![]()

![]()

![]()

![]()

-- Weekly Market Update for 15th July 2019

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bullish (04 Jan 2019) |

| US Equity (SPX) | Bearish (19 Apr 2019) |

| Currency (Dollar Index) | Neutral (15 Mar 2019) |

| Commodities (GNX) | Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

Gold and Inflation Expectations

Summary of current

thinking/positioning

1) The Dollar Index (DX) has

commenced a downward trend, but it could be a few months before the new

trend becomes consistent. In the meantime the price action could be

choppy, possibly involving a test of the June high near 98.

2) The

US$ gold price has broken out to the upside on a monthly basis.

Significant additional gains are likely within the next three months --

after the current correction has run its course. The US$ silver price

stands a good chance of making a catch-up move over the months ahead.

3) The gold-mining indices/ETFs became extremely 'overbought' late

last month and have since been in correction mode. The correction may or

may not be over, but either way there probably will be additional gains

within the coming two months.

4) The SPX probably will commence a

sizable multi-week decline soon.

5) An upside blow-off has set the

stage for a large T-Bond decline. The decline probably began on Friday 5th

July, although it could be September-October before the market starts

trending downward with conviction.

6) Oil's correction is probably

over, although there is still a risk that stock market weakness during

July-August will push the oil price to a new multi-month low.

7) We

are holding a cash reserve of 25%-30%.

A reversal in the

Treasury market

We now have evidence that a top

of at least short-term importance is in place for the prices of long-dated

US Treasury securities. The evidence is last Thursday's break by the 20+

Year Treasury ETF (TLT) below the bottom of the price channel that formed

over the preceding 6 weeks.

We think that TLT will trade a lot lower before year-end in response

to expectations for higher "inflation" and a rapid increase in government

debt supply, but other than expecting the early-July high to remain the

high for the year we don't have a firm opinion regarding performance over

the next two months. One realistic short-term possibility is a topping

process involving a multi-week low before the end of this month followed

by a rebound to a lower high over the ensuing few weeks.

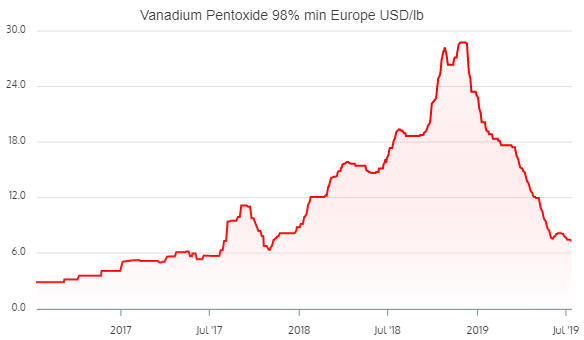

Commodities

Vanadium extends its

downward trend

Our most recent comment on vanadium was in

the 17th June Weekly Update, at which time the price had just bounced

following a major decline. We wrote:

"Our guess is that the

industrial demand for vanadium will increase over the next six months due

to the rebuilding of stockpiles that were drawn down over the past six

months and new Chinese rebar standards coming into full effect. This

should result in an upward bias in the price, but not the sort of

spectacular rally that occurred in 2018."

Our vanadium outlook

is unchanged. However, the following chart shows that the vanadium

pentoxide price in Europe made a new 18-month low last week, so the

anticipated upward bias hasn't commenced yet.

The Palladium bubble is intact

From the 1st

April Weekly Update:

"As ridiculously expensive as palladium

appears to be relative to other metals, most notably platinum, the decline

from the mid-March peak is more likely to be the start of a multi-month

correction than the start of a bubble collapse."

And from the

6th May Weekly Update:

"It's possible that the sharp decline in

the palladium price from its March-2019 high marked the bursting of the

bubble, but as mentioned in the 1st April Weekly Update it's more likely

that the decline is the start of a multi-month correction. This is based

on a comparison with the palladium rally of 1997-2000 and the fact that

the end of the first parabolic move in a cyclical advance generally

doesn't mark the end of the cycle.

If we are dealing with a

multi-month correction rather than the start of a bubble collapse then the

palladium price should not give a weekly close below its 50-week MA (the

blue line on the following chart)."

Our view that the sharp

decline in the palladium price from its March-2019 peak was probably the

start of a multi-month correction rather than the start of a bubble

collapse was correct, because over the past week the metal traded at a new

all-time high.

Palladium is in a bubble, but the bubble is not yet

fully inflated.

Despite the potential for another parabolic rally in the palladium

price over the months ahead, we are not the slightest bit interested in

buying palladium at its current stratospheric valuation. However, we would

buy platinum in anticipation of at least a partial catch-up move. Platinum

has a vastly superior risk/reward.

Platinum is still

relatively weak

The platinum price remains near an

all-time low in gold terms and not far from a 10-year low in US$ terms. We

suspect that in US$ terms it is 'coiling' in preparation for a large

advance, although the chart pattern (see below) leaves open the

possibility that last year's low will be tested prior to the start of such

an advance.

A weekly close above US$920 would confirm that the

expected large advance had begun.

More evidence of a correction low in the oil price

Last week the oil market added to the evidence that its correction

ended during the first half of last month. It did so by closing above its

early-July high, a short-term trend-line drawn from the April peak and its

50-day and 200-day MAs.

The big test for oil will occur during the

US stock market's next meaningful decline, because there is still a strong

positive correlation between the oil price and the SPX.

The Stock Market

Current US Market

Situation

Last week the S&P500 Index (SPX), the NASDAQ100

Index (NDX) and the Dow Industrials Index (Dow) all broke into new

all-time high territory on a weekly closing basis. Refer to the following

weekly charts for the details. Also, the new highs were confirmed by the

NYSE Advance-Decline Line (ADL). This is evidence that the bull market is

intact, but it doesn't provide any information about the market's likely

path over the coming 1-2 months.

As well as breaching previous highs, last week's closes in the SPX and

the Dow were above big round numbers: 3,000 for the SPX and 27,000 for the

Dow. Also, the NDX ended the week within spitting distance of a big round

number of its own (8,000).

Getting to these big round numbers

generates headlines in the press, but otherwise doesn't mean much for

investors. Also, as is the case with the upside breakouts it doesn't

provide any information about the market's likely path over the coming 1-2

months.

Based on sentiment and cycles, we continue to expect a

significant multi-week decline. However, for risk management purposes we

would exit short-term bearish speculations if the SPX were to make a new

high after this week.

The monetary inflation headwind

The year-over-year rate of growth in US True Money Supply (TMS) made a

new cycle low in June-2019 and is not far from its 20-year low. The

relevant monthly chart is displayed below.

This means that the

money-supply situation constitutes a steadily increasing headwind. Note,

though, that the cyclical equity bull market of 2003-2007 didn't die until

about 12 months after the TMS growth rate plumbed a similar level in

September-2006. This simply means that the monetary inflation rate is not

a good short-term or intermediate-term stock-market timing indicator.

Time to bet against Tesla?

In the 10th June

Weekly Update we wrote that almost regardless of what happens to the US

stock market, Tesla (TSLA) probably is on the road to extinction. We

thought that TSLA would be a good candidate for a bearish speculation if

the stock price were to rebound to around $240 (it was trading at $204 at

the time).

The following chart shows that TSLA has since rebounded

to the $240s and that the rebound is a test of the May-2019 downside

breakout. If you are interested in betting against this over-priced,

cash-consuming, debt-laden company, now would be a reasonable time to do

so.

Note that betting against TSLA is not a trade that we will be

doing in the near future, but only because right now we are involved in

more than enough different speculations.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Jul-15 | No important events scheduled |

| Tuesday Jul-16 |

Retail Sales Industrial Production Business Inventories |

| Wednesday Jul-17 |

Housing Starts Fed's Beige Book |

| Thursday Jul-18 | Leading Economic Indicators |

| Friday Jul-19 | Consumer Sentiment |

Gold and the Dollar

The 1980s comparison discussed above suggests that the HUI's breakout

will prove to be sustainable, in which case it will be confirmed by

related prices this week. However, it isn't reasonable to blindly assume

that over the next several weeks the gold-mining sector will mimic the

near-vertical ascent of March-April 1987. It possibly will, but additional

corrective action of sufficient magnitude or duration to push the daily

RSI(14) down to around 50 is required to create a new short-term buying

opportunity for the popular mining ETFs.

Unlike the gold-mining

sector, the silver market is not remotely close to being 'overbought'.

Consequently, for new buying at this time we prefer silver bullion to the

mining ETFs.

The Currency Market

Last

Tuesday the Dollar Index (DX) tested lateral resistance at 97.2 and

managed to close above its 50-day MA for the first time since early-June.

It then dropped over the remainder of the week. The catalyst for the

pullback was the non-subtle hint of easier US monetary policy in testimony

delivered by the Fed Chairman on Wednesday.

The Wednesday-Friday

pullback took the DX from lateral resistance at 97.2 to moving-average

support at 96.4.

It's possible that the DX's rebound from its June low ended last

Tuesday, but an extension of the rebound is also a realistic possibility.

Either way, we are anticipating significant weakness in the DX over the

next several months.

Future US$ weakness has been signaled by the

gold market and by the recent performances of the Swiss Franc, the Yen and

the Canadian dollar. Also, future US weakness meshes with how we see the

fundamental backdrop developing over the months ahead, although we hasten

to point out that the true fundamentals are US$-neutral at this time.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 12th July 2019:

Company

news/developments for the week ending Friday 12th July 2019:

[Note: AISC = All-In Sustaining Cost, EBITDA = Earnings Before

Interest, Tax, Depreciation and Amortisation (a measure of cash flow), EV

= Enterprise Value or Electric Vehicle, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, JV

= Joint Venture, MD&A = Management Discussion and Analysis, M&I = Measured

and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value using a

discount rate of X%, NSR = Net Smelter Return or Net Smelter Royalty, P&P

= Proven and Probable, PEA = Preliminary Economic Assessment, PFS =

Pre-Feasibility Study]

*Alkane Resources (ALK.AX)

published its quarterly report for the June-2019 quarter (the final

quarter of FY2019). After another above-plan quarterly performance from

the Tomingley Gold Operation (TGO), gold production for the full financial

year was 49K ounces. This was at the top of the upwardly-revised guidance

range and about 60% above the original guidance. In other words, the TGO

performed very well in FY2019.

Production guidance for FY2020 (the

financial year ending 30th June 2020) is 27K-32K ounces of gold at an AISC

of A$1300-$1450. Note: The current A$ gold price is around $2000/oz.

The Tomingley open pit is depleted and the current production is

solely from the processing of stockpiles. That's why the amount of gold

produced has been trending downward. However, the life of the operation

has been extended by the construction of an underground mine that is

scheduled to go into production during the March quarter of 2020. Also,

exploration results indicate the potential to establish a new pit within a

few kilometres of the existing plant.

With regard to the Dubbo

specialty metals project, which is where the bulk of ALK's value and

upside potential lies, the company's efforts to arrange financing and

offtake agreements are on-going.

ALK has a strong balance sheet,

with no debt and cash, bullion plus listed investments of about A$81M.

This figure is roughly the same as it was 6 months ago.

*Alliance

Mineral Assets (A40.AX) reported June-quarter lithium concentrate

production from its Bald Hill mine that was roughly the same as the March

quarter, enabling the company to achieve a production result for the first

half of CY2019 that was close to the top of its guidance range.

Specifically, during the first half of this calendar year A40 produced

78,937wmt (wet metric tonnes) of 6.0% Li2O-equivalent versus guidance of

65,000-80,000 wmt. This constitutes a solid production performance,

although production costs won't be known until the end of this month and

the complete financial picture won't be known until the annual financial

report is published in September.

Production for the next 6 months

is expected to be similar to production over the past 6 months.

We

are comfortable with the way A40 is performing on the ground, but like all

lithium producers the company is struggling against market headwinds in

the form of a downward trending lithium price. There's a high probability

that it eventually will be taken over by either Galaxy Resources (GXY.AX)

or Mineral Resources (MIN.AX), two companies that have lithium mines in

the same part of Western Australia as A40's Bald Hill project, but

hopefully the takeover will happen during a more bullish period for

lithium miners.

*eCobalt Solutions (ECS.V)

will hold a shareholders meeting on 19th July to vote on the proposed

merger with Jervois Mining (JRV.AX, JRV.V). If the merger is approved then

each ECS share will be exchanged for 1.65 JRV shares. Based on JRV's

current price of A$0.20 on the ASX and the current A$/C$ exchange rate,

the merger values ECS at around C$0.30/share.

We added ECS to the

TSI List as an intermediate-term trading position primarily due to the

stock's discount to the implied value of the JRV merger proposal. Also,

our view is that combining the two companies is in the best interest of

both ECS and JRV, so we think that shareholders should vote in favour of

the merger.

First Cobalt (FCC.V), the holder of a 6% stake in ECS,

has been sending out letters advising ECS shareholders to vote against the

merger. FCC obtained its ECS stake via a share swap with a third party

AFTER the proposed ECS-JRV merger was announced, for reasons that aren't

clear to us.

Note that FCC does not have significant financial

resources (the company had minimal working capital at 31st March and

probably has negative working capital right now) and therefore is not in a

position to make a positive contribution to ECS. JRV, on the other hand,

has about A$20M of working capital and is positioned to advance projects

in Australia and Africa in addition to the Idaho-based project currently

owned by ECS.

*Cobalt 27 Capital (KBLT.V)

is subject to a takeover bid from Pala Investments, its largest

shareholder. In the 19th June Interim Update we wrote that the bid was not

even remotely close to full value.

In June-2018 KBLT purchased from

Vale, at a cost of US$300M, a "stream" that entitles it to cobalt

production from the Voisey's Bay (VB) nickel mine in Canada beginning on

1st January 2021. The stream entitles KBLT to 32.6% of the cobalt

production from VB until 23.8M pounds have been delivered and 16.3%

thereafter. The timing of this purchase was inopportune to put it mildly,

as the cobalt price has subsequently crashed from US$35/pound to only

US$12/pound. However, by selling now the senior managers of KBLT would be

compounding their error. Having bought near a major high they would be

selling near what very likely will turn out to be a major low.

Furthermore, since production linked to the VB project doesn't commence

until 2021, the current price of cobalt is not relevant. What really

matters is what the cobalt price will be from 2021 onwards. By then it

could well be where it was in early 2018 or even higher.

All of

which raises the question: Why is KBLT's management supporting the Pala

takeover bid? After all, the company has a strong balance sheet and

therefore is not under financial pressure to dump high quality assets at

fire-sale prices.

A possible answer to the above question was

mentioned in the detailed and scathing response to the proposed takeover

provided by Anson Funds, a large KBLT shareholder. The full response, with

which we are in total agreement, can be read

HERE.

Anson notes that if the takeover is successful then

KBLT's existing managers will receive change of control payments and will

manage the spin-out company to be called "Nickel 28". In other words, they

will receive financial bonuses and will continue to draw their salaries.

Fortunately, minority shareholders will have an opportunity to vote

against this nonsensical takeover, and thus prevent it from happening, at

a future shareholders meeting.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI

stock selections the best candidates for new buying at this time, listed

in alphabetical order, are:

1) AAU in the low-US$0.60s (last

Friday's closing price: US$0.65)

2) CGT.TO (last Friday's closing

price: C$0.18)

3) ECS.V (last Friday's closing price: C$0.21)

4) PEY.TO (last Friday's closing price: C$4.01)

5) PG.TO near

C$2.00 (last Friday's closing price: C$2.06)

The above list is

limited to five stocks. It sometimes will contain less than five, but it

never will contain more than five regardless of how many stocks are

attractively priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

http://www.goldchartsrus.com/

https://www.vanadiumprice.com/