}