|

-- for the Week Commencing 15th December 2003, 2nd Page

Bonds and

Oil

The bond market sets long-term interest

rates while the Fed controls interest rates at the short end of the curve.

Also, the behaviour of the Fed effects the bond market and the behaviour

of the bond market influences the Fed. For example, if the Fed's monetary

policy is perceived to be too 'easy' then the bond market will begin to

move long-term interest rates higher in anticipation of an inflation problem.

After long-term interest rates have moved higher for a while the Fed usually

gets the message and begins to tighten its monetary policy. As things currently

stand, Greenspan and Co. have expressed a desire to hold the official short-term

interest rate at low levels for a considerable period. But whether or not

they will actually be able to do so will be determined by the behaviour

of the bond market.

Bonds peaked in June, crashed into

an August low, and have since recovered about one-third of their losses.

Our view is that the post-August recovery is a consolidation within a continuing

downward trend, that is, we expect that the next big move will be to the

downside. The below chart shows this consolidation pattern and what we

consider to be the most important short-term support and resistance levels.

A break below the higher of the two support levels shown on the chart (around

105.50) would strongly suggest that our view was correct and would set

the stage for a series of rate hikes by the Fed, while a break above the

resistance level shown on the chart would suggest that something other

than our expected scenario was playing out.

Our interest-rate view received a figurative

kick in the teeth at the end of last week when the oil price broke out

to the upside (see chart below). This is because bonds have, over the past

two years, been following oil with a lag of 3-4 months (refer to the 24th

November Weekly Update for an explanation). In other words, if last Friday's

breakout in oil 'sticks' then we should expect bonds to break upwards out

of their consolidation pattern in March-April of next year.

It is not uncommon for a market to

break above an obvious resistance level only to reverse lower a short time

later. Therefore, to confirm that any breakout is 'real' (sustainable)

we always like to see some follow-through. In oil's case, remaining above

$32.50 (basis the January contract) over the next two weeks would do the

trick. If this happens we would need to re-think our forecasts for long-term

and short-term interest rates.

We speculated, in the aforementioned

commentary, that the reason for the strong positive correlation between

the oil and bond markets over the past 2 years has been that geopolitics

has been the primary driver of the oil price. So, would the positive correlation

remain in effect if the oil price were driven higher by something other

than, for example, instability in an oil-producing region? After all, a

higher oil price could quite easily be explained by a combination of a

weakening US$, Chinese demand, and weather-related concerns.

In the current environment the positive

correlation between oil and bonds probably would remain in effect due to

the falling money-supply growth trend. Let's explain.

A rising oil price is not inflationary

because only money-supply growth can, by definition, be inflationary. Furthermore,

a rising oil price cannot cause the general price level to increase.

In the past, a rising oil price has

often been accompanied by an increase in the general price level. But this

was only possible because the total supply of money was increasing at a

fast enough rate to enable a price rise in one part of the economy (for

example, the energy sector) to push prices upward throughout the economy.

However, in an economy where the total supply of money is constant it is

axiomatic that a price increase somewhere in the economy will be offset

be a price decrease somewhere else.

Another way of saying the above is

that a rising oil price can only appear to have an inflationary effect

if the Fed monetises the price rise. At the present time, though, the money-supply

growth rate is trending strongly lower so the ability of the Fed to monetise

a rise in the price of oil is doubtful. Therefore, the bond market's initial

reaction to a sharp rise in the oil price would probably be a negative

one, but a sharp rise in the oil price at this time would likely have longer-term

bullish implications for bonds.

The bottom line is that the downward

trend in the money-supply growth rate is going to loom even larger if last

week's upside breakout in the oil price 'sticks'.

Natural

Gas

Below is a weekly chart of natural

gas (NG) futures. For the third time since 2000 the NG price is spiking

sharply higher during the December-February period.

The stock market's reaction to the

rising NG price has been subdued. For example, over the past 4 weeks the

NG price has gained 57% while the AMEX Natural Gas Index (XNG) has risen

by 9% and Chesapeake Energy (NYSE: CHK) -- a gas producer with substantial

leverage to the NG price -- has risen by 10%. A gain of 10% in 4 weeks

is not something to be sneezed at, but this gain is in line with the general

increase in commodity-related equities over the same period (the Morgan

Stanley Index of Commodity-Related Equities is up by 7.4% over the past

4 weeks). It seems, therefore, that the stock market expects this latest

spike to end the same way as the previous two.

We like the longer-term fundamentals

for the natural gas sector and expect that a large stock-market decline

over the coming year will create a very good buying opportunity for these

stocks.

Gold and

the Dollar

Yield-Spread Update

When long-term interest rates are rising

relative to short-term interest rates it is bullish for gold, and, even

more so, for gold stocks. As the below chart shows, the yield-spread (the

30-year interest rate divided by the 13-week interest rate) has been consolidating

over the past few months but is still close to its highs. This continues

to be a bullish factor for the gold market.

The Commitments of Traders (COT)

Report

The latest COT data are very bullish

for the US$ and are therefore consistent with the idea that the dollar

is close to a short-term bottom. The data, however, are not so lopsided

as to indicate that anything more significant than a 1-2 month dollar rally

is on the cards. That would change, though, if a downward spike in the

Dollar Index to around the 85 level were accompanied by aggressive buying

on the part of commercial traders. In this case a much longer dollar rebound

would likely occur. In other words; if a US$ rebound begins from near the

current level then we would look for it to last 1-2 months, but if the

dollar first drops another 4% or so then the ensuing rebound would likely

be much longer (3-6 months).

The COT data for gold indicate the

potential for additional price gains. We say this because the small traders

-- the 'dumb money' -- have a net-long position that is about 14,000 contracts

smaller than it was in early February despite the fact that the gold price

is now about $30 higher. In other words, the 'dumb money' is now less bullish

than it was it February despite the improved performance of the gold price.

The COT data suggest that gold is either

going to move sharply higher now, or consolidate for a while (in parallel

with a US$ rebound?) before moving sharply higher.

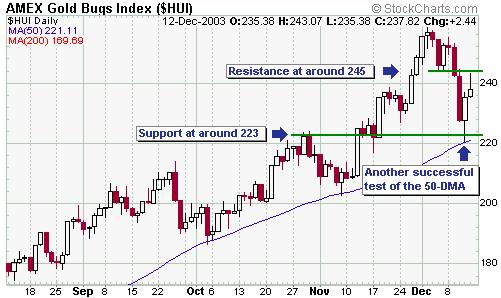

Gold Stocks

The Dow Industrials Index and the S&P500

Index hit new recovery highs at the end of last week, suggesting that gold

stocks are still a few weeks or more from a peak (since gold stocks aren't

likely to peak until some time after the broad market peaks). Last Thursday's

price action, with the HUI dropping sharply to test its 50-day moving average

and then rebounding (see chart below), is consistent with the view that

new highs will be seen over the coming months.

Last Thursday's upward reversal in

the gold sector doesn't mean that the correction is complete. The HUI has

some minor resistance at around 245 and on Friday it reversed lower from

just below this resistance. A daily close above 245 would suggest that

a move to a new high was underway.

By the way, investors in gold stocks

should consider the action over the past two weeks to be a warning shot.

Note, in particular, that the 15% decline in the HUI from its 2nd December

intra-day peak to its 11th December intra-day bottom occurred concurrently

with a marginal INCREASE in the gold price. Based on all the historical

data we have reviewed we expect that the HUI's next intermediate-term peak

will be followed by a fall of 40% or more in the space of 2 months and

that this fall will likely occur in parallel with a rising gold price.

Update

on Stock Selections

We

added Plum Creek Timber (NYSE: PCL) to the Stocks List in early November

and since that time the stock price has gained 11% and the company has

paid a 35c dividend. PCL is one way for conservative investors -- people

who might be put off by the huge volatility in many of our junior resource

stocks -- to play the bull market in commodities. Timber is actually one

of the safest and best long-term investments because depletion isn't a

problem (assuming the resource is well managed) and it grows (literally). We

added Plum Creek Timber (NYSE: PCL) to the Stocks List in early November

and since that time the stock price has gained 11% and the company has

paid a 35c dividend. PCL is one way for conservative investors -- people

who might be put off by the huge volatility in many of our junior resource

stocks -- to play the bull market in commodities. Timber is actually one

of the safest and best long-term investments because depletion isn't a

problem (assuming the resource is well managed) and it grows (literally).

In the short-term there's a good chance

that the PCL stock price will pullback because it has just moved up to

a level at which substantial resistance will probably be encountered (see

chart below). It would, however, be a low-risk buy on a drop to around

27.50. We expect that PCL will trade up to $40 within the next 18 months.

Argentine

agricultural company Cresud (NASDAQ: CRESY) is another reasonably conservative

commodity play, although the stock price has been quite volatile over the

past two months. CRESY, we think, will benefit from the fact that there

are very few ways for stock market investors to gain exposure to grains

and cattle.

We think CRESY is a 'hold' at Friday's

closing price of $13.85 and would be suitable for new buying below $11.

As

mentioned earlier in today's commentary, a position in USPIX (ProFunds

UltraShort OTC Fund) has been added to the Stocks List. USPIX is quite

risky, but it does have two significant advantages over put options. First,

time decay is not a problem with USPIX as it is with any out-of-the-money

option (all else being equal, the market value of an option will fall over

time). Second, active risk management -- for example, making an exit if

the market moves against you -- is more feasible with an inverse fund such

as USPIX than it is with an option (if you buy an option that is well out

of the money, by the time you realise you've made a mistake there probably

won't be much value left to salvage).

Metallica

Resources (AMEX: MRB) has completed a major equity financing. It now has

C$85M in cash and therefore has more than enough money to take its Cerro

San Pedro project -- a gold/silver project in Mexico -- through to production.

Cerro San Pedro is scheduled to be in production by the end of next year

and is forecast to produce 120,000 gold-equivalent ounces per year.

In addition to Cerro San Pedro MRB

owns the El Morro porphyry copper-gold project in Chile (Noranda has a

right to earn a 70% interest in this project). El Morro has an inferred

resource of 6.2B pounds copper and 7.4M ounces gold and provides some 'blue

sky' potential for MRB shareholders.

With the financing out of the way MRB

is a lower risk speculation and is suitable for new buying at around US$1.50.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.futuresource.com/

|