-- Weekly Market Update for the Week Commencing

11th July 2016

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Neutral

(27-Jun-16) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Bullish

(29-Feb-16) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Bearish

(19-Oct-15)

|

Bearish |

|

Stock Market

(DJW)

|

N/A |

Neutral

(04-Jul-16) |

Bearish

|

|

Gold Stocks

(HUI)

|

N/A |

Neutral

(04-May-16) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Bullish

(04-July-16) |

Bullish |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

The hyperinflation and deflation arguments are both wrong

Gold

is testing its 2011 high

Summary of current

thinking/positioning

1) Concerned about short-term

downside risk in gold, silver and the associated mining stocks, but

comfortable maintaining substantial 'core' exposure in anticipation of

large additional gains over the next two years. Continuing to pick away at

'special situations' -- small/illiquid gold stocks that could generate

large gains independently of sector-wide performance.

2) Building

up exposure to non-gold commodity-related stocks (primarily base-metals

producers/explorers, but also energy and agriculture companies) and hedged

against short-term weakness via XME put options.

3) Thinking that

the US stock market is unlikely to do much on either the upside or the

downside over the coming 1-2 months.

4) Thinking that industrial

commodities (oil, copper, platinum, etc.) and the main commodity

currencies (A$, C$) made long-term bottoms during Q1-2016. The bottoms

could be tested during the second half of this year as part of a basing

process, but prices are likely to be markedly higher a year from now.

5) Thinking that something will soon have to give, because T-Bonds,

the US stock market and gold are all now 'overbought' and at/near

multi-year highs.

6) Anticipating a tradable decline in the T-Bond

and averaging into TBT call options in an effort to profit from the

decline.

7) Maintaining an unusually-large cash reserve in

recognition of the downside risk in almost all equities, but gradually

reducing the cash percentage via the accumulation of non-gold commodity

stocks.

Commodities

Copper

The top section of the following chart shows that copper remains in

consolidation mode in US$ terms. It needs to achieve a weekly close above

US$2.30 to signal an intermediate-term trend reversal, although a daily

close above $2.25 would be an early warning that such a reversal was in

the works.

The bottom section of the same chart shows that copper

remains in a major downward trend relative to gold. In fact, at the end of

last week the copper/gold ratio was close to the multi-decade low reached

near the climax of the Global Financial Crisis in early-2009. This

suggests that either gold is very expensive or copper is dirt cheap. A bit

of both, we think.

Copper is probably in the process of turning upward on an

intermediate-term basis in US$ terms and close to a bottom in gold terms.

This is related to the likelihood that the T-Bond is close to an important

peak, in that copper's current downward trend relative to gold is linked

to the decline in the T-Bond yield.

Oil

Based on the performances of the commodity currencies and the Yuan, the

oil price turned down within the expected time-window (before mid-June).

However, up until now the decline has been less than expected.

The

chart pattern (see below) could be interpreted as a routine short-term

correction that has almost run its course or as a market slowly rolling

over into a more substantial decline. Neither of these possible outcomes

would surprise us.

The Stock Market

The US

It is usually the case that when there is no change in the fundamentals, a

higher price means greater downside risk. The fact that the US stock

indices rose last week therefore implies that the downside risk is now a

little greater, although there is unlikely to be anything more than a

routine pullback over the next few weeks. As explained in recent

commentaries, this is because the market is displaying more internal

strength than would be the case if a large decline were about to begin.

Sentiment is another reason to be unenthused by the market's

short-term downside potential. The Brexit sell-off effectively 'cleared

the decks' of weak-handed longs, and despite the fast rebound from the

27th June post-Brexit low there still appears to be a healthy amount of

wariness in the market.

It's possible that short-term downside risk

will return to a precarious level at some point over the next two months,

but we'll cross that bridge when we come to it. In the meantime we will

probably retain our reduced position in QID (leveraged NDX bear fund)

October call options, but we won't add to the position.

In a

nutshell: It's time to focus more on accumulating exposure to

commodity-related stocks and less on bearish stock-market speculations.

Turning to the charts, the S&P500 Index (SPX) has just achieved a

weekly close above its November-2015, April-2016 and June-2016 highs, and

is now within 5 points of last year's all-time high.

The SPX is likely to make a new all-time this month, but it's unlikely

to run away to the upside anytime soon. Furthermore, there's a good chance

that new highs by the SPX and the Dow Industrials Index will not be

confirmed by some other important indices. An example is the NYSE

Composite Index (NYA).

The SPX's performance in gold terms is very different from its

performance in US$ terms. As illustrated below, in gold terms the SPX is

not far from an 18-month low.

It is worth pointing out, however,

that even in gold terms the SPX is still holding above its February-2016

bottom. Almost regardless of what happens to the nominal prices of the SPX

and gold, if we are dealing with a US equity bear market and/or a gold

bull market then the SPX/gold ratio should take out its February-2016 low

within the next few months and shouldn't move above its 200-day MA.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday July 11 |

No important events scheduled |

| Tuesday

July 12 |

No important events scheduled |

|

Wednesday July 13 |

Treasury Budget

Important

and Export Prices

Fed's Beige Book |

|

Thursday July 14 |

PPI |

|

Friday July 15 |

CPI

Retail Sales

Industrial Production

Consumer Sentiment

Empire State Mfg

Survey |

Gold and the Dollar

Gold

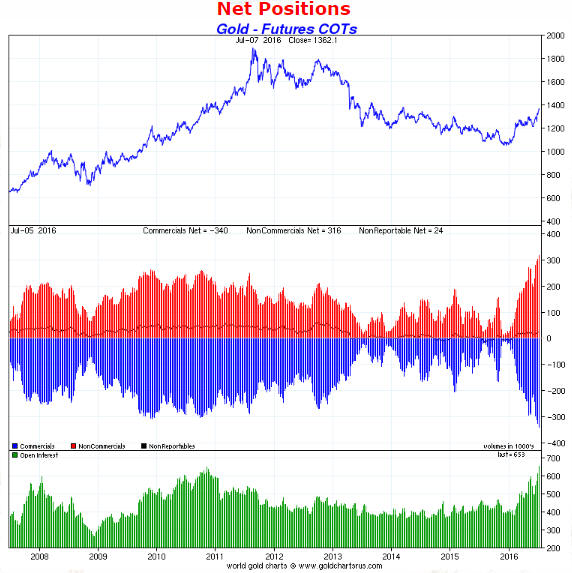

The COT Situation

The total speculative

net-long position in COMEX gold futures (the inverse of the commercial net-short

position -- the blue bars on the following chart) made a new all-time high last

week in absolute terms, although relative to open interest it is still just shy

of the extremes reached during 2006-2010.

The following excerpt from last

week's report still applies:

"The COT situation will never be the

reason for a trend reversal. Like other sentiment indicators it just creates

potential energy. The problem for gold will come when the trend reverses

downward for reasons that have nothing to do with the COT positioning and the

largest speculative net-long position in history has to quickly get unwound."

Current Market Situation

It seems

that there was something for everyone in the US Employment Report published last

Friday -- enough superficial strength to encourage the economic optimists and

enough underlying weakness to validate the concerns of the economic realists.

These differing views jostled in the currency, credit and gold markets, with the

result being significant intra-day volatility and not much in the way of net

change over the course of the trading day.

Of relevance to many financial

markets and particularly of relevance to the gold and currency markets, the

following chart of the January-2018 Fed Funds Futures (FFF) contract shows that

there was no change over the course of last Friday in market expectations

regarding the Fed's interest-rate moves. Prior to the employment news 'the

market' believed that there was only a 50% chance of a single 0.25% Fed rate

hike within the next 18 months, which is what 'the market' still believes.

Although the gold price only gained $5 on Friday, the price action was

bullish. This is firstly because the gold price dropped $25 in an initial

knee-jerk reaction to the higher-than-forecast jobs growth number included in

the US Employment Report and then quickly recouped this loss. Also, it is

bullish that last week's close was above the spike high of $1362 hit in the

immediate aftermath of the Brexit news on 24th June.

Despite the downside

risk stemming from the rampant enthusiasm of speculators in gold futures,

Friday's price action not only kept alive the possibility of a near-term rise to

$1400 but also increased the probability of such an outcome.

Gold Stocks

Last week, the HUI made its way through

long-term resistance at 250-260 as if it didn't exist.

The next

resistance lies at 280. However, the only remaining historical parallel with

this year's price action is the 1982-1983 rally, and if the HUI matches the

performance of the 1982-1983 rally then it will peak at around 300 in August.

Prior to the past few weeks we hadn't given much thought to the possibility

that this year's gold-sector rally would match the intensity of the 1982-1983

rally. This was partly because the 1982-1983 rally was an outlier in the

historical record, but it was mainly because the 1982-1983 rally was a rebound

within a bear market. The peak of the 1982-1983 rally was followed by a

multi-year downward trend rather than a multi-month correction.

Ultimately, the fundamentals will determine whether we are dealing with a new

cyclical bull market or an incredibly strong bear-market rebound. If gold's true

fundamentals become increasingly bullish over the months ahead then we are

dealing with a new bull market and it will be appropriate to buy corrections to

support in anticipation of large additional gains over the ensuing 1-2 years.

The Currency Market

Why

has the US$ been so weak?

The above question might seem strange

given that the Dollar Index has just broken above its late-May high on a weekly

closing basis, thus confirming that an intermediate-term bottom was put in place

in early-May and projecting a test of the 2015 peak within the next couple of

months. The question stems from our assessment that the Dollar Index has been

much weaker than it should have been given the fundamental backdrop, or, to put

it more accurately, the euro has been much stronger relative to the US$ than it

should have been given the fundamental backdrop.

How is the fundamental

backdrop US$-bullish/euro-bearish? Let us count the ways, from least important

to most important.

1) The European Union has started to come apart, with

the refugee/migration crisis apparently acting as the catalyst by shining a

spotlight on individual countries' loss of sovereignty. The pressure is now

building throughout Europe to hold EU-independence referenda, but there's a high

risk that, unlike the UK situation, the incumbent political leadership in most

EU-member states will not allow the pressure to be relieved via a democratic

process. This could mean that it ends up being relieved in more violent and

destabilising ways.

2) The ECB has been setting new standards in

central-banking imprudence and destructiveness. Moreover, with Mario Draghi, a

man who possesses the dangerous combination of extreme arrogance and extreme

ignorance, likely to remain at the helm until 2019, there's a high probability

that the current policy direction will be maintained.

3) The strength of

European equities relative to US equities usually determines the strength of the

euro relative to the US$. The following chart illustrates this relationship over

the past three years using the EZU/SPY ratio to indicate the relative strength

of European equities, but note that the relationship has been in force since the

birth of the euro.

With European equities having trended lower relative

to US equities since early-December of last year (as indicated on our chart by

the decline in the EZU/SPY ratio), the implication is that the euro should have

been trending downward over the past 7 months and should probably now be trading

below par. Instead, it has gained some ground.

4) According to the historical record, of equal importance to the strength

of European equities relative to US equities is the strength of the European

banking sector relative to the US banking sector. The relationship between the

euro and the strength of European banks relative to US banks is logical and is

illustrated by the following chart (the EUFN/KBE ratio is a proxy for the

relative performance of the European banking sector).

The chart displayed

below shows the same divergence over the past seven months as the chart

displayed above. It seems that the euro SHOULD have been in a powerful downward

trend during this period, but obviously it wasn't.

The question is: Why has the euro/US$ exchange rate defied the

above-mentioned fundamental forces?

One possibility is that these

euro-bearish/US$-bullish influences have been counteracted by another

fundamental factor, but this doesn't seem like a viable explanation to us. As

far as we can tell, at a fundamental level the euro had nothing going for it

over the past seven months.

We suspect that the answer to the question

has nothing to do with fundamental currency-market drivers and almost everything

to do with the overshoot that happened during the first 10 weeks of last year.

You should be able to see what we mean if you take another look at the above

charts and zoom in on the first quarter of 2015. Notice that the euro plunged

from 117 to 105 despite there being relative strength in European equities and

relative strength in the European banking sector.

Based on the most

important short- and intermediate-term drivers of the euro's performance

relative to the US$, the euro should have bottomed near the beginning of 2015 at

around 117 and the Dollar Index should have peaked at the same time at around

92. Instead, momentum-inspired speculation drove the euro down to 105 and the

Dollar Index up to 101.

Now, if currency-market fundamentals justified a

Dollar Index peak of no more than 92 in Q1-2015, then what happened over the

past seven months can be understood as a divergence that brought prices back

into line with fundamentals. In effect, the dollar's 'fundamental value' (we use

the term loosely) has been steadily rising this year but hasn't yet resulted in

a net price gain because the price was too high (relative to the euro) to begin

with.

Current Market Situation

By

ending last week above its late-May high the Dollar Index has provided evidence

that an intermediate-term bottom was put in place in early-May. Unfortunately,

the evidence was diluted to some extent by the dollar's inability to gain any

ground and close above its 200-day MA last Friday in response to a

superficially-strong US Employment Report.

Last week's breakout suggests

the potential for the Dollar Index to test its 2015 high within the coming two

months. It needs to remain above 96 on a weekly closing basis to maintain this

potential.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 8th July 2016:

Company

news/developments for the week ending Friday 8th July 2016:

*Ivanhoe Mines (IVN.TO) reported the results of initial

metallurgical tests done on a sample of drill core from the Kakula Discovery

zone at the Kamoa copper project.

The tests achieved copper recoveries of

86%, produced a copper concentrate with a high grade of 53% copper, and

indicated that material from Kamoa's Kakula and Kansoko zones (the main deposit)

could be processed through the same concentrator plant.

The results of

metallurgical testing usually don't move the stock price unless they reveal a

major problem, but this type of testing is critical and should be done early in

the exploration process. The results from metallurgical testing at Kamoa have

been positive to date.

*Pilot Gold (PLG.TO) is

mainly of interest to us because of its exploration-stage gold projects.

However, PLG also owns 40% of the Halilaga copper-gold project in Turkey (Teck

owns the other 60%). With the improving intermediate-term outlook for copper,

Halilaga becomes a more important asset and of greater interest to us.

Halilaga is a low-grade copper-gold porphyry deposit with a total resource

comprising 2.1B pounds of copper and 3.3M ounces of gold (roughly half

Indicated, half Inferred). A revised PEA completed in early-2015 suggested that

the project could be developed into a mine with robust economics at $1200/oz for

gold and $2.90/pound for copper. At these metals prices the NPV(7%) and IRR are

estimated to be US$474M and 43%, respectively. 40% of US$474M (PLG's share) is

US$190M, or about 2.5-times PLG's current market cap. Furthermore, the figures

in the revised PEA suggested that the project might still be viable at $1200/oz

for gold and $2.25/pound for copper.

If the copper price is in the

process of making a sustained turn to the upside then Halilaga is in the process

of becoming a lot more valuable, but as far as we can tell the stock market is

presently assigning almost no value to this project.

*Ramelius

Resources (RMS.AX) announced its FY2016 (1 July 2015 through to 30 June

2016) gold production and FY2017 production guidance.

Production during

the June quarter was above the top-end of the 28K-32K-oz guidance, which enabled

the company to slightly exceed its 110K-oz production guidance for the full

year. Moreover, gold production during FY2017 is expected to rise to 135K ounces

thanks to a full year's contribution of 55K ounces from the newly-commissioned

Vivien mine.

If we could be confident that RMS was going to continue

producing 110K-130K ounces of gold per year then we could justify a stock price

of A$1.00/share at the current gold price (the stock closed at A$0.56 last

Friday). However, maintaining an annual production rate in excess of 100K ounces

currently requires finding new deposits near the processing plant and bringing

new small-scale mines into operation every year or two. The lack of production

certainty when looking beyond the next 12 months warrants a discount to full

valuation, but what that discount should be is subjective.

*Resolute

Mining (RSG.AX) announced its FY2016 (1 July 2015 through to 30 June

2016) gold production and FY2017 production guidance.

The company met its

FY2016 production forecast of 315K ounces at a slightly-lower-than-expected AISC

(A$1210/oz versus A$1220/oz). FY2017 production is expected to be slightly lower

at around 300K ounces at a higher AISC of A$1280/oz (US$960).

According

to the company's press release, all of the FY2017 production from its flagship

Syama gold mine (Mali) will come from stockpiles and open-pit mining. This

implies that the Syama underground expansion won't begin to have an effect on

gold output until FY2018. Once complete, the Syama underground expansion will

boost Syama's production to 250K ounces per year (50K ounces more than the

current rate) and reduce the production cost.

RSG continues to perform

well on the ground and in the stock market. Despite the massive gains in its

stock price since the start of this year we think it makes sense to maintain

significant exposure, although a prudent speculator would have done some

profit-taking by now.

Solitario

Exploration and Royalty (XPL, SLR.TO). Shares: 39M issued, 41M fully diluted.

Recent price: US$0.79

We introduced XPL and added it to the TSI

Stocks List (at US$0.57) in the email sent to subscribers last Tuesday. Today we

are providing a bit more detail.

XPL's story is simple. The company has

two main assets, the first of which is easy to value and the second of which is

impossible to value at this time. The easy-to-value asset reduces the downside

risk while the impossible-to-value asset provides the upside potential.

The easy-to-value asset is the company's strong balance sheet. XPL has US$17M of

working capital (cash, US Treasury securities and fully-insured CDs) and no

debt. In effect, about 60% of its current market cap is covered by cash.

The impossible-to-value asset is XPL's 30% stake in the exploration-stage

Bongara zinc project in Peru. The other 70% of the project is owned by Milpo,

the second-largest zinc miner in Peru and a well-financed company.

XPL is

carried to production at Bongara, meaning that it won't have to pay anything for

the project's exploration and development until commercial production is

achieved. At that point, XPL would be obligated to start paying-off its 30%

share of the construction cost by using 50% of its share of the net proceeds of

production.

The project, however, is many years from production and at

this stage doesn't even have a PEA. That's why it is impossible to value. What

we do know is that the currently-defined resource comprises about 3.4 billion

pounds of zinc (across all categories) at a zinc-equivalent average grade of

around 13%. It's a rare project that contains a few billion pounds of zinc at

such a high grade.

Although we can't quantify the value of XPL's 30%

stake in the Bongara project it's likely that it is many times the US$10M

implied by XPL's current enterprise value.

The risk with XPL is currently

limited by the company's US$0.43/share of cash, but there are still risks.

There's the risk that management will blow the cash on an ill-conceived

acquisition. Based on past performance this is very unlikely, but it can't be

ruled out. There's the risk that Milpo will move Bongara forward at a snail's

pace due to the fact that for this relatively-large company it is just one of

several 'irons in the fire'. And there's permitting risk, which, in Peru, means

the risk that the local community will not be in favour of the project.

Unlike Taseko Mines (TGB), which was also added to the TSI List via the email

sent to subscribers early last week, XPL is not a leveraged play on base-metal

prices. It's a stock that is potentially very under-valued at current metal

prices and would be best suited to speculators prepared to wait a couple of

years (if need be) for the story to unfold.

The stock price broke out of

a basing pattern and moved sharply higher over the final four trading days of

last week, which makes it a little riskier than it was when we sent the email

last Tuesday. Based on the chart pattern the optimum place for new buying would

be around US$0.60.

New

stock selection: Sprott Resource Corp. (SCP.TO). Shares: 97M. Recent price:

C$0.60

SCP is an investment company focused at this time on

energy (oil, O&G drilling and coal) and agriculture investments. The stock looks

attractive to us near its current price for two main reasons. First, we are

becoming increasingly bullish on commodities. Second, it is trading at a

discount of almost 50% to its net asset value (NAV).

Also worth

mentioning is that SCP is one of the few stocks that provides exposure to

farming. SCP provides this exposure via its stake in "One Earth Farms", a large

privately-owned farming operation in Canada.

One risk is that SCP's

balance sheet is weak, in that at the date of the latest financial statements

(31st March) the company had almost no cash and a $16M loan due for repayment in

November. However, this risk is not a major concern because a) the loan was

provided by another part of the Sprott empire (Sprott Lending) and b) SCP has

since generated $12M of cash via an asset sale.

Another risk is that a

little more than half of the company's NAV is associated with investments in

private companies. These investments are both illiquid and difficult to value.

The opportunity here is that as sentiment towards commodity-related

investments improves, SCP's assets will increase in value and its discount to

NAV will shrink. This combination creates the potential for at least a doubling

of the stock price over the coming year or two.

Note that we don't see a

good reason to buy commodity-related stocks such as SCP with any urgency at this

time. As is almost always the case, a gradual scaling-in process would be

appropriate.

Potential

future TSI stock selection: Carpathian Gold (CPN.CN). Shares: 907M. Recent

price: C$0.075

CPN is a stock that we traded unsuccessfully

during 2011-2013. At that time the company was advancing two projects -- the

exploration-stage Rovina Valley (RV) gold-copper project in Romania and the

construction-stage RDM gold project in Brazil. We were primarily interested in

the RV project, but it was the debt taken on for the construction of RDM that

created a life-threatening financial problem for the company and prompted us to

exit with a loss.

The company now has a new lease on life. All of the

assets and liabilities associated with the Brazilian project are gone, leaving

the RV project as the only focal point. Furthermore, the Forbes and Manhattan

group has recently invested C$10M via a private placement and installed new

management and a new board of directors. A consequence is that the company is

now debt free with about C$10M of cash to be used for moving the RV project

forward.

CPN provides exposure to both gold and copper. The exposure is

highly speculative, but, unlike some other exploration-stage gold-mining stocks

that have been bid-up aggressively over the past few months, CPN's project has a

realistic chance of eventually being developed into an operating mine.

The RV project has a low-grade, porphyry-style deposit comprising 3.1M ounces of

gold and 759M pounds of copper in the M&I category plus 3.9M ounces of gold and

663M pounds of copper in the Inferred category. A PEA completed way back in

March-2010 estimated that with initial capital expenditure of $509M the project

could be developed into a mine that produced an average of 200K ounces of gold

and 50M pounds of copper per year for 19 years at a cash cost of $379/ounce

(taking copper as a byproduct). Assuming a gold price of $1000/oz, a copper

price of $3.00/pound and a conservative discount rate of 10%, the project's net

present value (NPV) was estimated to be US$544M.

The economics indicated

by the PEA are too far out of date to be relied on, but they suggest the

potential for the project to be viable at or not far from current metal prices.

As evidenced by a $20M investment made several years ago, Barrick Gold also

believed that the RV project had the potential to be economically viable.

In today's frothy market, CPN's current market cap (at C$0.075/share) of

around US$50M offers decent value given the risks. Furthermore, the stock has

reasonable liquidity in the C$0.07-C$0.08 range. However, we aren't going to add

CPN to the TSI List at this time, the reason being that it trades on a minor

Canadian exchange called the CSE. Canada-based accounts should have no trouble

trading on the CSE, but accounts outside Canada might not have access to this

exchange.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.stockwatch.com/

http://www.barchart.com/

http://www.sharelynx.com/