|

-- for the Week Commencing 11th August 2003, 2nd Page

Gold and

the Dollar

Junior Gold Stock Comparison

In the 25th June Interim Update we

included a valuation comparison of 15 junior gold stocks. Below are updated

versions of the comparison tables covering the original 15 stocks plus

6 new additions.

In the below tables EV stands for "enterprise

value" and TEV stands for "theoretical enterprise value". The enterprise

value (EV) for each gold producer is calculated by adding the company's

net debt to its stock market capitalisation, where net debt is total debt

minus cash. In the case of companies that are not yet in production (about

half the companies in the list) the calculation of the current EV also

includes an estimate of future mine development cost (by doing this we

hopefully create more of a level playing field). In other words, EV represents

the current total market value of each company. TEV, on the other hand,

is what each company's gold reserves are theoretically worth at a particular

gold price. It is calculated by multiplying a company's net profit margin

per ounce of gold (the assumed gold price minus the total cost (expected

future cost in the case of non-producers) to produce an ounce of gold)

by that company's total gold reserves. In the tables we've noted each company's

TEV at $350, $425 and $500, and also the percentage change that would be

needed to bring the current market price into line with the calculated

TEV. In other words, the percentages shown in the final three columns reflect

the gain that the market would bestow on each stock at various gold prices

if the valuation criteria we have used in compiling this table were the

market's only consideration.

In the first of the following tables

the companies are shown in order of value, from best value at the top to

worst value at the bottom, assuming a gold price of $350. In the second

table the companies are once again shown in order of value, but this time

assuming a gold price of $500. Note that "Adj. Resv." in the tables stands

for "adjusted reserves" and is calculated, for each company, by adding

50% of the company's "measured and indicated resource" to its "proven and

probable reserve".

|

Company Name

|

Symbol

|

Recent Price (US$)

|

Ent. Value (US$M)

|

Total Cost per ounce

|

Adj. Resv. (Moz)

|

EV $ per oz Res.

|

TEV at $350

|

TEV at $425

|

TEV at $500

|

Gain at $350

|

Gain at $425

|

Gain at $500

|

| Bendigo

Gold |

BDG |

0.15 |

285 |

200 |

6.0 |

47 |

900 |

1350 |

1800 |

216% |

374% |

532% |

| Gallery

Gold |

GGN |

0.11 |

74 |

240 |

1.8 |

42 |

193 |

324 |

455 |

160% |

336% |

513% |

| Desert

Sun Mining |

DSM |

0.93 |

53 |

240 |

1.2 |

46 |

128 |

215 |

302 |

139% |

301% |

464% |

| Afrikander

Lease |

AFKDY |

0.67 |

147 |

247 |

3.1 |

47 |

319 |

552 |

784 |

117% |

275% |

433% |

| Redback

Mining |

RBK |

0.27 |

82 |

240 |

1.6 |

52 |

172 |

289 |

406 |

110% |

253% |

396% |

| Metallica

Resources |

MR |

1.15 |

89 |

300 |

2.8 |

32 |

140 |

350 |

560 |

57% |

291% |

526% |

| American

Bonanza |

BZA |

0.22 |

58 |

210 |

0.6 |

97 |

84 |

129 |

174 |

44% |

121% |

198% |

| Western

Silver |

WTZ |

3.03 |

169 |

260 |

2.7 |

63 |

243 |

446 |

648 |

44% |

163% |

283% |

| Metallic

Ventures |

MVG |

2.76 |

113 |

260 |

1.6 |

70 |

144 |

264 |

384 |

28% |

134% |

241% |

| Cumberland

Resources |

CBD |

2.56 |

193 |

228 |

2.0 |

96 |

244 |

394 |

544 |

27% |

105% |

183% |

| McWatters

Mining |

MWA |

0.10 |

54 |

321 |

2.3 |

24 |

66 |

238 |

411 |

21% |

339% |

656% |

| Golden

Phoenix |

GPXM |

0.35 |

54 |

300 |

1.3 |

43 |

64 |

160 |

256 |

18% |

194% |

370% |

| Emporer

Mines |

EMP |

0.36 |

36 |

333 |

2.3 |

16 |

38 |

211 |

383 |

6% |

480% |

955% |

| Eldorado

Gold |

EGO |

2.16 |

494 |

276 |

7.1 |

70 |

520 |

1049 |

1578 |

5% |

112% |

219% |

| Apollo

Gold |

APG |

2.07 |

131 |

300 |

2.6 |

51 |

129 |

322 |

515 |

-2% |

145% |

293% |

| Aquiline

Resources |

AQI |

0.51 |

29 |

240 |

0.3 |

115 |

28 |

46 |

65 |

-4% |

61% |

127% |

| Novagold |

NRI |

3.60 |

269 |

250 |

2.5 |

108 |

250 |

438 |

625 |

-7% |

63% |

132% |

| Golden

Star Resources |

GSS |

3.55 |

333 |

243 |

2.7 |

126 |

284 |

483 |

681 |

-15% |

45% |

104% |

| Orvana

Minerals |

ORV |

1.02 |

133 |

160 |

0.6 |

238 |

106 |

148 |

190 |

-20% |

11% |

43% |

| Richmont

Mines |

RIC |

3.65 |

30 |

335 |

0.5 |

57 |

8 |

48 |

88 |

-74% |

59% |

191% |

| Bema

Gold |

BGO |

1.98 |

663 |

333 |

9.6 |

69 |

168 |

888 |

1608 |

-75% |

34% |

143% |

|

Company Name

|

Symbol

|

Recent Price (US$)

|

Ent. Value (US$M)

|

Total Cost per ounce

|

Adj. Resv. (Moz)

|

EV $ per oz Res.

|

TEV at $350

|

TEV at $425

|

TEV at $500

|

Gain at $350

|

Gain at $425

|

Gain at $500

|

| Emporer

Mines |

EMP |

0.36 |

36 |

333 |

2.3 |

16 |

38 |

211 |

383 |

6% |

480% |

955% |

| McWatters

Mining |

MWA |

0.10 |

54 |

321 |

2.3 |

24 |

66 |

238 |

411 |

21% |

339% |

656% |

| Bendigo

Gold |

BDG |

0.15 |

285 |

200 |

6.0 |

47 |

900 |

1350 |

1800 |

216% |

374% |

532% |

| Metallica

Resources |

MR |

1.15 |

89 |

300 |

2.8 |

32 |

140 |

350 |

560 |

57% |

291% |

526% |

| Gallery

Gold |

GGN |

0.11 |

74 |

240 |

1.8 |

42 |

193 |

324 |

455 |

160% |

336% |

513% |

| Desert

Sun Mining |

DSM |

0.93 |

53 |

240 |

1.2 |

46 |

128 |

215 |

302 |

139% |

301% |

464% |

| Afrikander

Lease |

AFKDY |

0.67 |

147 |

247 |

3.1 |

47 |

319 |

552 |

784 |

117% |

275% |

433% |

| Redback

Mining |

RBK |

0.27 |

82 |

240 |

1.6 |

52 |

172 |

289 |

406 |

110% |

253% |

396% |

| Golden

Phoenix |

GPXM |

0.35 |

54 |

300 |

1.3 |

43 |

64 |

160 |

256 |

18% |

194% |

370% |

| Apollo

Gold |

APG |

2.07 |

131 |

300 |

2.6 |

51 |

129 |

322 |

515 |

-2% |

145% |

293% |

| Western

Silver |

WTZ |

3.03 |

169 |

260 |

2.7 |

63 |

243 |

446 |

648 |

44% |

163% |

283% |

| Metallic

Ventures |

MVG |

2.76 |

113 |

260 |

1.6 |

70 |

144 |

264 |

384 |

28% |

134% |

241% |

| Eldorado

Gold |

EGO |

2.16 |

494 |

276 |

7.1 |

70 |

520 |

1049 |

1578 |

5% |

112% |

219% |

| American

Bonanza |

BZA |

0.22 |

58 |

210 |

0.6 |

97 |

84 |

129 |

174 |

44% |

121% |

198% |

| Richmont

Mines |

RIC |

3.65 |

30 |

335 |

0.5 |

57 |

8 |

48 |

88 |

-74% |

59% |

191% |

| Cumberland

Resources |

CBD |

2.56 |

193 |

228 |

2.0 |

96 |

244 |

394 |

544 |

27% |

105% |

183% |

| Bema

Gold |

BGO |

1.98 |

663 |

333 |

9.6 |

69 |

168 |

888 |

1608 |

-75% |

34% |

143% |

| Novagold |

NRI |

3.60 |

269 |

250 |

2.5 |

108 |

250 |

438 |

625 |

-7% |

63% |

132% |

| Aquiline

Resources |

AQI |

0.51 |

29 |

240 |

0.3 |

115 |

28 |

46 |

65 |

-4% |

61% |

127% |

| Golden

Star Resources |

GSS |

3.55 |

333 |

243 |

2.7 |

126 |

284 |

483 |

681 |

-15% |

45% |

104% |

| Orvana

Minerals |

ORV |

1.02 |

133 |

160 |

0.6 |

238 |

106 |

148 |

190 |

-20% |

11% |

43% |

Notes and conclusions:

1. Please read the analysis that accompanied

the comparison tables in the 25th

June Interim Update because the comments made about specific stocks

at that time still apply. Most of the below comments deal with the new

additions to the tables.

2. We haven't taken hedging into account

in our valuation comparison. Of the companies included in the above tables

only Emporer Mines (ASX: EMP), which operates a mine in Fiji, and McWatters

(TSX: MWA) have done significant hedging of their future gold production.

Had we considered the effects of these hedge books when estimating the

values of these companies at a $500 gold price the change in our valuation

of MWA would not have been material but the valuation of EMP would probably

have fallen by 20%-30%. However, EMP is presently so under-valued that

even if we lopped 30% off its theoretical value at a $500 gold price in

order to account for the opportunity cost of the hedge book the stock would

still be at the top of the second table.

Durban Deep (DRD) owns 20% of EMP and

DRD's CEO (Mark Wellesley-Wood) sits on EMP's board. Furthermore, Wellesley-Wood

recently said that DRD was looking to expand its Australasian business

by acquiring a company or companies that are already in production (as

opposed to acquiring exploration-stage companies). Given DRD's current

involvement and EMP's extreme relative under-valuation it is not much of

a stretch to conclude that DRD will eventually make an offer for EMP. Hopefully,

the offer will come after the stock has already moved well above its current

level.

3. When a company appears to be extremely

under-valued relative to its peers there is usually a good reason. In EMP's

case there is a significant hedge book, political risk because the company

operates in Fiji, and poor recent production results due to lower grades.

In MWA's case the stock is very cheap because the company has issued a

massive number of new shares over the past several months in order to raise

money and because there have been some operational problems. An investor

therefore needs to ask himself/herself the following question: Is the apparent

discount in the price sufficient to make the stock a buy in spite of the

obvious problems? In the case of both EMP and MWA we think the answer to

the question is yes and that both stocks have attractive risk/reward ratios

at their current prices.

4. Metallica Resources (OTCBB: METLF)

scored well in terms of its leverage to the gold price. Actually, half

of this company's in-ground resource is silver so the stock is as much

a silver play as it is a gold play. The company is probably going to issue

a large amount of new equity at some point over the next 6 months. When

the stock was added to the TSI Stocks List we therefore suggested that

investors take an initial position immediately and then add to the position

into significant weakness following an equity raising.

5. Afrikander Lease (JSE: AFL, OTC:

AFKDY) is a junior South African gold producer that is expected to grow

very quickly over the next few years (from 70,000 ounces of production

this year to annual production of 300,000 ounces in 2006). Like all South

African mining companies AFL is going to struggle if the Rand continues

to strengthen, but if the Rand started to weaken (see the Rand chart included

later in today's commentary) then AFL would be a reasonable stock to own

due to its strong growth profile.

6. Gallery Gold (ASX: GGN) is about

to commence construction of a 100K oz/year mine at its Mupane project in

Botswana and also has substantial gold resources in Tanzania. The stock

represents very good value at its current price. As is the case with a

number of the other small gold mining companies we follow, at some point

over the next few months GGN will need to raise a substantial sum of money

in order to finance mine construction. This, when it occurs, will probably

put some pressure on the stock price.

7. Both NovaGold (TSX: NRI) and Aquiline

(TSXV: AQI) fared quite poorly in terms of their relative valuations at

a gold price of $500, but this is because only current reserves and measured/indicated

resources are considered in the above tables. In NRI's case there is a

massive inferred resource at Donlin Creek that will almost certainly be

brought into the measured and indicated category over the next year or

two. In AQI's case the drill results released over the past month strongly

suggest that its eventual resource will be much greater than the 500K ounce

figure used in our calculations.

Gold Forecast

In the 23rd July Interim Update we

included a chart illustrating what we considered to be the two most likely

outcomes for the gold price over the remainder of the year. Both outcomes

were bullish, with one being that a major advance was already in progress

and the other being that the consolidation process would continue for a

couple more months before a major advance got underway. Below is an updated

version of this chart. As was the case in the previous commentary, we've

included a chart of the euro below the chart of the gold price since any

gold price forecast must be consistent with a currency market forecast

(and vice versa).

In order to arrive at a reasonable

upside target for the gold price over the next several months we've used

a chart of the gold price in euros. We've done this because the major channel

top for the euro gold price is well defined. Previous rallies in the gold

price over the past few years have ended at the top of the channel shown

on the below chart and if the current rally does the same then a logical

upside target for gold is 370 euros. Assuming a euro-US$ exchange rate

of 1.25 gives us a medium-term upside target for the US$ gold price of

around $460.

Currency Market Update

Below is a chart showing the Australian

Dollar in terms of the euro (the line on the chart rises when the A$ is

out-performing the euro). Over the past few years the A$ has done well

relative to the euro during those periods when the US stock market has

been strong and has fared poorly during the stock market declines (the

boxes on the chart identify the periods when the stock market was strong

or stable). The AUD-EUR rate reversed lower at around the time the stock

market was peaking in June-July. If the stock market behaves roughly in

line with our current expectations then the A$ will probably be very weak,

relative to the euro, during the first half of next year.

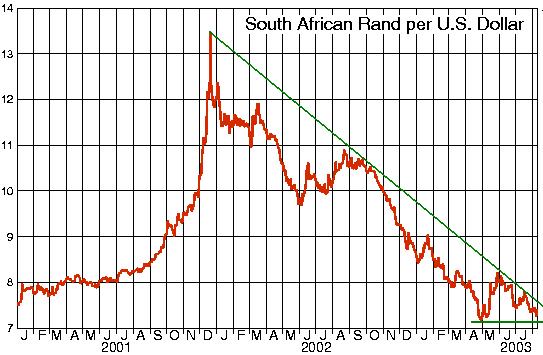

After being one of the weakest currencies

in the world for many years the South African Rand has been the strongest

currency in the world since late-2001. However, the below chart shows that

it wouldn't take much of a fall in the Rand to break the trend-line that

began almost 2 years ago (note that a falling line on the chart indicates

a strengthening Rand). It is quite possible that the US$-Rand exchange

rate bottomed in April and that the recent weakness (strength in the Rand

relative to the US$) is a test of that bottom. A decisive move above the

trend-line drawn on this chart would suggest that this was, in fact, the

case, and that a substantial counter-trend rally was underway. Such a rally

in the US$ relative to the Rand would, of course, benefit the SA-based

miners.

Chart source: http://pacific.commerce.ubc.ca/xr/plot.html

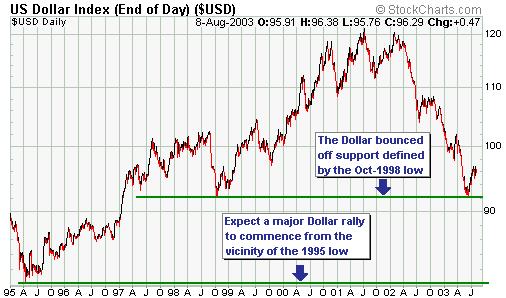

Earlier this year the Dollar Index

bounced off support defined by its 1998 low, but we don't have any technical

or fundamental evidence that a major low is in place for the US$. However,

we do expect the dollar to receive substantial buying support once it drops

to the vicinity of its 1995 low. We expect that the 1995 low will be reached

by mid 2004.

Current Market Situation

Below is a daily chart of December

gold futures. After having bounced off its 200-day moving average during

the week before last gold had managed to move above both its 18-day and

50-day moving averages by the end of last week. Provided gold doesn't close

down by more than $2 on Monday we will therefore have confirmation that

a pullback low was put in place on 1st August.

We are skeptical of gold's ability

to hold above the 200-day moving average during its recent pullbacks because

this widely-watched level often has to be broken before a sustainable bottom

occurs (as was the case earlier this year). However, the behaviour of the

gold shares suggests that the gold price is about to move sharply higher.

Anyway, regardless of whether or not we get a drop below the 200-day moving

average over the next few weeks we will be very surprised if gold does

not trade well above $400 before the end of this year.

Below is a chart of the HUI/gold ratio.

The rise in the ratio to near its mid-1996 level suggests that there is

little additional upside potential in the senior gold stocks relative

to the gold price. In other words, any further gains in the senior

gold stocks will probably need to be accompanied by equivalent percentage

gains in the gold price. If we owned any large-cap gold stocks (we don't)

we'd be starting to scale-out now and would probably be shifting our investment

funds from the stocks to the bullion. As confirmed by the valuation comparison

included earlier in today's commentary there is, however, a lot of potential

upside in the junior gold stocks and we are not inclined to take any profits

on our junior gold stocks at this time. However, we will probably exit

some of the juniors if the gold price accelerates higher over the next

few weeks. When the appropriate time to do some selling does arrive, the

decision as to which stocks to exit will be made by taking into account

both valuation and price action.

By the way, as we've discussed in the

past it makes little sense to forecast the gold price based on the dollar's

current price action and to forecast gold stocks based on gold's current

price action. It does, however, make sense to forecast gold based on what

is happening to gold stocks and to forecast the dollar based on what is

happening to gold. In the current situation, with gold stocks leading to

the upside, it is likely that gold stocks will peak before gold peaks and

that gold will peak before (perhaps well before) the dollar bottoms. For

example, we wouldn't be surprised if the final $50 up-move in the gold

price occurs AFTER the major gold stock indices have peaked and if the

final plunge in the US$ occurs AFTER the gold price has peaked.

Below is a weekly chart of the silver

price. Silver did what it was supposed to do over the past week and pulled

back to the former resistance area (now support). We continue to expect

that silver will make its way up to at least $5.80 over the next few months.

Update

on Stock Selections

In

the 30th July Interim Update we briefly discussed the way junior mining

companies use private placements of new shares to raise money and said

that the best the management of these companies can generally do is to

time the placements to coincide with stock price strength. Wheaton River

(TSX: WRM, AMEX: WHT) is definitely not in the junior category anymore,

but its recent announcement of a large equity placement is a good example

of how such deals ideally should be timed. In

the 30th July Interim Update we briefly discussed the way junior mining

companies use private placements of new shares to raise money and said

that the best the management of these companies can generally do is to

time the placements to coincide with stock price strength. Wheaton River

(TSX: WRM, AMEX: WHT) is definitely not in the junior category anymore,

but its recent announcement of a large equity placement is a good example

of how such deals ideally should be timed.

Below is a chart of WRM. On the day

prior to the announcement of the new issue WRM had hit resistance defined

by the all-time high reached in May of 2002, so a pullback in the short-term

was likely with or without the new issue (especially given the large advance

in the shares over the preceding 2 months). As such, the new equity issue

simply assisted in prompting a pullback that would have happened anyway.

Also, the new issue was priced at a slight premium to the market price

at the time and the warrants issued as part of the deal were well out of

the money. This means that the financing will not dilute the value of existing

shares.

Given the large size of the financing

(C$100M) it is probable that WRM's management has another acquisition in

mind.

The

feasibility study on Desert Sun Mining's (TSX: DSM) Jacobina gold project

in Brazil is due to be complete later this month. A positive feasibility

study (we see no reason why it won't be positive) will confirm that DSM

is worth more than C$2/share assuming no increase in the gold price.

In

the 2nd July Interim Update we explained why NovaGold (TSX: NRI) was probably

worth around C$6.60/share assuming no increase in the gold price. NRI has

since moved up from $3.25 to $5.00 and is still reasonable value, although

the stock is obviously not as attractive now as it was 6 weeks ago. We

don't think it makes sense to purchase NRI now given the recent surge in

its price, but buying following a pullback to near the top of its former

channel (see chart below) might make sense for those looking for relatively

low-risk exposure to some gold juniors.

Although

we think the odds favour new recovery highs in both the S&P500 and

the Dow over the next few months, the risk/reward ratio for the US stock

market is terrible. If new highs are achieved they will most likely only

be a few percent above the June-July peaks, but we estimate that the market

has downside risk of 30%-50%. As such, longer-term investors should remain

out of the US market except for a few special situations such as gold stocks

and, to a much lesser extent, commodity-cyclical stocks.

Due to the market's poor risk/reward

we are going to add another QQQ put option position to the Stocks List

at this time. We'll add a second position in the QQQ December-2003 $25

put options (QAVXY) using Friday's closing price of US$0.60 for record

purposes. If the market falls sharply over the next few weeks we will probably

take the opportunity to exit all December-2003 put options with the aim

of entering longer-dated QQQ put options (options that expire during the

second half of 2004) later this year.

Copyright

Reminder

The commentaries that appear at TSI

are copyrighted material and may not be distributed, in full or in part,

without our written permission. In particular, please note that the posting

of extracts from TSI commentary at other web sites (for example, at discussion

boards) without our written permission is a breach of copyright.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://bigcharts.marketwatch.com/

http://www.futuresource.com/

|