![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 15th January 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bearish (12 Jan 2018) |

| US Equity (SPX) | Neutral (12 Jan 2018) |

| Currency (Dollar Index) | Bullish (15 Dec 2017) |

| Commodities (GNX) | Bullish (29 Dec 2017) |

Last week's posts at the TSI Blog

Monetary

Policy Madness?

A reality check regarding China purchases of US debt

Summary of current

thinking/positioning

1) Expecting that gold will test

its 2016 high of US$1377 during the first half of 2018 (possibly as soon

as next month).

2) Expecting a tradable US stock-market correction

to begin soon and planning to add a bearish position in the form of QID

and/or QQQ puts to the TSI List after a downward reversal in the market.

3) Thinking that industrial commodities such as oil and copper will

make short-term price highs during the first two months of 2018.

4)

Thinking that the Dollar Index (DX) has resumed its longer-term downward

trend and that there is a risk of downward acceleration over the coming

three weeks. At the same time, recognising that currency-market trends are

already stretched on a short-term basis and at risk of sharp reversals.

5) Thinking that the T-Bond has almost completed an intermediate-term

topping pattern within the context of a long-term topping pattern.

6) Holding a cash reserve of about 25% and looking for opportunities to

boost this reserve to 30%-35%.

Commodities

EV Metals

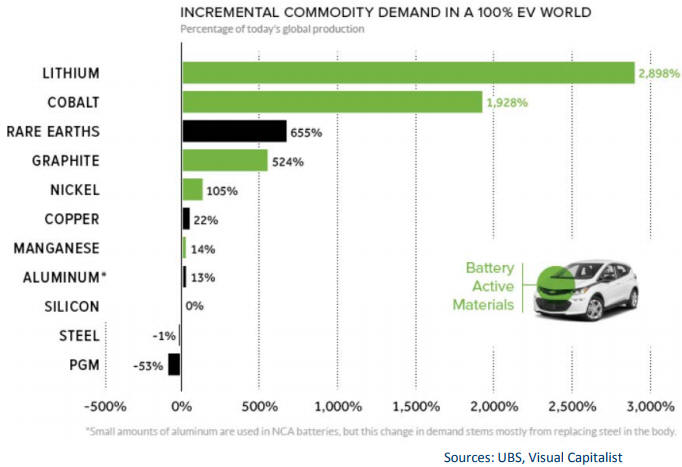

We found the following chart in a presentation by Alkane Resources

(ALK.AX). It shows estimates of the percentage increase in production of

various commodities that would be required if all vehicles were electric.

There are good reasons to expect that all new motor vehicles will be

electric by the middle of the next decade, so in this respect the chart

doesn't assume something outlandish. The estimates are unrealistic,

though, firstly because battery technology* will change dramatically over

the next several years and secondly because it's likely that the

intersection of EV advancement, self-driving technology and ride sharing**

will result in there being a lot less cars on the road. The details are

inestimable at this time, but the chart is still interesting and useful

because it provides a very rough idea of the scale of the production

increases that may be needed to satisfy future demand.

It will not

be possible to get production increases even remotely as large as those

that could be required for lithium, cobalt and the REEs (rare earth

elements) without the incentive of much higher prices. That's why there's

a good chance that the prices of these metals will remain in or enter

powerful upward trends over the next few years.

*To get an idea of what may be possible within the next

several years, watch the short interview linked

HERE. Apparently, the technology already exists to develop a

high-performance EV that can go for 700 miles on a 1 minute charge.

**It's likely that major car manufacturers will be partnering

with companies such as Uber, Google and Amazon to make this happen. An

example is the

new strategy recently announced by Toyota.

Getting

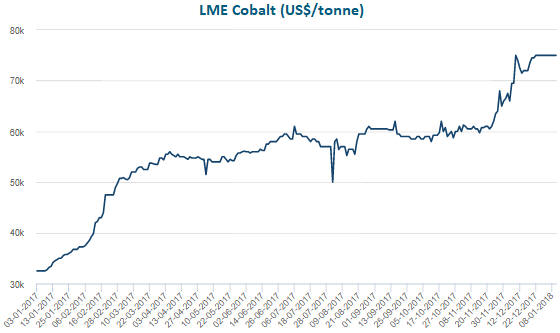

exposure to cobalt

The following chart shows that the

price of cobalt has more than doubled over the past 12 months to

US$75,000/tonne (US$34/pound). We normally wouldn't be interested in

purchasing exposure to a commodity after it has just doubled within a

year, but, due to the EV trend and the fact that cobalt supply is largely

price-insensitive (thanks to almost all cobalt supply being a byproduct of

copper and nickel mines), it's likely that a much higher price will be

attained within the next two years.

Investors can participate in the cobalt bull market without taking

exploration or country risk (almost all of the world's high-margin cobalt

deposits are in the DRC) by purchasing the shares of Cobalt 27 Capital

Corp. (TSXV: KBLT). KBLT currently owns 2,983 tonnes of physical cobalt

stored in LME warehouses and some royalties on early-stage cobalt

projects. It also plans to do cobalt streaming deals at mines where the

cobalt byproduct is small relative to the mine's total revenue.

KBLT has only existed for about 7 months. It has 34M shares outstanding

and ended Friday's session at C$12.45/share.

Based solely on its cash and physical cobalt, that is, assigning no

value to its royalties, we estimate that KBLT's current net asset value

(NAV) is about C$9.00/share. This means that KBLT is trading at about a

38% premium to NAV.

Taking into account the paucity of choices when

it comes to cobalt-focused investments and KBLT's plan to do streaming

deals, this is not an unreasonable premium. It could therefore make sense

to take an initial position near the current price, although we are hoping

that a better buying opportunity will arrive within the next couple of

months.

A much better buying opportunity is not likely, because a

stock such as this usually will trade at a significant premium to NAV and

there probably won't be a large decline in the cobalt price. Consequently,

we think that the current NAV defines the downside risk.

KBLT will

be added to the TSI Stocks List if it trades at C$11.00.

2018 Commodity Forecast

Our 2017 commodity forecast was

for a Q1-2017 top, an important bottom around mid-year and general

commodity-price strength during the second half of the year. The following

chart shows that this turned out to be exactly right, although some of our

reasoning was wrong.

So, what's on the cards for 2018?

To use a cliche, 2018 will be

a year of two halves for the commodity markets and many other markets. To

begin with, here are some of our commodity-related expectations for the

first half.

If we had written this forecast five weeks ago we would

have stated that the basket of commodity prices that constitutes the GSCI

Spot Commodity Index (GNX) was set to trend upward during the first half

of 2018. That's still our prediction, but due to the intervening price

action there's now a higher risk of it being wrong.

Risk has

increased due to the recent sharp advances in the prices of some

commodities, most notably oil and copper. In particular, the approximately

$9 rise in the price of oil (West Texas Intermediate Crude) from around

$56/barrel in early-December to a high last week of almost $65 has

substantially reduced the intermediate-term upside potential of what is

still the world's most important commodity.

Oil and some metals,

including copper, now look set to make multi-month price highs within the

first two months of 2018.

In oil's case, counter-balancing the

extent to which price and speculative sentiment are stretched into

'overbought' territory is the fact that the fundamental backdrop remains

bullish. As long as the supply-demand situation in the physical market

remains bullish, as evidenced by significant backwardation in the futures

market, it will be reasonable to assume that nothing more bearish than a

run-of-the-mill 1-2 month correction is in store. We therefore expect that

oil will exceed its Q1 price high during Q2.

In copper's case the

fundamental backdrop is now neutral at best. This may mean that whatever

high is made by the copper price during the first two months of the year

will be the high for the first half of the year.

If the first half

pans out roughly as expected then the second half should contain a lot

more downside volatility. In particular, we expect that a substantial

decline in the broad stock market during the second half will lead to

pronounced weakness in the prices of industrial commodities as the

dominant concern temporarily shifts from "inflation" to "deflation".

In the above discussion we singled out oil and copper, because these

are two of the small number of commodities that we follow closely. For

most commodities we have no opinion regarding likely price performance in

2018. For example, we have no idea what will happen over the year ahead to

the prices of wheat, corn, cattle, hogs, cotton, sugar, lumber and coffee.

However, here are some additional brief thoughts on what we expect from

specific commodity markets:

We think that uranium made a long-term

price bottom near $18/pound in late-2016, but that a new bull market will

not begin in the foreseeable future. Uranium-mining stocks should,

however, continue to be good for the occasional short-term trade.

Due to a physical supply-demand situation that remains very supportive, we

think that zinc's bull market has a long way to go.

When platinum

began trading at a discount to gold in 2015 we thought it was a temporary

state of affairs, but we now view it as a more-or-less permanent shift.

Rather than spikes below 1 in the platinum/gold ratio signaling that

platinum offers excellent value relative to gold it may now be the case

that spikes above 1 in this ratio signal that platinum is expensive

relative to gold. Long-term fundamental changes support this conclusion,

with gold benefiting from the increasingly manipulative/counter-productive

efforts of central banks and platinum being hurt by the trend towards an

all-EV world. That being said, we think that there will be an opportunity

to sell platinum in the $1200s (more than 20% above the current price)

during the first half of 2018.

We guess that natural gas will trade

above US$4.00 within the first half of 2018.

2018 T-Bond

Forecast

Here's how we summarised our

annual T-Bond forecast at this time last year:

"We expect that

it will be another losing year for the T-Bond due primarily to rising fear

of inflation during the second half of the year, but that a major T-Bond

decline won't happen. Preventing a major decline will be price-support

from central banks and periodic flights to safety, with the flights to

safety being caused by stock market volatility in the US and political

drama in Europe.

The current price for the T-Bond is 151. We expect

the price to trade near 140 before year-end, but not below 130. This

expectation is based on the strong tendency for intermediate-term declines

in the T-Bond to bottom at or slightly below the 84-month moving

average...".

This forecast proved to be too bearish. 2017

turned out to be a flat year for the T-Bond as what we interpret as a

long-term topping pattern continued to develop. The long-term topping

pattern is evident on the following monthly chart.

The above chart shows that the T-Bond has major support at 146 defined

by its lows of the past three years and its 84-month MA. A monthly close

below this support would confirm that the multi-decade bond bull market

had ended.

We expect that the aforementioned major support will

hold if tested during the first quarter but will be breached during the

second quarter in response to rising fear of "inflation".

In the

second half of the year we expect to encounter substantial 2-way

bond-market volatility, with a strong 2-3 month rally at some point in

reaction to falling equity and commodity prices.

Overall, we are

anticipating a down year for the T-Bond (an up year for long-term interest

rates), but not a large decline. We expect that major weakness in 'risk

free' government bonds will be one of the next decade's big stories.

The Stock Market

The first of the following daily

charts shows that the nominal (US$-denominated) S&P500 Index (SPX) was in

a consistent upward trend throughout 2017 and accelerated upward during

the first two weeks of 2018. Referring to the bottom section of the chart,

notice that the upward acceleration has pushed the SPX's daily RSI(14) to

a very high level. It is actually the highest level achieved by this

momentum indicator in decades, suggesting that on a short-term basis the

SPX is as 'overbought' as it ever gets. What does this mean?

It

probably means that the SPX is close to a short-term top, but not a

long-term or even an intermediate-term top. This is because longer-term

SPX tops rarely -- we are tempted to say never, but there could be

exceptions we aren't aware of -- coincide with short-term RSI extremes.

Instead, they tend to be associated with waning short-term momentum and/or

a bearish momentum divergence (a higher-high for the price in parallel

with a lower-high for momentum).

Also worth mentioning is that the

bearish divergence of market internals that was evident for about two

months beginning in late-October has disappeared. That is, the price surge

of the past two weeks was broad-based.

The second of the following

charts shows the performance of the SPX in euro terms (SPX/euro).

The difference between the two charts is stark. Whereas the nominal SPX

was in a strong and consistent upward trend over the past 12 months,

SPX/euro is no higher today than it was in early-March of last year.

The implication is that what we've witnessed since early-March of 2017

is primarily a reaction to US$ weakness. This is the case for most of the

major asset markets, not just the US stock market.

We are expecting a significant (>5%) short-term correction to occur

during the first quarter of this year, but the correction obviously hasn't

begun yet.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Jan-15 | US markets closed for public holiday |

| Tuesday Jan-16 | No important events scheduled |

| Wednesday Jan-17 |

Industrial Production Housing Market Index TIC Report Fed's Beige Book |

| Thursday Jan-18 |

Housing Starts Philadelphia Fed Business Outlook Survey |

| Friday Jan-19 | Consumer Sentiment |

Gold and the Dollar

Platinum

Platinum has channel resistance and

'round number' resistance at $1000. Above that there is important lateral

resistance at $1025-$1050.

It is currently short-term 'overbought'

and testing the lower of the aforementioned resistance areas. We expect a

multi-week price peak at around this level or following a near-term spike

to $1025-$1050.

Gold Stocks

Current

Market Situation

A week ago we wrote to expect a 1-2 week

correction in the gold-mining sector that would take the HUI down to the

vicinity of its 50-day MA. Then, in last week's Interim Update we wrote

that a correction may have already come and gone, with Tuesday's touch of

lateral support at 191 marking the end. However, at that time there was

still a chance of some additional corrective activity incorporating a test

of the 50-day MA.

Due to Friday's rise to a new 2-month high we now

know that a minor correction did, indeed, end last Tuesday.

With

regard to the coming week we have no expectations other than we don't

expect the HUI to trade below last week's low. With regard to the next

month or so, a test of resistance at 220 is likely. The 220 level acted as

a ceiling throughout last year, so how the HUI performs when it reaches

220 will be informative.

The First Majestic Silver takeover of

Primero Mining

Primero Mining (P.TO) encountered major

problems at its flagship San Dimas gold-silver mine (Mexico) over the past

couple of years, leading to desperate sales of some non-core assets and a

near-death experience over the past 6 months. However, the company has

been rescued via an agreed takeover bid by First Majestic (FR.TO). The

announcement of this bid on Friday resulted in a 125% increase in the

price of P shares, although the following chart makes it clear that only

recent buyers of the shares could have profited.

Given that San Dimas had gold-equivalent production of about 85K

ounces over the past 12 months and that P's post-bid market cap is only

C$52M, on the surface it seems that FR is getting the San Dimas mine at a

bargain price. However, taking into account P's net debt and the amount

that FR will pay to Wheaton Precious Metals to restructure the San Dimas

streaming deal, the total cost of the purchase will be about $320M. This

seems like a very high price to pay for a troubled 85K-oz/yr mine that

will be subject to a streaming arrangement that limits the gold sale price

to $600/oz on 25% of production.

Prior to this deal FR was a

leveraged play on silver that was only good for the occasional short-term

or intermediate-term trade. That's still the case, although the risk is

now higher.

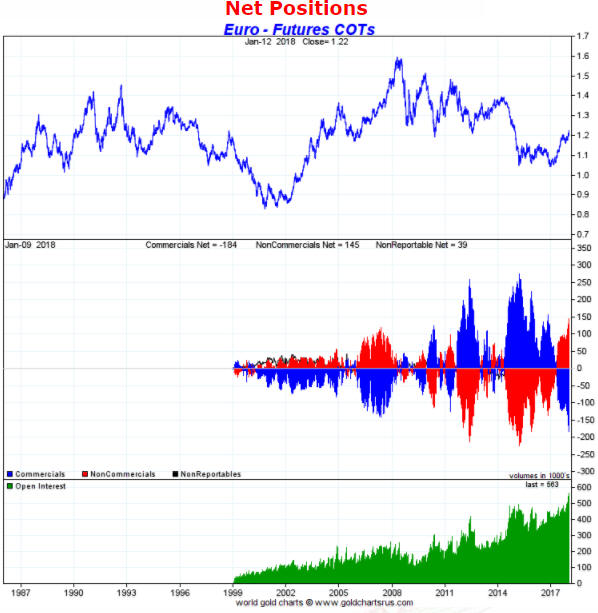

The Currency Market

Last week,

the intensity of speculative betting on a rising euro continued to ramp

up. The result was a large rise in the total speculative net-long position

in euro futures to another new all-time high and a new high for the open

interest in euro futures. Refer to the following long-term weekly chart

for additional details.

The rapidly-increasing speculative enthusiasm for the euro and the

rising price are self-reinforcing, in that trend-following speculators are

ramping up their bullish exposure in reaction to higher prices and the

speculative buying is fueling the price rise. We know how this ends, but

don't know when.

The speculator-driven rise in the euro to a new

multi-year high broke the Dollar Index (DX) below support defined by its

September-2017 low (refer to the chart below). Unless this breakdown is

painted as false by a reversal within the next few days then a 2-3 week

steep additional decline in the DX may be in store.

We don't have

an opinion on whether it's more likely that last week's breakout will be

quickly reversed or lead to significant additional movement in the

direction of the breakout (down for the DX, up for the euro). However, it

makes sense to assume that the breakout is genuine/sustainable until

proved otherwise.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 12th January 2018:

Company

news/developments for the week ending Friday 12th January 2018:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery,

MD&A = Management Discussion and Analysis, M&I = Measured and Indicated,

NAV = Net Asset Value, NPV(X%) = Net Present Value using a discount rate

of X%, P&P = Proven and Probable, PEA = Preliminary Economic Assessment,

PFS = Pre-Feasibility Study]

*Alio Gold (ALO)

reported December-quarter gold production of 16K ounces from its San

Francisco mine in Mexico. This was a poor result, but it was in line with

the guidance provided by the company about two months ago.

We

expect that ALO will have positive news-flow during the first half of this

year. In particular, the company should be able to report a much improved

production performance from the San Francisco mine in each of the first

two quarters and good news in the form of the FS for the Ana Paula project

in the second quarter.

Completion of the Ana Paula FS could turn

ALO into a takeover target.

*Premier Gold (PG.TO)

announced positive news that the stock market ignored. The news is that PG

has done a deal with Barrick Gold (ABX) that entails the major gold

producer spending US$22.5M by June-2022 to earn a 60% interest in the

exploration portion of PG's McCoy-Cove gold project in Nevada. PG will

retain 100% ownership of the deposits hosting the project's existing

high-grade resource.

This deal suggests that ABX's management sees

a lot more value in McCoy-Cove than the stock market is presently giving

PG credit for.

The first look at the economics of McCoy-Cove will

come via a PEA that was originally scheduled to be complete by the end of

last year and is now expected by the end of this year's first quarter.

After that, PG will extract a bulk sample of up to 120K tonnes from its

100%-owned portion of the project that will be processed by ABX for an

agreed price.

*Ramelius Resources (RMS.AX)

reported an above-plan production result for the December quarter. The

company produced a record-high 58K ounces during the quarter from its

operations in Western Australia, or about 3K ounces more than the top end

of its guidance range. The newly-acquired Edna May mine contributed 21K

ounces, which was roughly as expected, while the Mt Magnet operations

delivered better-than-expected output.

Production costs and most

other financial details won't be known until the half-yearly report is

published in February, but the press release issued last week noted that

the company had A$61.8M cash on hand after paying $38M for Edna May and

spending $13.2M on capital development during the quarter.

This is

good news. It confirms that RMS has substantial valuation-related upside

potential.

We think that RMS is worth at least A$0.80/share at the

current gold price.

*US Gold (USAU)

announced the results of an updated PEA for its Copper King gold-copper

project in Wyoming. Here are the salient numbers:

- Average

annual production of 41K ounces of gold plus 11M pounds of copper over a

17-year mine life

- Pre-production capex of US$114M

- M&I resource comprising 966K ounces of gold plus 235M pounds of copper

- After tax NPV(5%) and IRR of US$162M and 29.7%, resp., at a

gold price of $1275/oz and a copper price of $2.80/pound

The above

numbers suggest that the Copper King project would be economically robust

at today's metal prices. Copper King underpins USAU's market cap, but it

isn't the main source of the stock's upside potential.

The bulk of

USAU's reward potential is associated with the Keystone project in Nevada.

This project is at a very early stage of exploration, with only scout

drilling having been done to date. The results of the first few scout

holes are expected during the second half of this month.

USAU has

rebounded strongly from its November low near US$1.00. This is not

surprising, because as we mentioned at the time the plunge to the low-US$1

area on no news was another in a long line of examples of the stock market

being wrong.

Despite the strong rebound, the stock is still not

expensive. With only 14.3M shares outstanding the market cap is about

US$40M, which is more than fully justified by the Copper King project.

This suggests that buyers near the current price aren't paying anything

for the upside potential associated with Keystone.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI

stock selections the best candidates for new buying at this time, listed

in alphabetical order, are:

1) ALK.AX (last Friday's closing price:

A$0.335)

2) ALO (last Friday's closing price: US$3.64)

3)

EGD.V (last Friday's closing price: C$0.36)

4) NSU (last Friday's

closing price: US$2.39)

5) PG.TO (last Friday's closing price:

C$3.53)

The above list is limited to five stocks. It will sometimes

contain less than five, but it will never contain more than five

regardless of how many stocks are attractively priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.goldchartsrus.com/

http://www.lme.com/