-- Weekly Market Update for the Week Commencing 14th March 2016

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Bullish

(26-Mar-12) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Bullish

(29-Feb-16) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Bearish

(19-Oct-15)

|

Bearish |

|

Stock Market

(DJW)

|

N/A |

Bearish

(30-Dec-15) |

Bearish

|

|

Gold Stocks

(HUI)

|

N/A |

Bullish

(23-Jun-10) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Neutral

(09-Nov-15) |

Bullish

(28-Apr-14) |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

Bad logic on trade

Brazil Boom and Bust

This week's FOMC

meeting

In the FOMC statement scheduled

for this Wednesday the Fed will likely say that it is taking no immediate action

and that it remains data dependent. Furthermore, the statement will likely be

worded in such a way as to leave open the possibility of a second rate hike as

soon as June.

It is not reasonable to expect the Fed to do/say anything other than what we've

outlined above, but many traders could still have different expectations. How

the markets react to the Fed's announcement will be determined by what most

traders are expecting.

Note that what the Fed says it plans to do over the months ahead and what the

Fed actually ends up doing are unrelated. What the Fed does over the next few

months will mostly be determined by the performance of the stock market.

More leeches!

The euro-zone wrecking-ball

known as Mario Draghi did what he seems to enjoy doing last Thursday and created

a brief period of chaos in the financial markets. In terms of additional

'unconventional'* monetary measures, the ECB did everything that most currency

traders were expecting and then some. The result was a huge intra-day swing in

the euro.

The additional/ramped-up measures comprise a further push into

negative-interest-rate territory (the rate on deposits at the ECB has been

reduced from minus 0.30% to minus 0.40%), an expansion of the asset monetisation

(QE) program from 60B to 80B euros/month, the inclusion of corporate bonds in

the assets to be monetised, and the re-introduction of long-term (4-year)

repurchase operations (LTROs) beginning in June. The rate on the new LTROs can

be as low as the deposit rate (minus 0.40%), which means that the ECB will

simultaneously be charging banks to lend money to the ECB (via deposits, which

are loans) and paying banks to borrow money from the ECB (via LTROs).

Why is the ECB charging banks to deposit money on the one hand and paying banks

to borrow money on the other? That is, why is the ECB transferring money from

one pocket to the other?

The explanation is convoluted. One reason is that the negative interest rate on

deposits imposes a cost on the euro-zone banking system that, as we discussed in

a recent commentary in relation to US bank reserves, cannot be avoided. An

individual bank could avoid or minimise the cost by transferring deposits to

another bank, but the cost cannot be avoided or reduced on an industry-wide

basis. By paying banks to borrow money at the same time as it is charging banks

to deposit money, the ECB is allowing banks to offset the cost of NIRP (negative

interest rate policy).

But why have the NIRP in the first place? What good can possibly come of it?

The answer is that no good can possibly come of it. It is damaging to both the

economy and the financial system. However, this is an example of one

ill-conceived intervention by central planners creating a problem that

necessitates another ill-conceived intervention.

In this case, aggressive central-bank support of government bonds led to many of

these bonds having negative yields, which would have prevented the bonds from

being purchased as part of QE operations. This is due to a guideline that only

bonds that yield at least as much as the deposit rate can be monetised by the

ECB. In other words, earlier ECB actions led to a situation (negative yields on

bonds) that would have greatly limited the ECB's future actions unless the

official deposit rate was set below zero.

As we said, the explanation is convoluted.

The initial reaction of currency speculators to the ECB's new tactics was to

aggressively sell the euro, causing it to plunge 1.6% (an unusually-large

intra-day move by the world's second most important currency). But that was

nothing. The next reaction of currency speculators was to aggressively buy the

euro, causing it to surge by 3.6% from its low. All of this happened within the

space of four hours in the aftermath of the ECB announcement.

Why the sudden turnaround in the euro's exchange rate?

It's likely that speculators first sold the euro on the belief that the

accelerated pace of money-pumping would result in more "inflation" and that the

monetary stupidity was destined to continue unabated, but then bought on the

belief -- based on comments made by Draghi at a press conference -- that the ECB

had effectively gone 'all in' for the time being and would now be on hold for an

extended period.

It seems to us that the 'market' misinterpreted Draghi's press-conference

remarks to mean that the ECB would take no further actions to promote

"inflation", whereas all he actually said was that a further reduction in

interest rates was probably not on the cards. He did not imply that other

pro-inflation measures would not be taken.

In last week's Interim Update we said that the ECB's senior policy-makers, in

looking at the world through a Keynesian lens, were like astronomers trying to

understand the paths of the planets based on the theory that the Earth is the

centre of the universe. Another appropriate analogy is the medical profession's

ancient theory that all manner of illness could be alleviated by applying

leeches to the patient's body. In this case the body is the euro-zone economy

and the leeches are interest-rate suppression and "quantitative easing".

The ECB has been applying the monetary equivalent of leeches in an effort to

cure an illness it does not understand. When the economy fails to respond

positively to the application of leeches, the solution is always: "More

leeches!"

Unless Draghi and his crew of monetary quacks are stopped, eventually there will

be no blood left to suck.

*We placed inverted commas around the word unconventional

because in the realm of monetary policy what used to be called unconventional

has transmogrified into the norm.

The Stock Market

The US

The S&P500 Index (SPX) reached its 200-day MA on Friday 11th March. For the past

few weeks we've viewed the vicinity of the SPX's 200-day MA as the most likely

place for the rally from the January-February double bottom to end, so the fact

that it has moved this high is certainly not unexpected. The challenge is in

figuring out the most probable path from here on.

We'd like to be able to unequivocally state that the stage is now set for the

next bear-market downward leg to begin, but we can't. We can't because although

the market is now 'overbought' on a short-term basis, there isn't yet any

evidence that something more than a routine consolidation lies in the near

future. In particular, market internals and sentiment indicators are currently

not flashing warning signs.

To give you an idea of where we think the market is now positioned, here is a

chart of the NYSE Composite Index (NYA) covering the past 17 years. The red line

on the chart is the 200-day MA and the green arrows mark the tops of the

bear-market rebounds to near the 200-day MA in 2001 and 2008.

The chart shows that, based on the historical record, it was reasonable to

expect a rebound to near (slightly above) the 200-day MA from the

January-February 'oversold' extreme. Also, the chart suggests that if a bear

market is in progress then prices should soon begin rolling over to the downside

without making much additional headway.

Considering the current lack of bearish warning signs in measures of market

breadth and sentiment and the fact that the NYA hasn't quite reached its 200-day

MA, it's unlikely that a strong downward trend will begin immediately. Instead,

the most likely near-term outcome is a form of topping pattern involving a

pullback followed by a marginal new rebound high, with acceleration to the

downside not happening until April or May.

We stress, however, that the short-term risk/reward is now decisively skewed

towards risk and that it is reasonable to view the current strength as an

opportunity to scale into bearish speculations. For one thing, although the

stock indices are probably going to make new rebound highs within the next few

weeks, they probably aren't going to move a lot higher. For another thing,

although the odds favour a topping process over the next few weeks, there is

definitely a risk that the next downward leg begins as soon as this week.

The World

The Dow Jones Global Index (DJW) has almost reached the top of a well-defined

intermediate-term price channel. This means that it isn't just the US stock

market that is probably close to a rebound peak.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

| Monday Mar

14 |

No important events

scheduled |

| Tuesday

Mar 15 |

PPI

Retail Sales

Empire State Mfg Survey

Business Inventories

Housing Market Index

TIC Report |

| Wednesday

Mar 16 |

FOMC Announcement

CPI

Housing Starts

Industrial Production |

| Thursday

Mar 17 |

Philadelphia Fed Business

Outlook Survey

Q4-2015 Current Account |

| Friday

Mar 18 |

Consumer Sentiment |

Gold and the Dollar

Gold

The Missing Link

The most important fundamental driver of the gold market that hasn't yet begun

to move in a gold-bullish direction is the US yield curve, represented on the

following chart by the 10yr-2yr yield spread. The yield curve is bullish for

gold when it is getting steeper, as indicated by a rising 10yr-2yr yield spread

(a rising line on the following chart). With the 10yr-2yr yield spread having

recently made a new 8-year low and not yet shown any sign of reversing upward,

the yield curve remains unequivocally gold-bearish.

The yield curve is also one of the most important economic indicators to not yet

warn of a US recession. As pointed out in a recent TSI commentary, it isn't an

inversion of the yield curve (the 10yr-2yr yield spread dropping below zero)

that warns of a recession, it's a trend reversal from flattening to steepening

after the yield-spread has fallen to a multi-year low.

Based on what happened over the past 50 years, a trend reversal in the yield

spread is not a prerequisite for a gold bull market. As long as sufficient other

fundamental drivers (e.g. credit spreads and the real interest rate) are

gold-bullish it is possible for gold to commence a bull market in the absence of

a supportive yield curve. This is exemplified by the bull market that began

during 1976-1977. However, it would be unprecedented for a US recession to begin

in the absence of an upward reversal in the 10-yr-2yr yield spread.

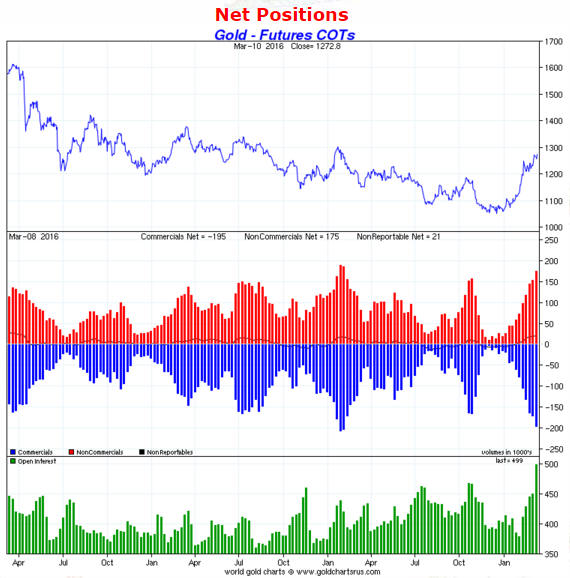

The COT situation is now sounding a loud warning bell

The following chart shows that the total speculative net-long position in COMEX

gold futures moved to near a 3-year high last week. This increases the

short-term downside risk because it means that there is now more scope for long

liquidation by speculators in reaction to a declining price.

As mentioned many times in the past, a drawback of sentiment indicators such as

the COT report is that there are no absolute benchmarks. For example, if a gold

bull market has begun then the speculative net-long position in gold futures

will tend to make progressively higher highs over the coming 1-2 years along

with the price. However, it is still prudent to view a rise in the speculative

net-long position to near the high of the preceding three years as a signal to

be cautious.

Current Market Situation

From last week's Interim Update:

"...a short-term top has still not been signaled. This means that a rise to

$1300-$1308 remains a realistic possibility prior to such a top (a price peak

that holds for 1-3 months).

As noted in earlier TSI commentaries, the first clear sign that a short-term top

was in place would be a daily close below the 20-day MA. This MA is now at $1235

and should be above $1240 by the end of the week.

In addition, the $1240 level is now shaping up to be significant lateral

support, given that the gold price reversed upward on Wednesday following a

decline to slightly above this level. Therefore, over the next few days gold's

position relative to $1240 could also be used to confirm/deny a short-term top.

Specifically, it would now be reasonable to interpret a daily close below $1240

as evidence that the US$ gold price had made a top that will hold for at least a

month."

The price action is becoming increasingly choppy, with a move below $1240 being

quickly reversed on Thursday 10th March and then a move to a new high for the

year being quickly reversed on Friday 11th March. Friday's price action was

obviously a little bearish, but a short-term top still hasn't been signaled.

Until it is there will be a realistic chance of a final surge to resistance at

$1300-$1308, but the probability of this resistance being tested in the near

future diminished last week.

It would be normal for the coming correction to retrace at least half of the

preceding advance, which suggests that there will be a decline to the $1160s or

lower over the weeks ahead IF it turns out that last Friday's intra-day high was

the rally top. However, it will be important to take the evidence as it comes.

In particular, the pace at which speculators liquidate their long positions in

the futures market will provide useful clues regarding the length and magnitude

of whatever correction follows a short-term top.

Gold Stocks

Current Market Situation

Although Friday's new high for the year in the US$ gold price wasn't accompanied

by a new high for the year in the HUI, the gold-mining stocks generally

shrugged-off Friday's downward reversal in the gold price and the HUI/gold ratio

ended the week near a 9-month high. This means that the HUI is still

outperforming gold.

As discussed in last week's Interim Update:

1) A daily close below 160 would indicate that a short-term price top was in

place.

2) Until a short-term top is signaled there will remain a realistic chance of a

surge to a new high for the year, with round-number resistance at 200 probably

defining the maximum upside following a break above the recent high in the 180s.

The HUI's rally from its January-2016 bottom fell behind the pace of the rally

from the Q4-2008 bottom last week, but it is still the second-strongest rally

ever from a multi-year low. This augurs well for the coming 1-2 years, since it

is clear-cut evidence that we have witnessed the start of a bull market rather

than just another bear-market rebound. However, significant corrections occur

within bull markets.

Our concern over the past few weeks was that the HUI had become very stretched

to the upside on a short-term basis. As indicated by the RSI shown at the bottom

of the following weekly chart, it is now also stretched to the upside on an

intermediate-term basis (the weekly RSI just hit its highest level since 2010).

This is a normal occurrence in the early part of a bull market, but it is a

further warning to be prepared for a multi-week correction/decline.

Quarterly Index Changes

The quarterly changes to gold-mining indexes and the associated ETFs become

effective at the end of this week.

Evolution Mining (EVN.AX) is the TSI stock that will probably be influenced to

the greatest extent by these changes, because it is going from 3.93% to 0% of

GDXJ (it is being removed from GDXJ due to the fact that it is no longer a

junior). Consequently, GDXJ will have to sell about 50M EVN shares, which

equates to about 8 days of average trading volume, by the end of the week. This

will naturally put downward pressure on EVN's stock price, although the effect

of GDXJ selling could be partially offset by GDX buying. Unfortunately, we

haven't been able to find out what changes are being made to GDX component

weightings.

Other TSI stocks that could be affected by changes to GDXJ weightings are AKG,

PG, PVG and RSG. In each of these cases the stock price will be helped by GDXJ

buying, but the effect is unlikely to be significant.

The Currency Market

Thursday's dramatic intra-day upward reversal in the euro was driven by hints

that the ECB would not apply additional monetary leeches for at least the next

several months. If you conclude that this is not a solid foundation for a euro

rally, you are right.

The euro's upward reversal from support at 108 last Thursday is short-term

bullish, but the euro's intermediate-term outlook remains bearish due to the

relative weakness over the past 6 months in euro-denominated equities.

Zooming out, 12 months ago the Dollar Index was as 'overbought' as it ever gets.

This created the potential for a major US$ top, but the subsequent sideways move

has fully corrected the 'overbought' condition without doing any technical

damage.

The extent to which the Dollar Index's situation has shifted over the past 12

months is illustrated by the Rate of Change indicator at the bottom of the

following chart. This indicator shows that at around this time last year the

Dollar Index was 25% above its level of 250 days earlier, whereas it is now 3.8%

lower than it was 250 trading days ago. This effectively means that it is down

on a year-over-year basis.

Think back on the extreme US$ bullishness that prevailed 12 months ago. Almost

everyone was convinced that the US$ would continue to rise over the coming 12

months. Instead, it fell. The sentiment extreme has been corrected along with

the momentum extreme, although it is fair to say that there are still a lot more

US$ bulls than US$ bears.

A full correction of last year's US$ sentiment extreme is not going to happen

this year unless there is a decline in the Dollar Index to well below the lows

of the past 12 months, which is very unlikely. More likely is that the

range-trading continues for at least another month, after which the Dollar Index

embarks on its next -- and probably final -- upward leg.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 11th March 2016:

Company

news/developments for the week ending Friday 11th March 2016:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, MD&A = Management Discussion and Analysis,

M&I = Measured and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value

using a discount rate of X%, P&P = Proven and Probable, PEA = Preliminary

Economic Assessment, PFS = Pre-Feasibility Study]

*Energy Fuels (EFR.TO, UUUU) made three notable announcements last

week.

First, it announced that it plans to produce 950K pounds of uranium and to sell

550K pounds of uranium this year. Most of the sales will be into long-term

contracts priced in the high-$50s (the current spot price is below $30) and will

be profitable.

Second, it announced that it sold about 4.4M new shares at US$2.40 (C$3.25) per

share to raise US$10.5M. The news of this low-priced equity financing caused the

stock price to plunge by around 15% last Thursday.

Third, it announced that it is buying Mestena Uranium LLC, a privately held

uranium producer that operates the Alta Mesa ISR (In Situ Recovery) project in

Texas, at a cost of 4.5M EFR shares. Alta Mesa is a fully-permitted production

facility capable of producing 1.5M pounds of uranium per year. It is currently

on standby pending a higher uranium price.

With its White Mesa mill, its Nichols Ranch ISR project and the newly-acquired

Alta Mesa project, EFR will have the ability to ramp up uranium production to

more than 10M-pounds/year once the uranium price moves high enough.

Consequently, it is positioned to be one of the 'go to' uranium stocks during

the next multi-year upward trend in the uranium price. However, it probably

won't be a strong candidate for new buying until there are signs that the

uranium price has turned upward. Given that the uranium price made a new

18-month low last week (see chart below) we are obviously not at that point.

*Energold Drilling (EGD.V) announced an interesting acquisition.

It has agreed to purchase Cros-Man Direct Underground, a small company that

provides horizontal directional drilling services for the telecommunications,

water, sewage, hydro and oil and gas markets in central Canada. According to

EGD's press release: "Cros-Man's primary business involves the trenchless

method of installing cable and piping systems underground in a shallow arc along

a predetermined path, by the use of highly specialised drilling equipment. Over

the past eleven years, Cros-Man has generated an increasing portion of its

revenue from engineering and telecommunications drilling services and also

maintains an ongoing presence in the oil and gas pipeline market in Central

Canada."

Cros-Man is a debt-free growing company that generated $4.7M of revenue in 2015.

The purchase price of $3.5M up front plus about $800K/year for the next three

years therefore looks like a reasonable deal for EGD. The acquisition appears to

be accretive and has the benefit of diversifying EGD's overall business by

adding a segment that doesn't rely on commodity prices.

Despite the long-term upside potential stemming from its low valuation, we view

EGD as more of a hold than a buy at this time.

*Pretium Resources (PVG) reported the sixth set of results from

its infill and stope-definition drilling program. The latest batch of results

included four intersections of greater than 1,000-g/t gold over narrow (0.5m)

widths.

This program, which is scheduled to be completed in Q2-2016, has thus far

generated results from 186 holes with 29 intersections grading more than

1,000-g/t gold. According to PVG's management, it is achieving its intended

purpose of increasing confidence in the resource model and assisting with

planning the first three years of production.

With the completion of the recent $133M equity financing (the initial $120M

financing plus the exercising of the underwriters' $10M over-allotment option

plus the exercising by Orion Mine Finance of its proportionate ownership

entitlement), PVG is fully funded through to production in late-2017.

Unfortunately, there will continue to be uncertainty regarding the validity of

the resource estimate and the mining plan until after the project goes into

production.

List

of candidates for new buying

From within the ranks of TSI stock selections the best candidates for new buying

at this time, listed in alphabetical order, are:

1) FCG, with a sell stop at $4.06 if buying for a short-term trade (last

Friday's closing price: US$4.39)

2) PRQ.TO (last Friday's closing price: C$2.80)

Note that the above list is limited to five stocks. It will sometimes contain

less than five, but it will never contain more than five regardless of how many

stocks are attractively priced for new buying.

The

FCG (Natural-Gas Equity ETF) Trade

FCG was extremely volatile over the first two days of last week, first surging

to a new high for the year and then plunging to support in the low-$4 area. At

this stage the sharp decline on Tuesday 8th March looks like a routine pullback

within a short-term upward trend, but a decline to below the 8th March low would

suggest that a short-term top was in place.

Consequently, the FCG trading position will be removed from the TSI List if FCG

trades below last Tuesday's low of 4.07 within the next two weeks. In setting

this 'stop' we are ensuring that the worst-case result for this trade will be a

profit of 15%.

The trading position will also be removed from the TSI List if FCG moves up to

$5.60 within the next two weeks, because at that price the short-term

risk/reward would no longer justify the position.

XME

put-option suggestion

XME, an ETF that tracks the S&P Metals and Mining Index, has rocketed upward

since bottoming in January. According to its daily RSI(14), which is shown at

the bottom of the following chart, it recently reached its most 'overbought'

level of the past few years. It is also close to important lateral resistance at

$20.

The price action suggests the potential for a rise to a new high for the year

this week, but the short-term risk/reward is now decisively skewed towards risk.

Even if a bull market has begun it would be normal for this ETF to retrace at

least half of its January-March rally before resuming its advance.

Our intention at this time is that for TSI record purposes, QID July call

options will be the exclusive focus of a short-term stock market bearish

speculation. However, we wanted to point out that XME put options now look

interesting, either as a hedge for anyone with long positions in

commodity-related equities or as an outright bearish bet.

We bought a small position in XME June-2016 $16 put options for our own account

last Friday and will possibly add to the position if XME becomes even more

extended to the upside over the days/weeks ahead.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.sharelynx.com/

http://www.barchart.com/